New Zealand has the disadvantage of not having any current data for the number of new houses built.

This sort of data is fundamental to policy decisions and is available in almost all other countries.

But for some reason, probably related to the way our fragmented house-building industry is structured, there is no easy way to collect this data.

And new houses are rarely sold through licensed real estate agents. Certainly, privately contracted new house builds don't need an agent.

The Council's 'Certificate of Practical Completion' is a data source unused, but that comes with delay issues again (not to mention, no one is collecting this data). Most housing is built and lived in many months or even years before this paperwork is finalised.

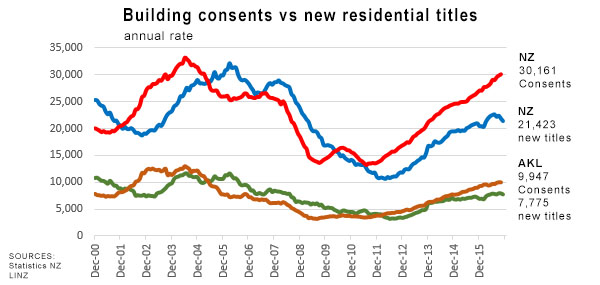

So we rely on 'building consents' as a proxy for how much new housing is added to our housing stock.

But as most of us know, building consent data is a poor indicator. Some consented dwellings may actually never be build, or it could be constructed any time in the next two years, and all sorts of variations can happen if it does go into construction.

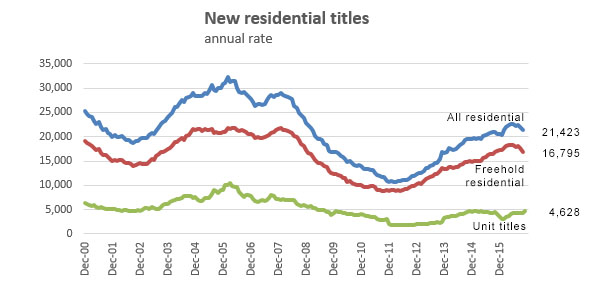

So we have taken a detailed look at an alternative series - the land title data at LINZ.

This has its own issues, but they may be easier to deal with than the consent numbers.

Firstly, when a title is first registered, the Council will start assessing residential rates. The pressure is on to build and sell. But occupation of residents could still be many months away.

In the case of unit titles, however, the impact is more immediate. Unit titles generally aren't issued until the dwelling is ready for occupation and after the building is completed. These are very good indicators of new dwelling availability.

There are many classes of new property titles and we are just focused on two of them here; residential freehold, and residential unit titles. (We may look at other types at some point in the future.)

The overview (to November 2016) shows a new and marked decline in freehold titles being issued. This is almost all due to the sharp slowdown in new building in Christchurch.

The other feature of this national overview is what is not there - any growth in unit titles. Nationally, these are still running at just half the rate we saw a decade ago.

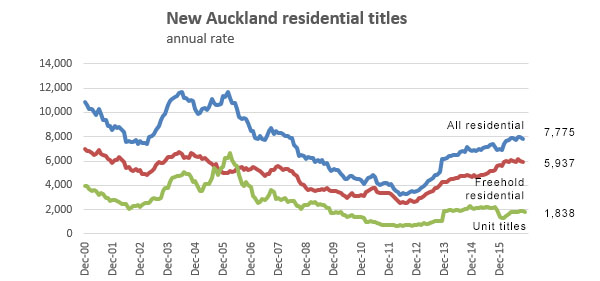

The languishing of new unit title residences is even more marked in Auckland. This is surprising given the housing pressures there.

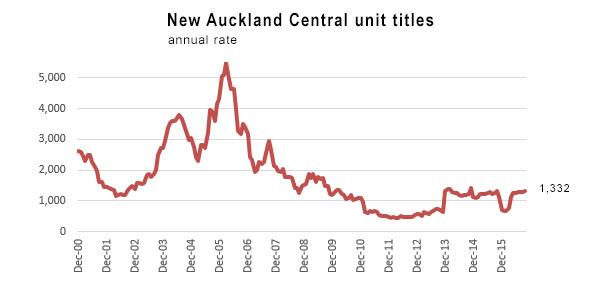

The 2005-2006 boom was driven by aggressive development of shoe-box apartment living, and even tinier 'student accommodation'. That period has passed and the reviews of such development have not been kindly received. The new demand is for more upmarket units and the volumes of these are much less. This is not something developers mind as these newer, larger units are undoubtedly more profitable. And given the boom in non-residential construction, there is not the capacity to repeat the 2005-06 volumes. Nor is there planning tolerance for such construction. But that means far fewer units are coming on to the market, and most that do are out of reach of those on modest incomes.

