By Gareth Vaughan

With the Reserve Bank having recently declared the banking system "robust to a severe dairy stress test," it begs the question as to what could be big enough to really rattle the banking system, or financial stability, to its very foundations.

There are plenty of potential overseas scenarios that could threaten financial stability in New Zealand. An economic meltdown in China, a prolonged freezing of international credit markets, a major act of terrorism, war, etc, etc.

But back in NZ the Reserve Bank, prudential regulator of our banks, has effectively declared NZ's banks safe from a major dairy derived disaster. Remember about $38 billion, or 10%, of their lending is to the dairy sector.

If we accept the Reserve Bank's conclusion from its dairy stress test, then domestically only one sector banks lend to can be considered a threat to financial stability. And that sector, of course, is the housing market.

My argument is that if as it clearly is, housing is the biggest domestic threat to NZ's financial stability, banks should be holding more capital against their housing loans.

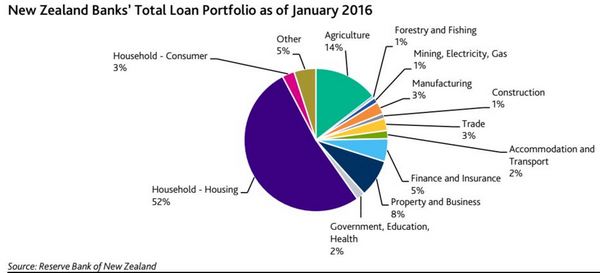

As the Moody's chart below demonstrates, NZ banks have about 55% of their lending exposed to housing. To give some context of size, total household debt stood at $228.5 billion as of January, which is equivalent to 93% of last year's $246 billion Gross Domestic Product. Mortgage sizes are at record highs, and as my colleague David Hargreaves recently noted, NZ's household debt to disposable income ratio is at a record high of 162%.

More capital required to cover business & rural loan losses than losses on housing lending

Against this backdrop it's worth pointing out that banks' Reserve Bank enforced capital rules mean they hold less capital against housing loans than they do against lending to businesses and farmers to cover any losses. A perusal of disclosure statements from ANZ, the country's biggest bank and number one mortgage lender, and from state owned bank Kiwibank, demonstrates this.

ANZ, like ASB, BNZ and Westpac, is allowed to use the Internal Ratings Based (IRB) regulatory capital approach. This means they develop their own models to calculate their regulatory capital requirements and must then get them approved by the Reserve Bank. All other banks, including Kiwibank, run what's known as the standardised approach where the Reserve Bank prescribes their requirements.

The latest disclosure from ANZ shows what's known as a risk weighted exposure of $14.5 billion on $57.5 billion worth of on-balance sheet residential mortgages. The sum of risk-weighted exposures represents the total credit exposure the bank has accepted. ANZ thus has a total capital requirement held against its mortgages to cover potential losses of $1.163 billion.

Just to reiterate for ANZ that's about $1.2 billion of capital held against total mortgages of $57.5 billion.

ANZ has an exposure-weighted risk weight on residential mortgages of 24%. In contrast, ANZ's risk weight on $36.2 billion of corporate, including rural, lending is 56% with total capital held against this lending of $1.73 billion. Thus capital held against corporate lending exceeds what ANZ holds against mortgage exposures by $567 million, or a third, even though mortgages top the bank's corporate lending by $21.3 billion.

Kiwibank has risk weighted exposure of $4.464 billion on $12.8 billion of on-balance sheet residential mortgages. Thus its minimum capital requirement is $357 million, and as a standardised bank, Kiwibank has a 35% risk weighting on its mortgages. Kiwibank has most of its much smaller business lending exposure ($728 million) at a 100% risk weighting, with a small slice of this at 50%.

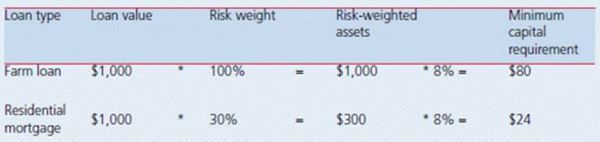

The Reserve Bank chart below gives an example of how risk weights impact the amount of capital banks hold against different asset classes.

