By David Hargreaves

News that the indebtedness of New Zealand households has reached new highs provides food for thought and prompts a certain amount of head scratching.

Is this bad? A portent of disaster? Or is it 'move on, nothing to see here'?

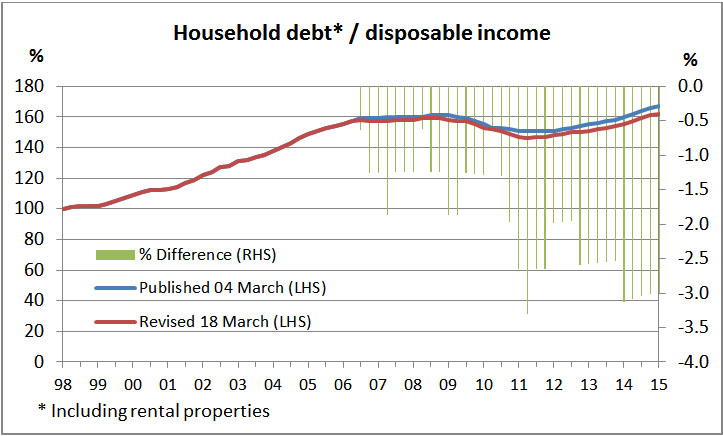

There's a kind of interesting sub-story here. ANZ economists in a recent newsletter drew attention to the new figures, and said they were "not sure we like the end game". They were commenting on the basis of Reserve Bank household figures that showed the household debt to income ratio hitting a new high of 167%.

These comments from the ANZ economists seemingly attracted the attention of the RBNZ itself, whose figures were the centre of attention. Curiously, in having another look at their own figures, the RBNZ have now discovered an error "that occurred when incorporating the annual disposable income benchmarks to the quarterly household income series. We inadvertently did not apply the correct annual benchmarks, which are sourced from Statistics NZ".

The new figures (which can be seen in the first graph below and a comparison with the earlier incorrect figures) show that the debt to income ratio was in fact 162% in December - but the sharply upward trend portrayed in the earlier version of the figures is still very much in evidence in the new corrected data.

In the interests of allowing the ANZ economists a say on the new figures, in their latest weekly market focus, they commented that the 162% figure was "not quite as bad, but still in excess of the GFC peak [in 2009] (of 159%").

"So it doesn’t really change our view that there has been deterioration in some important structural metrics within the economy. Household saving has fallen, and while not as extreme, the ratio of household debt to income has still risen considerably. Households are re-leveraging. It needs to be watched," the ANZ economists said.

Indeed. At which point I come back to the question in the headline on this article: "How much is too much?" It is not a rhetorical question, but it's one that appears impossible to answer.

The fear is that we find out the answer when it's too late and there's a very nasty accident already happening.

I suppose the first thing that should be stated is that we as a country are not 'out there' with our debt levels. On the contrary.

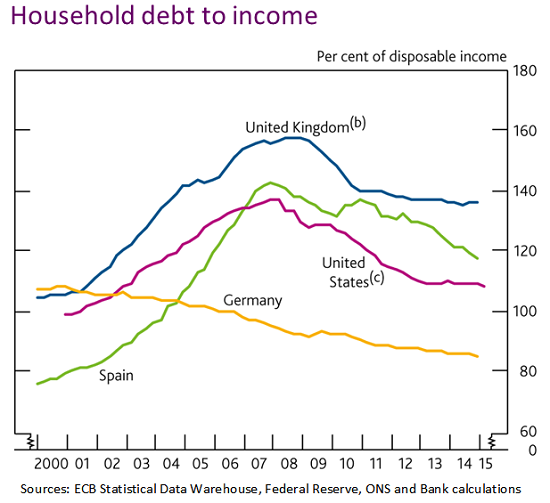

OECD figures as of 2014 had the ratio in Australia at over 200% in 2014, although Reserve Bank of Australia figures - as shown in the second graph below from just last month - paint a slightly, though not much more, conservative picture.

The same 2014 OECD figures showed Denmark's ratio of debt to disposable income was over 300%, while fellow Scandinavian countries were over 200%.

The attached Bank of England graph from last year (below) shows that the UK, German, US and Spain are somewhat more restrained than us and haven't been rising quite like ours have recently.

