By Bernard Hickey

An economist who has studied asset bubbles extensively overseas and has been tipped to win a Nobel Prize has co-written an academic paper identifying Auckland's housing market as again in bubble territory.

Yale Econometrics Professor Peter Phillips and Auckland University Economics Lecturer Ryan Greenaway-McGrevy have just had the paper published in the latest issue of New Zealand Economic Papers, which is co-edited by former Reserve Bank Chairman Arthur Grimes.

Phillips was named a Thomson Reuters Citation Laureate in 2013, which is a predictor of future Nobel Prize winners. He has also published acclaimed papers on asset market exuberance that built models able to explain the expansion and collapse of bubbles. He is ranked as one of the Top 10 economists in the world by RePEc (Research Papers in Economics).

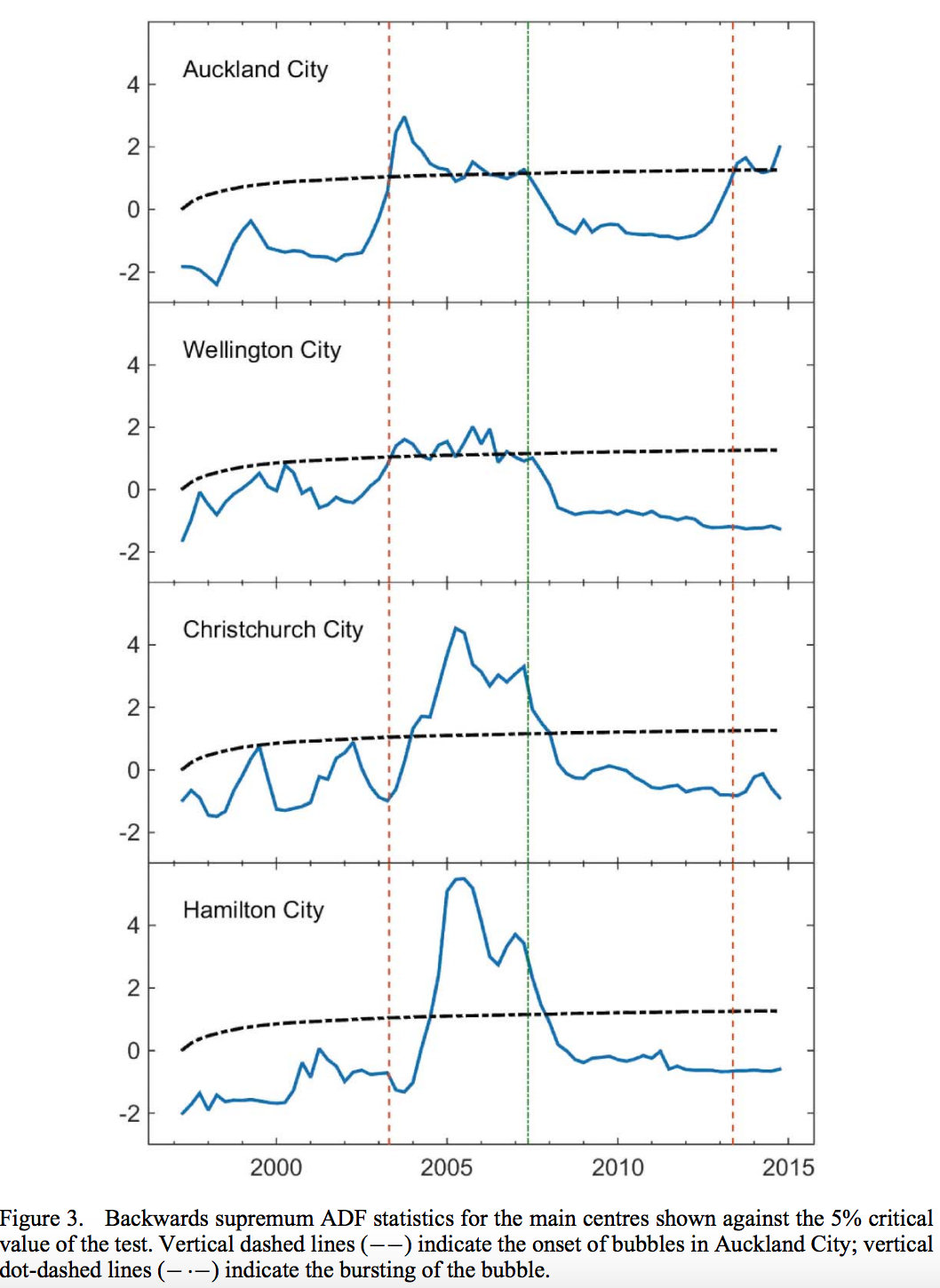

The paper applied econometric techniques used to identify asset bubbles in the United States and elsewhere to New Zealand house price data. It found Auckland experienced a housing bubble from 2003 until a collapse from mid 2007 to early 2008. Phillips and Greenaway-McGrevy found that bubble spread to the rest of the country and that a new bubble developed in Auckland in 2013, although it had not spread as of the middle of 2015, which was the last data used in the study.

"Using recently developed statistical methods for testing and dating exuberant behaviour in asset prices we document evidence of episodic bubbles in the New Zealand property market over the past two decades," they said in the paper.

"The results show clear evidence of a broad-based New Zealand housing bubble that began in 2003 and collapsed over mid-2007 to early 2008 with the onset of the worldwide recession and the financial crisis," they said, pointing out they had used new methods to analyse market contagion and spill-overs from the Auckland market.

