The days of ever increasing housing values appear to be coming to an end with Quotable Value's latest House Price Index showing property values flattening around the country.

"Values continue to plateau in Auckland, Hamilton and Christchurch in a trend seen since October last year," QV National Spokesperson Andrea Rush said.

"Wellington and Dunedin are now experiencing a similar trend."

The average value of homes in the Auckland region dipped slightly to $1,044,303 in July compared to $1,045,059 in June.

Within the region values were down in July compared to June in Rodney, North Shore, Waitakere, Manukau, Papakura and Franklin, with only the Central Auckland suburbs recording a slight rise.

Compared to June, July's average values were also down in Waikato, Taupo, Wellington City, Nelson, Christchurch and Dunedin, but they were up Tauranga, Rotorua, Whakatane, Napier, New Plymouth, Palmerston North, Porirua, Hutt Valley, Queenstown-Lakes, and Invercargill.

Nationally, the average dwelling value increased from $639,051 in June to $641,280 in July.

"The latest QV House Price Index figures show nationwide values are still rising, but this growth is now being driven by regional and provincial centres rather than the larger cities," Rush said.

Here's how things look in the main centres:

Auckland: Average dwelling value $1,044,303

"The Auckland residential property market is still cooling, with sales volumes down more than 30% below the same period last year, while there are twice as many properties listed on the market as there were this time last year," QV Auckland valuer James Steele said.

"This is meaning properties are generally taking longer to sell and auction clearance rates also remain low, but auction rooms are still well attended so it appears people remain very interested in what the market is doing.

"We are also still seeing well presented properties in sought after locations sell well to owner-occupiers, but in other areas that were favoured by investors, we are now seeing a reduction in prices where speculation was previously a strong part of the market

"Some sellers however are choosing to withdraw their properties from sale if they are not receiving price offers that meet their expectations," he said.

Hamilton: Average dwelling value $540,840

"The Hamilton market has remained stagnant over the past month and the average time properties are taking to sell has lengthened, which is giving buyers more opportunities to negotiate," QV Hamilton valuer Stephen Hare said.

"With the heat now having come out of the market, listing numbers have increased and clearance rates have fallen at auctions, however well presented and well located properties continue to sell over asking prices and with buyer competition.

"The drop off in the number of investment buyers has created opportunities for first home buyers, who were previously getting beaten when vying for properties."

Tauranga: Average dwelling value $691,350

"The market in Tauranga and Western Bay of Plenty is steady at present, with most agents reporting more normalised levels of demand," QV Tauranga valuer David Hume said.

"Clearance rates at auctions are down on this time last year although a lot of conditional deals are being done post auction."

Wellington Region: Average dwelling value $607,011

"The Wellington market continues to slow and residential property values have largely flattened over the last two months," QV Wellington valuer David Comford said.

"Sale numbers are down compared to 12 months ago and this confirms there is less activity from both vendors and buyers.

"Both buyers and sellers seem to be taking a wait and see approach and this will likely continue until after the election and the spring months are upon us.

"New builds and off plan purchases are selling well as these are not impacted by the LVR restrictions introduced last year.

No chart with that title exists.

"Christchurch: Average dwelling value $495,098

"The Christchurch market is stalling, there doesn't seem to be a lot of activity and properties are increasingly harder to sell," QV Christchurch valuer Daryl Taggart said.

"We are seeing a number of cases where asking prices have been reduced to achieve a sale, especially those who require a quick sale.

"Rents are also decreasing which suggests there is an oversupply of rental property on the market."

Dunedin: Average dwelling value $373,857.

"Demand for residential property in Dunedin remains strong and there are very low listing levels, but the rate of value growth has slowed," QV Dunedin valuer Aidan Young said.

"Buyers do prefer well presented, modernised, low maintenance properties and these properties are selling quickly and achieving good prices."

Here's the link to QV's average dwelling values for towns and cities throughout New Zealand:

![]() QV House Prince Index 31JUL2017-7157387c8f1a14e1b84e1e71cfd7aec2c1dd08d8.xlsx

QV House Prince Index 31JUL2017-7157387c8f1a14e1b84e1e71cfd7aec2c1dd08d8.xlsx

207 Comments

Remember that QV data is over a three month period so the data's disadvantaged is that it does not fully reflect any short term / current trend.

Clearly the recent report by the RBNZ that investor buying in Auckland is considerably down is telling in that there is a collective view of an expectation that prices in Auckland will be soft to falling in the near future (or until such time there is considerable increase in yields due to rising rents).

They'll look for a tax dedution. When house prices rise the investor "bought for the rental income" so any capital gain is not taxable. When house prices fall the investor "bought the house for the purpose of resale at a profit" so any resulting loss is deductible.

Same thing happened in 87 sharemarket crash (e.g. pre 87 all share sales were capital gains as bought for dividends, post 87 all shares were trading stock as bought to sell for profit so claimed the losses on sale).

With all the easy Chinese money gone the values have to naturally come back down to what normal kiwis can afford and are comfortable with.....I'm sorry to say but some greedy and selfish people out there are gonna lose alot of money.....furthermore the sediment has changed so these ridiculous asking prices we have been seeing is a thing of dreams now.....

Agree. Prices will slump towards what a person working and paying tax can afford. The higher the rise, the greater the fall.

Specuvestors better pray that Labour and winston dont get over the line. Labour may just let winston be PM, as deputy is better than being in opposition for a 4th term. http://www.labour.org.nz/housing, first item is speculation.

Prices will slump towards what a person working and paying tax can afford.

Should that happen, it'll be good news for most New Zealanders with children. They might have a house worth a bit less when they retire, but they won't have to save all that house capital to pass on to their children, and their children will have a chance to work and live and raise grandchildren in a home nearby.

It wouldn't be as good for specuvestors who feel deserving of the world revolving around them, but...they don't really need to be considered over and above the needs of average NZers for having a place to call home.

We will build even less houses, so poor people will be even more totally screwed than they are today. We will have to increase social transfers and put up taxes to help out the poor. Equality then will increase as everyone gets to be poorer.

And all because Len Brown and Phil Goff decided to jack up building costs in Auckland for no good reason.

Pretty hard these days I'd imagine - the CCP has been getting pretty serious in its anti-corruption efforts.

https://en.wikipedia.org/wiki/Anti-corruption_campaign_under_Xi_Jinping

Doesn't matter, the Chinese have the same access to market data that we do and can see the obvious.

Buying property means suffering 5% capital losses in Auckland or Perth, compared to buying into Melbourne or Sydney or Toronto for 10% capital gains. International investment has more choice available than local investment.

Denial stage of the property cycle. QV show a lack of understanding of the market, prices have been declining for most of the year. This is a normal correction and will accelerate on the way down, there will be a bottom but it could be a few years away yet and then prices will plateau.

So long as people have prepared for it there shouldnt be too many issues ie reduce debt, sell off low yeild or high out going assets and accept that prices could reduce by 20 - 30%.

I have property in holiday areas which are still 30% below the 2006 values and thats not unusual., just have to accept that is what happens and be prepared......

Okay so what you have said Jono seems reasonable. House pricing has a cycle. The last cycle seems to have gone up considerably faster than previously thus the drop/plateau can be expected to be as fast.

What I don't understand is everyone saying this bubble is bursting? What suggests this is happening? The need for housing in NZ is not decreasing and the cost of building isn't either?

Do people expect/want housing prices to drop to what they were 10-20 years ago? I don't see how that could happen.

Prices from 10-20 years ago seems too extreme, and will never happen. I think most people just want prices to return to "normal" levels, which is not 10x income but maybe around 5-7x for Auckland. Big influences for the meteoric rise is due to Chinese capital flight and local investor activity - now both gone (or at least drastically reduced) I would say going back to around 2014 CV levels to be very possible.

Unnecessary terror is going to be inflicted on New Zealand households. It's easy for us all to sit at our desks and tap away about what may, or may not, happen. But the fear of missing out has 'encouraged' many of our citizens, young and old, to jump into a market that is/was obviously extended and it has only one party to blame; and the fear of watching a lifetime's worth of effort go up in a puff of deprecating smoke likewise will have only one author - US! We have done this to ourselves, and elected successive Governments to enact our foolishness. Anyone who thinks 'Spending is Down' hasn't seen anything yet. And as Consumerism grinds to a halt, so will jobs and careers. This....is going to be bad, and we via the Government and the RBNZ are to blame.