To switch back to New Zealand, if we go back a while, the RBNZ figures show that as of December 1998 household debt to household disposable income stood at 100%. Presumably that was considered a lot then - given that it was a lot higher than had been seen historically.

But with the onset of the early 2000s housing boom the ratio blew out rapidly, going past 150% by early 2006, before peaking at 159% in 2009.

After that there was a pullback as far as 146% by early 2012, but since then its been onward and upward again and the 'go' button seems to have been really pushed in the past calendar year, which saw the figure blow out from 155% to the new record high of 162% in December.

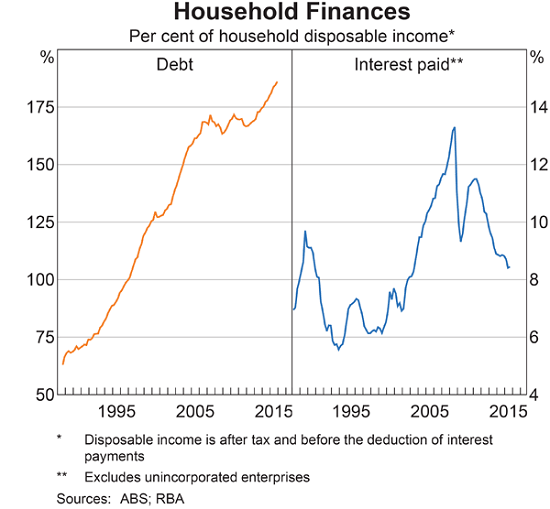

So, what does this all mean, really? Well, the key thing really is not so much the quantum of debt - but the serviceability.

Back in 2009 when the debt to disposable income ratio hit the previous high of 159%, the portion of disposable income going toward servicing that debt was just a tick under 14%. Now, however, the figure (as of December) has actually been dropping and sits just above 9%. As some form of comparison the debt servicing ratio figure is now lower than it was in 2000 when household debt to disposable income stood at 'just' 107%.

What this tells me is that there is plenty of room for that 162% figure in December 2015 to be blown out much further this year as we look at the RBNZ likely driving interest rates down even lower. Next stop 200%. Anybody for 250%?

But are interest rates going to stay at this level forever? They are at historic lows now, surely that is every reason to believe at some point they will go up again - by how much, we can only speculate.

The point is the higher and higher that debt to income ratio gets, the more there's a real risk of something really nasty happening if and when interest rates revert to levels more like those seen in the past.

I don't think we can be complacent now. I think this is one instance in which people may need saving from themselves.

To me the logical answer here is for the RBNZ to be looking very soon to increase the amount of capital that banks must hold against mortgages. Probably the best way of doing that would be to simply increase the 'risk weightings' the banks have to give their mortgage portfolios when calculating their capital adequacy ratios.

I know it's the international rules, but it seems very strange to me that banks can effectively get away with including less than a third (in the case of the big banks) of the value of their mortgage portfolios when working out their capital ratios - this for assets that in fact make up more than half of all banks' exposures.

By forcing the banks to hold more capital against their mortgages the RBNZ will rein in the mortgage lending - helping to, as said, save people from themselves when it comes to over-committing.

If there's no action now, you just wait and see what that debt to income figure will look like in 12 months time.

If a figure starts to look scary, do something about it. Before there's a big mess.

55 Comments

Thanks David. I think that the focus on serviceability of debt is problematic as it ultimately reflects interest rates. But you can rightly argue that interest rates are low for a universal reason: the global economy is sick. That makes the whole issue of private debt more complicated.

I would think that understanding what are the limits of private debt is partly answered by the equilibrium with public debt. Secondly, given that we run persistent current account deficits, that would suggest that our tolerance greater private debt to be relatively higher than the Watanabe family in Japan.

.............." people ..... need saving from themselves........ ".

Why do we need to nanny people ?

Having asked that , we do need awareness programs and reckless lending laws for Banks like many countries have .

If a bank or lender lends recklessly or in a predatory manner to a borrower , then they should not have recourse in the case of default .

banks can effectively get away with including less than a third (in the case of the big banks) of the value of their mortgage portfolios when working out their capital ratios - this for assets that in fact make up more than half of all banks' exposures

Well done David. You put it so diplomatically, burying your case deep in the depths of the article. Why not lead with a big bold "irresponsible" headline like:

BANK RESERVE FIGURES ARE A BIG CON.

or more diplomatically:

ARE BANK RESERVE FIGURES A BIG CON?