Although NZ banks' capital rules are the responsibility of the Reserve Bank, they are based on international standards set by the Basel Committee on Banking Supervision.

The table below details regulatory capital covering the big five banks' mortgage lending.

| Retail mortgages | Exposure-weighted risk weight |

Risk weighted exposure | Minimum capital requirement | |

| ANZ | $57.476b | 24% | $14.531b | $1.163b |

| ASB | $52.922b | 28% | $15.521b | $1.242b |

| BNZ | $35.421b | 31% | $10.974b | $878m |

| Kiwibank | $12.755b | 35% | $4.464b | $357m |

| Westpac | $48.240b | 31.06% | $14.984b | $1.199b |

*ANZ, BNZ and Westpac figures as of September 30 last year, ASB and Kiwibank figures as of December 31 last year.

As we reported last July, NZ's big banks do have higher risk weights on mortgage lending than their Australian parents. That's despite Australia's 2014-15 Financial System Inquiry requiring the parents of NZ's big four banks to raise about A$12 billion of capital to lift their mortgage risk weights to at least 25% from about 16%.

'Overall lending is weighted towards residential lending and away from the productive sector'

Even within the banking industry not everyone thinks it's a good idea for banks to favour residential mortgage lending over business lending to the extent they do.

Here's some comments I reported in 2012 from BNZ's CEO of the time Andrew Thorburn. He touched on the financial stability issue noting a house price fall of 10% could lead to greater wealth destruction than caused by the 1987 sharemarket crash. And he also noted a "massive long‐term bias towards" investment in residential property at the expense of the productive sector.

Thorburn acknowledged the imbalance in favour of investment in residential property over productive businesses was "writ large" in New Zealand banks' balance sheets.

"Almost 50% of BNZ’s lending book, for example, is supported by residential housing, and it’s pretty much a rock‐solid asset for us, as it is for our competitors."

The expression "safe as houses" had deep resonance for bankers, he added.

"I can’t speak for the other banks, but it has long concerned me that overall lending is weighted towards residential lending and away from the productive sector, at a very time when New Zealand is slipping down the OECD ladder of GDP per capita, at a time when so many young New Zealanders are unemployed or think they can make a better living in Australia and other places, and during a period in which we’ve essentially maintained our standard of living as a nation by borrowing from the savings of people in other countries. Long‐term, this is unsustainable," Thorburn said.

And;

New Zealand is one of the few developed countries in the world without a capital gains tax applying to investment in residential housing. We also support negative gearing and have no stamp duty on property purchases," said Thorburn.

"As a consequence, we have seen in this country a massive long‐term bias towards investment in residential property - a non‐productive asset in investment terms, albeit a critical life requirement for people and families."

Thorburn, incidentally, is now CEO of BNZ's parent, National Australia Bank.

A precedent

In terms of the Reserve Bank making banks increase capital held against a specific asset class, there's a recent precedent, which looks a very wise move in hindsight.

In 2011 the Reserve Bank made the big four banks increase the risk weights on rural loans to up to 90% from 50%. (It was 100% prior to 2008, and other rural lenders including Rabobank, are at 100%). Alan Bollard, Reserve Bank Governor at the time, told a parliamentary select committee banks had been very lucky dairy prices had rebounded. Bollard said as the Global Financial Crisis (GFC) kicked into gear, with dairy prices going up, farmers rushed out to borrow and consolidate and banks "rushed out to lend."

"It's pretty clear to us and it should be to them as well, that they over-stretched themselves," Bollard told the select committee in 2011. "Actually some of them have been very lucky that dairy prices have picked up again."

With dairy farmers now looking at three consecutive seasons of payouts below the breakeven level estimated by the Reserve Bank to be $5.30 per kilogramme of milk solids, who would now argue the 2011 move to make banks hold more capital to cover potential losses on rural loans was not the correct one?

Houston, we have a problem

Widespread concerns about Auckland house prices have been well documented over the past two or three years. Here's but a few examples:

Reserve Bank Governor Graeme Wheeler recently noted Auckland has a house price to income ratio of 8.5 times, with the rest of NZ at 5.1 times. A median multiple of 3.0 times or less is generally regarded as a good marker for housing affordability. This follows the Auckland Council saying last October it wants to see the city’s median house price to median household income ratio halved to 5:1 by 2030 in an attempt to improve housing affordability.