They might have held off if the govt had a) been open about foreign purchasers and b) outlined what they would do if it got out of hand. Instead we got deny, deny, deny, it got out of hand and now we have a daily bill of $140k to house people in motels, because of, to paraphrase Bill English, what might have been an unforeseen problem.

How is that possible? Remember, this is an index for entire Auckland.

CoreLogic don't just make up the sale details.

Remember that this isn't a lead indicator.

I think there will be more bias due to changes in decisions to sell, and area factors, but on the most part, I'd say the index is a fair representation of the overall Auckland market.

Big deal. If you bought between 1990 and 2007 you probably don't have anything to worry about. I seriously doubt that house prices will drop below 2007 level, and that is 10 years ago. Furthermore according to the report, '...Central Auckland suburbs recording a slight rise' - not sure why people are cheering for house price crash so much, as if they want to 'steal' the houses at cheap as prices. It's a crime!

Precisely! There will be a number of investors who don't realise that they can't sell that first purchase from 1990 that is now 'in the money' because it's been 'sold to themselves' to finance the next bit of the portfolio and it's going to come to some as a shock. Likewise those that do sell might discover that The Bank won't allow them to extract the 'profit' from a property sale, but will require them to pay down the gross debt first. Markets in reverse can be brutal. It's always easy going up the stairs of profit, and painful falling down the lift-shaft of loss.....

Not sure why people are cheering for house price rises so much, as if they want to 'steal' the money from buyers at high as prices. It's a crime!

Hey here's a song to cheer you up;

https://youtu.be/XB383WkXcqE?t=15s

Not sure if there's anywhere you could get that for free, but you might be able to extract it from QV property insight reports?

https://www.qv.co.nz/property-insights-blog

http://content.corelogic.co.nz/July/index.html?page=20

Interest.co.nz also has some data summaries under "Tools", but this may not cover private sales.

So in summary, after the imposition of the most restrictive LVRs for trading banks in the history of NZ, and changes made to dissuade offshore funds of dubious origin, prices are essentially flat to slightly down in Auckland, and in overall in NZ are eeking out small gains. Time for economics 101, supply and demand restricted supply with large increase in the cost of supplying said product (ie cost of house construction) is being offset by the the movement of the demand curve to the left (due to tighter LVR restrictions).Means speculative froth knocked out of market, and we have a new equilibrium with essentially static price despite the fact that the market should have fallen with the LVR restrictions. This is not the setting for a crash, max 10% decline with plateauing of prices due to underlying fundamental demand.

Gee, that's a lovely story. How about this one:

The biggest credit bubble in NZ history is starting to unwind. Having built up over many years, it will unwind over many years of falling real term values. The unwind was initially caused by lenders restricting credit at the top of the bubble as even they realised that prices were unsustained and posed a serious risk to their businesses. Once investor demand was seriously diminished by negative capital values and tighening credit, it was discovered (unsurprisingly) that the fundamentals of the market were so out of whack that owner occupier demand could not support prices at anywhere near the prices at the top of the bubble. While RB LVR restrictions were loosened, they were replaced by lender LVR requirements were similarly restrictive. The unwind was also propelled by a slow but steady increase in international interest rates as QE unwound. The unwind accelerated as a result of the spectacular collapse of the Australian property bubble and near death experiences for 1 or more Aussie banks, which had the effect of severely restricting mortgage credit available to their nz subs. The unwind resulted in a deleveraging of households and a reduction in household debt to income from 170% to 100%, and a corrresponding drop in house prices of 40% in real terms.

That's a worst case, but it's equally as likely as your scenario.

Falling real prices ie adjusted for inflation is not a concern. Declining nominal/ actual prices would be more of a concern. If inflation is 2% and property prices rise 1% per annum, I would be happy as the property still provides rental income tied to inflation, and the actual value rises 1% per annum.

I own property in Wellington, I would not purchase in Auckland. But I do not see a large fall in Auckland property prices, my estimate 10%. I have previously given the reasons I see this, the most prominent being the high replacement cost of existing property, go out and get the price of getting a new dwelling built, you will be shocked. I also do not see interest rates rising, and for all the central bank talk they cannot get rates up to any great degree. The reason rates are not rising is said debt load. If rates rise the whole system collapses so rates will stay low. Rates can be suppressed via money printing and using this cash to push interest rates down via bond purchases. This money printing is deflationary (out-dated thinking would state it is inflationary), the low interest rates suppress income from savings, but more importantly reduces the cost of capital this is driving increasing productivity and falling prices think robotics , horizontal oil drilling etc. So businesses around the world looking to expand evaluate the cost of modern robotics and other plant versus the cost of human employees and the machine are winning out. As the interest on borrowing say $50 million to automate production is low and makes sense on a cost benefit analysis. And regarding deflation/ disinflation every year more income is spent on services with no marginal cost, think telecommunications, netflix etc this is inherently deflationary. Those who see rates rising are living in a world populated by those who cannot adapt their thinking to a changing environment, even though they are repeatedly proved wrong by only transitory interest rate rises.

It is not a big deal to me. I don't feel like I need to do anything drastic about it and I certainly don't need to panic. Still come to work everyday, work hard, and relax in the weekend with friends and family either at my place or at someone else's. My advice to people is that please don't dwell on it too much as life goes on if you don't have to buy nor sell.

Just because you have an opinion doesn't mean it's not a stupid opinion. Do you think the Earth is flat, too? I mean you are entitled to that opinion but that doesn't make you appear like you're thinking logically here.

I get that you're trolling and you're saying these crazy things to get a reaction. Well, at least I hope you're trolling because if you genuinely believe the rubbish coming out of you then I don't think anyone can help you there #PrayForDGZ

I cant believe how fast this correction is happening, we normally get about 6 years of good and 4 of bad, 2002 was good to 2008 but down to most of nz to 2014, this time it went up like a rocket and dropping as fast in corrections terms, I hope people learn by this , people get confused by the saying the housing market always goes up, it does long term, length of your 30 year mortgage, and so it should and has to because everything goes up, if you put $100000 in a long term investment in 1960 you would have done well to, but we have booms and busts over the 10 year area all the time and for whatever reason it starts investors and flippers go nuts, that's where the government and RBNZ should try and keep balance, BECAUSE IT WILL CRASH , from the early days to now we have pushed up the mortgage length and DTI , these booms are getting worse, I think we are at a turning point, this boom was fast, LVR,s and DTI need to become common place or this stupidity will keep happening, the people in involved that loss jobs and cant sell housing because being under water and stress needed happen

Follow the price of oil until 2008 and then to 2010. What we see is a genuine shortage driving up costs multiplied by a significant speculative aspect and when the big gains have --edit-- finished we could well see such speculators exit in droves collapsing the market very quickly.

There are layers on layers of gambling going on in just about all assets world wide as speculators chase high returns. Such actions de-stabilize an economy on so many levels.

Just imagine a NZF and Labour lead Govt policy combo, tax loss ring fence, door slam on overseas buyers, decrease in immigration numbers, increased tenancy protection, extended flipper tax window, and a govt funded state house building program for affordable housing. Lets not forget all the talk of higher rates etc, China continuing to tighten capital controls and recovery (show me the money....or volunteer for organ harvesting) and the crazy lending all on interest only. Property bulls feeling the stinky breath of the bear down their neck yet, or is the "they're not making any more mate, it always goes up mate" music still making reality blurry...?

Those with high equity, and secure income and good loan structure will have no worries. Those stupidly leveraged (and there are plenty), those with significantly reduced income (talked to any RE Agents lately), and those on low interest and interest only tax offset ponzis will be getting lined up by their Banks for the flusher.

End of the day you will vote for the few (bank profits and specuvestors debt farming combo), or vote for the averageman (kiwis working and paying tax in NZ). Simple choice.

a) has to be 3 way Labour-Green-NZF though watching Labour implode maybe 4 or 5 way. By itself I think this is a slam dunk National 4th term now, but b) you are right with all the other happenings it make sense to exit anyway and I think we are seeing that. Certainly if somehow the Left get in it could turn from a stubbed toe event into a blood bath.