The issue you deal with here is really important, why be frightened of making a little noise? The point is the central bank planners have taken off where Gosplan left off, all those years ago. Gosplan tried to set prices individually and failed. The current crop of well intentioned central planners have been trying to set all prices at once via interest rates. They have failed too, but are still denying it. The result is a level of debt that is unrepayable.

Many websites need advertising and sponsorship to make $. So they never directly hurt the hand that feeds them. That's the world we live in, where one(reader) must often read between the lines to get the hard facts and truths.

So i go to multiple sites and check the background. If in reading something I think there is something hidden between the lines then this is especially true.

Anyone else notice how the household debt/income chart for New Zealand has a very similar trend to the average house price statistic over the same period?

Hmmm what could that possibly suggest?

Well yeah. I'm sure all that debt wasn't spent on iPhones.

Anyone else notice how the two items IO mentioned have a similar trend to NZ dairy land prices up to 2015?

Has the future already been shown?

Debt and the ability to service debt or repay debt are predicated on the perpetual-growth-on-a-finite-planet narrative, the notion that the future will always be bigger than the past and bigger than the present.

That is mathematically impossible, of course, and the writing is on the wall that limits to growth have been reached.

Dropping interest rates to zero or negative has held the system together in the short term but fiddling with interest rates does not fix the fundamental predicament of declining finite resources (and a finite capacity to process pollution)..

Once the global energy supply goes into terminal decline (perhaps already starting to happen) the expansion-forever financial system will collapse.

Can your crystal ball tell me what the collapsing financial system will be replaced with please? Also, I think you mean "fossil fuel energy supply"., The Earth's energy supply won't run out until the sun stops shining not to mention we have other non-solar technology already that does not rely on fossil fuel. Why can't fossil fuel energy supply just be replaced with new technology? Why does it always have to be the end of the world as we know it?

The energy density from solar is nowhere close to that of fossil fuel. As the EROEI of fossil fuel declines solar will take over but it's not going to be pleasant. We wont all be able to live like kings anymore.

Solar is but one option. I say new technology will take over and we'll just keep on destroying the planet and accumulating debt. I don't think we will be so lucky to see the end of fossil fuels lead to some sort of beneficial change for the planet and all of it's inhabitants. I think the end of debt will be around about the same time as the end of human occupation here.

I'm pretty sure a Kiwi was involved in discovering the answer to the energy problem nearly a hundred years ago.

Yeah but nuclear is a hell on earth nightmare. Globally there's one meltdown every 10 years on average. About 985,000 deaths from Chernobyl alone apparently. I like the idea of direct conversion of gas to electricity- Bloom energy etc.

What a crock of absolute crap. Drinking the green party kool-aid?

Chernobyl, the worst disaster in history and totally incomparable to modern western power stations, racked up about 6000 deaths. Bad enough if you were Ukrainian. But even including Chernobyl in your reckoning, which you shouldn't because the rest of the world doesn't use Soviet technology to do nuclear, and considering impact on environment and human cost of all historical disasters, nuclear is the cleanest and safest form of energy production BY FAR.

Wrong - Fukushima was the worst nuclear catastrophe in the history of mankind. It was a triple melt down with a criticality fuel pool explosion. The death toll from Fukushima over the next 30 years will probably be in the millions. Regarding Chernobyl, the 900K+ death toll is from a meta analysis published in the Annals of the New York academy of sciences called "Chernobyl: Consequences of the catastrophe" . Fukushima was a Mark 1 general electric reactor. There are many reactors of this type in operation all over the world. Its just a matter of time before another one blows up.

...and a 30 second google of "Regarding Chernobyl" brings up... Stick with WHO.

"In this book, they suggested a departure from analytical epidemiological studies in favour of ecological ones. This erroneous approach resulted in the overestimation of the number of accident victims by more than 800 000 deaths during 1987-2004. This paper investigates the mistakes in methodology made by Yablokov et al and concludes that these errors led to a clear exaggeration of radiation-induced health effects."

"The value of this review is not zero, but negative, as its bias is obvious only to specialists, while inexperienced readers may well be put into deep error. ... Yablokov's assessment for the mortality from Chernobyl fallout of about one million ... puts this book in a range of rather science fiction than science."

