By Gareth Vaughan

International credit rating agency Moody's says New Zealand is among the high income countries most exposed to a housing downturn, due to a rapid rise in house prices and household leverage.

However, Moody's says unless any such downturn was accompanied by other "long-lasting negative shocks," it's unlikely to fundamentally undermine NZ's sovereign credit profile.

Moody's makes these comments in a report covering NZ, Australia which is home to the parents of NZ's big four banks, Canada and Sweden. All four countries have 'Aaa' sovereign ratings from Moody's with stable outlooks. See credit ratings explained here.

The credit rating agency has benchmarked the four countries against Ireland, Spain and the US in the late 2000s, when all three countries experienced major housing downturns.

"The order in which the four countries are listed in the heatmap [below] represents our assessments of their relative exposure to the key transmission channels, but does not characterise the likelihood of housing market corrections," Moody's says.

"New Zealand is most exposed due to its economy's heavier reliance on residential construction, the potentially more volatile nature of increased housing demand, households' exposure to interest rate shocks, and significant pressures on housing affordability," says Moody's.

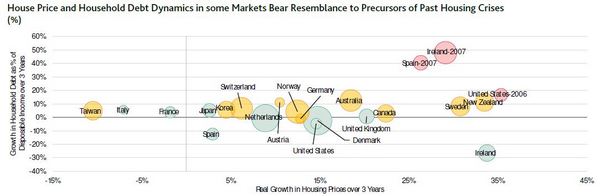

Note: Bubble width represents household debt as a percentage of disposable income (80% for Italy, 260% for Denmark).

Red bubbles represent peaks of housing market cycles that preceded disorderly corrections; green bubbles represent markets where housing prices have not fully recovered since 2006-2011

corrections in real terms; orange bubbles represent all other cases included in the sample.

Sources: National authorities, Bank for International Settlements, Moody's Investors Service

'House price increases in Sweden and NZ closely resemble those registered in Spain, Ireland and the US'

Concerns Moody's cites about NZ include house prices having risen by more than 30% in real terms over three years.

"In real terms, house price increases in Sweden and New Zealand closely resemble those registered in Spain, Ireland and the United States on the eve of their respective housing market corrections," Moody's says.

In contrast wage growth has been moderate leading to a deterioration in housing affordability, demonstrated by higher house prices to income and debt to income ratios. Although low interest rates have thus far mitigated the impact of house price increases on overall housing affordability, the short-term mortgages favoured in NZ - of up to two years duration - mean mortgage affordability would weaken sharply if interest rates rose.

Moody's also notes that NZ authorities expect population growth will stay in the 1.5% to 2% range at least through 2019.

"While these projections point to sustained demand in housing, a reversal in population trends would lead to a sharp increase in property vacancies, depressing house prices and further weighing on demand," Moody's says.

Meanwhile, a slow down in demand from foreign property investors, which already appears to be happening, remains "a source of risk."

The credit rating agency also points out residential construction activity now accounts for 7.5% of NZ's GDP, up from 5.8% three years ago, and 4.5% five years ago.

"The increase in the share of residential construction as a share of total value added matches that observed in Spain. However, New Zealand still relies on this sector much less than Spain did, suggesting weaker spillover effects to other sectors from a potential housing market correction. At its peak, the sector directly accounted for 12% of Spain's value added."

'Sizeable spillovers'

Moody's points out a broad-based housing market correction, whether the initial negative shock or triggered by other economic or financial shocks, generally results in lower economic growth. This weighs on revenues and leads to higher government spending to offset the impact of the shock, both of which weakens public finances. Additionally governments may have to bailout the banking sector if it comes under "acute" pressure.

Moody's says a NZ housing downturn would involve "sizeable spillovers" to the broader economy through the supply chain and impacts on employment and consumption. Exposure to residential mortgages constitutes about half the NZ banking system's assets. Moody's argues this is mitigated by the Reserve Bank enforced restrictions on banks' high loan-to-value ratio (LVR) residential mortgage lending, and the fact NZ operates under a full-recourse loan regime making strategic defaults on mortgages less likely than in the US.

Such "proactive macroprudential measures" restrict the availability of credit for marginal, highly leveraged residential mortgage borrowers.

"[The] proactive macroprudential policy approach also contrasts with regulatory forbearance observed in some markets where housing corrections translated into banking crises in the 2000s. Partially as a result of macroprudential restrictions, lending standards have remained tight and capital buffers large," Moody's says.

