The number of homes newly listed for sale on Realestate.co.nz fell to the lowest level on record last month, and asking prices for Auckland properties continued to slide.

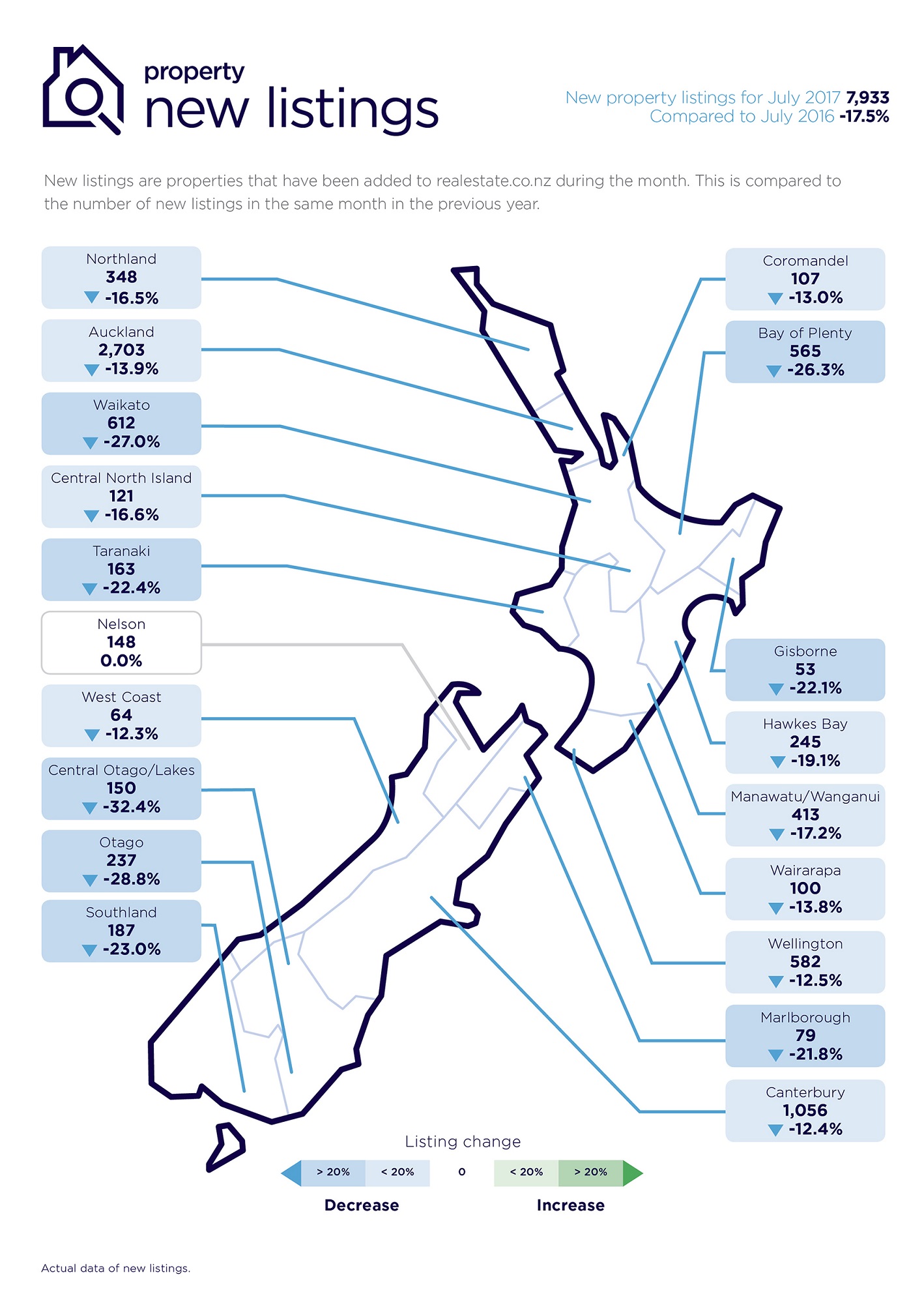

There were 7933 homes throughout the country newly listed on the property website in July, down 17.5% compared compared to July last year and the lowest number in the month of July since its records began in 2007.