So you're saying that a 349 page long meta analysis which is based on hundreds of scientific papers. Papers by Russian scientists who were locked in prison for studying the deleterious effects of Chernobyl fallout. You're saying that meta analysis is wrong! A meta analysis by the way is the highest quality of scientific evidence. Anyway the meta analysis is wrong because you googled the abstract of a single paper with a single author who claims that the meta analysis had a methodology flaw. okay!

And then there was the WHO meta analysis posted below. Did you miss that? Your hand wringing is baseless.

I'd be very skeptical about anything the IAEA touched. Their mandate is to promote nuclear power.

I see the author is a co founder of Greenpeace Russia - now that will be a an unbiased opinion. I think I'll stick with WHO on this one.

And Fukushima. Hand wringers had it so easy before Google came along...

"Global report on Fukushima nuclear accident details health risks

28 February 2013 | GENEVA - A comprehensive assessment by international experts on the health risks associated with the Fukushima Daiichi nuclear power plant (NPP) disaster in Japan has concluded that, for the general population inside and outside of Japan, the predicted risks are low and no observable increases in cancer rates above baseline rates are anticipated. "

http://www.who.int/mediacentre/news/releases/2013/fukushima_report_2013…

Um not so sure,

http://www.globalresearch.ca/new-book-concludes-chernobyl-death-toll-98…

or,

http://www.theguardian.com/environment/2010/jan/10/chernobyl-nuclear-de…

Also sure we dont use their design but there have been enough incidents around the American PWR/BWR or its waste storage that I'd be a little circumspect. PS In fact Ive worked on subs with PWRs and Id rather not go near them again however safe they are claimed to be.

"Ive worked on subs with PWRs and Id rather not go near them again" wow :)

985,000 deaths? "Most emergency workers and people living in contaminated areas received relatively low whole body radiation doses, comparable to natural background levels. As a consequence, no evidence or likelihood of decreased fertility among the affected population has been found, nor has there been any evidence of increases in congenital malformations that can be attributed to radiation exposure.

Poverty, “lifestyle” diseases now rampant in the former Soviet Union and mental health problems pose a far greater threat to local communities than does radiation exposure.

Approximately 1000 on-site reactor staff and emergency workers were heavily exposed to high-level radiation on the first day of the accident; among the more than 200 000 emergency and recovery operation workers exposed during the period from 1986-1987, an estimated 2200 radiation-caused deaths can be expected during their lifetime.

About 4000 cases of thyroid cancer, mainly in children and adolescents at the time of the accident, have resulted from the accident’s contamination and at least nine children died of thyroid cancer; however the survival rate among such cancer victims, judging from experience in Belarus, has been almost 99%."

Not entirely true. Ever heard of Thorium reactors? Liquid Salt reactors? Do some research

They are fascinating pieces of kit. If Nixon had not killed its research off I think we'd have thorium reactors all over the place producing electricity safely and cheaply today. If I could spit on his grave I would.

I very much hope you are wrong as the end of debt looks rather close.

Solar isnt a good transport fuel. So to make it so needs even more technology and equipment driving its price even higher for cars, well for some ppl, the well off sure. Then consider the massive dumper trucks needed to haul poor grade ores from deep and how they would even use batteries, well they will not. "kings" yes agree. However how will the non-kings of today seeing they will never get to be kings like us react when they see it aint gonna happen?

"A natural gas deposit straddling British Columbia, Yukon and the Northwest Territories could be one of the largest in the world, according to a recent assessment."

http://www.cbc.ca/beta/news/canada/north/liard-gas-basin-nwt-1.3494985

CH4 + O2 goes to CO2 + H2O

So, if all that gas does get extracted and burned the Earth will become uninhabitable a little faster.

https://scripps.ucsd.edu/programs/keelingcurve/wp-content/plugins/sio-b…

{kind=link}

Take a lie down AFKTT. 6CO2 + 6H2O -> C6H12O6 + 6O2.

Profile, I know you don't like inconvenient FACTS that demolish your ideological arguments, such as that emissions of CO2 far exceed photosynthesis, which is why the atmospheric CO2 is at a record high and the annual rate of increase is increasing.

https://www.co2.earth/co2-acceleration

Here's another inconvenient FACT which demolished your 'everything is wonderful' narrative: global temperatures were a record high in February 2016 and severe droughts (largely unreported by the mainstream media) are destroying food production in numerous locations.

https://www.theguardian.com/science/2016/mar/14/february-breaks-global-…

With record high CO2 (and increasing) we must expect temperatures to go much higher, much faster and the mayhem to increase..