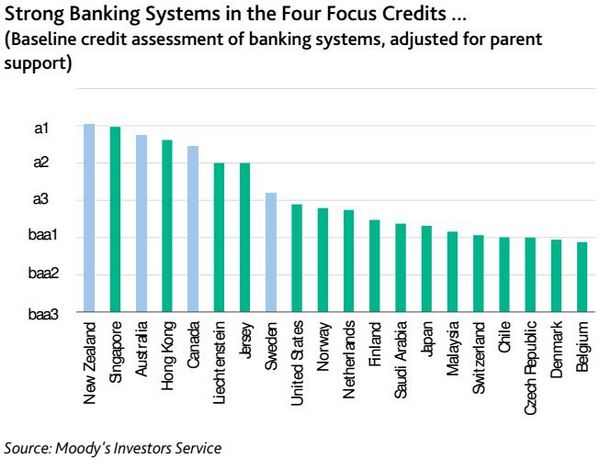

The credit rating agency also highlights high capitalisation levels, conservative business models and the strong liquidity of the NZ banking system.

"Although not immune to them, the [NZ, Australian, Canadian and Swedish] banking systems would be relatively resilient to negative shocks that involve a housing correction, thereby limiting the potential fiscal costs of sovereign support to banks," says Moody's.

My view

Should a major housing market downturn hit New Zealand all bets are off. We simply do not know exactly what the catalyst would be, nor what the domestic and international backdrops would be.

Given the intertwined New Zealand and Australian banking systems and economies, how likely is it that such a downturn would occur across both countries?

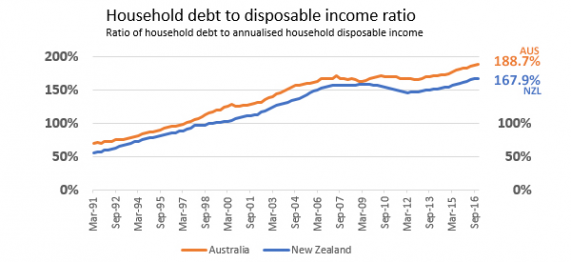

Both countries have experienced strong house price growth in their major cities of Sydney, Melbourne and Auckland. And both countries are running record household debt to disposable income ratios.

As Greg Ninness detailed recently, the Auckland housing market is on the verge of having all of the capital gains it made over the past 12 months wiped out. A, if not the, major factor in this is the slowdown of money coming in from China. Nonetheless, Auckland house prices are still way ahead of where they were even three years ago.

Should the proverbial hit the fan, I'm not as confident as Moody's is of the banking system's resilience. A regulatory capital system that requires* the country's biggest bank ANZ, for example, to hold $1.4 billion of capital against $74.7 billion of residential mortgages concerns me. Thus the Reserve Bank's impending review of bank capital requirements will be of interest. (See more on banks' housing loan exposure here).

Note the International Monetary Fund recently suggested aiming for capital adequacy ratios for New Zealand’s large banks that are "somewhat higher" than the Australian Prudential Regulation Authority’s “unquestionably strong” capital targets for large Australian banks "could be a reasonable benchmark."

There's also complacency in New Zealand when it comes to housing downturns. An 'it couldn't happen here' attitude in some quarters, especially those with vested interests. Two years ago when the Reserve Bank was establishing a new asset class for bank loans to residential property investors I reported the following;

In its summary of submissions and final policy paper issued on Friday, the Reserve Bank says a majority of submissions didn't support its rationale for creating a separate asset class for property investors. One submission noted New Zealand banks have not suffered significant loan losses on property lending since the 1930s. "Many larger banks and property investors were the most critical of the Reserve Bank's rationale," the Reserve Bank says.

Also in 2015, the Reserve Bank noted;

"The absence of a severe housing market downturn in the last 20 years is not evidence that one could not occur. House prices have reached unprecedented levels relative to income in Auckland, so historical New Zealand downturns may not be a good guide to the consequences of a future severe downturn. This leads us to look at other countries that have had severe downturns. While origination practices in the US and Ireland differ from New Zealand in important ways, we still consider that the empirical evidence from those downturns is relevant to considering what would happen in a severe New Zealand downturn.

If the worst does happen, and I hope it does not, we may also have the Reserve Bank's Open Bank Resolution, or OBR, Policy to deal with. This is of particular interest to bank depositors. See how the OBR policy might work, if implemented, here. And there's also a useful backgrounder from the Reserve Bank here on New Zealand banking crises of the past.

*New Zealand banks are holding more capital than the minimum required by the Reserve Bank, as detailed here.

**This article was first published in our email for paying subscribers early on Wednesday morning. See here for more details and how to subscribe.

