Over the past three years, median house prices in Auckland have risen +40% (from $600,000 at the end of 2013 to $840,000 at the end of 2016).

Over the same time frame, the median rent in Auckland for a 3 bedroom house has risen only +19.2%, or less than half the house price change (from $520/week at the end of 2013 to $620/week at the end of 2016)

Given Auckland's widely observed 'housing shortage', how can rents rise so much slower than house prices?

With home ownership rates falling, on the surface this seems to fly in the face of common sense.

So it is time to look at the underlying data of the overall Auckland housing market, with a special focus on tenure.

Unfortunately, the raw data is only available from the Census reviews, and they happen infrequently. Even Statistic's NZ's subnational data on households is infrequent, and when it is released, it is only their estimate based on the change trends they see in the census data.

But there may be another way to bring the Census data up to date.

What we know

As far as housing is concerned, there are only a few key data elements needed to make an update, and a couple of assumptions for which we can be pretty sure we can agree on.

Statistics NZ have published this Census data for Auckland:

| 2006 | 2013 | ||

| # | # | ||

| Owned or part-owned | 204,711 | 201,411 | |

| Held in a family trust | 52,791 | 67,533 | |

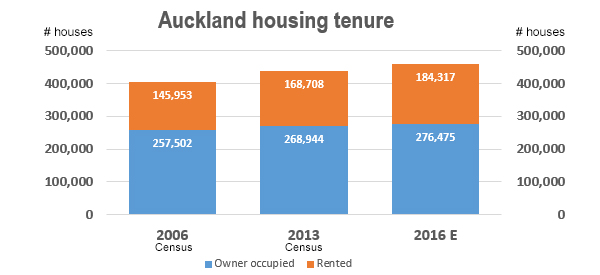

| Rented | 145,953 | 168,708 | |

| ----------- | ----------- | ||

| Total households declared | 403,455 | 437,652 | |

| 'not elsewhere included' | 30,851 | 31,851 | |

| Total Households | 434,265 | 469,503 | |

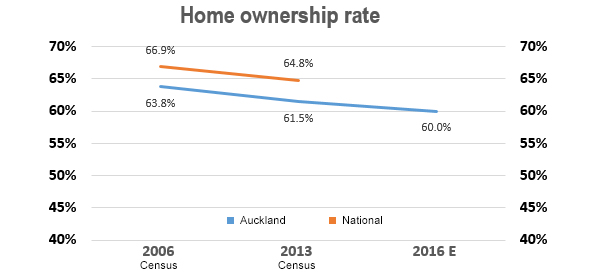

| Home ownership rate | 63.8% | 61.5% |

In that seven year period, the number of total households in Auckland grew by +35,238 or a bit over +1% per year.

But the number of households renting grew by +22,755 or +15.6% or more than +2% per year.

Essentially, housing was converted from 'owner-occupied' to 'rented'.

In the same period the volume of owner-occupied housing only grew by +4.4%, or 11,442 over the seven years. That is a remarkably low 1,635 per year.

Fast-rising rental supply kept a lid on rents. Conversely, slow-rising owner-occupied supply helped juice up prices.

Small-time property investors have been hard at work 'removing' owner-occupied housing from the market and adding it to the rental market.

In conjunction with strangled new build supply, this has had a distorting impact on both rents and house prices.

We can update this data to 2016

On an 'educated guess' basis we can update the 2013 Census data to 2016. Essentially, Auckland's housing supply is increased by the number of consented new residences issued. If we assume that it will take about a year to bring a 'consent' to occupation (and if we just ignore some minor practical details like housing demolition, and consents that never get built, and 'renovations' that end up as extra rented premises), we can expand the above table like this:

| 2006 | 2013 | 2016 | |

| # | # | #E | |

| Owned or part-owned | 204,711 | 201,411 | 203,475 |

| Held in a family trust | 52,791 | 67,533 | 73,000 |

| Rented | 145,953 | 168,708 | 184,317 |

| ----------- | ----------- | ----------- | |

| Total households declared | 403,455 | 437,652 | 460,792 |

| 'not elsewhere included' | 30,851 | 31,851 | 32,500 |

| Total Households | 434,265 | 469,503 | 493,292 |

| Home ownership rate | 63.8% | 61.5% | 60% |

23,140 residential building consents were issued in the years 2013, 2014 and 2015, and these are added above to give a total of 493,292 households at the end of 2016. Assumptions about the home ownership rate and the level of ownership in family trusts are estimates that allow us to complete the table.