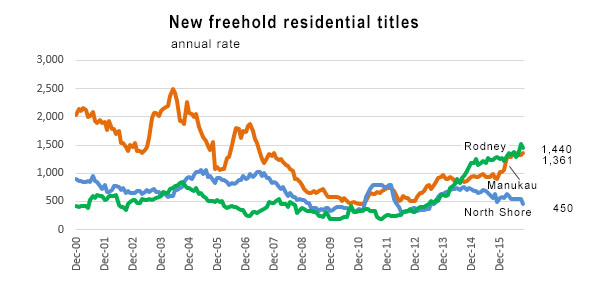

Drilling in to the data further, it is clear that far fewer unit title dwellings are being built on the North Shore. From 2003-2006 these averaged 425 per year in that city zone, but today that is down to just 150.

But nothing compares with the 5,000 annual average reached in central Auckland in 2005 - and that is now down to just over 1,300. That is a lot of 'missing' dwellings.

For freehold dwellings, we can see that development is ramping up in the north (Rodney) and south (Manukau) of the Auckland Council area, both imposing long commutes for those that choose to work in the central City. But of course, most people don't do that. The other feature is how weak new freehold title registration is on the North Shore. And not shown on this chart is the atrophying of the numbers for the central isthmus area.

Given that Auckland seems to need at least 13,000 new dwellings per year, none of this data suggests the Council is about to get anywhere near these levels, despite what the building consent data shows.

Just how different this 'new title' data is from the building consent data is easily seen in this chart:

An eye-opening feature of this comparison is that for five years - 2011 to 2016 - new titles issued for residential land and units have been running at least 5,000 lower per year than the consents being issued. By the end of that period, this difference is up to almost 10,000. Why is that?

Please note that this data is indicative only. There will be some housing included in the consent data that is not in residential title data we have selected, such as houses built on new lifestyle block titles, for example. Housing built on new cross-leasing or leasehold titles are not included here either. So that will be some of the answer. But the difference remains large.

What we really need is an official monthly survey, by local authority, of new housing added to the real estate market. Until that happens, we will have to rely on these inadequate proxies, which draw us into too much wasted effort trying to reconcile them. Time for MBIE, Councils, and the residential building industry to sort this out so that better public policy decisions can be made.

25 Comments

when ovelay the population of the same period you can see whilst one increases 20% the building rate does not.

this is a failure of the last two governments to match and enable both to grow at the same speed

It's more of a failure to not encourage enough of the current population in Auckland & recent immigrants to move to the regions where populations are on the decline becoming ghost towns.

Auckland's share of the NZ population is only going to get even bigger in the future due to inaction of not making other parts of New Zealand more attractive.

a discussion i had today with an immigrant is how great auckland is at the moment as it is quiet being half empty almost like when i grew up, easy to get around no crowds,

her response (been here for ten years) oh its boring too quiet, not enough people around we need more people like big overseas cities

i guess that translates to those that come here expect it to change to match where they come from so they feel more at home

whereas some of us want it to be more space and less people

..dude they left for a reason. Its called jobs.

no 1/2 off auckland are busy infesting the regions on holiday, giving them a taste of being crowded out, traffic etc

It is quite a risky enterprise to build or buy a brand new house in NZ currently, with a significant lack of trust by NZers in the quality of building products, workmanship with larger contracting arrangements, and financial liabilities/risk.

I would want to find a sole builder with good reputation if building - having watched my mother in law's new house with a series of technical and materials faults and shortcuts etc. still ongoing.

The way it is currently setup, is that it makes the most sense financially to build houses as cheaply as possible to the minimum standards in the building code and nz standards. Insulation is a case in point, as you can spend a bit more to upspec the insulation, which can save the home owner thousands in energy savings. But many spec houses are just done to the minimum spec. If you get a house built, it is recommended to spec and detail everything, otherwise it will likely be done the cheapest way possible. It is a good time at the moment being a building company.