42 Comments

"Sources of risk" and "sizable spillovers". Plenty of what if scenarios and unknown events and consequences.

Moodys is indirectly demonstrating why bubbles are not actually that good.

Personally, I don't buy into "the banks are OK." In the worse case and less-than-desirable scenarios, this will bite the average joes on the ass, whether they're direct players in the charade or not.

Well if the rating agencies that didn't see the 2008 dabacle coming, think all is well, then there's is ABSOLUTELY no reason to worry.....come on, is any one awake? Otherwise how come someone would write this propaganda???

Otherwise how come someone would write this propaganda???

Because that's what they do. They don't know the eventual outcomes, so scaring the sheeple is deemed to be irresponsible.

Setting aside that this is the same ratings agency that gave top investment grade ratings to subprime securities this review looks good unless you start doing some superficial digging.

BNZ has moved away from meth houses and obtaining profits as a matter of proceeds of crime and back to the everyday person. Their survey indicates that people with mortgages would struggle with repayments if they increased by $120 per fortnight or $3120 per year. On $250k that's a 1.25% increase in interest rates (approximately).

How would they respond to the increase? 20% would increase the term of the loan and 35% would pay for it with savings or retirement savings. That's right they'd throw away their retirement to pay off their house.

Plenty of other interesting survey statistics in there.

http://www.stuff.co.nz/business/money/91486667/one-in-five-homeowners-l…

It works like this dictator. To invest in one sick cow would be unwise. But if you aggregate a bunch of them together the risk goes away. Moody's were the clever people who first brought this wondrous truth to our attention and should be rewarded.

I guess the big difference is that Moody's, S&P et al were not even considering or discussing housing risks before the GFC. In fact they outright dismissed them at the time. Whereas, here, they are not only discussing a housing correction, they are discussing who it will and won't effect. That's actually quite something for a ratings agency.

Ratings Agencies will always downplay risks or they risk creating panic and instability. There job is to mostly maintain the status quo and only downgrade anyone in the utmost dire scenarios.

Govt need to ban interest only mortgages to reduce risk although with current supply imbalance difficult to see prices imploding...just a bit of reality after the madness.

"New Zealand is among the high income countries most exposed to a housing downturn"

OK, so the banks are ok.

How about many of those first home buyers who have extended themselves to the limit over the past couple of years who are likely to be facing decreasing equity and most likely increasing mortgage rates?

The Economist (11 March) pointed out that NZ is the most over-valued for house prices of OECD countries. Over-valued 114% for rental income, 59% for income.

They point the finger squarely at "the impact of foreign money .... a growing horde of rich foreigners see NZ as a safe haven". Funny that the NZ Initiative couldn't spot that in their well-funded analysis.

If this source of $$ dries up, all bets will be off. Unless the various generous taxpayer subsidies to landlords keep the market propped up - but then, these are all predicated on tax-free capital gains.

Okay this headline actually reads ...... Stuff the young Kiwi homeowner and ensure the Aussie banks are safe and cozy .

The reality is the Banks are complicit in the problem , they have been throwing money around like drunken sailors on shore leave , and the bank lending has bordered on reckless at times .

This all is possible only because head of the country - Our PM supports and allows it.

To paraphrase Ronald Reagan, to compare banks with drunken sailors is to insult drunken sailors who, unlike banks, are only reckless with their own money.

Something missing here is that New Zealand is 3 hours from its closet Neighbour, Ireland and Spain partly failed due to population being able to get up and go to someplace else in Europe, with freedom of movement, if Nz economy nosedives then our currency depreciation will further float house prices as we become more attractive. A standard 3-4 bedroom home in a grey Lynn type area in Singapore is valued between 6 to 7 million SGD, houses are cheap in Nz especially for those 1 million Nz expats

Plenty will flee New Zealand if it ''nosedives'" Keywest. This is not the day of sailing ships. A $1000 airfare will get you far far away in a single day.

Some will just decide on the spot, drive to the airport, leave the key in the ignition, buy a ticket at the counter and never be seen again, leaving a fouled nest behind..

It was quite surreal having that happen when Dubai tanked. If there's zero reason to stay then why bother.

Where can a New Zealand citizen go for more than 3 to 6 months (excluding Australia) with out a visa? And that's a holiday visa mind you, under 30's do get the 1 year U.K. / Europe work visa as well for completeness

Don't forget all those Work Visas and Students. They'll skip town in the instant they realise their NZ adventure has become financially worthless. Then the Permanent Residents from single permitted citizenship countries, who elected to retain their original citizenship. Last, but not least, Dual Nationals. Some of us might be NZ born, but we'll jump ship in a second if this ship goes full retard.