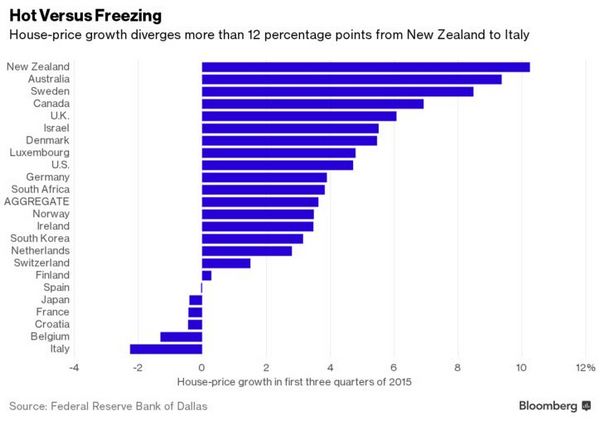

A Bloomberg report over Easter shows NZ house prices have risen the most across a range of countries over recent years.

"Since the global property market bottomed out at the start of 2012, house prices have risen most in New Zealand, Australia and South Africa. Increases of more than 30 percent in the three countries compare with an average gain of 11 percent in the sample," Bloomberg reports.

Yale Econometrics Professor Peter Phillips, an economist who has studied asset bubbles extensively overseas and has been tipped to win a Nobel Prize, co-authored with Auckland University Economics Lecturer Ryan Greenaway-McGrevy, an academic paper identifying Auckland's housing market as being in bubble territory. As of the end of February, the median Auckland house price was up $215,000, or 40%, in three years to $750,000, according to the Real Estate Institute of NZ.

And credit ratings agencies remain wary of the threat to NZ's financial stability from strong house prices. Here's Standard & Poor's from last October;

"In New Zealand, we believe that robust house price growth - particularly in Auckland - is elevating risks in the financial system; hence, on August 14, 2015, we negatively revised our Bank Industry Country Risk Assessment (BICRA) on New Zealand and at the same time took various negative rating actions on financial institutions. This negative BICRA change followed an extended period whereby New Zealand's previous economic trend was negative primarily because of property concerns," says S&P.

So we do have a problem with high house prices and housing affordability. And our bank's have the lion's share of their lending in a sector that poses the biggest risk to NZ's financial stability. Things could get particularly tricky if there was a spike in interest rates, even back to something resembling historically normal levels off current lows, or if unemployment surged and loan default rates started rising. Note the average bank two-year mortgage rate is currently about 4.5%, but was as high as 9.9% in March 2008. And the current 5.3% unemployment rate is way below the 11.4% recorded in 1992.

Reserve Bank reviewing banks' capital requirements but unsympathetic to higher mortgage risk weights

So why not simply increase the amount of capital banks must hold against their housing lending, along the lines of what the Reserve Bank did to rural lending in 2011?

The Reserve Bank is currently reviewing bank capital requirements and the IRB capital modelling used by the big four banks. So why not simply bump up the risk weights required on mortgage lending to say, 50%? After all that's where they were until lowered to current levels in 2008. Bizarrely this reduction was made the same year the GFC was sparked by a US housing market collapse.

Actually rather than bump up capital requirements on home loans to 50% of risk weighted exposures, why not make it 20% of total mortgage exposures? The banks could have say, a three year period to phase this in.

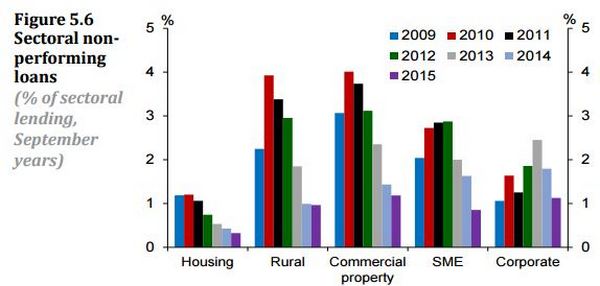

Doubtless bank bosses, their shareholders and lobbyists, anticipating less profitable mortgage lending and higher costs, would vigorously protest this impost. They'd also point to the fact that housing loans tend to sour at a lower rate than rural, commercial and business loans as demonstrated by the Reserve Bank chart below.