"Evidence from the latest data reveals that the greater Auckland metropolitan area is currently experiencing a new property bubble that began in 2013," they said.

Policy makers should be concerned, given the inter-generational effects of rising house prices, the risks to financial stability and the risks that high housing prices could stunt Auckland's growth as employers struggle to find workers able to afford to live in Auckland, Phillips and Greenaway-McGrevy said.

What they studied and found

"Our findings suggest that the Auckland metropolitan area is currently experiencing a property bubble in terms of the house price-to-rent ratio that began in 2013. We also document evidence of an earlier and much broader-based bubble in New Zealand property markets that emerged in the mid-2000s and subsequently collapsed upon the onset of the Great Recession," they wrote.

"The evidence indicates that this bubble likely originated in the Auckland region before spreading to the other main centres. If that recent history were to repeat itself, the ongoing property market bubble in Auckland would be expected to affect property prices in other regions. But, as yet, there is no empirical evidence of this contagion to the other centres from the current Auckland real estate bubble," they wrote in mid 2015 with data up to the end of June 2015.

Since then house price inflation has accelerated in Hamilton, Tauranga, Whangarei, Wellington, Dunedin and other larger cities where Auckland investors have been active.

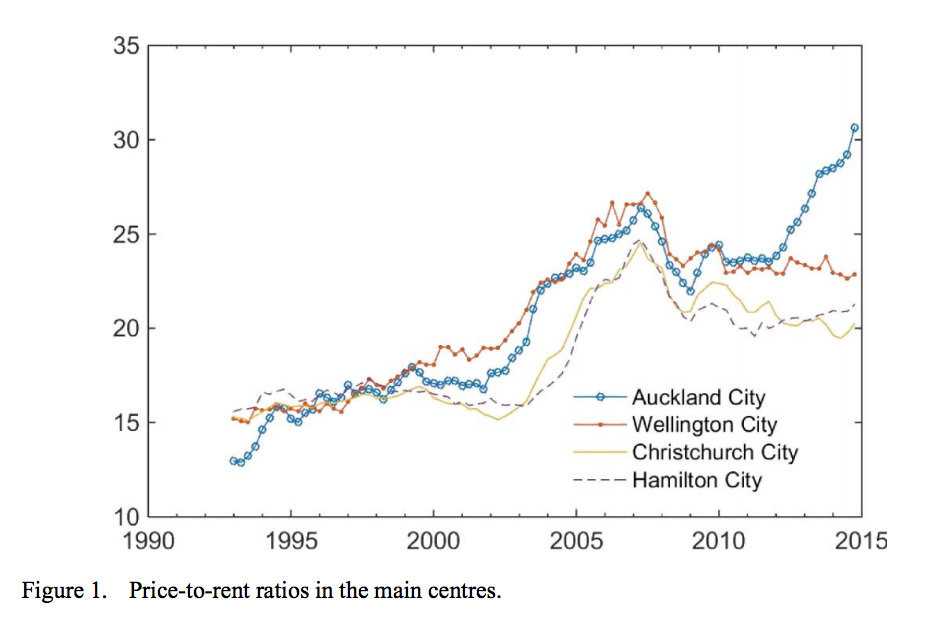

Their paper included indicators of where the bubbles began and when they collapsed, both for Auckland and other cities, and within Auckland. The areas above the horizontal dotted line indicate bubble periods.