It would be useful having actual data on how many are going to owner occupiers or are developers. That's not usually something that is evern collected in a buildling consent application.

As MortageBelt pointed out there are problems with a lot of new builds. I know I've had a few issues myself with one issue being expensive. Then again from what I see in the existing housing stock is a lot of deferred maintenance and other serious problems. The housing stock is mostly crap here and a liability.

Great article David. Can I suggest another another useful graph?

A graph dividing population growth by newly constructed residencies for our growth areas -Auckland, Greater Christchurch and the golden triangle -Hamilton and Tauranga etc. With a line showing the regions average home occupancy.

If we had good enough data we could show if the construction boom is greater than the immigration/population growth boom. For instance Auckland built approximately 10,000 residences in 2016 and its population grew by approximately 45,000, so that means each new home has to accommodate 4.5 new Aucklanders -on average. Auckland's overall average home occupancy is 3.0.

So currently we are not eating into Auckland's housing shortage.

NB - in the last graph - consents v titles issued - there would have to be a time gap of approximately up to 1 year between the issue of a consent and completion and issue of Title

If you shift-offset the "Title" line back by 12 months there is a distinct visual correlation for the NZ graph

Not so for the Auckland Graph

David, you state: "An eye-opening feature of this comparison is that for five years - 2011 to 2016 - new titles issued for residential land and units have been running at least 5,000 lower per year than the consents being issued"

You cannot compare building consents with titles of the same date because titles lag consents by about 18 months, this is actually nicely shown in your graph. That is the answer to your question "why is that". To make my point more obvious, look at the graph for the period 2007 to 2009, it looks like there were about 5000 more titles than consents, how could that be ? Again it's because of the lag titles have after consents are being issued (I know, I'm an Architect)

I wonder if that time lag has changed over time. People I know in the industry for 30+ years have been saying that it takes longer and longer to build in AKL. What is your experience?

Also, the title measure would be a better measure of when buildings can be occupied, right? Whereas consents are probably the best leading indicator we have of dwelling stock. Thoughts?

Good article, David. I agree with you and have to point out that better construction data is already in the hands of councils, in digital form and so could be easily collated in a few hours by Stats or MBIE if they were sufficiently motivated. We could for instance collate new starts simply by noting when a first inspection is undertaken on a project and completions would be even easier since we already have a formal step of issuing a CCC.

Just to clear up a few points:

- Not sure what you mean by a Certificate of Practical Completion. I take it you mean the Certificate of Code Compliance (which basically means a building is complete and can be occupied).

- Titles are almost always issued about the same time as building consents are issued (give or take). A council generally wouldn't issue a BC if a subdivision was incomplete but once the subdivision has received its RMA s223(4)(a) approval then it is all go. The process of getting the subdivision formally approved in a Council meeting and then submitting the survey plan to LINZ for issuance of titles can be time consuming. But RMA s225(1) allows building to commence before the formalities are complete. I would expect in an active market that consenting building and issuing titles occur about the same time although building can often precede the issuing of a title.

- Don't know for certain but if is possible to build dwellings on Maori land then there wouldn't be any related issuing of title for those either (similar to freehold and cross-leases).

- I tend to think of building consents as a good proxy for building starts just because it is so painful to get one that you wouldn't apply for one unless you were ready to start right away. The only exception is apartments. It's probably safer to assume that only 50% or so of BC's issued for apartments actually turn into dwellings.

Another thought to measure new housing completions is to use the council rating database as these are now able to be updated monthly during the rating year. What you'd look for are properties where the value of improvements increases massively indicating a new building completed, or vacant properties becoming improved properties.

Councils operate a core property database which records all the land parcels and their valuations within their territory. The rates records "hang off" the property data. I guess they load the initial valuation based on the claimed value of construction contained in the application for building consent. Otherwise they have to wait for the three-yearly cycle of valuations. And it really doesn't matter because many (most?) councils give new properties a rates holiday until the new rating year starts so rates officers may not even load the base rating data in until closer to that time.

Way safer to look at inspections.

Councils (at the least the Christchurch City Council does so) now can update during the rating year and update your rates payable within the rating year. I think there was a recent amendment to the legislation allowing this.