That suggests the rate of conversion from owner-occupied to rentals actually picked up in the three years to 2016 to over +3% pa (half as much again as in the 2006-2013 period). And that supports the slowish rate of growth in house rents, while median house prices rose faster.

This conversion of owner-occupied to rental tenancy is one factor, albiet an important one, in why prices have risen so fast in the Queen City. Investor conversions are a significant part of the distortion in prices.

Auckland's home ownership rate has probably slipped below 60% about now.

Until now, renters have had the advantage of a relatively better deal for their housing costs. It has 'paid' to rent.

It is debatable about the overall social pressures renting is causing. Tenure issues are undoubtedly social pressure points, and as most residential landlords are amateurs, there is a lot of tenure risk renters assume.

But at the same time 'households' are forming later in life. The demand for owner-occupation may have been lower than a decade or three earlier. This is worth a read on the subject.

A serious increase in new house building is likely to keep a lid on overall Auckland house rents. But until latent demand is seen to be satisfied, it seems unlikely that it will depress house prices Christchurch-style. Only a sustained rise in supply over many years will do that.

No chart with that title exists.

61 Comments

"A serious increase in new house building is likely to keep a lid on overall Auckland house rents. But until latent demand is seen to be satisfied, it seems unlikely that it will depress house prices Christchurch-style. Only a sustained rise in supply over many years will do that."

A very mainstream POV, and for most market commentators, this is the safe bet. However, I suspect that a more sinister phenomenon can occur: flat house prices strangle consumer spending and basically stifles the economy. Very few economists and market commentators are prepared to address the likelihood of this happening. However, considering h'hold debt levels and flat income growth, it is fair to say that this poses the single biggest threat to the economy. Forget house prices and milk powder, consumer spending is the lifeblood of our economy and spendthrift behavior and attitudes are the last thing we need.

J.C , undoubtedly the NZD would fall in this scenario, and lowering interest rates may not be possible.

NZD will fall due to reduced consumer spending? Not sure why that would happen. I agree that interest rates needs to be relatively higher in NZ to fund our debt and spending.

I agree very much with you that falling house prices pose the biggest threat to the economy. Most people can't see that (just read how many comments call for the real estate market to drop). People think that, if they don't own a house, it would be great for the R E market to crash, not realising that everyone will be worse off and that, possibly, themselves will be out of a job

Unemployment went up to about 9% (IIRC) post-GFC.

Realistically, though, most people commenting on this site probably won't be the ones losing their jobs.

Unintended consequence?

We know that low interest rates have inflated asset prices ( property and shares) , but not wages ( and therefore rents have possibly stayed subdued in relation to house prices because people cant actually pay much more )

I reckon this is what happens when you destroy the value of money is all sorts of thing you would not have seen coming .

The OCR was nearly 9% in 2007 , and its now 1.75%

That boils down to a spectacular destruction of savers wealth and income , and a massive disincentive to saving .

Like a hangover , we are going to wake up to this reality of what we have done at some future point

Maybe Ben Bernancke will re-write his thesis one day

nail on the head.

EIther we have to have rampant inflation and wage growth to catch up with the house price inflation. Or property prices have to drop. Rents are somewhat proportional wages, which should be proportional to house prices. But house prices have got right out of whack, especially in Auckland.

Many savers have put their money into housing, due to the terrible returns, hence another reason why house prices are in a bubble.

Terrible returns like the NZX50 doubling in value since 2009? Expectations are obviously high, but are they realistic?

Most kiwis fear or don't understand the stockmarket. It's unfortunate and I'm trying to educate my friends but it's a very slow process as only a few are able to save or invest.