Banks will also argue stress testing, including of their housing lending, shows they could survive a serious economic shock including chunky rises in unemployment and home loan default rates. But the problem, as those working in and around the dairy sector will discover, is this comes at a wider cost. Forced asset sales and reduced lending to those who really need it are just two likely side effects. The risk weighted ratio system can make it hard for entrepreneurs to borrow, especially in tough times when entrepreneurship is especially needed, because they're deemed to be risky. Yet it supports a housing bubble because residential mortgages secured by houses are deemed safe.

The key point from a financial stability perspective is if things get ugly in the housing market, the impact on the entire financial system (and New Zealanders' wealth) is much greater than if rural, commercial property or business loans sour significantly.

Based on previous comments from the Reserve Bank, the regulator appears unlikely to significantly raise risk weights on housing loans. Here's Reserve Bank Deputy Governor Grant Spencer from 2013;

Risk weights play an important part in the Reserve Bank’s supervision of the banking sector. They help to determine the amount of capital that the banks need to set aside to cover losses on their lending to different sectors. In essence, the riskier the sector, the more capital must be held against lending to that sector.

The risk weights factor in things like the borrower’s capacity to repay the money, the type of assets put up as security for the loan, and the amount of security relative to the size of the loan. History provides some insight into the importance of these various factors.

As a result of these risk factors, risk weights vary for different types of lending, with housing having a lower risk weighting than business or rural lending, which typically involve more risk.

The risk weights are not set in order to incentivise any particular lending type over another. Instead, they reflect the different risks inherent in different types of lending, leading to capital holdings against loans that are appropriate for the risks involved. This tends to result in higher lending margins on riskier loans, but does not imply that banks will always lend to housing ahead of other sectors. In principle, banks will set loan margins such that risk-adjusted returns will be similar across sectors.

Thus the Reserve Bank views mortgage lending as less risky than business and rural lending, and doesn't see itself having a role in promoting economic and social objectives such as increasing lending to the productive sector and away from property speculation, as outlined by Thorburn above.

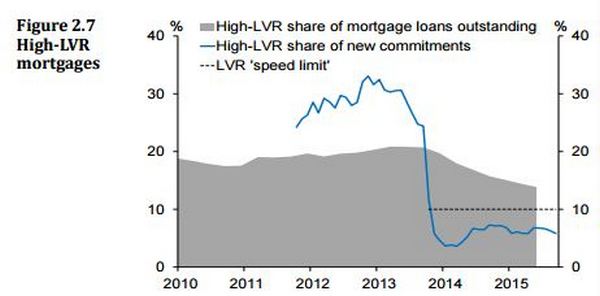

LVR move derisking mortgage books

To be fair to the Reserve Bank, it did take a step towards derisking home lending in 2013. This came through limiting banks to doing no more than 10% of their new mortgage lending to borrowers without equity in their property, or a deposit, equivalent to at least 20% of the purchase price. The so-called loan-to-value ratio (LVR) restrictions. In last November's Financial Stability Report the Reserve Bank noted the share of bank mortgage debt with an LVR of more than 80% has fallen to 14% from 21%, "increasing the resilience of bank mortgage portfolios."

We've now also seen the Reserve Bank introduce a rule that Auckland residential property investors seeking a mortgage require a 30% deposit, whilst outside Auckland banks can now do up to 15% of their new mortgage lending to borrowers with LVRs exceeding 80%, regardless of whether the borrowers are owner occupiers or residential property investors. As a result, house prices have started rising in regions outside Auckland.

Give us a leverage ratio

The Reserve Bank has steadfastly refused to introduce the leverage ratio, which is part of the Basel Committee on Banking Supervision's post GFC international banking reforms. This ratio weighs all assets equally and serves as a backstop, potentially helping prevent banks from lending too much money into "safe" and therefore unproductive assets such as housing.

