Nearly 100 Auckland suburbs have joined the million dollar club, following the latest Auckland Council rating revaluations.

Those are suburbs where the median Council Valuation (CV) is $1 million or more.

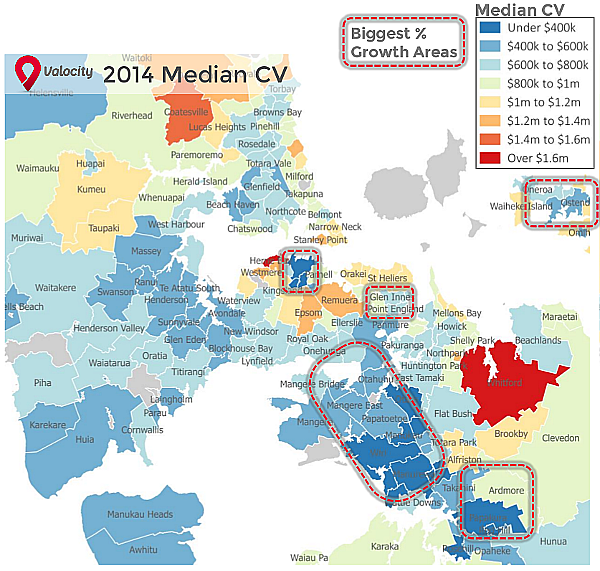

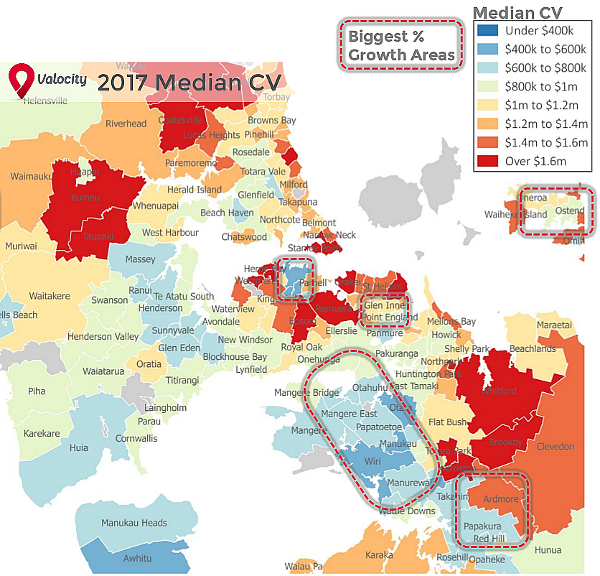

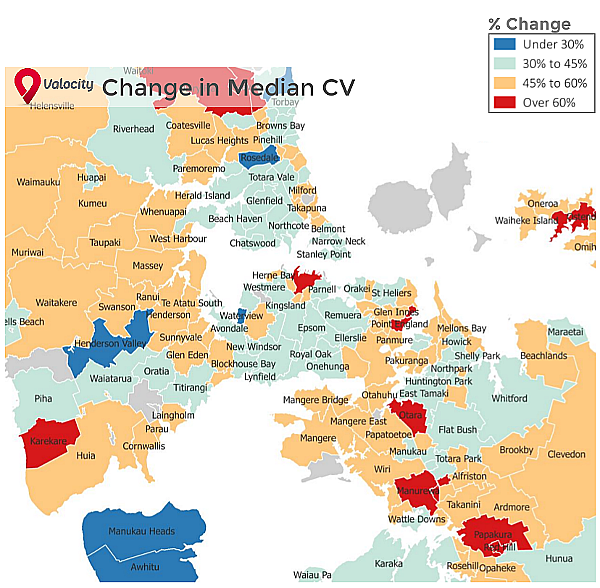

Property valuation and data company Valocity has created maps which show the upward drift in rating valuations throughout Auckland since they were last issued in 2014, and the new valuations that went live on the Auckland Council website this week.

A notable feature of the maps is that areas in the 2014 median valuation map coloured dark blue, denoting that the median valuation was under $400,000, have completely disappeared form the 2017 map.

And in the 2017 map, there are now far more areas colured red, denoting median values above $1.6 million.

Other trends noted by Valocity are that Central Auckland was one of the biggest movers, indicating large growth in apartment valuations, while the biggest growth in city fringe suburbs occurred in Glen Innes and Point England.

There was also generally strong growth in the south east of Auckland, its western suburbs and on Waiheke Island.

Only a handful of suburbs had growth below 30%, including Waterview, Rosedale and Long Bay.