.

I have no idea what the current system will be replaced with in the short term because the global 'elites' will attempt to impose increasingly fascistic regimes in order to maintain some semblance of status quo.

However, further down the track barter of things of value is the likeliest system

The present system is critically dependent on pumpable and storable liquid fuels -especially hydrocarbons in the C number range 8 to 15. (petrol, aviation fuel, diesel, shipping fuel etc.)

All so-called alternative technology is in fact a sub-set of the fossil fuel economy; you cannot make anything from metal, plastic or ceramic without fossil fuels. Mining, transport to refining facilities, reduction of metal ores to metals, purification of ceramic ingredients conversion into useful products and transport to the place of use are all dependent on fossil fuels. Try removing everything made from oil or made using oil from your home and you will be left with almost nothing..

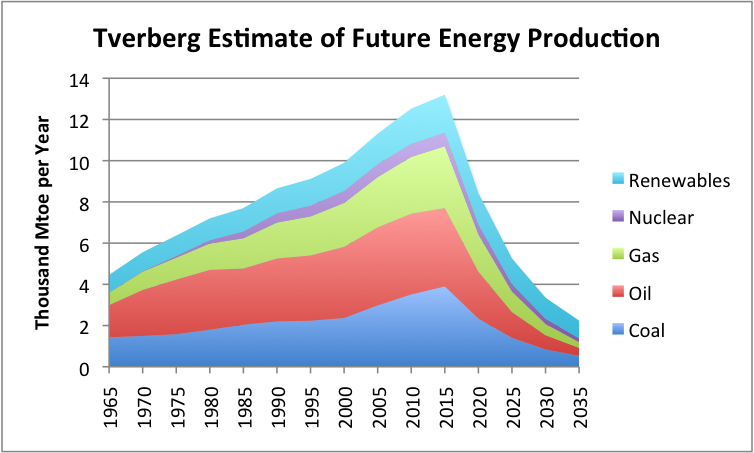

Even if this analysis

https://gailtheactuary.files.wordpress.com/2014/01/tverberg-estimate-of…

{kind=link}

is out by several years (unlikely) it is clear present system has no future.

New Zealands household debt, yes New Zealand has a problem , by simply encapsulating all the data to hide the problem . Auckland household debt/income exceeds 300 percent .

Yes - but these figures include the roughly one third of Auckland homeowners who have no mortgage.

If you calculate AKL household debt for those with mortgages you will be looking at well over 400%.

No problem apparently - I am not so sure.

Asleep at the wheel ?

Power to Gas(P2G)is the big new thing that is coming out of Europe. They take surplus renewable energy, convert it into hydrogen gas which then gets stored in the national grid system and is then used when required.

The Hydrogen fuel cell cars are the way forward. I have driven one. You can literally have a wind turbine and run a car from it. It's not too bad on costings either. Toyota pulled out of Electric cars to focus on Hydrogen.

Back in 2005 George Bush declared that within a few years the US would have a hydrogen economy. It was all a lie, of course, because it takes much more energy to make hydrogen than is released when it is oxidised, and hydrogen cannot be liquefied for transport; nor can it be economically transported or stored in the gas form because it is the lightest gas and the most capable of leaking past valves.

A hydrogen economy is like stating with $100 and trading it for $90, and then watching the $90 evaporate...89,88,87,86....

Despite 'promises' made from the 1960s on, there isn't a hydrogen economy and there never will be one.

;

URL? storing hydrogen in a Ngas grid ie the same pipe would seem very strange.

Just consider that we need about 90million barrels per day and about 27million barrels per day is petrol/diesel (from memory). So we have to build plant to make the electrical power and then plant to convert it to hydrogen, that is Trillions of dollars that needs to be invested today very fast to make a noticable impact in 10 years time.

Then there is the issue of running heavier plant with hydrogen which is no small undertaking.

This is even of course if the technology is affordable and works.

@Machiavelli -Why does it always have to be the end of the world as we know it?

It's a futile exercise arguing with them. Reminds me of that Star Trek mis-quote "It's life Jim but not as we know it."