The Australian Government's recent Financial System Inquiry (FSI) recommended the introduction of the leverage ratio, which is defined as Tier 1 capital as a percentage of total assets and off balance sheet exposures with an initial minimum of 3%. The FSI report said the risk-weighted approach to capital requirements should be supplemented with a leverage ratio that protects against potential weaknesses in the risk-weighting system.

"The major (Australian) banks currently have a leverage ratio of around 4–4½ per cent based on the ratio of Tier 1 capital to exposures, including off-balance sheet. An overall asset value shock of this size, which was within the range of shocks experienced overseas during the GFC, would be sufficient to render Australia’s major banks insolvent in the absence of further capital raising," the FSI said.

"A highly leveraged institution has smaller buffers available to absorb loss before insolvency. Leverage can also amplify the effect of shocks on an institution’s balance sheet. This may spread shocks to other institutions and cause systemic risks. A number of countries have introduced leverage ratios, including the United States, the United Kingdom and Canada. Australia does not currently have a minimum leverage ratio requirement, although APRA has indicated that it may introduce one in line with the Basel framework."

Specifically the FSI recommended the introduction of a leverage ratio "that acts as a backstop to authorised deposit taking institutions’ risk-weighted capital positions." This has been endorsed by the Government, with the Australian Prudential Regulation Authority instructed to implement the recommendation.

Here, however, the Reserve Bank has said it won't introduce the leverage ratio because the one-size-fits-all aspect of it is poorly targeted and can give a misleading picture of risk in some situations. The leverage ratio would "undermine the value of the existing risk-based approach to the calculation of required capital," which if properly applied "renders a leverage ratio unnecessary," the Reserve Bank has said.

But David Mayes, Professor of Banking and Financial Institutions at the University of Auckland and a former chief manager and chief economist at the Reserve Bank, last year urged his former employer to introduce the leverage ratio saying; "Risk weighted capital ratios tend not to be very good limiters of problems. Most banks which get into serious difficulties are meeting the requirements for risk weighted capital. But it's much more difficult to finesse the leverage ratio requirements."

Another tool in the toolbox

There's also another tool in the Reserve Bank's macro-prudential toolbox, alongside the LVR restrictions, that could be implemented to force banks to hold more capital against home loans. Formally this tool's called adjustments to sectoral capital requirements, which is an additional capital impost that may be applied to a specific sector (such as housing loans) in which excessive private sector credit growth is judged to be leading to a build-up of system-wide risk.

Surely there's a strong argument, based on the evidence outlined above, that this build up in system-wide risk stemming from housing loans is as clear as day right now?

So what are the Reserve Bank and government waiting for?

Because if things went pear shaped in banks' residential mortgage books we may be left searching for the remnants of the NZ economy under the ashes of the housing market.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

31 Comments

IRB models are fantastic. On the condition that those using the results of the modelling are competent at understanding the model and it's limitations. Except that I'd find it highly unlikely that an expert at building the model is in change of decision making.

It's not like believing a garbage in garbage out model has caused problems before, or indicated no risk and in doing so contributed to increasing risk to an unsustainable level.

There seem to be a number of problems with Wheeler's own stress tests. They look like they've been chosen to produce a result rather than produce one where the outcome is unknown.

Excellent useful article. Thanks.

The best for the financial stability would be to burst the bubble BEFORE the new global financial crisis arrives. That way the losses for banks can be softened by benefits like new loans with higher margin interests.

But when the global financial crisis arrives all the banks will immediately cut the credit flow (and of course the bubble will burst eventually if it hadn't done so), hence not even the solvent families will be able to borrow to absorb the assets offer and the damage for banks will be even greater.

The housing bubble will eventually destroy the productive economy, and that's a shame because it could have been avoided.

Luckily it was all overseas speculation with overseas money, so nothing to worry about. Right?

I have to say that bureaucracy is killing the productive economy also. All you ever hear about is more red tape and regulation to siphon another tax dollar or levy to keep the titanic economies afloat but never any deregulation( no I'm not a dairy farmer).....and I'm not referring to the banking & monetary system which clearly needs a massive overhaul that may come after the inevitable GFC 2.0 .....maybe.

It would appear the entire global economy is now based on only feeding, incentivizing, and bailing out the biggest ponzi scheme in human history. Banks have taken over the world and governments know it, but telling the people is just not in their interests it would seem.