Absolutely Double-GZ, Prices could drop by 30% and most people wont even notice unless they sell. Plenty of parts of NZ have probably dropped 10% already if you tried to sell today.Supply and demand wont underpin the correction, there are plenty of houses for sale..

Exactly right Jono33. I seriously don't give a toss about the so called 'correction' as I'm still living my life like I normally do. Some people are describing it as if the houses are now less precious and we can start knocking things around, making a dent or two on the wall and poking holes in the ceiling *yawn*

Yes, the "I'm alright Jack" attitude is a natural reaction among most people. How falling prices impacts on economic activity and the sheeple's collective sense of self worth is the bigger issue. It's not the kind of topic that the media and govt relays to the public as they typically don't have any idea as to the implications. These are the kind of issues that the Robert Shillers explore and what you hear about in the aftermath of asset price bubbles.

People will notice. For the vast majority of NZers their house is their sole financial asset. If that asset lost 1/3 of its value, it would bother you a lot. Wallets with would slam shut.

It's laughable to suggest that people who relish in quoting their ever increasing CVs at each other (gosh, ring any bells) wouldn't care if those CVs went into reverse.

The Q is if there is a 30% drop in values are the NZ banks still solvent? I'd like the answer to that one because if they are not its starting to look very messy. Given the OBR framework then with a 30% drop it would be sensible for depositors to leave?

Personally my view is long term we are going to see a 60~75% loss of value so any whimpering from a 30% loss will turn into very loud wailings as most depositors lose their shirts.

The stress testing by RB apparently showed that banks could sustain a circa 40% fall in house prices, with all that implies for delinquencies, and still be solvent. At 30-40% there will be mass negative equity and the wider economy would be in real trouble. Plenty of people would be walking away from loans they no longer could service, or no longer wished to service.

Of course, every regulator in history has said similar just before the banks collapsed, "the banks are well capitalised, bla bla". I am not aware of a market where these types of falls have not led to a banking crisis, maybe I am wrong. I am not saying the RB is wrong, I would however say that merely because they say it does not mean they are right. I think one of the scenarios the RB should have tested is what happens if there are simultaneous property downturns in Aus and NZ, and the Aussie banks get into distress in Aus. We are pretty much on our own then, the Aussie govt and regulator will not bail us out. There are people in the market who are betting on an ausssie banking crisis of some sort in the next few years ie short selling the banks.

If there are big credit events for banks I do see how the govt can avoid giving a guarantee for deposits, up to a cap. The alternative is a bank run which will infect the whole system.

The value of the properties are not on the bank balance sheet - this is just a reflection of risk. It's possible loss provisioning will go up, but there shouldn't be any solvency issues.

The weighted average LVRs in the big banks are still pretty sound per RBNZ and the capital adequacy is good. Of course, RBNZ could respond by requiring more capital... which, if anything, would make deposits "safer" because they'd need to retain them

What's your view on the RB stress tests? Maybe u have more insight on them than I do. I can't say the are wrong, but historically regulators have a pretty poor track record in credit bubbles of vouching for bank strength. If they aren't testing for severe bank stress in Australia I don't think the tests are very complete. Any assumption as to parent co credit support may be optimistic.

Haha no it won't, you're confusing the increase since 2007 compared to decrease from now.

e.g. price rise of 60% on $1m house since 2007 equals $1.6m now. Price decrease of 60% on $1.6m house equals $640k house.

It's actually about a 38% decrease from current prices that gets us back to 2007.

75% loss of value? I have a nice brick and tile rental worth about 720K. If it went down by 75% it would be worth 180K. That's one year's income for a lot of households. One year's income for a nice house! You could get 25K in rent from that property which would be about 14% return. If you bought it on a 100% mortgage it would net you about $300 a week. That's why it wont happen.

This highlights the flawed paradigm we have (and why I believe we're in a bubble)....you think its okay for it to be worth $720K but it's outrageous for it to be worth $180K.

Real value is probably some where in the middle....But if you're caught up in the mania, then yes, its definitely worth $720k.....

Haha yes this very much a LOL! situation isn't it DGZ. I think you understimate the ramifications of a property bubble if this unfolds how it has the potential to do so.

Couple of terms to google because suprisingly you appear to be unfamiliar with them, despite permanently being in their presence....

- Narcissism

- Greed

- Foolishness...

There are currently over 50 listings in TradeMe with either 'DGZ' or 'Double Grammar Zone' or 'Grammar Zoned' are you saying all the vendors are Narcissists too because they approved the wordings? For example this one:

DGZ GARDEN DELIGHT

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

And this over stated idea about houses always going up, don't forget every time there's a boom a medium price for your area might be X , at the beginning of a boom but there usually heaps of work done to old houses and new houses built normally taking the values of houses up by simply making them better, I've had plenty of houses, done no work on them and they have hardly gone up 4% per year, BUT IF I HADNT BROUGHT THEM FOR LONG TERM I Probably wouldn't have saved the money so I'm happy to be a long term investor , I guess flippers are ok because they feed on themselves on the way up and last one standing losses, but others get dragged in

http://www.rbnz.govt.nz/statistics/s32-banks-assets-loans-by-product

When you have so much recent debt created at the peak there will be a lot of negative equity out there. The poor FHB's and mom and pop investors suckered into buying overprices crap boxes in the belief it will go up forever.

There goes the neighborhood... https://www.youtube.com/watch?v=dG6yQZ1QIRs

Well let's look at this situation logically. We all know that property prices are falling, particularly in Auckland.

We all know that the average income for a couple in Auckland is around $85k and $60 for an individual in Auckland (Sorry if I'm concentrating on AKL but it is the epicentre of the problem).

So the maximum borrowing capacity if they have a deposit of say $50k is going to be around $500k when all is said and done.

Logically you are looking at a -40% decrease for Auckland over the next few years. Plus it would be rather pointless allowing the banks to be more flexible with LVR rates that will just lead to people defaulting on their mortgages. Though the banks could drop their rates that would help people to borrow more.

Personally I think we're better off to bite the bullet and let property prices falling to realistic levels.

Agreed, otherwise if mass inflation on everything to catch up the imbalance which will be far more damaging to everyone, and especially damaging to retiree's which are now a very large voting block. Its understandable that anyone who is long on property and expecting the last 10 years of capital growth to continue, could have trouble accepting this. Leverage in bidirectional.

Crux of the election. Vote for banks profits and a speculator inflationary bail out, or vote for a return to normal price to income rations. Everyone will vote for their own self interest, that is democracy.

If you are being logical you need to use the average household income for owner occupiers of property. What people earn on the minimum wage and other low income professions is irrelevant, as going forward not many minimum wage earners will be owner occupiers of property. As home ownership rates falls as it is in NZ, property ownership every year is more skewed to higher income earners, so the average income of owner occupiers will be rising (assuming high earners are more likely to own their own home). Also need to factor in the average mortgage for owner occupiers if want to go down the affordability path, as not every person buying a home for themselves is scraping together the minimum deposit. I believe the average owner occupier mortgage is in the 50-60% range, as many owner occupiers have built up equity. They may live in a $1 million property but may only owe $400K, as they have built up equity over the years, via previous property purchases, other investments, inheritance etc.

Im not sure I understand the gyst of that.

So its all about the high income earners, and houses only being affordable for them.

Who cares about the rest of NZ.

Im not sure that makes sense as well, as surely we want all NZers buying houses, and even high income earners want the value of houses lower.

I may have this wrong so apologies.

Double-GZ , ok you're a glass half full guy , everyone on here have had ear full of that and your little area for a long time, BUT that was a boom, it's not now, if you can't handle lots of people's questions and problems and answers and worries over a correction maybe you should rethink the site you are on, people that brought from 1850 to 2014 probably would be ok if they didn't use there house as a ATM , but thats not what this is about

I'm going to use some very simple maths (no negative gearing, interest only mortgages and arbitrary growth across all properties) to run through the problems of our current housing market as I see it.