They finished the paper with a discussion on how the bubble might collapse, concluding that it was likely to be through nominal prices falling rather than the share of rents being spent on housing rising.

"The price-to-rent ratio can fall by house prices falling, by an increase in rents, or by some combination of these two channels. Household incomes ultimately place an upper bound on the amount of income that can be spent on housing costs (assuming that household incomes are exogenous to housing prices and rents)," they said.

"We show that rental expenditures as a proportion of income have remained remarkably constant over the past decade in the main centres of Auckland, Wellington and Canterbury. For example, in the Auckland region rents have remained consistently around 25% of expenditure since 2003," they said.

"Thus, if a market correction were to come through an increase in rents, this would involve an unprecedented increase in rental expenditure shares. In our view, therefore, any correction is more likely to come through an adjustment in prices driven by a demand or supply side shock, or combination of the two."

It pointed to the 2007/08 collapse where nominal house prices fell by 11% in Auckland City, 8% in Wellington City, 10% in Christchurch and 12% in Hamilton.

"Our findings regarding bubble collapse mirror those typically found in asset markets: termination of a bubble is associated with a fall in the nominal price of the asset, rather than a rise in the fundamental (such as rents or incomes)," they said.

"The magnitude of the price correction is however smaller, and more drawn out, than those found in more liquid asset markets (such as equity markets)."

They do note supply constraints and changes in demand that could be factors in the exuberance and bubble behaviour, beyond the fundamentals of rents and incomes.

"In the New Zealand market, for instance, supply constraints include the country’s physical geography, local zoning regulations, a variety of resource consent or building consent obstacles, as well as shortages of skilled trade labour and construction workers," they said.

"Demographic changes from a growing population, returning expatriates and immigration provide additional demand pressures by injecting new money into the housing market especially for desirable real estate in Auckland City, waterfront, rural and island locations. These pressures overspill with relocations, retirements, vacation home and multiple rental home purchases in a diaspora of new demand in regional markets," they said.

"This short and incomplete summary indicates some of the multifarious influences at work in driving real estate markets beyond the immediate return from rental income and the effect of policy measures that include interest rates and lending practices in the financial industry. Just as the combined effects of these many variables may lead to market exuberance, unexpected shocks to them may equally well lead to market correction."

Why it's a concern

In an introductory part of the paper they explained why policy-makers and the public should be concerned.

"First, the rising cost of housing has major intergenerational wealth effects, reducing the relative wealth and welfare of younger generations, renters and first-time home buyers in relation to extant property owners," they said.

"Escalating house prices also exacerbate inequality by increasing the wealth gap between home owners and renters, raising social tensions."

Secondly, large mortgages and high leverage levels created financial and macro-economic stability risks.

"A third concern for households and policy-makers involves the labour market. High housing costs in metropolitan areas can be an impediment to growth. These costs typically inhibit labour mobility and prevent labour from moving from depressed outlying regions to booming city centres to fill job openings," they said.

167 Comments

In other news, the Pope has confirmed he is still Catholic.

I'd like to believe you, but um... can I see your credentials first? We only accept the word of professors from Yale who are about to receive Nobel peace prizes, and yes, we will also need to see some squiggly lines on graphs also...

no no no i have been told by everyone in auckland until my ears bleed that house prices only go up.

luckly i part deaf though

RBNZ just reloaded the debt bazooka, so I guess it's sympathies and concerns about the risk attached to residential property bubbles lie dormant for now. Isn't it embedded central bank theory that financial stability should only concern the setting of rates to the extent that it interferes with hitting inflation goals?

So it would appear we have a bubble on top of a bubble that never really deflated properly the first time. The bubble is well and truly filled with the hot air of landlords and property speculators. How high will she fly?...

Very high. Chinese money is back.

Silly not to, given the RBNZ governor's welcoming stance.

Yep....and the 1st April is not far away either.

so are you saying...double bubble...?

Jeepers, QE is a Yale Lock, on steroids.

I do believe it is pot calling kettle to task, not in the black, but the red.

Trillions, I do believe..

John Key says he is wrong. So he must be.

Interesting watching some of the interviews by the Irish PM in the lead up to the end of the Celtic Tiger and bursting of their property bubble. Much like we're witnessing with the 'Rockstar' economy and the 'to infinity and beyond' Auckland housing market.