So investments for most is money in a savings account. People have taken those savings and invested them to get better returns. Now a lot of retirees have rental income and no savings. They are not able to respond quickly to changes because of this. That said a mix of shares and bonds would be serving most retirees better. Low interest rates have made a complete mess.

I know how you feel, I have many discussion about it with work colleagues paid a lot lot more than me

nearly all are to afraid to buy any shares and it is ingrained into the nz way of being brought,

ie the ONLY way to growth wealth is to buy rental homes and you can only lose your dough on the market

It seems that a lot of kiwis believe they understand property and invest in it. Fact is most have no idea and have not seen the problems that those in the construction industry are aware of, and have little understand of the risks associated with a mortgage. Then they decide they want to become a landlord apparently unfamiliar with all the problems associated with letting flats.

Yet a lot or shares provide better returns without the hassle of obtain court orders or turning up with a bailiff to evict someone. I'm pretty sure most people don't want a second job.

You overlook the huge gains to be made by using leverage. A mere 10% gain in house price becomes a 50% gain if you have an 80% mortgage. So your 100% over 7 years just doesn't compare. Yes, it's nuts, but that is why kiwis love houses.

ahh leverage a wonderful tool in a rising market, a nightmare in a falling one.

do you think most property investors A understand they are using leverage and B understand how it works both ways, especially those that are using IO loans.

most property tutors or mentors or whatever you like to call them base there seminars around using leverage.

after 2008 there were a lot of loss making investors that banks forced to liquidate properties that are probably still scratching their heads trying to figure out what happened

The practical trick with using leverage is to deleverage over time. A 30 year mortgage isn't a great way to do it but at least the debt goes down, however interest only mortgages create an exceptional risk for the borrower.

Sorry dictator but I couldn't disagree more, I only use Interest Only loans and I never intend on paying them back. Why would I want to pay a loan back for an investment house ??? Tell me why ? (it's different for your own home)

It has all to do with the level of risk you are willing to accept. There is no right and wrong just risk and return.

My comment was more targeted to small investor or owner occupier. Especially those that get in over their head.

I'm assuming you own a number of properties and understand exactly the risk of the interest only loans are. I also assume you plan to hold the properties in the long term rather than flip them.

Personally, I've invested in the sharemarket and in real estate, I lost money in the sharemarket (maybe I'm not good at it) but I have never lost a single $ on a house even in the biggest crash of the last 30 years, in 2008, when house prices dropped a catastrophic... 8%

Sounds like you are correct in the way you describe yourself. You have certainly missed out on some fantastic opportunities by not being in the equity markets. Stick to real estate and keep getting those average returns.

Unfortunately most people get poor advice in relation to equities. Best to apply modern portfolio theory or just buy index funds (where you don't beat the market, nor do you fall behind it).

"Either we have to have rampant inflation and wage growth to catch up with the house price inflation. Or property prices have to drop"

This is based on a nice old fashioned Kiwi idea that most of us should own our own house, but is it really the case ? Trends here and worldwide suggest not

youre missing the point that debt must continually grow ... central banks know this ... this is why they are desperate to get lending going by devaluing money.... but its only pouring in to capital values, not wages. So return on capital edges ever closer to nothing ...

Once debt goes to zero interest. you ll know it has been a ponzi scheme.

If we are to accept that home ownership is no longer to be the norm then landlords need to accept that people still need homes and in that our tenancy laws are utterly woeful and must change.

Absolutely right PocketAces, I grew up on the 5th floor of an apartment building in Switzerland, all of my friends lived in apartments as well and everyone was very happy with it. But the tenancy laws in other countries give tenants security and in NZ they do not. My mum still (after 50 years !) lives in that same apartment

exactly Boatman.

We need debt growth to continually grow wealth... debt is wealth - the financial system mandates this ... but to ensure that the debt is growing, we have devalued money to the point where we now have a capital system with no return on capital.

Capital growth is not enough ..unless you can also grow the wages of the masses, their dwindling demand collapses the system.

We are now on fumes only...

Rents are determined by the law of rent.