Median Council Valuations in 2014:

Median Council Valuations in 2017:

Percentage Change in Median Council Valuations 2014 - 2017:

77 Comments

The LVRs need to go ASAP. How is anyone supposed to buy anything when you need a $200,000 deposit.

Translation: send mo' munny. It's plain to see the house prices are the problem not credit availability. Just look at the names of the real estate agents and it's obvious who needs to go. Then you've got the hostile councils and ripoff building materials.

People must be doing it though.

Woohoo, million dollar mortgages all round. That will solve the problem.

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=119…

I’ll give it 3 years & they’ll be some real change from the current ponzi

Unlucky for those you failed to catch the peak and profit

They’re left to make excuses fudging statistics to justify their stupidity

Prices will most likely be higher in 3 years than they are now

Why?

Every wage and salary earner is going to have a legislated pay rise of 100% am I right?

Hi Yvil,

I believe you'll be shown to be correct.

Notably, none of the credible forecasters are picking a fall in (average) house prices.

RBNZ is picking a 2% per annum increase over the next 3 years. (That may well be the order of magnitude that transpires.)

TTP

I thought anz were picking a 12% drop.

Why are they not credible?

Hi Fritz,

Anyone picking a 12% drop is certainly not credible.

TTP

Hi TTP, I feel anyone that predicts a 12% drop is being conservative! Seriously, do you think Infometrics very own Gareth Kiernan is not credible? https://www.interest.co.nz/property/86171/nz-house-prices-look-set-fall…

In your eyes, are these people not credible either?: https://www.interest.co.nz/news/87027/moodys-says-house-price-increases…

Of particular interest is what the NZ Reserve Bank said in 2015; The absence of a severe housing market downturn in the last 20 years is not evidence that one could not occur. House prices have reached unprecedented levels relative to income in Auckland, so historical New Zealand downturns may not be a good guide to the consequences of a future severe downturn. This leads us to look at other countries that have had severe downturns. While origination practices in the US and Ireland differ from New Zealand in important ways, we still consider that the empirical evidence from those downturns is relevant to considering what would happen in a severe New Zealand downturn.

TTP, these people ARE credible.

Hi R-P,

Gareth Morgan is associated with Infometrics........

Enough said.

TTP

Also, I'm very weary of anyone who thinks what happens in given countries abroad is likely to be mimicked in NZ.

American-fried Kentucky theory need not work in NZ. And the same for Spain, Perth, Ireland and so forth.

There are a number of structural factors that impact on NZ in quite different ways than they do for other cities/countries. You should be able to work that out for yourself.

TTP

Your weariness around the view that what happens overseas must happen here is well placed. However, your view that NZ is unique and could never experience a bust is not well placed.

You take a very black and white view of the world. The world is hardly ever that simple or predictable.

In living memory, NZ has never experienced a property bust/crash - and there's little to suggest that the situation is about to change.

If I saw a crash coming, I'd certainly be vocal about it. But I'd need good evidence first.

My personal desire for a crash (so that I could buy up property cheaply) is not sufficient reason to go around the place shouting that a property crash is imminent.

TTP

TTP, once a serious slump ensues, for the over leveraged its already too late. Through limited insight, your suggested vocal warnings would come after it had arrived!

I agree. In New Zealand you can't just walk away from an interest only loan and hand the keys back to the bank. In America that is exactly what many did do because their loans are "non-recourse". In Australia and NZ, we have "FULL Recourse Loans", which means borrowers are stuck at the price point that they purchased at, regardless of whether or not the property value increases or decreases. But either up or down, the Bank owns you until the day that debt is repaid in full, even after a a forced mortgagee sale in a declining market. Our banks will also legally bind you to pay off the difference in any outstanding loan, should the property sell in a declining market.

TTP, that response was a bit shallow. Is this your way of expressing sympathy towards feral cats?

These are warnings from well respected and credible sources!

FHB, wait for the distressed sales!

Hi Ttp,

You want infometrics well here you go and you're still screwed; http://fingfx.thomsonreuters.com/gfx/rngs/CHINA-DEBT-GRAPHIC/0100315H2L…

Enough said with real facts!

In your opinion.

I have long held the opinion that anz are pretty much the best bunch of bank economists. That's my opinion.

It's a frankly laughable call by TTP to say anz and Infometrics are not credible. Because he doesn't like the message.

I don't agree with the reserve bank's opinion but that does not mean I don't think they are a credible organisation. And my disagreement with their opinion doesn't mean I think they cannot be right.

Some people have dangerous levels of confidence/arrogance.

If you like ANZ that much - then go bank with them.

But as for its housing market predictions, believe them at your risk/peril.