Mom & Pop bought their house for $200k, they've paid off their mortgage, despite never earning exceptional money. 4 years ago it was worth $1m.

4 years ago they bought investment house 1 for $500k, they used $100k of equity in their own home for a deposit. They now have $500k debt and $1.5m assets. Prices rise $150k that year - they still have $500k debt but now have $1.8m assets - $300k in a year, this is great let's do it again.

3 years ago they buy property 2, using equity in their existing assets, price is up to $650k, so they borrow $130k from their existing assets. $1.15m debt (2 investments and their own home), the houses rise again $150k so they now have $2.6m in assets. Awesome $450k this year, let's have some more.

2 years ago they buy property 3, price is now $800k for a comparable home, they borrow $160k from existing equity as a deposit. They now have 4 houses and are $1.95m in debt, serviced by tenants paying off interest only loans, prices rose again by $150k so their assets are now $3.55m. $600k profit in a year, so great right now.

Prices start falling, they still have $1.95m debt, but their assets are now only worth $3.2m, another month of falls and suddenly they're looking at $2.9m assets. Prices drop to where they started their glorious investment strategy, they're left with $1.95m debt on $2.5m of assets, they're actually worse off than they were when they started.

They had $1m now they have $550k (their original home is still worth 5x what they paid for it), they sell all their investment property and owe the bank $450k because they used their existing house as collateral. Mom and Pop are now servicing a mortgage they can't afford on their family home, which was mortgage free 4 years ago. Mom & Pop could never afford to own that many houses. Mom and Pop are screwed.

Indeed, not just them. It will come down to a classic can kick down the road and make the children and grandchildren pay for our stupidity call as mon and pop "investors" demand their losses are made good as their parents, the OAP "investors" demand the Govn guarantees their deposits. Then the shareholders in the banks also get bailed as "we cant allow the pension industry to go to the wall" panic by Govn. Then the FHBs in huge negative equity also demand relief.

At some point this mountain of private debt cannot be taken on or has to be defaulted on at some point down the road when the Govn of the day doesnt have the income to pay it.. Sadly those ppl causing much of this will actually probably dodge their fair load of the pain they caused from their greed.

Mom and Pop are likely to be earning 180K and only shelling out a few hundred a month. Why sell when it would cost you more? Just sit tight and wait for the prices to go up again. The years go by quickly when you are a bit older. Rents will rise and they are likely to end up being positively geared. In twenty years they end up spending a few weeks in the Bahamas or somewhere like that every year.

But Yvil - what about the 60 years before that? Or are you going to base your trends upon what might have been a signficant anomoly?

Here's the USA (note the significant anomoly that was their bubble):

https://caldaro.files.wordpress.com/2011/01/case-shiller-updated.png

{kind=link}

And Yvil - looking at that chart it would appear we had 'normal' price appreciation up to about 2000 or 2002/3, then since then we may have had an anomoly on top of an anomoly....very bold to suggest the extravagent price appreciation we've witnessed the last 15 years is the new normal - it simply can't be because debt creation and salary growth can't support it (and that's not head in the sand mentality, that is most likely a reality)..

The first bubble can be explained by this piece (possibly the second as well),

Are these real or nominal values? Who could tell. All it shows is that since early 2000s there has been persistent and extraordinary increases in house values. So what, we know that already. The question is, is that trajectory permanent and will any current gains be lost in the future? 10 years of those gains relate to QE and historically low rates. A similar US chart would show a similar climb, a spectacular crash and then a long period of static or moderately increasing prices. We didn't have that crash in 2007. Are we therefore immune to real term price falls? No. Our bubble kept growing, now we are at the point where it can plainly not be sustained and the wheels are slowly but surely coming up off.

Sell up and recognise your gain - oh but then the whole market has gone up so you haven't increased your purchasing power one little bit so in reality you're not better off than you were before...hmmm what to do......

What I will find highly entertaining is if all these 'investors' sell up and have cash in the bank because they don't know what else to do with their 'gains' - only to end up in an OBR event as a result of a down turn if/when they do sell.... I think that would be suitable karma...

But you've probably just received the best ROI ever (literally, that can't be repeated - you've essentially won lotto..) so now is the time to sell...your future ROI on that same asset is only going to get worse - it can't get better....unless of course you think we're going back to 10,15,20% p/a growth on an asset class that the bank won't support through credit and through which the local population can't support either through income..?

OK Zachary let me make it even more simple for you - Mom and pop didn't have, don't have and never will have the money to service those houses. They have been extended a line of credit - Mom and Pop are the new financial crisis, banks have loaned to investors who could never afford the properties they bought, much like the banks loaned to "home owners" who couldn't afford the properties - subprime mortgages. Banks have merely taken subprime up a notch, to people who "on paper" could afford those things - they can't, could never and will never. The last GFC removed lower-socios from the mix, the coming one takes out the middle class.

Take a deep breath mate ... dont assume something you are not sure of ..

"banks have loaned to investors who could never afford the properties they bought, much like the banks loaned to "home owners" who couldn't afford the properties" ... there is no such pig in NZ that can fly .. We are not the crooked US .... where daytime robbery is a national sport , and the biggest gang leaders there are the Regulators!! .....

Banks HERE are not idiots and DO NOT LEND money to people who cannot service their loans .. and they check on them every 6 months to see that they are still employed or have enough and adequate income to service the loans ..... you could be forgiven for listening too much to this kind of crap and BS on this website from some ignorant and blindly biases people, but you might like to do some asking around first before assuming and dishing out such lies ... ask your bank or lender for a loan today and prepared to be shocked about what their requirements are !! ..BTW this has been going on since last Sept. but getting very tough recently .... One of the major causes of the current property slowdown is the tight lending ..

Assumption is the Mother of all Stuff ups ( to put it politely) !!

Since last September eh? Wow, that's rigorous and clearly stopped all the lending prior to that! You're clearly in safe hands... Remind me again when did the property slow down begin? Take a breath mate, stop beating the property drum and see what's in front of you.

You don't get it do you Eco Bird. The reason why the banks have tightened up their lending especially to speculative investors is to the absents of top end foreign buyers who have flown the coop since the start of this year. They were the ones driving the Auckland market and pushing property prices to unaffordable levels since there seemed to be no limit to their spending budgets.

Now that the big spenders are gone, the banks can no longer take the very high risk of lending to local property speculators even if they have large portfolios.

And yes I have spoke directly to NZ and Ozzy banks about their lending restrictions for local Investors.

They now have to borrow against the individual asset which has thrown on the breaks for most investors.

For the savvy Investors who can afford to wait for the market to bottom out, that's exactly what we're going to do. Why should we pay over the odds and pay far more that a property is worth!

Im not completely sure what you mean but if you mean the banks can only lend against each asset in isolation thats incorrect, they lend against the pool as they always have done. Secondly the tight liquidity you see is the banks following reserve bank guidelines combined with indications the market is topping. There is no evidence that overseas buyers were in control of the marginal price. This topping process looks like every other, price has outrun affordability/yields leading to declining sales, although exacerbated by tighter reserve bank guidelines on LVRs (they dont call it a speed limit for nothing) and responsible lending criteria.

FFS: average growth rate of 5.5% over 20 years?!! I assume you mean in real terms, not nominal?

I mean, if we make unrealistic assumptions, then all problems can be made to melt away. So this time we are not saved by interest rate cuts, but by an assumed real growth rate plucked out of thin air. Nice work.

That is a growth number without inflation stripped out. It is the average net real growth of about 3.65% (since 1986) plus inflation of about 2%. The reason you dont strip inflation out is because inflation effects the house price but not the debt (ignoring interest rates).

Why did mum and dad sell?

Lets assume for a second that mum and dad arnt mentally disabled and hold the portfolio for 20 more years, say at an average growth of 5.5% p.a. Now lets compare scenario 1 to scenario 2:

1) 20% correction - home value $920,000, then in 20 years its worth 2.68 million

2) 20% correction - asset value 2.84 million, debt 1.95 million, then in 20 years its worth 8.26 million, minus the debt of 1.95 comes to net 6.34 million.

In scenario 1 they retire broke and in scenario 2, they retire rich. Hope that clarifies things. Happy investing.