In "normal" (non speculative) circumstances, the selling price is calculated by looking at the actual economic potential of a given property (annual income that could be derived from leasing it) and calculating how much money would be necessary to obtain the same income by merely putting the money in one's bank.

During a land mania (i.e. during what we currently see in Auckland and New Zealand), nobody bothers to look at such details as "fundamentals" and instead the price is limited by the bidders' imagination about future values and their ability to borrow bank-created-credit (or otherwise obtained financial capital).

Until now, renters have had the advantage of a relatively better deal for their housing costs. It's has 'paid' to rent.

That's not to say it's better to rent than own. I know plenty of people in Auckland who would love to own their own house but are paying so much in rent and living each week from paycheck to paycheck, even on professional salaries.

Rents have not gone up because they're at the maximum people can afford. House prices seem to have gone up because interest rates have dropped and not enough new houses are being built.

I assume that those listed as held in family trust are not rented? Is that right? So, in a sense, quasi owner-occupied? Given their share of the total households is also trending upwards (13% in 2006; 15.4% in 2013 and 15.8% in 2016), I wonder what that trend is telling us, e.g., a lot more aging boomers who won't be able to afford their own residential care in the future?

Kate, if anything there will be a greater % of rented houses held in Trusts because investors are more likely to set up Trusts than owner occupiers

Yeah, what I can't figure out is how they are treating these when calculating the home ownership rate. Hence my question with respect to assumptions in that regard.

Disagree. The family home makes more sense to be in trust. Investors want losses to offset other income. You cant allocate losses from a trust to personal income.

Unless your investments are positively geared. Then you put them in a trust and distribute the income to beneficiaries, and maybe one or several of your trusts beneficiaries are on the 10.5% tax rate. Right?

Many thks David.... great article....

One Big point...

there is a gap between number of residences and number of households.. with your data

in 2006 403,000 residences and 434,000 households...... 31,000 households living where.??

in 2016 460,000 residences and 493,000 households.... 33,000 households living where..

http://www.aucklandcouncil.govt.nz/EN/planspoliciesprojects/reports/Doc…

On page 3 of this doc. by ACC it says there were 473000 occupied dwellings in Auck in 2013 ( using census data).... PLUS ..there were 33000 unoccupied dwellings..??

David, ... are your numbers straight from the census data..??

also.. on page 13 of that doc. also show that the av size of household is growing a little.

Data from lines 3 & 4

There was an increase of 57000 residences in Auckland over 10 years 2006 thru 2016

For an average of 5,700 per year

That's not good is it

David, possibly an oversight, when estimating the change in rental/ownership, and appreciating the difficulties in estimation , the charts are redistributing only the' new ' homes that have come on stream. However ' investors' have far outstripped FHB over the past 4 years in purchasing existing homes , in numbers far greater than the preceding census periods , which would make home ownership rates significantly lower.

The median rent chart tabs replicate NZL AKL WGN CHC but it is different data?

Anecdote, but another sidelight into the housing markets.

As a caravanner, I see lotsa 'permanents' in most camping grounds. And there are tiny houses, caravans and other Building Act escapees parked up in surprisingly remote areas: not all would be permanently occupied but some do show the signs: wood stacks, tyre tracks, and smoke out the chimney.

The housing squeeze will certainly be prompting this 'dispersed trailer-park' approach: it's discreet, fast to set up (or move one click ahead of officialdom), and for the most part unobtrusive. West of the Takaka Hill, it is very evident.

And I bet it is not being Officlally Measured. Anywhere.

What applies to caravans also applies to boats, births and marinas. A few thousand dollars each year will buy you a permanent birth at a marina.

True. I read an article a few months ago about a young couple in Whangarei living on their own boat in a marina because it was a viable alternative for them.

I wonder how long it's going to take before someone starts renting out houseboats. You know, with a tagline something like this:

"Fancy life on the ocean wave? Enquire now about renting one of our houseboats, ideal for the more adventurous tenant, and STILL cheaper than land-based accommodation! Our houseboats are well-maintained, and are guaranteed not to sink (terms and conditions apply). Gone on, take the plunge!"