I have my preferred forecasters - and they might well differ from yours (which is fine).

TTP

That's fine.

But to call certain organisations out as non-credible just because their view differs from yours....well it just exposes you as the troll we can all see you are

Happy to settle that issue by seeing whether prices fall 11-12 per cent.

If economic forecasters get their predictions that far out, then they certainly lose credibility. It happens. No point having warm fuzzies about it.

TTP

Surely credibility should be based on past performance and the quality of prediction methods used not just whether you agree with their opinion? What's the point of a forecaster then if you only listen to ones that reinforce your beliefs? Although I suspect replying to you and calling you out on this kind of basic stuff is a waste of time.

The simple fact is people cannot afford to buy. Who is going to buy if people cant afford to buy. Who is going to buy if banks are not lending.

Saying properties will go up is fine. But you need someone to buy the property for it to actually go up.

I will say it again TTP if your so sure, create an investment memorandum, get investors to lend you money, borrow to the hilt and you will be a very rich man if property is such a sure thing. Money and mouth.

Easy money.

Hi swapacrate,

You focus on the demand side of the housing market. Fine.

But there's also the supply side. Prices tend to be "sticky-down" in the house market, because owners won't sell - unless they have to - when house prices start falling. (It's a kind of built-in stabiliser mechanism.)

No doubt some people here will dispute this - but, in reality, that's been the way the market's worked in NZ for at least the last 70 years.

I won't be taking you up on your challenges in your last paragraph. There's no need to do that and, in any case, I'm not that way inclined. I'm not an active buyer/seller of property - just a sideline observer.

Cheers (and I enjoy your contributions),

TTP

That NZHerald article seems more positive about prices holding than negative. We still haven't seen the breakdown of prices by apartment/houses yet which has surprised me. Was there an unusually high number of apartments sold in Central Auckland last month? Does anyone know a figure like this many apartments sold in September and this many sold in October?

The next challenge is how best to leverage our equity into the consumer economy. When we master that issue, we will have created the most advanced economy the world has ever known.

If you declare your equity then the government will issue that to you in cash. Equity goes up, claim the difference. It’s called growing the economy because money grows on trees and money is economy.

I guess you're just joking, but actually I'm dead serious. Here's what the ASB has to say on the matter:

If your CV increases, you might be able to borrow more against the equity created in the property. For example, this might take the form of a top-up on your home loan for property renovations or the purchase of a new car. ASB may be able to use the CV figure, or we may request a different type of valuation (for example, one conducted by a registered valuer involving an on-site inspection) to confirm the value of the property. Again, any new application for borrowing will be based on your ability to service the additional loan amount.

So based on the POV of ASB, they will support consumer spending based on renovations and new cars by letting you borrow more money.

I'm talking about something more spectacular, like buying that food item you always put back on the shelf.

Borrow borrow borrow! Can’t afford the repayments?? No worries we can put you on interest only because house prices will only double in 10 years time?

Maybe you've just answered my question for me

We can't borrow our way to happiness/prosperity?

Hi Davos36,

Perhaps not - but some will have fun trying.

Seriously, personal/family wellbeing is important and owning the roof over your head can help a lot.

Doing the hard yards to get a home can be well worth it.

Don't be too put off by all the negative comment here.

TTP

I would rather be mortgage free and not have the stress of high debt levels. We will downgrade our expectations to be mortgage free. It makes life a lot less stressful.

Yes - that’s a very good idea, swapacrate.

Keeping life stress-free is a virtue.

TTP

I would love to see Auckland Council lowering the rates with the CV going down...

1) The rates are not determined by the CV

2) How is lowering rates going to help fund transport and infrastructure ?

In 2014 the CV on my property dropped dramatically, My rates did also drop significantly, so much so that I got a note from council that there was actually a limit to the amount they were able to reduce the rates, and my rates would be below it - so they could not reduce it as much as what the calculated amount was meant to be. The rates dropped by a few hundred dollars.

However now the CV is back up by 50% I expect the rates will rise substantially again.

We also received a drop in rates by a few hundred dollars in Auckland just after the GFC in about 2010. Our CV dropped nearly $80K, but this was before the four cities turned into one Supercity. Neverless, those CV's sure amped up again the following year.

Is there a graph showing suburbs where median combined income is greater than 200K? i.e. the "severely unaffordable" 5X income point.

I'm puzzled as to why the land values in Remuera have been blown out of proportion to such an extent that a piece of 320sqm land can be worth $2,150,000 now compared to $1,190,000 in 2014. Is this happening in other suburbs too??

https://www2.aucklandcouncil.govt.nz/property-rates-valuations/Pages/ra…

I agree with Zach re: the credibility of the 2017 CV's. The house values look to be largely unchanged or showing a decrease in value.