Must we go through the very worst of times before anyone does anything effectual?. The guy from NZ Treasury this mornings RNZ was a great example of someone doing their very best to spin some kind of economic positives......while disregarding global realities like zero headed to negative interest rates (including our own), global & national debts.....etc. Anyone else hear that twat? Optimism is one thing, Delusional is what I heard.

There is no bubble like "There is no spoon" - The Matrix

The risk weights are not set in order to incentivise any particular lending type over another. Instead, they reflect the different risks inherent in different types of lending, leading to capital holdings against loans that are appropriate for the risks involved. This tends to result in higher lending margins on riskier loans, but does not imply that banks will always lend to housing ahead of other sectors. In principle, banks will set loan margins such that risk-adjusted returns will be similar across sectors.

Banks always lend to the sector demanding the lowest risk weighting and offering the most liquidity - hence the Australian banking industry reliance upon the residential mortgage market as the primary asset.

Australia’s banks turned into giant building societies, lending almost exclusively against residential property and rarely, if ever, making unsecured loans to businesses or people any more. Read more

Didn't Spencer come from ANZ?

From the wireless:

How misguided theories of finance have led to an unhealthy relationship between debt and the modern economy - with Lord Adair Turner of the Institute for New Economic Thinking (London), and author of Between Debt and the Devil: Money, Credit, and Fixing Global Finance.

The housing bubble has only just begun inflating - a long way to go yet as swap rates plummet

And our interest rates have miles to plummet. Its not like we are anywhere close to zero yet, can you imagine what will happen to property when it gets that low ?

Dimishing returns as the principal component becomes the larger.

I was just running numbers on rental yields for a hypothetical Auckland house. How on earth do you investor types make it work? Seems like you might just be cashflow positive at around 50% LTV?

but it has long concerned me that overall lending is weighted towards residential lending and away from the productive sector Bottom line here is that because Governments have chosen to subsidise rather than regulate the housing sector, they have actually contributed to financial instability and the risks we face. Helps to put the article on Systemic Risk (here)from a few days ago into perspective. When will they ever learn?

Agree, a lot, LOL. It seems the Govns and RBs of the world failed strategically medium and long term, the very thing they are there for. However they were probably doomed to as from the 1970s oil crisis the developed world moved away from making goods to providing services as these used less raw materials and energy. We then exported out good making to the developing world that had cheap raw materials and cheap labour to compensate. The thing is no one in Govn it seems challenged the orthodoxy that we could continue to grow for ever on a finite planet.

"When will they ever learn?" we wont it seems, so nature will teach us the hard way. Yet as a species we do have the capacity to do so but the inability to act on it.

Last week some time I had commented that the current economic models were focused on protecting the rich and powerful, and a responder stated having just read an analysis of the fall of the Roman Empire and stated that the parallels with the current time were frighteningly similar, so the old saw about being unable to learn from history seems to be true.

Great article. Question: we hear frequently about our banks needing to borrow from offshore. Given that they own the printing press (http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin… ) is this borrowing perhaps to meet their reserve requirements? If so, would higher reserve requirements mean more offshore borrowing? Surely not - but I'd love someone to explain what the offshore borrowing is all about.

no... Capital adequacy has to do with Bank Capital... not borrowed money.

Banks are able to create credit, which is an IOU note .. a claim on money.

The distinction is important.... ( It getts complicated because credit is fungible... we accept it as money )

Every day Banks have to honour those IOU notes when they reconcile their accts thru the RBNZ payments system.. Any imbalances have to be settled in "real Money"...(called outside money ).

Generally alot of the different Banks IOU notes cancel each other out when things are reconciled..BUT any imbalance must be settled with "cash" ( metaphor for outside money )..

This becomes a constraint on how much credit (IOU notes) an individual Bank can prudently create.

Thats why our Banks borrow heavily in the offshore wholesale lending mkt..

This is why Banks take deposits...

They are juggling the mix of the credit they can create with the need to able to settle their accts, thru the RBNZ payment system , each day..