That's the trouble with using a macro approach looking for answers that can only be answered with a micro analysis

The rental market is not static. It is dynamic, made up of a number of components

In the absence of any micro-data to rely on my guess would be the largest segment of rental properties would be long-term dedicated rentals that are committed to the rental market and "probably" have little to no mortgages and the proprietors are "probably" relaxed about the levels of rent income and do not chase the very last dollar in the interests of retaining quality tenants

Then there would be a segment of proprietors who have low levels of equity and high levels of external funding who are sensitive to costs, a segment to whom interest cost reductions over the last 3 years have been tantamount to a proxy rental income increase. So lowering interest costs have restrained the need or desire to increase rents. Reductions in costs that have been more than significant.

Then the is the turnover segment of properties, ie new entrants, existing investors leveraging up, investors exiting the market, foreign investors and so on who are the marginal cohort who squeeze the most from their rentals

The significance of thsecond segment is minor compared to the first segment, and in the averaging process the "average" result is not much of an increase

Plus of course there is the restraint of tentants incomes and willingness to pay

At current levels of LVR for owner occupiers, they alone cannot drive any increase in the national debt to income ratio. It is residential investors who now drive increases in debt to income, - banks do not require much income from rentals to lend investors gobs of money (DTIs >8).

Hence, until DTIs are imposed or LVRs to investors lowered, we will see much more conversion of existing homes to rental housing.

Peri, can't see how you are able to say that residential,investors drives DTI levels.

If a property is returning say 500 per week in rent that is 26k per annum gross.

On that basis with many thinking that the DTI level should be about 5 times that only allows Banks to lend $130k.

See how the DTIs are not going to work for investors.

Even couples on good money won't be able to afford to buy in Auckland with a 5 times limit either.

From years of experience I can tell you that there is one reason only why rents remain moderate.

Wages have not grown in pace with house prices and the humble classes simply cannot pay more. QED

If wages had have kept pace with house prices then the need for the likes of landlords would have been much, much less. You should thank your lucky stars for all the effort made to keep wages suppressed while at the same time allowing everything imaginable to send house prices into the stratosphere, oh, and while you are on your knees doing that, you should also thank the public of NZ for chipping in for rents that are still too high for people's earnings.

Have to agree with you BD. It's a woeful story of NZ's gradual economic demise.

"That suggests the rate of conversion from owner-occupied to rentals actually picked up in the three years to 2016 to over +3% pa (half as much again as in the 2006-2013 period). "

I notice that the actual number of owner occupied households had increased in the period - over 10K to 2013 and a further 8K estimated to 2016 - So if the article is presenting this data as facts and evidence - could it please refrain from talking about owner occupied properties being converted to rentals - a more accurate report would be that a higher % of new dwellings are rentals than previously - likewise - the comment that home ownership rates are dropping - is only true as a % of dwellings - number of homeowners in NZ continues to increase! It also suggests that in reality, new builds, one of the key solutions to any shortage in accommodation, is largely driven by investors - not surprising given how difficult the process of consent is with Auckland Council - and any onerous restrictions or barriers to developers is likely to reduce the number of new builds before they even reach break even point far less catch up with the shortfall -

Few dynamics at play (+ve) and (-ve) for rent prices (in order of importance)

(-ve) Kiwi Landlords of course would like more money but they’re extremely reluctant to raise the rent on good tenants. If you’ve got a good tenant you should hang on to them. Raising the rent will result in a high tenant turnover, and greatly increased risk of getting a nightmare bad tenant. There’s a supply and demand of good tenants and in recent years a lot more landlords looking for tenants.

(-ve) As big daddy pointed out wages haven’t gone up. In poorer areas of Auckland tobacco price increases mean that smoking consumes more than half of peoples WINZ benefits. This leaves poor people virtually nothing to spend into the community, to buy food with, and to pay rent with.

(+ve) Many high income young people in the 30’s and early 40’s are now forced to live in shared accommodation (in Auckland) rather than buying and owning their own homes. Therefore the number of people per dwelling is increasing. Landlords who know that they’re harvesting multiple incomes can raise the rent.