Story: In 1988 I went and stayed in the firms Tokyo ex-pat house ( Roppongi), a stand alone typical 1960's house that could have featured in Teahouse of the August Moon. It was in the firms books back then at $45 mio. 5 years later we had it recorded at...$4.5 mio. Today it's probably worth $25 mio. Time may indeed heal all, but time is finite for all of us and after 30 years, it's been a slow crawl back to not too far of half what it was. "But that's Tokyo!" most people will say, and yes it was and is. And so is Auckland.....Never, is a long time....

Story: In 1988 I went and stayed in the firms Tokyo ex-pat house ( Roppongi), a stand alone typical 1960's house that could have featured in Teahouse of the August Moon.

The mention of Japan usually elicits some dippy response such as "but the population growth is negative and the population is ageing." The fact that Roppongi is one of the most urbanized areas on the planet would not register.

5.5% is a pretty bold prediction - so assuming interest rates don't rise, incomes will need to grow higher than that (given the ratio of 10:1 in Auckland - price to income ratio) - so might need to be 10% or more....not going to happen...so therefore you're assuming growth is going to come from more debt...but we're already up to our eye balls in debt and the banks just won't keep lending more and more....so I just don't see where the money is going to come from to assume 5.5% gains for the next 20 years...in all honesty, I think you're dreaming...

Perhaps you meant 5.5% over 20 years? (5.5/20?)

Its not a prediction its simply the historical (since 1986) net real rate of 3.65 plus inflation of 2. In effect im saying the long term trend will remain in place for 20 years. I dont know if thats true, eventually the long term trend wont be true, but im not smart enough to say if that trend ended in 2017 (it doesn't seem like it will be), so i use standard metrics to estimate the future until it becomes clear to me that the sea change event is upon us and the grand interest rate cycle goes in to reverse (if it ever does). The longest trend estimate is (0.91%*GDP) net real if you are curious. That would put scenario 2 at 4.6 million net, still miles ahead of where they would be with just the family home, that sad case would only be 2.13 million.

You can suppose such things but people said the same things about San Fran in the USA. Saying things is easy. Evidencing them takes a little more work. You could easily have argued Auckland was over priced in 2000 and 2007 and yet here we are. People suppose the reserve bank will not repeat its past but that is an extraordinary claim and it requires extraordinary evidence.

Thank you laminar for explaining all that ...

So @ Independent_Observer, Bobster, Solidname etc .. Was that too difficult to digest ... a+b=c ... or is it that you are choking on your own Assumptions and fundamentals or nonsense comparisons with other countries ??.... this whole story of property investment is a risk profile management based on historical behaviour of a certain market in a certain area ( much like buying an IPO or company shares) ... people who decide to take that (calculated ) risk have SO FAR been doing very well and there is no reason that the future trend is going to be different ... the earlier they buy the MORE secure that investment will be .... the 5.5% is an AVERAGE over long term ( 10 - 20+ years) Investors BUY and Forget ... the only time they revalue their portfolio is when they are about to BUY again.

Indeed, in 2000 and 2007 the Auckland market was deemed to be over priced ( I purchased properties in both these years and in between ) yet these have doubled in price in the last 10 years alone while our Darling Interest Only Loans remain the same... rents have gone up with time to cover expenses. Investors do not SELL, until the last day, or only if they have to !!

Now that wasn't that difficult eh ? .... Oh by the way please stop getting too concerned about Prop Investors ... lol, they dont need your input nor your sympathy !!

http://www.sharechat.co.nz/article/a202f465/nz-property-value-gains-slo…

:) ...School yourself mate, maybe these discussions could teach you something new and you could become better off one day ... real property investors know what they are doing - Lucky or not that is our business and our risk ... Confusing investors with fly-by-night speculators jumping on the gravy train at the last minute is incorrect and unfair , it only proves that you don't know what this whole business is about.

Blind leading Blind actually applies exactly to your case ...( I say that in a nice way)

Few investors here have been trying to educate you lot ( at least correct your views and assumptions to prevent poisoning others with silly theories and correlations), .... so many Investors also have pointed out ( almost everyday) that it is not a gamble ..it is an investment class with calculated risk and a business needed to be looked after like any other in order to grow.

BTW, Investors group together nowadays and form and investment company to be able to buy properties they couldn't buy individually after the 40% LVR !! young people are doing that too to get the benefit of negative gearing and CG ... creative Investing with small income rather than spending - A Free food for thought.

cheers

Clearly not working is it Eco Birdy, your quote "BTW, Investors group together nowadays and form and investment company to be able to buy properties they couldn't buy individually after the 40% LVR !!"

Sorry you're still stuffed! Falling returns on rental yields are hardly attractive for group investment and the NZ rental market is already tapped out which we all know!

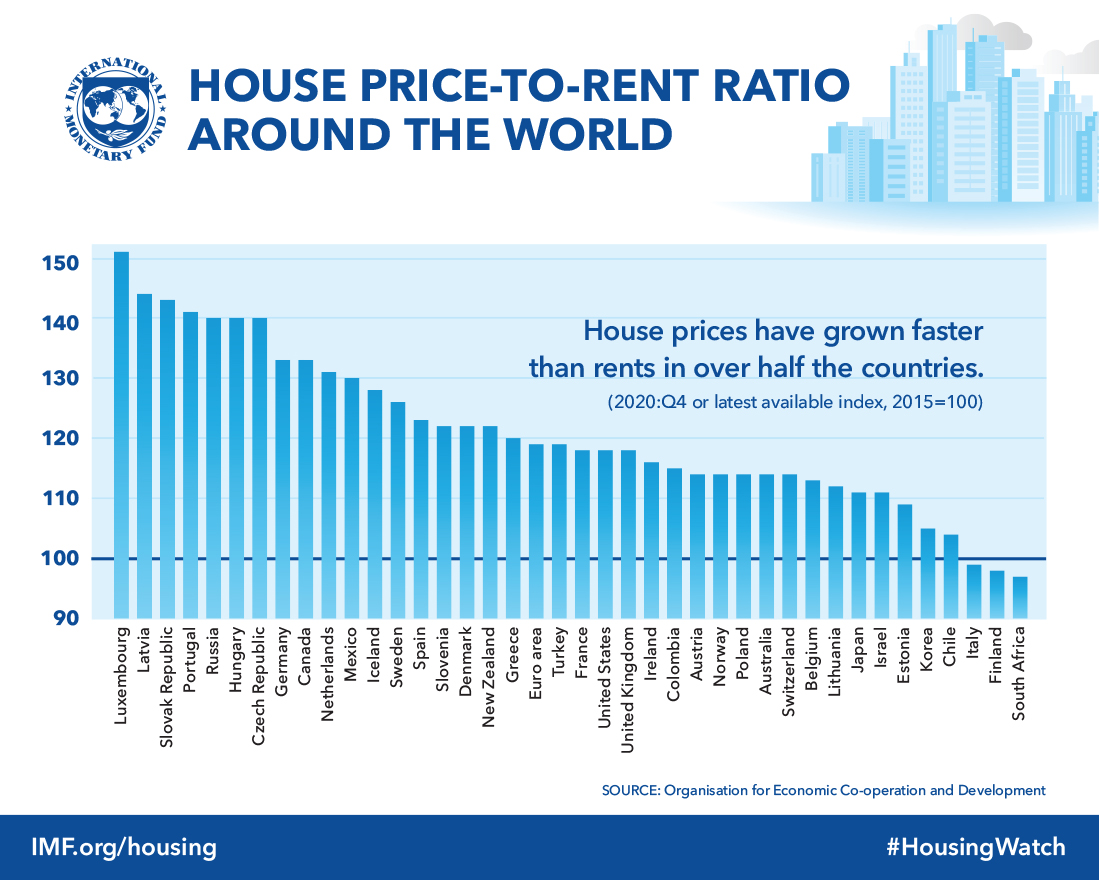

Here are the facts: http://www.imf.org/external/research/housing/images/pricetorent_lg.jpg

{kind=link}

And group purchase for FTB's are highly unpopular, since they don't really work out all that well for the group owners. People simply have to move about so frequently these days to keep up with the global jobs market.