This is why Banks borrow short term and lend long term . ( yield curve)

This is why Banks buy wholesale and sell retail .. ( interest rate margins )

The idea that Banks simply create money out of thin air.... unconstrained... like a "printing press" is fanciful... ( If they were able to too... then they could simply create money and buy any asset they wanted to... without limit ... just like a counterfeiter )... Only a Central Bank can create money out of thin air .. ( outside money )...

Banks create Credit... (The distinction is important if u want to understand why Banks have to borrow in the Wholesale Money mkts )

This is my view ... I don't claim it to be the "truth".....(I asked the same questions you have , I spent alot of time sifting thru all the half truths and misunderstandings too reach my own understanding...And there is alot of misinformation out there )

Thanks very much, very helpful. So your understanding is that all bank borrowing is short term to cover their balance of payments? I seem to remember reading somewhere about bank long term borrowing - but could easily be wrong. Do you know for sure that they are not allowed to count such borrowed money against their reserve requirements? (This would seem sensible but that doesn't guarantee it's what's true.)

No.... Banks can borrow from the interbank mkt or from the Central Bank itself in order to cover its balance of payments ( payments system ) ....( if they need too... on a very short term basis )

What I was meaning is that Banks , in their normal business of lending , are not dissimilar to a finance company.. .. Banks Borrow and relend... ( they are intermediaries... just like a finance company )

They borrow short term ( at lower interest rates ) and lend it out longer term ( at higher rates )

eg.. they lend out money that is in depositors on call accts..

They also borrow long term , in the offshore wholesale money mkts, and relend that money long term.. ( eg.. borrow for 5yrs at 2% and relend for 5 yrs at 5% )..

Of course ...a Bank is more than just a financial intermediary... Banks also create credit..and are a part of the "payments system"... ..With the Resreve Bank they facilitate transactions....etc..

regarding reserve requirements... Borrowed money is a liability.... Reserves need to be assets... ie.. Capital... owners equity.

RBNZ operates on Capital adequacy ratios ...which is a little different to the "reserve requirements"... of fractional reserve banking.

Thanks! So if I'm understand you, they can create credit, but that requires reserves (or capital adequacy), so they may find it more profitable to borrow long term from overseas. Makes sense.

http://www.rbnz.govt.nz/regulation-and-supervision/banks/prudential-req…

Prudential policy determines how much leverage a bank can have

In regards to credit creation:

See page 6 of ur linked Bank of eng. article.... fig 2.

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin…

This shows how a Bank has to attract deposits and/or reserves in order to settle the transaction that results from the creation and spending of credit...

Credit creation is not magical.... There are natural constraints to it..

Accounts have to be settled..... the final step in a bank creating a loan.

More work to be done?

Which banking units will monetise the new government $NZ IOU to create the Crown deposit at Westpac and ultimately, in the near term, the RBNZ, which will on-lend back to the banks via a collateralised repo/currency swap type operation?

The New Zealand Debt Management Office today announced that $1.5 billion of 15 April 2025 nominal bonds have been issued via syndication.

The bonds, which carry a coupon of 2.75%, were issued at a spread of 28 basis points over the 15 April 2023 nominal bond, at a yield to maturity of 2.745%. Total book size, within the initial pricing guidance range of 24 to 29 basis points, exceeded $2 billion.

Settlement will occur on 15 April 2016 and further issuance of the new 2025 nominal bond will not occur prior to July 2016. Read more

The next recession or financial crisis can't be too far off now. Everything is feeling just as crazy again.

Next time there will be no interest rates to left to cut.

The problem is all the major banks in New Zealand are no longer New Zealand banks. We are now tied into the Australian economy whether we like it or not. We should have tossed our currency and gone to the Aussie dollar when it hit parity but thats another story, Kiwi pride standing in the way of that going forward. For it all to hit the fan here its also all going to have to hit the fan in Australia and I simply cannot see it happening. Even if we hit GFC 2.0, whats to say its going to be worse for us than the first crash ? not sure about you but I never even noticed it. Stayed in a job, kept paying the Mortgage, situation normal.