(+ve) Many Chinese purchase houses and just leave them empty. Certainly if you’re selling a house and want a Chinese buyer you should make sure the house is un-tenanted. I was told that by an agent.

David, have you put "housing shortage" in quotation marks because you don't believe there is indeed a shortage?

Graham you sound a little skeptical that there is "not" a housing shortage. Well there are 3817 properties advertised on Trademe in the Greater Auckland area. Compare that with the likes of Nelson / Tasman with a tiny population of only 100,000. (1/15 the size of Auckland) This area has 132 properties advertised to let. Scale that up for Auckland and you would get a total of 1980. Now if there were only 1980 properties advertised for the whole of Auckland then you could reasonably claim that Auckland had a rental house shortage.

Best you factor in higher home ownership rates in the regions compared to Auckland now, therefore creating a larger pool of rental houses in Auckland and a smaller pool in the regions compared to overall number of dwellings.

Well done on your statistical studies. You should have completed the study by plugging the number of rentals advertised on Trademe. Compare the numbers for Auckland with other areas around the country. It is easy to see that Auckland actually has more properties advertised on a percentage basis than many other areas of the country. (higher vacancy rates) It is this high supply that is keeping the rent prices subdued. Long live the free market. It does work and is far more responsive than a socialist economy.

Seeing as the free market is changing NZ from a nation of home owners into one of reluctant renters, it clearly has not responded to anything other than lining the pockets of investors and speculators. Bring on a bit of socialism to right the wrongs of the free market.

Maybe the renters simply cannot pay anymore.

Economic theory suggest that if supply is limited and demand is high then the price will increase. But it forgets the actual commodity in question - Money

The supply can charge all they want, and the demand can want/need it above anything else, but if the money is not there to pay, then no transaction occurs (at least not officially)

For the proof, you only have to look at how many physical bodies are now living in each property. Something this article does not remotely touch upon.

I have seen 40+ people live in a three bedroom house in London (Official tenants on lease = 6)

From what I see now, there are similar properties in AKLD with 20+ people in them.

So our slumlords need to pick up their game. We could easily have 50+ here, as most properties in NZ come with at least a garage or a shed, and often a small patch of grass. All it takes is a bit of investment in bunk beds, some nice hospital curtains in the living areas and hallways, a set of stairs into the roof space, move the car/junk out of the garage/shed, and a tent or two in the yard.

Of course we can't be using anecdotal evidence can we? must use official reports. Official reports are official after all, always correct, not politically biased, and people never lie, misrepresent, or fail to answer when questioned by officials.

"Economic theory suggest that if supply is limited and demand is high then the price will increase. But it forgets the actual commodity in question - Money"

Ahh, what?

You don't realise that access to capital (money) is represented in the demand curve?

Bob the guy renting the house gets $600 a week in wages. When the landlord raises the rent is Bob going to use "access to capital" to pay another $30 or $50 bucks? No cause the money he gets is REAL not capital, not equity, not debt, it's the dollars and cents he gets each week, it's cash flow.

Really? can you show with adequate evidence and examples?

Yes, because it is logical.

If price is a function of supply and demand (which it is), then it holds that price is also a function of access to money. Hence, access to money is an intrinsic element of the demand curve.

Rent is $100. Bob has $100. Bob is represented on the demand curve and can rent.

Rent is $100. Bob has $150. Bob is represented on the demand curve and can rent.

Rent is $100. Bob has -$1000. Bob is represented on the demand curve and cannot rent.

See the pattern? - money/capital/ability to pay is an intrinsic element of the supply-demand relationship. It is not a forgotten element, as you say.

To even out the demand-supply imbalance put into law that immigrants must buy new builds, this will stop upward price pressure on existing houses from overseas buyers and increase the demand for new house builds

Wrong.

Demand for new houses increases the demand for developable land. Given that Auckland council wants this land to be predominantly in the form of rezoning (under the unitary plan), property prices will substantially increase in redevelopable zones.

Nah. We need to put a stop on building new houses, the new infrastructure required is too expensive.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.