You would know that if you weren't a redundant RE. :)

Out of interest - how old are you Eco Bird and how long have you been 'investing' in property?

i.e. how long is the cape on your darklord suit?

http://www.muonline.info/wp-content/uploads/2014/09/darklord-1.jpg

{kind=link}

Solidname. Only 5% of NZ property investors have more than 2 rental properties. From personal experience even 3-4 years previously, beyond 2 million in borrowings banks very reluctant to lend, despite high non-property related income. So your doom porn scenario is unlikely to work out in the real world.

My "doom porn scenario" is very likely to happen, we're in unchartered territory, QE is the biggest economic experiment we've ever seen, it hasn't worked - interest rates will not stay this low.

I've not factored that into my very simplistic equation, this is neither envy, nor jealousy. It's a fact - houses are unaffordable and people have taken on more debt that they can manage. Despite my salary also being easily top 1% and my wife's being double mine, ooooohhh look at me...

This is great news for the country as a whole in the long term. In reality, capital appreciation in real estate doesn't really have any net gain to the prosperity of the general population in the long term - particularly as it negatively affects the generations to come.

The same appreciation in our stock market, technology startups, primary sectors and innovation would have a much much better effect.

Capital gains are not really disappearing, they are being masked by price distortions within the Auckland market. This period is a transition away from Auckland's rapid cost inflation boom to the rest of NZ where there is a slower more traditional type boom occurring.

The Auckland cost inflation boom was much easier to invest in and a lot quicker growing since it required no effort (buy land + do nothing = profit), but it was not sustainable as nothing of value is created. The Auckland cost inflation boom has peaked and the city is now highly unattractive to invest in.

The traditional boom occurring in NZ outside Auckland is happening slower, because house prices go up based partially on increased value as more new houses get built nearby.

What happens now is the prices in Auckland will lose relative advantage to the faster growing cities of NZ for the next 20 years as more value is built in places outside of Auckland than in Auckland.

Actually Zachary I realized that property prices in Auckland had gone far beyond where they should be, completely decoupled from wages which leaves them completely unsustainable, especially now that the top end foreign investors are gone. So you and Yavil are stuffed more so than most NZers. :)

@Laminar: And that's how property prices get decoupled from wages along with a huge influx for foreign buyers who take to property asset stripping popular cities until they're tapped out as Auckland is now.

At the end of the day Landlords and banks still need people with good stable wages to fill their boxes if not the whole economic system will collapse. If the cost of living gets too out of hand and people simply can't afford to live here, those wage supplying companies go under and then we're in a recession that we can't recover from. Hence why it's better to bite the bullet now and let property prices drop to affordable levels.

Not sure if you've noticed but even the current Government is expecting a sever property correction for AKL. Take a look at the recent rates reassessments a lot of the CV values haven't changed.

assumptions yet again !! who gives a shite if they are coupled or not ... Look under your feet man !! go and have a look at the price of your sold properties today !! if they were even at the same price you sold them at , then buying them back today will cost 2X RE fees and legal, etc lol, that would be about $30K - $50K a piece ( you know that your purchase price includes the sellers RE fees eh?) ... If it makes you feel better ,,then keep theorizing and chewing the same old fat .... maybe one day you will realise that you have sold too soon and your theory was wrong ... We shall take this subject up again come October !!

http://www.sharechat.co.nz/article/a202f465/nz-property-value-gains-slo…

You really are loosing it aren't you Eco Bird judging on how you're attacking people on this site. Look I know you're stuffed but the facts speak for themselves, you can't just keep on ignoring them.

We're pretty much in property correction territory already; look at the recent Realestate.co.nz figures. Auckland's property asking prices have been sliding for over five months now currently down -7.7% and falling. Auction results have been terrible with tiny sales volumes.

https://www.interest.co.nz/property/89054/downturn-aucklands-housing-ma…

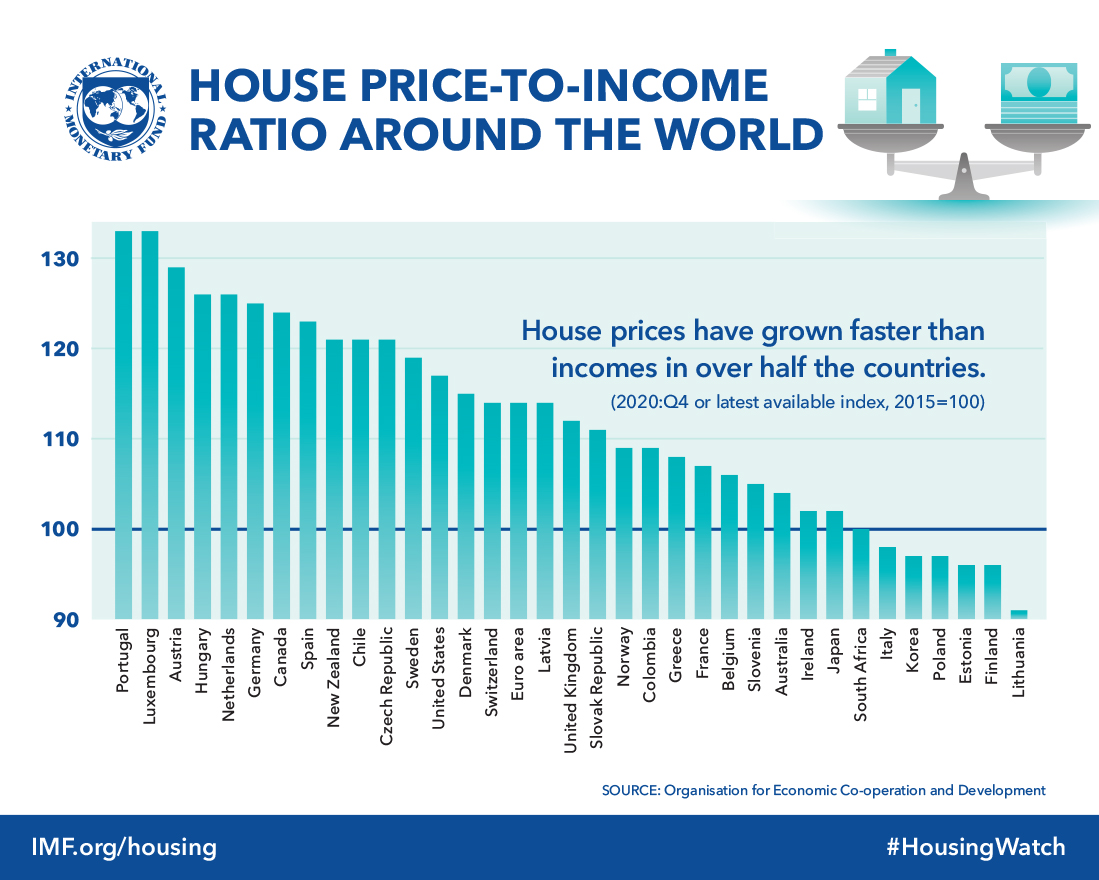

Even the IMF recognizes that we're the most over prices country in the world. So I am very glad that I sold and got out around the peak of the market thank you.

http://www.imf.org/external/research/housing/images/pricetoincome_lg.jpg

{kind=link}

Do you honestly think that the market is going to turn around in the Spring time (October)? That's highly unlikely, even if National got in it still wouldn't make the slightest bit of difference.

The AKL market needs to bottom out to affordable realistic levels and that's what's happening.

lol, I am not losing anything mate ...and not attacking anyone, just call it as it is, people who cannot stand the heat should get out of the kitchen !!

Without delving deeply into politics ( as you like to do) but after yesterday's fiasco, I think that Nats has more chances of coming back ... not sure why would anyone invite chaos by 3 equally weighted parties ( who are not exactly in sync with each other and two of which are in Damage Control mode) into the NZ politics when the country is doing so Well !!

I honestly don't give a toss about what IMF and similar organizations think, Do, or Recommend - they do not frighten me at all - and they are not exactly the angels they sound - they have their own vested interests.

You have been an investor ( a landlord) and I believe that you will understand this next bit : What will determine the future Price of House Z in the area Y built to Quality X at any given time?? ..... the IMF?, The neighbour's wages? Your cousin's salary? Number of homeless people? number of FHBs looking for houses?? ...