The number of new listings was down in 18 of Realesate.co.nz's 19 sales districts, with only Nelson going against the trend with new listings there unchanged from a year earlier.

in the North Island the biggest falls in new listings compared to a year ago were in Waikato -27.0%, Bay of Plenty -26.3% and Taranaki -22.4%.

In the South Island the biggest falls in new listings were in Central Otago/Lakes --32.4% and Otago -28.8% (see chart below).

Asking prices are also falling, with the national average asking price falling for the third consecutive month in July to $608,143.

That means it has now fallen by $40,619, or 6.7%, since it peaked at $648,762 in February.

The slide in average asking prices is most pronounced in Auckland, where it has fallen for the last five consecutive months and was $903,752 in July, down by $74,900 (7.7%) from its peak of $978,652 in February.

That suggests vendors are starting to accept that the market has weakened and are being more realistic with their asking prices.

The drop in prices in Auckland may be starting to spread to other regions, with July's average asking price being lower than June's in 11 of Realestate.co.nz's 18 sales districts.

That includes several areas where the market has remained relatively buoyant, even as Auckland's property market cooled, such as the Waikato, Bay of Plenty, Manawatu/Whanganui and Otago, all of which recorded lower average asking prices in July than they did in June.

However while new listings and asking prices are down in many regions, inventory levels, the total number of properties listed on the website are up.

In July Realestate.co.nz had a total of 24,518 residential properties available for sale on the site, compared to 22,644 in July last year.

59 Comments

Just shows what an impact foreign and domestic speculation had. Chinese money stopped by requiring ird number, and PRC cash controls. Domestic stopped by requiring investor/speculators to actually have some equity. What a mess, Nat should be ashamed for not acting years earlier than they did.

Hahaha... you reckon mr. English will agree with you?

I understand chinese domestic housing market is also slowing while still lots of capital coming out of the country and cash buying here is not less but more.

Where's your evidence of that Mrp? In your assumption that Chinese 'cash buying here is not less but more'??? Personally I think you're talking out your derriere.

There's a whole avalanche of news articles that points to the opposite; that Chinese Foreign Investors have had their credit line stopped and aren't even able to get cash out of their country in significant quantities hence why our property market is re-correcting and quite probably going to crash in the long run.

Here's just a sample of evidence that points to the impact of Foreign Buyers globally and how their absents effecting property markets.

Article: China’s PBoC Announces An Army of Over 400,000 To Prevent Money Laundering

https://betterdwelling.com/chinas-pboc-announces-an-army-of-over-400000…

China’s Massive International Real Estate Buying Spree Is Officially Dead

https://betterdwelling.com/chinas-massive-international-real-estate-buy…

National didn't do squat. China's government and the Reserve Bank of NZ did all the work.

I think it's due to the 40% LVR and bank lending tightening much more than foreign money. Investor lending is 48% down June 17 to June 16. Can't buy houses with no credit

Correct Yvil. There's always Resimac for lending but its easier to sit around and do nothing. Why tie up equity now? Better to wait. Many investors like me have equity but we'd rather sit on it when the market isn't creating more in a hurry.

Looks like a fall in prices coming just in time for National in the Election.

The thing is that it is likely not to affect them too much, as prices were always expected to drop back quite a bit. I mean they can't just rise at record levels, and never go back down again. eg what goes up must come down. It is lucky for national that the election isn't next year, when the dropping prices, and potential interest rate rises may make people worry a lot more.

I can't believe the heralds choice of headline

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118…

The NZ Herald has become a propaganda piece, its a disgrace this is our national paper. The reporter who wrote this has no place calling herself a journalist

Totally agree. With the exception of some op ed pieces by contributors, the heralds property coverage is useless. No, it's worse than useless, it's dangerous. They are paid schills. They are totally in thrall to the real estate industry's advertising revenue. It's disgraceful.