Really, why should the banks care. If they go bust the honchos have already got their bonuses. They declare bankruptcy, move on, skip to Aussie for a few months, come back and start up another bank and 'she'll be right'. Who loses is the term depositor/ investor who entrusted their money to the bank to operate in a financially responsible way, which they are not doing of their own accord. They have to be forced to keep the appropriate capital or it would be even worse. The banks nor the RBNZ believe in deposit insurance offered for the saver so it could well be the average NZder that will lose their life savings along with general economic turmoil caused by a situation that could have been avoided.

Why is it the depositor as an investor bears no responsibility to invest wisely?

Who would be the insurer? the Government? ie the tax payer? or a third party?

No this turmoil cannot be avoided we have reached the limits to growth and the system has to grow, hence its now consuming weaker parts of itself.

Why is it the depositor as an investor bears no responsibility to invest wisely?

Banks create deposits when they make loans - the decisions concerning the veracity of the loan conditions is not a designated depositor function. They (savers) are just barely in receipt of the loan proceeds upon the sale to the debtor that purchased the for sale asset - in most retail cases a residential property.

Would it be wise to avoid the big 4 and put money into the NZ banks eg HNZ,TSB and SBS.

It's too difficult to say. Depending on how the loans are structured and potential failures any of them could have liquidity problems or a bank run.

The big banks use IRB and if their models are correct and their capital reserve large enough they might ride it out. The smaller banks as far as I'm aware use the by the book figures for their capital requirements under the banking regulations. This may mean they have more capital reserves as a percentage than the large banks.

In short there is no way to know which ones will be safer, could be big, small or there could be individual bank failures. The approach I've taken is to limit the amount of cash I hold in any bank.

'''limit the amount of cash i hold in any bank''

Are you saying you spread your money around the different banks or do you put your money elsewhere.

If it is elsewhere i would sure like to know where or an example of where.

I don't recommend spreading around other banks unless you have another purpose for doing it.

I am shifting money that isn't needed for cashflow into construction activity, and financial instruments (at the moment primarily shares for long term investment). I've even stepped up my mortgage repayments this week.

There's risk and volatility but holding financial instruments that I could liquidate if necessary is better than holding large sums of cash in bank accounts. That and I'd like to get use out of the money I've made rather than lose it in the event of a financial crisis.

Even if deposits aren't lost if you look at Greece the daily withdrawal limits were a major problem during the bank run.

My view is the central banks think "next recession" can be endlessly prevented by endless QE. But investment decisions are distorted under such policies. There approach will be to print endlessly to prevent deflation. But I think they will fail.

As always, there needs to be an economic shock whether it be in GDP/World trade/derivatives/demographic related.

Taking a step back from it all, I recall walking to work in July 2007, and thinking about the world economy on my way to work. Something was telling me something had to crack. One month later Bear Sterns collapsed.

I dont "feel" like that right now but, I do feel the risk is rising for a shock. falling world trade is a concern as it has many flow on effects. That sort of thing tends to show up first in corporate earnings and stock valuations.

I think the world will be a very different place in 2020.

As for negative interest rates. Hmmm, so I borrow 100K today and repay 98K in 12months you say? Wow, awesome! Lets plough the free money into property!

Logic would suggest negative interest rates will see property prises surge.

But, the net effect of negtative interest rates is a "reduction" in the money supply, therefore you would expect this to have a downward effect on price levels over time. Uncharted territory, but my assumption the opposite would apply to everything compared to the normal positive interest rate scenario. Therefore I would expect deflation to become more entrenched by a negative interest rate policy.

There ain't no friggin' money. It's a mouse click recorded in "the cloud".

"My argument is that if as it clearly is, housing is the biggest domestic threat to NZ's financial stability, banks should be holding more capital against their housing loans."

Here's a real easy way for banks to do it Gareth.

Put up the interest rates for depositors and....... mortgage holders to reflect the actual risk out there!

But, see, they no longer can because even say...... a 2% increase in rates would be terminal for a great deal of borrowers, thus the obvious hazard to banks.

So....we are heading to zero and negative with the rest of the OECD countries that inflated huge property bubbles they now must keep feeding or .....GFC 2.0

The current options they are ALSO looking at to "lock in everyone to borrowing" and using banks are as follows:

Removing higher denominations of currency, implementing cashless societies, taxing gold etc.......in the hope this will stem any run on banks.

Sounds to me like the GFC bailouts are already happening by stealth!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.