OR the general state of the Economy? .. Government business and TAX directions?? .. Unemployment rate?, Supply and demand? New houses & Building material prices? Availability of free sections in the area? Transport, School Zone? New Infrastructure or New business hub in that area? ??

So who gives a toss at external research or few self serving articles here or there like the ones BH used to write, and some do that now on this site? should serious property investors follow every chicken little running around the place calling falling skies,, they would have been out of business ages ago ... or should we all sell out because Vancouver hit the fan?? or London Properties are declining ... Seriously??

Bottom out ? Sure, I agree !! , BUT, When? and at how much? which suburb? what areas? for how long? we do that on Average or Median prices? And who is going to decide and announce that? The IMF? B&T? or Mr, Eqube ? maybe the RBNZ

Are you serious?? .. you want people to catch falling knives or wait when everyone rushes to buy houses going up like crazy ... Market Bottoms are only known after months or years of their actual occurrence and No one will know without extensive data for at least two quarters seasonally adjusted!! - so that is just like saying the sun will shine tomorrow ....

Here is another bit of free info for you: There are currently heaps of cashed up investors in the market waiting for the dust to settle in September, and these are quietly looking and sieving through what is available the market - buying anything of Value and paying current and even last year prices ( not discounted prices) for some areas.....

I still believe that prices will correct to the Up side come October this year ...Yes, they will pick up .... If the market did not pick up BY December 17 / January 18, then we could almost certainly be for a continued correction of maybe 5 -10% -- many people in this business think that will not happen.

if the Banks keep the lending restrictions to Developers and Buyers for another 6 -12 months or so then it will be choking the supply side more than the Demand and will exacerbate both availability and affordability issues ... IMHO,.House prices do not fall because of lack of buyers, they fall when everyone rushes to sell at discounted prices!... and that is highly unlikely to happen, hence we see the stalled market place we have today ... tons of listing and very few buyers ( at the asking prices) I do not subscribe to the idea that that eventually will lead to prices coming down - Don't think so, A house is not a bike, or a car to sell on trademe auctions as some like to draw analogies from.

There are always two sides to a story and analysis - so we just have to agree to disagree.

You're really rambling and foaming at the mouth Eco Bird. You might want to pour some of that Vodka that you're so fond of on your cornflakes to calm you down (Personally I don't touch the stuff).

Look there is now overwhelming evidence that highlights that Auckland's property prices are dropping and we all know the reasons why they're heading south. Have you honestly seen any evidence of property prices heading upwards recently, I very much doubt it. I wouldn't be surprised if we get yet more articles from RE agencies saying that prices are continuing to fall. You have to look at the evidence, stop ignoring reality.

Proper regulation of bank lending would require that lending is based on income (wages) by use of macroprudential tools such as DTI limits, or requiring banks to lend prudently.

If lending is linked to wages/income, and house prices are linked to lending, then house prices will track wages/income.

Unfortunately NZ does not have adequate regulation of bank lending, so you are correct

"This is fair warning that a real estate agent..... (is) going to be held accountable. Before, it's been a bit loose, but this is fair warning that the accountability is starting to mount....

http://www.afr.com/real-estate/residential/toorak-fight-is-a-warning-fo…

On the radio today still a 6.4% YOY GAINS in national house prices. It also very much depends on where you are as to the effects. Basically its been totally FLAT in terms of gains over the last 3 months. Still think its going to simply Plateau for many people. The types of declines some people are hoping for are simply not going to happen.

Exactly. And the residents of 1071 and 1050 will welcome the upgrade of the intersection of Tamaki Dr and Ngapipi Rd this month - work begins from late Aug yay! https://at.govt.nz/projects-roadworks/tamaki-dr-and-ngapipi-rd-intersec…

Anyone worried about their housing investment in Auckland declining by 30% need not fear. The cost of building is only going up.

Can we expect a flattening? Yes. - A decline? Indeed! 30% - not a chance. Just ask BH what he thinks.

A flattening and slight decline is highly desirable for the country. A 30% drop is not. Be sensible people, whichever side of the equation you are on. I'm on the losing side this month apparently. Funny, I still feel like a winner.

It largely depends on external conditions that we have no control of, leading to supply and demand. Also if the banks raise their rates, then it will affect the amount of money people can borrow, and thus afford to buy. It all comes down to what someone is prepared to pay, as houses don't have set values. Valuations are only based on what the market will pay at the time it is assessed.

Cost of building will come down as the market corrects, its happened every other time. Building companies get in trouble as people bail out and they cant sell stock, they fold on Friday and start up on Monday ....... seen it all before. Anyone remember Blue Chip .........history repeating none of this is new.

On a positive note the NZX hit a new record today with many good shares still paying 5 - 7% dividends and strong positive capital gains.

Except we still have record immigration, levels, and these people need new homes to live in. Builders need staff to build them. There is also not much competition in the building materials market, so we pay more for materioals. Then all the red tape and complainance with building, which is a huge part of a a building cost.

THE PAST AND FUTURE, the past 100 years we could buy a house for 1 years income from ONE person, about 20 years ago that went to 2 incomes needed, we pushed mortgages to 30 years, 2002 to 2007 we pushed the 5x limits , lately we have gone completely stupid , wages are and always will be the barrier, THE FUTURE for long term prices to always lift like the past, NEVER HAPPEN , get this in your head, wages and barrier

In the long run Rob it will be fine, this is a correction in asset values not the end of the world. Over the long term buying a home you like for your family, in an area you want to live in is a great investment. Dont look at the short term just enjoy your new home.

I notice on zagga (the new p2p loans scheme) someone wants to borrow 640K to "refinance", on interest only terms @ 8.89%, an Auckland residential property (68% LVR based on a notional value of 940K ).

I don't get it. Why are they borrowing way over banks carded interest rates? How does that make financial sense to the borrower, particularity in the current Auckland environment?

As an admission that my crystal ball is blurry, I've been incorrectly calling for a downward correction since 2011. Luckily there was no way I could short the market as I would have been a victim on Keyne's observation that “The market can stay irrational longer than you can stay solvent”. Instead, for business reasons, I actually ended up even longer property and therefore have benefited from capital gains.

With that confession out of the way, let me say that now I am sh!t scared of a correction and am therefore looking to sell my primary residence. Let me explain my rationale,

Rental yield is now 3.5-4.0% on Auckland property. Property price inflation has continued to push this yeild down so that in just 3 years it has dropped a 1%.

Rental yeild source is http://www.interest.co.nz/saving/rental-yield-indicator (calc using lowest quartile) but could be even lower, see https://www.barfoot.co.nz/market-reports/2017/june/suburb-report

When you factor in council rates, insurance, depreciation, risk of tenants not paying, management of tenants & down-time between tenants then rental yield should really be a couple of percent higher than TD rates to make it worthwhile. Right now you can get 4.30% on TD for 5years (or bonds in utilities at 6.9%, but I'll stick to TDs). Therefore, I see a rationale landing spot being a correction bringing us back to 6.30% return. That would be about a 36-52% drop in prices.

That kind of decrease is over the top as we expect rental price inflation, given continued housing shortage, and because of cultural preference in property over other asset classes (especially demand for owner-occupied because it is much nicer to own your own home) you could say 1% over TD is more appropriate. But even if you half it to 18%-25% that is a scary fall. And once it starts it has potential to run off its on momentum and be irrationally lower with higher yield than should be the case.

Therefore, I'm now looking at selling our house and renting (although I'll still be long property for commercial reasons). I can tell you from browsing trademe that it is not easy to find a good rental but even at these crazy rental prices I still think it is worth it to avoid being over exposed to the potential crash. If nothing happens, no drama for me as will have the TD money + gained on property I do have. I feel truly sorry for others not is such a good position, such as recent new home owners, and believe that for me, and most people like me, it has been luck more than anything that got us there.

Sorry to interrupt your lovely story but I think your right, that crystal ball is still a bit blurry and might use a bit of polish ...