Apples and oranges. Irish market wasn't dealing with Chinese money looking for a safe haven.

You think Auckland property is a safe haven......

I wish it wasn't but it is. Think about how much money is trying to get out of China.

It may be trying , but as I asked before where is your evidence .... you keeping making these statements with no evidence.

The 80% clearance rates being recorded? The fact that an apartment that sold for 735k in oct last year just sold for 917k.

Keep up the denial, it's tactic that works as shown by Key.

I call that the bigger fool ... also selective use of statistics... and who says Chinese are not fools as well.

"kiwis so stupid lah", the biggest fool is the one selling out the younger generation.

Just look at the Chinese stock market over the last ten years. The behavior is either 'all in' or 'all out'.

It has been all in on Auckland property of late. Can't be long till it's 'all out'. There doesn't appear to be any half measures. Confidence is either incredible high, or incredible low. A very strong herd mentality which creates strong boom/bust cycles.

And, do we really believe that the govt won't hand all that buyer information over to Beijing with minimal arm-twisting?

They've obviously cut a deal already. Get them to register and then hand over as part of Operation Foxhunt. Squeaky bum time.

That's my feeling. It's a trap. Like a big cardboard box propped up on a stick with a carrot under it. When will they pull the string?

John Key is the Bertie Ahern of the South Pacific. The man of the people schtick, doing daytme radio interviews. The role of financial genius, giving speeches to other countries on how to replicate the tiger. And then it was gone. The lack of any guiding principles or vision - read Ahern's wikipedia entry:

https://en.wikipedia.org/wiki/Bertie_Ahern#Legacy

"What does he actually stand for? In some ways Bertie's lack of vision was a positive, it made him flexible and willing to compromise, and he was certainly outstanding in that regard. But I dissent from the universal plaudits going around at the moment. He had no social or economic vision for the state he led. There was no fire in his belly. He didn't really want to change society for the better. He was the ward boss writ large. But at the moment it seems it's unfashionable to say anything adverse about Bertie"

Ryanair chief executive Michael O'Leary noted in a radio interview that

"Bertie squandered the wealth of a generation and I think in time it will be proven he was a useless wastrel." In November 2009 Ahern was again criticised by O'Leary, being described as a "feckless ditherer".

Who the heck is Bertie Ahern ???????

Does he play for the All Blacks ??????

The greatest gangster to play for Ireland (Govt squad!)... I was replying to the message above about comparisons with Irish PM. I completely agree. When Key falls he will fall hard because expectations of him are so high yet the delivery and reality can't keep up. The "do nothing" PM will become his legacy. He rode a bubble or two, told a few porkers and embarrassed us occasionally on the world stage.

Oh yes, the former minister for Finance who famously did not 'have a bank account'.

.

I must check and see what he's up to now....

This is a really good watch given current circumstances:

It's funny. You can imagine being in the future, looking back on now with the start of the China slowdown, the impact on the dairy industry, the banks lending crazy amounts to anyone and think 'how could we/they not see it?'. But we are not really seeing it or feeling it. The power of the media, politicians and herd mentality. I genuinely hope that a bubble doesn't pop even though I want house prices to stop rising. It would be a disaster for NZ.

The best way to stop cancer is through chemo. We must feel the pain before we start to get better.

Unfortunately, it doesn't matter anymore.

How can a downward movement of 11% in Auckland be a 'collapse'? That's simply a decent correction. A collapse is what happened in the US, UK, Spain, Ireland, etc where the movement was more like 40% or so. Besides, is a collapse in Auckland likely with such a high level of immigration, a large housing shortage and the place rapidly developing into what we are told is a 'world' city? Sure, there will be further corrections, but a 'collapse', unlikely. In my experience since 1970, there has never been a collapse.

In my experience since 1970, I've never had a heart attack. Therefore I will never have one in the future.....

i just cant see prices going down till interest rates go up.Wern't the interst rates 10% in 2007 when the last correction happend?Basicly anyone can afford a rental or two at4.5% interest rates

Yep, just have to fog a mirror.

"Wern't the interst rates 10% in 2007"

Yes, and even then it was too little too late. The game has changed since those pre GFC bailout days though. Now due to the even more debt out there, here and globally, they (RB's) have essentially locked themselves into a game they can't win without forcing a crash to reset everything. That will does not exist at present, so........on we go lower & lower until NZ also is at zero or dare I say negative at some point. Unless the correction occurs sooner which I think in NZ it will before they get to that level.