Interesting, innit, how a thread starts off relatively rationally, and then veers off into the gumbo.

Perhaps, DH, your crew could graph the divergence from the Path of Reason - standard deviations or somefink.

I suspect the result could resemble them Awful Debt plots.....

Yes back to the topic - Steve Keen's models predict that as the private debt rises the financial sector will grow at the expense of the workers share of income. I guess that means continuing destruction of the middle class. Eventually GDP is supposed to collapse and then it's game over. Perhaps in five years time, if it all keeps going, the OCR will be at 0.5% and we'll all be getting a "basic income" from the government of $5000 NZD per year.

Debt levels have be allowed to increase as interest rates have been set ever lower. Many say 'When interest rates eventually rise again some are going to find it tough'. But the question is, is it actually possible for interest rates to return to 'historical levels' (hugely subjective how you actually define that IMO) if principle has crept ever higher in the interim of lower rates?

For example, how would society fare if interest rates were set to 1985 levels tomorrow?

Savers would have a big smile on their faces but credit growth would turn acutely negative without doubt.

Debt is in a sense a structure. If that structure changes over the decades then surely how interest rates are applied to that debt, and to what extent, must also change. This is especially so if income does not adjust in unison as we have experienced in this country.

If we went to 1985 levels of interest you'd find retirees would have cash flow again. I'd put up my rates to help pay for my mortgage (not really it's just an excuse). I would maintain a 30 year mortgage and laugh as the principle diminished to nothing. Savers would suffer as interest rates would be less than inflation.

There would be a lot of pain from those who are already overextended and we'd get financial collapse in some parts of the banking system. Increases in interest rates need to be gradual so the fall out can be managed. Rather than say RBNZ putting rates by 1.75% in a year to chase imaginary inflation.

If you are in china or japan I do not think you ever saw such rates? so we are relying on an anomaly? that with peak oil is now in the past IMHO. Did we get lazy with our capital? I suspect so.

a) No I dont think we'll ever see high rates again.

b) Society would fare badly as our economy would go into recession just like it did before and indeed for every other country that has raised it since 2008.

c) The thing is businesses really only borrow to expand to meet demand. If there is no demand or very little and the costs are too high they will not borrow.

It would be interesting actually if the OCR went up and then no one borrowed. Supply and demand would then apply as it does now, too much deposits no one wants then the returns would surely collapse? or banks refuse to take $s? whatever the OCR rate?

Problem I see is we just don't know what will happen. It would be prudent to pay down debt - but I think NZers are so scared of missing out (fear and greed) - I don't think that will happen.

Could not help notice the decline in German debt levels , they were the highest in 2000 ............ those folk really are single minded when they do things and of course prudent

I noticed that as well - but Germany has always been a bit like that - not like the Anglo-Saxon debtor countries.....

The article glosses over the fact that with miniscule inflation, NZ consumers are still hammered by high real interest on their debt . In Germany you can get 100k mortgage at under 2pc interest. We are relatively speaking, still paying through the nose at a time when incomes for many are flat, and further asset rises uncertain.

Groma - fund your own borrowings internally as a country and you have a chance of getting those rates. Borrow from the rest of the world because of an incapability to save, and you pay what the world will fund your banks at. Comparing Germans and NZ borrowing attitudes, market size/liquidity, credit rating etc is like comparing the proverbial chalk and cheese, and only of interest to those with little idea of finance that may think it is relevant.

What ! I just agreed with Grant A.

Simply put, the more government debts you have, the lower your interest rates, highly indebted countries like Japan, UK, US have very low interest rates, whereas low indebted countries like Brazil, Russia have high interest rates. Of course I explained that using reults based method, if you used system based method then you end up with many more different theories, none of which make any more sense if approached logically.

Which is more relevant, the ability to repay interest, or the ability to repay interest and principal? Hargreaves thinks the only thing that matters is the interest portion, because as long as you pay that, the banks are all good. However if you are only paying interest on non income producing debt, (bad debt) you are pretty much on the road to bankruptcy.

So is the 'ass u me' in this story, that everyone has interest only loans or what? You double the loan, you double the principal payments regardless of interest rates, but you cleverly avoid the topic and disingenously try and focus on serviceability minus principal payments. Which is the kind of loans, giggling property speculators have, but are financial suicide for mum and dad families.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.