You missed a couple of things, but the most important one is that at times like these ( just like 1999 and 2007) a huge disconnect happens between price and yield due to the fast rate of price rise - never in NZ property market even in its darkest days have property prices dropped by 20-30-or 40% and certainly a 1-1,5% drop in yield does not necessarily change the Value of properties by that much- to prove that, Investors are still happy to buy at 3.5 - 4.0% at present.

Not sure why you dropped Expense claims, depreciation, and CG or rent rise from your calculation - these are (on average) 5.5% higher than TD add yield and you get more than 8.5 - 9.0% pa ... But dont take my word for it.

Good luck with renting, it is certainly a great and cheaper option ( not from investment point of view), but what you gain on the road you lose it weekly in "Rent".

Eco Bird, I think you might have your cause and effect mixed up. The huge disconnect in yield is a result of purchases (demand) that were in excess of what it should be given the rental return. People may buy at low yield because of an expectation of capital gains - something that becomes more and more risky the further you stray from good yield (as reach top of cycle) and then drops completely when capital gains fall away. It is an effect of irrational buying not the cause.

Anecdotal evidence of some investors buying in this environment does not match the stats which show a slow down - i.e. the data suggests less investors are buying now (slow in demand) unless you have stats which show otherwise?

How do you get 3% additional yield from expense claims & depreciation? Rent rises are not a certainty, and even a 10% p.a. rise would add only 0.35% to the yield.

I'm very open to counter argument because I have skin in the game, and want to make the right choice, however the numbers still point to me to there being a risk of a 15-25% decrease.

Here is quick bit of math that illustrates some of the more subtle effects of houses vs term deposits:

Net Yield 4%

Inflation 2%

Interest rate 6%

Tax rate 33%

House price $1,000,000

Buy @ $1,000,000

Year 1:

Interest cost $60,000

Net income $40,000

Loss: $20,000

Tax adjustment: $6,600

Adjusted loss: $13,400

Price rise $20,000 (inflation only)

Capital gain: $20,000

Change in net worth: +$6,600

That example is a very simple way to demonstrate that there is much more to it than yield comparison. Most here would guess that purchase would have equated to a huge loss, they would scream the property is over priced, and yet the investor walks away almost 7K up. That example requires a gross yield of about 4.7% which isnt common any more in Auckland but it serves to illustrate that just looking at interest and yield hides half the picture.

Ok, thanks for taking the question seriously. Would you invest with those numbers?

I wouldn't as the 20k capital gains, 2% above inflation, is not a guaranteed return. the 20k inflation is a likely average over time, but not in current environment, however capital gains above inflation, specifically rent price inflation, cannot continue indefinitely else as it will decrease yield further. In a market the rental yield should remain reasonable parallel to yield on other asset classes (yield comes down across the board then naturally have asset prices increases but should be reasonably evenly distributed over classes). I take the point that yield can be consistently lower on property given tax incentives (and other homeowner benefits vs other asset classes).

Subtract rates, insurance, depreciation, down time between tenants and general risk of global downturn impacting property (same applies for equity) and it doesn't seem preferable over TD in my view.

I think time horizon matters a lot here as well - I'm looking at only a 5 year period from now.

Question, would yield would it take for you to sell?

One thing I have noticed is that it has always been very easy to talk yourself out of investing in property. I remember doing this exercise twenty years ago and coming to the same conclusion. It was only when I accidentally found myself to be a landlord for a couple of years that it began to make sense.

Yes, I agree - I was doing similar calcs from 2005 to 2008 and it never made sense so stayed out of market but probably would have benefitted from getting in earlier. It was only in 2009 that I bought as numbers made sense.

It's true that at most times in last 20 years if you jumped into the market, even when yield numbers didn't stack up, you still would have benefitted considerably (mostly from capital gains.) If you think that our recent history of property is best indicator of future performance then I see your point. However, if you think that we'll see a return to more consistent yields across asset classes, as markets should dictate, then I think the numbers hold true and we have to see a fall in prices.

Something else to consider - especially if it concerns your primary residence.

If you mange to time the market well ( difficult as you already know ) renting may stack up cheaper for a while. Sooner or later someone in your position is likely to want to buy back ( as a renter you lack control etc. etc. ) . Transaction costs involved in both selling and buying are not trivial .

Ill just note the part where you claim that 'markets should dictate' (a return to historical yields). Markets do not dictate a return to historical yields unless the long term interest rate trend reverses. Its hard to see governments and the private sector, saturated in debt, allowing the reserve banks to do so which out blowing up the planet, and reserve banks do not often choose to blow up the planet.

Lastly ill note that the idea of a 'historical yield' is in itself a falsehood. Actually what you are referring to is a historical margin and margins are not as stretched as yields because interest rates have changed substantially.

@hamsterintheclouds: My comment is only to illustrate some of the math and why yields on property are only half the story. As to what you should do, because I do not know your situation in great detail i dotn know. Ill say that in general time frame is crucial and housing is a risky asset class that can take a long time to recover losses so any investment property purchase should only be done after careful consideration of the risks and how that could impact on a persons life.

To address your other points though, growth in housing should generally exceed inflation because there is likely genuine growth in GDP.

Capital gains cant exceed rent growth forever thats true, but in order for that to stop interest rates need to change their long term trend, and thats a hard call to make.

So Eco Bird - correct me if I'm wrong - your logic being applied to housing is that its never experienced a signficant correction in the past, therefore it will never experience signficant correction in the future...?

You crazy....

'I've never had a heart attack before, so based on my history, I shall never have one in the future.' Sound like good reasoning...

It means that he isnt just guessing. Look at it another way, if you have never had a heart attack, what are the odds you have one tomorrow? The day after? The year after? How long would you be wrong before you were finally right? Suppose you choose not to go to work because youre sure you are going to have a heart attack soon. How much income would you have lost by the time you actually had the heart attack? How much lifestyle have you missed out on? What if the heart attack never, even, happens?

To continue the analogy, it does feel a bit like we are an obese, heavy drinking, smoking and unfit 80yr old man right now so chances of collapse are up. I would not be risking any intense exercise right now. You do adjust your behaviour based on chances of a heart attack and so you should with chance of house price fall.

Serious property investors mostly just buy all the time whenever they find a good value purchase. They are in effect always 'averaging in' to markets with slightly increasing buying as prices falls and slightly decreasing buying as prices rises. So in that sense youre absolutely correct. However in the background there is the looming possibility of the sea change event, when the grand interest rate cycle goes in to reverse, if it ever does, and that is more what the arguments on here are about. Is this a regular correction or a grand sea change.

You have to go with Eco Bird and history I'm afraid. The backside fell out of the USA so badly in the GFC and it hardly touched our house prices. Short of another world war do you really want another event that big just so you get to buy a cheaper house ?

You short sighted...

Really Carlos67!! I was cashed up before to the GFC and could buy land at half the cost prior, any money I have ever made on residential property was purchased at the bottom of the dip. No buyers and lots of stock, when the market is at that point it can feel like it will never recover (hard to believe on the way up). This is a normal cycle and given a major event will play out as normal with winners and losers along the way.

If anyone wants to take comfort from history it is that the market has always returned to the long term average. We will probably overshoot on the downside, as others have said, but the market will recover to the long term average over time. Its a long game remember. Happy investimg.

Jono33/Zach/DGZ and Eco Bird are all correct. This is just a typical real estate cycle. Have a look at past data!! Its all there. Price growth will start again around 2020. I have 7 rental properties purchased in 2005/6. Rents are now 420 per week average for my house and units. All debt and other expenses are paid for from rent plus I make 60K taxable profit. Yes Trump could cause a war and that might make things a bit riskier but all investments would wear that sort of risk. I remember when people were buying houses with 150K loans. I thought they were mad at the time. I soon caught on. I dont know if there will be a huge drop in prices, but right now I have enough equity to get through a 50% drop. Rents are going up, immigration is pushing demand up. This is going to keep going even if they stop immigration within the next few months. So whats the risk really???

I agree with you Mr. Chew. I just had a tenant asking for 12 months extension so I have raised the rent by $30/week for this particular rental. I thought my B&T Property Manager would take some time to negotiate with the tenant but no, they accepted the increase straight away. So there you go, immigration is definitely pushing the demand up.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.