Double-GZ, TTP, Zachary Smith, Yvil, are all the same Real Estate Agent trying to manipulate the forum.

My name is Legion, for we are many.

I can't understand why John Wheeler hasn't included my name?!!

Usually, we're all lumped in together - "Villains United".

Now I'm being left out in the cold.......

TTP

Because your comments are so inane and repetitive some people have tuned you out as background noise.

Or, there are plenty of people here who only want to hear about a crash.

And since I don’t do that, they’re keen to sideline me - - or silence me altogether.

TTP

.

No, they are individuals who just agree on common ground. They all have very different writing styles which reflects their different personalities. Zachary and DGZ are definately not the same person!

These new valuations ( CVs) PIN DOWN the current housing prices, meaning that these prices are now here to stay and will only go north of these values in future ( speed and trend may vary but the direction is upwards) ... I bet that every reserve price at any Auction would at least start from its CV valuation ...

July / August was a bottom and these CVs confirm that now ... LOL, my home has now a higher CV value than the estimated one on Home.co.nz ( CV is 10% higher :) - Go Figure !

market fundamentals haven't changed since last July ...the supply is shrinking while the organic demand is slowly growing ... The market has come to almost a standstill after frightening all the Horses ( both buyers and sellers) by creating a chaotic environment full of uncertainty in the housing market ... and this No Activity is the actual Killer - of course the doomers like to think that people will have to sell , so prices MUST come down!! .... or eventually Have to buy, so they will dictate their prices on the market which

in turn Has to accept them!! ... Yeah Right! , However, we did not see prices capitulate and they wont now, Not after an official CV coming from the Council which every Bank and Lender relies on as a guide !

The new minister is still dishing around election campaign slogans - no action is yet to be seen - we keep hearing from the government that " good things take time" and the good old cheese will be distributed by the ballot box when ripened ... sounds like rations!

Early days? , absolutely, but No changes has happened yet other than the Mess we are in ...and indications of tightening the rental market and drying up rental supply by trying to frighten the landlords with the new rental law amendments next year.

So, who is going to sell a $1M freshly valued property for, say, $800K? ... who will have the guts to sell at 20% discount from CV and why should they ??

Should that brave ( or desperate ) home owner exist, how many are there to make a dent to a freshly valued market ??

BTW, Am i the only one who is hearing about plenty of redundancies going around in the last few weeks, or is this becoming a widespread phenomena as some business and service activities are slowing down as reported?

Behold, interesting times and Jokes ahead ...

@ Eco Bird; So, who is going to buy a $1M freshly valued property! None! Your goose is cooked: China’s Massive International Real Estate Buying Spree Is Officially Dead!

https://betterdwelling.com/chinas-massive-international-real-estate-buy…

China’s PBoC Announces An Army of Over 400,000 To Prevent Money Laundering

https://betterdwelling.com/chinas-pboc-announces-an-army-of-over-400000…

China's Debt Problem

http://fingfx.thomsonreuters.com/gfx/rngs/CHINA-DEBT-GRAPHIC/0100315H2L…

Thats it, you can say the house is worth 10 million, but who will buy it. It just sounds like monopoly.

People can only buy what they can afford, and what the bank will lend them. Sounds simple to me.

On that note Swapacrate, I had a little squizz at what the bank would lend me, as you do, a few months ago it was $1.5m which was way too much but still "technically" affordable. Tried again yesterday same data input, loans ranged from $600k to $800k, the tides they are a changing.

Indeed.

My word, CJ099, you are in a gloomy mood tonight.

Relax and enjoy life, my friend. Things aren't too bad at all.

TTP

Actually it's the opposite, I'm in an excellent mood! I'm a Millionaire don't you know but then that's because I own Auckland property. Where as you don't! :P

Good to hear it, CJ099.

Congratulations, my friend.

I'll know where to head when I need a loan. (-;

TTP

Nahhh... I've invested else where so don't have any free capital at the moment, try Zachary. ;)

Eco Bird, good to see you back. I sort of agree with you about the RVs although I suspect people will sell for less than the current RV as they won't be able to get the RV in many cases. Nevertheless they do set a sort of precedent and it's not good news for the anti-spruikers. I wasn't expecting some of the valuations to be so high as Epsom was deemed to have appreciated 42% while one of my properties went up close to 70%. I have a place which I think is worth 1.6M tops yet the RV is now 2.225M. The last RV was 1.3M which I felt at the time was 200K too much. Do you think I should contest it? Or will the high RV be a favourable factor when I come to sell?