Yeah...wow...that headline linked to is shocking. I'm still struggling to believe the Herald has dropped so low.

Pretty much the same desperate propaganda in Stuff.

The headline fits Wellington. Wellington has the lowest number of properties on the market in 10 years. Seatoun to Tawa has 423 listings on trademe. When I moved back to NZ early 2008, there were 200 properties on the market in Waikanae alone, and over 1000 properties listed for the Kapiti Coast. Houses are getting destroyed by slips faster than they are being put up and the population continues to grow.

Yeah Sat Herald is only good for sports pages, and lighting the fire for the rest of the week. The rest is just advertorials. MSM wonders why they are in trouble.

click bait - NZ herald is a bit of a Tabloid these days, next they will have a page 3 girl....

The page 3 girl is to show the effects of inflation and the difficulty of affording sufficient food and clothing in the coming hard times.

Will she be Chinese or Indian?

Strong lobby. NZ = For The Rich, By The Rich, To The Rich.

Think and Vote.

Hopefully all the houses will be sold out in a few weeks time, forcing the house prices to sky-rocket again.

Pray tell please advise the readers where buyers are going to get the money to buy these houses....

the nurse must have doubled your meds this morning

hahaha good one

Real funny. Auckland Listings have been sitting at 9.5k for a loooooooong while now. Wait till spring and watch the listings explode!

A 75k fall in asking price indicates to me that they were asking too much in the first place.

Nothing major here just sellers not being so greedy.

The fact that Auckland has 49.3% more stock, and weeks stock has returned to the long term average, seems to have been overlooked as not newsworthy?

The slide in average asking prices is most pronounced in Auckland, where it has fallen for the last five consecutive months and was $903,752 in July, down by $74,900 (7.7%)

Only about 20% to go...

The frightening thing is, that takes prices to 2014 levels? 7x income. Still seems bubbly.

Costs of new builds are too high to allow Auckland to attract new business based on good value, the long term future of Auckland is low growth over priced stagnation. 5 - 7x income is the new normal.

The regions are where it is at and will provide better long term gains as their cost structures allow better route for investment.

The problem for NZ is that Auckland is big and when the big city goes as stupid as Auckland Council, it makes for a high proportion of wasted investment.

Glendowie home bucks slowdown trend, sells for double its CV!

https://youtu.be/TgMjtuQt96M

http://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=118…

http://rwmissionbay.co.nz/properties/sold-residential/auckland-city/gle…

Ooooh! good times are just around the next S bend!

What's coming is going to be appalling, and it was all so avoidable. John Key was right when he said "You don't get out of debt by borrowing more money". Yes there is a time and place for debt, but hot on the heels of a debt inspire near-death experience ( the GFC) is not it. At the local level, debt ( and so property prices) should have been contained in 2008 and debt reduced in aggregate. Some, along with Terry Serepisos, would have been worse off - the rest of us would have coped. Now? There is no Hope in Hell of 'the rest of us' avoiding the calamity at our door. "Chicken Little!" Maybe. But in one version of that tale, The Fox does eat the birds.......every other encounter was merely to inspire false confidence that 'We'll be ok. We saw him off last time"...and then, the whole lot got taken.

Japan has seen him off for almost 30 years. The market can stay irrational longer than you can stay solvent.

It's the ELECTION that is weighing on the market.....and has been since....well since November 2016 I guess....but prices are set to double in the next few months due to 'MERICA's CUP!!! and NO MOAR LANDZ!!! and DEMOGRAPHICZ!!!

And if prices don't double, then it's because of post election and Christmas. But just wait until after Chinese New Year 2018!!!! After that it's probably quiet because of the 2.5 year lead up to election 2020. That's when Auckland lifts off from the earth, forms a ring in space, and becomes Elysium for real. Millennials you can get to Elysium, but you need to fill your solid fuel rocket boosters with lots of avocado and sky decoders.