Tally it up. That's a lot of people who aren't quite so trapped in paradise as you might believe.

I and most people I work with (happens to be a sector in demand, I guess) get regular offers from AU, UK and elsewhere. I don't think it would take that long for a bunch of people in our industry to head off abroad.

My statement remains valid, NZ is a more difficult place to leave ( and immigrate to) than Spain, Ireland and Sweden, hence why their bubble is different to ours

The psychology of bubbles are frightening predictable.

The phrase "this bubble is different because" as has been written right here by Keywest is a classic example.

The only place a New Zealand citizen can go is to Australia with out a Work visa. Any new permanent resident or citizen can only go back to the country they came from (there was a reason why they left) a European on the other hand can go anywhere in Europe and they do every day, we are somewhat trapped in the South Pacific

It must be raining

Thats the only reason you could be getting depressed.

We have often thought these dark thoughts, travelled the world, worked in Aus, frozen in the NZ south.

We have an EU passport but....no pension.

The place to run if it all turns against you is Northland, its warm and if you have to, consider mowing lawns.

Finally someone has said something that confirms what other people have been saying all along. This is not the time to put a negative spin on a positive thing or a positive spin on a negative. It is time to set aside our similarities and focus on our differences. It is a time to look at property as a home and not just a house...to look at property investment as a way of making money through the purchase of houses. We need to understand that not every Chinese person is made in China but that every Chinese person not from China is still Chinese. We need to show more interest in banking and pay less interest to banks.

Agree. NZ's political parties need to cease their abandonment of the young and upcoming generations of Kiwis and recognise their responsibility for what is handed on to the next generations.

Douglas Murray describing the philosophy of famed conservative Edmund Burke:

Edmund Burke was right in the central point of his philosophy: that a culture, a society is not simply about us here now, but it is a deal between the dead, the living and those yet to be born. And that you cannot break that pact, and that what you have inherited you do not have the right to give away, any more than you have the right to destroy future generations of your own family or future generations yet unborn, it is a very central pact of civilisation, that deal, between the dead, the living and the yet to be born.

If you give it up and say it doesn't matter if the next generations' society resembles Mogadishu more than Stockholm, then you are breaking that pact.

What could possibly go wrong?

houses could go up

houses could go down

banks could make too much money

banks could go bankrupt

immigration to NZ continues

immigration to NZ stops

Chinese money frees up

Chinese money freezes up

Donald Trump

Global Warming

North Korea

Russia

Brexit

Isis

Earthquakes

Tsunamis

Volcanic eruptions

Meteorites

Antibiotic failure

England winning the next world cup

1 in 5 and $120 is not a lot given avg debt levels

http://www.stuff.co.nz/business/money/91486667/one-in-five-homeowners-l…

get long popcorn futures

So far, every time I've bought a new car, the economy went into recession not too long after. Last time I bought was 2007.

I just bought a new car last week. Sorry.

Damnit, James!

James, that is unnerving. I too will pick up my new car on Wednesday, having had the old one for 10 years. Moodys need to know about this...

There are Aucklanders moving to our region. Some building 2 million dollar houses. I might be wrong but over time I wonder if they will get their money back when they sell in 15 years time. My reasoning for this is land in the regions is plentiful, if in 15 years time you had a couple of million to spend on a house in regional NZ. Wouldn't you rather build a new one?

If they have cashed up their Auckland property for $4m-$5m and spend $2m to build a new house in the region, do you think they care about what it will be sold for in 15 years time?

Exactly,

And they are providing ongoing income for the region while they blow it all on booze and fast cars.

The house becomes available later at its depreciated value.

On that note it seems appropriate to recall the words of George Best:

"I spent a lot of money on booze, birds and fast cars. The rest I just squandered."

First laugh of the day...

They tell you this now AFTER prices have peaked. lol

The lack of a deposit insurance scheme in NZ bothers me a little. I know how OBR would operate in the event of a bank collapse here and I have taken steps to alleviate the risk by spreading my TDs among several banks. I have an email from the RB which says; "The first point to make is that the subsidiary of an Australian parent bank would be ring-fenced".

Can anyone answer this question? If I as an NZ citizen living in NZ, were to open an account in Australia,would I be covered by their deposit insurance in the event of the bank failing? My own bank-ANZ-can't tell me and I have had no response from the Australian RB.

I am sure that one of the many smart people on this site will know the answer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.