Oh Labour are going to have a field day with showing the false economy that National created. Yes mark my words, if Auckland property sells it will be below RV (CV)!

Only a money launder will buy above RV value in Auckland and I'm sure our current Government will be very happy to add them to their list and point them out to the PBoC.

Hi Zac,

thanks, ... i think you should contest an over valued property especially if you have had a recent independent valuation .... over valued property could be useful for borrowing more against it ( while paying a few $$s more in rates) , but in today's lending restrictions that option has gone for a while ... when you come to sell, it will me market value that dictates the price on the day regardless of CV ( as we saw in the last 3-4 years)

I was successful in the past in contesting over valued properties and that worked well for me...

I have found that the new CVs came almost spot on on my home and the rental ( lol, the Home.co.nz value is off by 10%) ... I have one rental that came much undervalued but I am happy with that ...

I suspect that anyone would sell under the New CV values as these are considered as independent and " official " valuation unlike RE or Valuers' expectations in such a messy market .... people who have advertised properties recently had Zilch response to their ads... this Market stagnation could last for long and is not pleasant at all ( to everyone).

You should stick with the 2.225M coz it is ACTUALLY worth that much!!

Thanks guys, now I don't know what to do! I do tend to be a bit pessimistic with prices, that way I am rarely disappointed. The house needs some renovating so I could market it claiming that if a couple of hundred were to be spent on it it would be worth the RV. Psychologically this could be a good strategy.

Also I could claim a buyer was killing me with their lowball offer of 500K yet happily accept the offer.

Zachary Smith, contest your CV. Why? Because you will reduce the outgoing costs of your rates and improve your yields. Also, your property will still be worth the same in relation to all others that sell in your immediate neighbourhood, so by reducing your CV it won't affect what your house will sell for because buyers get the price guide from recent sales!

hi Eco Bird,

You're correct, I believe.

NZ house prices, historically, are sticky down.

People avoid selling if prices weaken - unless they're forced to...... and the great majority won't have to.

Once in property, people like to stay there.

Same old, same old......

TTP

Hi TTP,

Indeed, .... I was just stating a fact which most here dislike although most are homeowners ... not sure why they are unhappy and grumpy !

Just checked the CV on my house built 18 years ago, Never once had the CV gone down during these years ... even throughout the GFC ...so if the council think that values never go down , who are we to disagree lol?

I was in Oz last week and the same issues are alive there as they are here, some prices there are beyond imagination but that is how it is ... the only difference is that they have better public transport which enables those who wish to live afar and work in the cities.

Tough times ahead my friend, the coming 3 years are going to be both funny and challenging.

But you don't own property do you TTP! Ahh well time for you to move on I guess. We're you going to Palmy?

Hi CJ099,

Palmy’s still affordable for old trolls like me.

But even there, prices have moved up the last couple of years.

There’s s leafy suburb I like there - called Hokowhitu. Suggest we team up and buy something - your cash and my enthusiasm.

TTP

Thanks for offer TTP. Though I'd rather invest in new tech rather than NZ property at the moment. At least I'm more likely to get a return on that investment.

Palmy is in a speculative bubble. Palmy does NOT have a shortage of land and all of the building companies are flat out building new homes in new sub-divisions and many new commercial buildings are going up, or in the process of being developed. Architects have wait lists 18 months long, just to get to sit down with them. So why are prices sky rocketing? The same reason why everywhere else is going off the charts.

Summerhill is the new "Hokowhitu" suburb and has the highest prices if that is what you are looking for. This suburb overlooks the entire city from a perch up on the hills. Or Whakaronga is a good alternative with brand new house and land packages and semi-rural.

Ahh, the missing member of the Troika is back.

"So, who is going to sell a $1M freshly valued property for, say, $800K? ... who will have the guts to sell at 20% discount from CV and why should they ??"

I have just one question - You have seen the QV house price index and it's method of calculation, right?

Right around 2008 there is a perfect example of this occurring.

This whole situation is ridiculous . How is it even possible we have got ourselves into the unenviable situation where even the most modest home in our biggest city is unaffordable to all except the very wealthy ?

The last 9 years.

Time for salaries and wages to catch up!!

It will take at least a couple of decades of wage increases to catch up to the 30 year debt burdens that people have taken on. Unless inflation starts rising dramatically, that 30 years of debt will see alot of people suffering on the breadline, while trying to keep the bank from knocking on their door. At this stage, hyper-inflation might actually be a good thing!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.