That paper seems to be missing some contextual detail...

1. China has poured 6.6 gigatons of cement since 2007. That's more cement than the 4.4 gigatons that was poured by the United States over the entire 20th centuary.

2. China's Debt to GDP ratio has almost quadrupled from 7.4 (in 2007) to 28.2 (Q2-2014).

3. James Rickards in his book "the Death of Money" describes whats going on in China as "the greatest episode of capital flight in human history". Despite denials from the government it seems pretty obvious that Chinese capital is the primary driver of Auckland's house price inflation.

Perhaps that has nothing to do with anything, but it doesn't seem sustainable. I sold a house in AUckland on Wednesday. Thankfully I got way more that I was expecting. The buyer was Chinese.. I've lost confidence in the Auckland market. Glad to be out and debt free.

He is ranked as one of the top ten economists in the world by RePec. And how are the rankings collated. . Sorry there is nothing in his numerous works that give any credibility to his ramblings about predicting forecasting or indicating bubbles. A Nobel prize for what .

Cowpat - "his ramblings"....? Info on "Peter C.B. Phillips selected a 2013 Thomson Reuters Citation Laureate"

"The distinction highlights the significance of Phillips’ work in the eyes of the scientific community. Each year, Thomson Reuters — a world leader in intelligent information for businesses and professionals — chooses individuals for the distinction based on analysis of data from the research and citation database Web of Science, which identifies the most influential researchers in the categories of chemistry, physics, physiology or medicine, and economics. The company predicts that the researchers named Thomson Reuters Citation Laureates will be Nobel Prize winners, either this year or in the future".

"Phillips is among eight economists chosen as laureates. Along with six others, he was selected for contributions to economic time-series, including modeling, testing, and forecasting".

Firstly , his ranking is based upon the number of articles he writes/coauthors. Write more, ranking improves. He is one of 74 Thomson citation laureates for economics over the last decade. There is one Nobel prize for economics per year, alongside true sciences of medicine , physics and chemistry .His most cited works relate to the unit root . I cannot recall any of his much vaunted works/economic models predicting with accuracy any financial/asset bubble over the past two decades. Possibly he needs to nail a bubble to get the prize. Again his commentary of the New Zealand housing market 2003-2007 is inaccurate .In almost all regions prices moved in timely tandem, in fact Queenstown Lakes moved first, the spillover from Auckland as quoted appears inconsistent with the REINZ regional median house price in that period. The RBNZ, another group of economists appear at odds with his forecasting prowess.I brought an Auckland home in 2002 , when arriving at the airport after 8 years away, I asked the taxi driver how were things feeling in general .I did not use any Phillips modelling to make a decision . Those on the ground generally will give a better summary of the economy than those that are stuck in 'tall' buildings. By the way did he date stamp the dairy powder bubble .(As an aside I believe Auckland to be a monumental financial risk to New Zealand, I do not recall using Phillips works to come to that conclusion)

Well then, isn't the world unjust? It sounds like you deserve a Nobel prize more than he.

If you had any experience in economics/econometrics you would be well aware of the contribution of Phillips over the past 30 years and understand why he is deserving of a gold medallion in the future. His work on time series has had an influence on, essentially, all modern forecasting methods.

The fact that his publishing is, arguably, light on bubbles in particular is relatively irrelevant in this case. The true fact of the matter is that he, along with Ryan, is an world class econometrician who can be trusted to provide robust methods of statistical analysis and forecasting in all of his works.

If you are at odds with their analysis by all means write a rebuttal to the methodology and results. Any journal (and research institution) would be very interested in a researcher who could reliably challenge him.

Until then there is nothing that gives you the credibility to question his deserving of a Nobel prize. In my opinion..

We are in the biggest residential property bubble since records began.

Every day that prices continue to rise, the closer the day comes when the bubble will burst.

It is even making international headlines with NZ and Australia leading the dangerous race to the top.

See:

http://www.cnbc.com/2016/03/18/australia-nz-property-prices-the-stronge….

I give it 12 months tops, before it blows.

Warning: If you own highly geared residential property, get out now while you still have the chance. .