Turns out the lead character in Elysium is Max Da Costa lol. Well Auckland you Max Da Costa nearly a year ago! Did you just feel a shiver down your spine? That's because it was quite cold last night. Can't go wrong with Auckland property maaaaaaate.

What you say sounds really familiar.

I can't quite place it, though.

Anyway, stop being so pessimistic. Housing never goes down.

On that note, I'm off to find some arbitrary outlier property sales and place the links in this comment thread.

Then I will make a sarcastic comment pointing out that paying $6m for a house is perfect for FHB who are starting a family.

But only if it is in double Grammar, though, right?

No chance of that zone ever getting split up, eh?

Take all the upvotes you magnificent bastard!

The GFC was a baby compared to now. This has been made in nz and has blown every % or figure a mile high, and it shouldn't have been aloud to happen, should have been stopped way back in 2015, there'll end up being heaps of listing and sales ok as people drop ther prices then it'll stop and turn to stalemate, then it'll be a different breed of people selling, the one that didn't take part in this and the normal people selling for normal reasons

You guys remember our buddy Ted Stanton?

"by Ted Stanton | Wed, 18/01/2017 - 13:50

China is going to buy up Auckland after Chinese new year 28 Jan to Feb 3.

Five bedroom houses 300sqm in Albany or Flatbush is what Chinese desire."

http://www.interest.co.nz/property/85512/median-house-prices-dropped-mo…

He's probably saying the same things over on nbr.co.nz now, under a bunch of nomes de plume.

The election is the new chinese new year

"The slide in average asking prices is most pronounced in Auckland, where it has fallen for the last five consecutive months and was $903,752 in July, down by $74,900 (7.7%) from its peak of $978,652 in February."

When looking at the graphic here http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=118… the average asking price for Auckland in July shows 942,999 however the Interest.co Auckland average is 903,752 can someone confirm which is correct?

The Herald piece uses the American X12-ARIMA standards - ie" Seasonally Adjusted Asking Prices. I can't figure how Seasonality relates to Asking Price?

With ARIMA it doesn't matter if you have seasonality or not.

It just reduces the model down. Just like if you take out the integrated part, or the autoregressive aspect.

"The Coromandel led the way with a 11.2 per cent lift in asking prices compared to the previous month"

Hurry Up - Listings are at record low - BUY NOW or you will miss out!

This is what they are trying to pass on in a smart way....

Sit back and watch the market keep falling. Wait and see approach don't try and catch a falling sword....vey dangerous move.

Like the Flu, Auckland catches a cold and everywhere else starts to sneeze.

I'm actually seeing a lot of homes being pulled from the market due to not achieving their desired price. They havent sold, as I've seen them pop back up later with a new real estate agent, or they are put up as private sales on Trademe or Facebook. I think a lot of vendors believe they just have to wait until the market "recovers".

Agreed. I think houses in the Residential- Single house zone that are listed in the $4-6m market are in for a large tumble. Kiwis working and paying tax in NZ did not push prices to that level and unless there is an option to increase density by the new Mixed Housing Suburban, and Mixed Housing Urban, just cant see that ever being considered "worth it" by local Kiwis. Perhaps rich kiwis will flood back from London and or Australia, but I cant see them wanting to pay more than they should either.

Accordingly I think those vendors will be in for a long wait, unless money not limited to the constraints of working and paying tax in NZ returns to the market (e.g. Chinese money).

London money will stay in London, you'd be mad to sell up for the lowest pound in 31 years to convert it to buy in what is considered a massive bubble in Auckland.

Same can be said for any english family looking to convert their well build two story brick, double glazed house with back garden anywhere in UK and see what they can get for their equivalent stirling in Auckland right now.