At cross-purposes, I think. Yes, new properties are added at any time to the property database which the public largely see as the Rating Information Database. But actual rates are only assessed from the start of the next rating year. So David is slightly off in claiming that developers must sell properties quickly to avoid increased rates but, in practice he is mostly right.

But that's all beside the point. If you want accurate and timely stats on construction starts and finishes then the Building Consents database already exists and it would be trivial to collect good data from it and collate it on a national basis.

Buyers wont look at all these graphs to make a decision.

Most buyers dont even consult a lawyer for legal advice before signing a sale and purchase agreement.

Aucklanders are simple creatures we hibernate in the winter spring and then just buy up large between February and April.

That is not what the data shows. It is 2016 that is unusual - buyers were scarce in Auckland in the usually busy Sep/Oct/Nov period. Yes, March is usually busy too, but given the unusually weak spring, you would be hard pressed to just assume March 2017 will be normal.

Alot more buyer interest mid December and during the holidays we have noticed as realestate salespeople. My prediction is a January increase in sales earlier than February as the LVR contaigon in Auckland has worn off and old stock is starting to sell.

Really Ted, if that was the case then you would be seeing a huge increase in the number of Auction sales and listings. I say one again; go look at TradeMe for Auckland and you can clearly see that there's hardly any new auction listing, they're mostly being placed as priced or Negotiation sales.

Are retirement village residential units covered in new dwellings data? If not, is there any estimate of the number? I have wondered if this growing type of accomodation causes a significant underestimate in residential units, and lead to an oversupply down the track some time.

Yes, Dave, they are.

If you check out the data published by StatsNZ they break building consents down into lots of categories. For new residential there are four categories:

- house or stand-alone dwelling

- townhouse/flats

- apartments

- retirement village units

The point David is making is that building consent data collects the number of dwellings proposed to be built regardless of the form of land tenure. LINZ only tells us about titles issued which can be the traditional fee simple, house on a section or may be unit titles in a multi-dwelling complex.

Both have their faults which means we don't really know with any kind of accuracy what is really going on. And my previous comment was that it would be almost trivial to collect accurate data in near real-time except the government doesn't care enough to make it happen.

Costs are soaring and this jeopardises viability of projects over the term of the project. Project costs are viable at consent phase, but become non-viable.

Take for instance the small apartments sector:

The 2005-2006 boom was driven by aggressive development of shoe-box apartment living, and even tinier 'student accommodation'. That period has passed and the reviews of such development have not been kindly received. The new demand is for more upmarket units and the volumes of these are much less. This is not something developers mind as these newer, larger units are undoubtedly more profitable.

These "reviews" of small apartments not being "kindly received" is highly contradicted by their resale performance. So highly contradicted in fact, that I would go so far as to say they do not really exist.

The apartments built in the 2001-2006 boom are on average trading at prices in excess of their original pricing - a good investment currently in high demand and not showing any depreciation. The growth in value they have shown would have been enough to guarantee massive production today and they were the obvious solution to a housing crisis. This is a proven phenomenon that has occurred in competing markets - Brisbane, Melbourne, Sydney.

Unfortunately we live in Auckland and are governed by the idiocy of Auckland Council, who have shoved land prices through the roof. As land costs have soared ever higher this has marginalised out of existence the profitability of building small apartments. The largest chunk of the apartment market can no longer be feasibly constructed in Auckland. The only segment is the low volume, high profit premium apartment segment.

Auckland Council has decided to Make Land Costs Go Really High Forever And Ever. Soaring costs equals development retardation.

Councils have zero clue about the time value of money. So stalling decisions, asking for more info, kicking the ball over the fence into another department for a while - all the BAU of getting a consent through - can eat up months or years. During which time markets shift, lending costs and credit lines are reviewed, materials cost inflation chugs on and the 'carry' - the ongoing costs per month which are the sum of all the unavoidable or sunk costs - is thus what sinks most developments.

All blissfully unknown and therefore uncared about by Councils.

Now, to float an old idea, if Councils were to be charged IRD's UOMI each month, on the declared value of the sunk costs plus the accumulated carry per project, they would receive real data about the costs they so blithely impose on all that are unfortunate enough to have to deal with them. Behavioural and cultural changes might well ensue.

But I wouldnae Bet the Farm on that happening.....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.