Yes, I see a lot of that also. Waiting for Spring and the market pickup ........there are going to be a lot of properties coming on the market and peoples expectations are going to struggle to reconcile with reality

I think one big change that I can see with this cycle is the amount of information. One of the big advantages of residential property is that unless you put it on the market it is hard to now what it is actually worth therefore people dont really see the dips just the long term trend. Most other assets are very transparent as to value eg share price goes up - feel good or goes down - not so good. Imagine if I could see on a weekly basis what my houses were worth!! The difference week to week could be 10's of thousands up and down depending on who was prepared to buy them. We now have much better visibility (still way less than other assets). I saw a stat last week that during June 7.9% of house sales in Christchurch were at a price less than they were bought for (May was 6.5%). Anyhow all this data can only assist people in understanding the value or declining value of there biggest asset and that in a double edged saw.

What do others think?

I think that being able to see what properties sold for on homes.co.nz, QV and TradeMe has changed the game. Now you can see exactly what the prior sale price was, and what other homes in the area sold for, so you are not going in blind. For instance, two identical townhouses, one sold last Sept for $500k the other is on the market currently for $560k. Chances of it selling at that price? Nil. When you are better informed, you can make better offers.

I am seeing houses on the market in Chch listed for less than what they sold for in 2014. Its becoming a common sight now. People simply overpaid in the 2013-15 period post earthquake, partially due to the high rents that properties were getting. Of course, rents have declined since then, so prices will too.

Real Estate agents are telling vendors that its a quiet market, not many buyers around, and to wait for spring/post election/insert other excuse here - so there is going to be a massive influx of properties in October!

I agree.

It can be a double edged sword though, given the underlying reasons for stickiness in property prices.

What we really need is a better set of indices for the market(s). homes.co.nz and trademe.co.nz are constructed very poorly and the methodology for QV is only good in larger samples.

It must really piss the real estate agents off, though. It begs the question why commissions are still so high in the industry given that their value add is significantly dwindling.

It is a good thing though if you want to sell a house yourself. Now you know what the comparable sales in the neighbourhood are, and you can price your place accordingly. No stressing out because you've priced it too high or too low. Just put a $ figure on it, put it on TradeMe and cut out the agent. No more shopping agents based on which one gives you the highest valuation, then attempting to manage your expectations down when it doesnt sell at that price, and still taking a hefty commission even though they couldnt sell it at the price they said they could.

...absolutely.. the 'prior sale prices' are true numbers , which to make objective calculations for offers..some realism in the property market at last..

I've read this website for many years, never commented but laughed at the various opinions from various characters. This downturn is just cyclical, if you take the time to graph house sales since 1993 you will see, every 10 years there is a downturn, and 2017 is it. In 2020 house prices will inch up again, not as much as they have in the past but they will go up. The value of the dollar has gone down because of monetary policy, plus there has been pressure from increased demand (returning Kiwis and rich foreign immigrant/investors, and add to that the lack of supply, council costs, building/material costs etc. The books that show info back before 1993 still show this 10 year cycle.The reasons for the cycle are many and varied. In my opinion just hold onto to your houses and wait this out. I bought 9 rentals between 2004-6. All more than doubled in price. Good equity and positive cash flow now. People/family were telling me this was very risky. They have a different view now.. I laughed that Bernard sold his house because he thought the market would drop by 30%. Well everything is risky but from what I could tell from past data this was the least risky thing to do (these cycles have been going since Adam was a boy but no-one tells you at School). I was told that we would not have superannuation by the time I hit 65 yrs old, so I bought these all with bank money(OPM), using my house as security. Paid off big time. Its not rocket science. Go figure. I don't give a toss what the market does right now. It would have to go down by 60% to make me worried. The thing is that this is going to happen again and again. When I was buying property at 150K each that was big money. I remember thinking in the 1990's that people who had 150K mortgages were really stupid. No way they were going to pay that money back. Its chicken feed now. You dont pay the money back, inflation takes care of that. The govt has a vested interest to keep the dollar devaluing to keep a bit of inflation. They dont want stagflation, thats the worst outcome for our politicians, so use that fact. Buy in the regions where prices are lower and rent out. Try Nelson, Palmy, or New Plymouth.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.