Not before we hit 1.8m median, like in Vancouver

That would be good

As far as I am concerned there are many better investment opportunities than AKL property. Anyway AKL is a tiny market when you look at other urban areas in the world. Places like Lyon, Manchester, Virginia Beach, Columbus, Hartford are places in the world which you may not necessarily heard of but are larger. The NZ share index is up nearly 30% over the last couple of years as a comparison- not bad.

I'm personally more interested in investing overseas right now as the NZD is at least 10% too strong with everything going on in the Dairy industry.

If people are prepared to chuck more money at the AKL property market then I will sit back and reap the rewards on paper at least.

The funny thing is that even the Govt have said they don't want AKL property prices to go up more and will introduce further cooling measures if prices do keep going up. Look at how the UK Govt have halted the overseas buying of London real estate in last year.

Hartford has a declining population with 30% living below the poverty line. It is smaller than Hamilton. Even Greater Hartford is smaller than Auckland.

https://en.wikipedia.org/wiki/Hartford,_Connecticut

Australia’s house prices, particularly in Sydney and Melbourne, and high household debt levels have become a headache for regulators. Mortgages account for about two-thirds of the loan books of the nation’s largest banks, forcing the regulator to increase supervision and introduce in new rules to protect the financial system from a housing downturn. Read more

Perhaps even the banks have forgotten about diversification of risk

You will notice that the amounts loaned to 'investors' by the Australian banks have been curbed - in several ways including charging a higher interest rate for the same mortgage amount for all investors compared to owner-occupiers.

Somewhat different from NZ where it seems that the investors are the prime beneficiary of the lowest residential mortgage interest rates in 50 years and still clamouring for even lower rates - supported by the RBNZ and the main political parties.

Will Donald Trump be the Black Swan that bursts several such bubbles ?

We can only hope.

.

People tend to focus on the expensive suburbs in Auckland when talking about high selling prices however I have been checking TradeMe asking prices for houses in the less affluent southern suburbs like Manurewa and Papatoetoe and found that many are asking 70% plus over CV. This one advertised as a "Brick And Tile Beauty - Price To Sell !" is a staggering 111% over CV:

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

These suburbs seem to have shot up recently because they are affordable and attract FHBs and PIs.

The one above if bought for CV would yield 10.4% which would be a great return. Even at its current asking price it would yield 4.9% if you can get the rent claimed which aint bad.

A combination of high rent and low mortgage interest rate will at least keep prices stable.

The bubble is not in question, just the date of it popping.

It could go on for a while or explode next week.

How do people sleep at night without wondering if the fat lady is clearing her throat or the bastardo who rings the bell at the top has lost his clapper?

I think bubble bursting is the wrong analogy. Housing in Auckland cannot be compared to the classic Dutch Tulip bubble where the product wasn't in actual fact worth much. Houses get rent and provide places to live. The super city of a country is likely to always be valuable because that is where the work is, that is where the cultural activity for new migrants is and so on.

So bubble may spring a leak which will eventually be patched but it wont "pop".

My prediction of worst case scenario barring an epic event like natural disaster or war would be that prices would return closer to CV and people who have bought in Hamilton or Tauranga or South Auckland for twice CV could enter negative territory if they only had small deposits. But with low mortgage interest rates they would just hang on. Landlords may just sell one or two of their houses that have high capital or even their own family home if it is mortgage free and balance their portfolio. It's not like the end of the world.

The thing is you could say to someone," your house isn't worth that much!" They would say, "but it yields 5% and my mortgage is only 4%" or "okay then don't buy my house go and buy in Tokoroa".

Slight variation - prices will drop then stagnate as people don't want to sell and realize any loss. Yes NZ is in a global market and it may be events in another part of the world that cause the most pain. Aussie banks coming under increased pressure due to bad loans at home - the 60 Minutes video referred to elsewhere shows that it may not be Sydney or Melbourne that sinks the banks but the little towns where prices got unrealistic due to the boom - and now the loan is far greater than the value of the asset. These add up .....

For the record, I have been saying exactly the same thing, for the last couple or three years.

I can beat that. I have heard people saying this since 1985!

I remember a guy telling me he was selling up because at 70K houses had reached their limit and weren't viable. In 2003 I remember reading reader comments in investment magazines claiming they were waiting to buy when the bubble burst and they could scoop up cheap property from desperate FHBs.

Zac you sound like the wise men who were promoting stocks in 1929 just before the fall. If you were smart you'd at least show some caution to the precarious situation we find ourselves in. But it's like your amygdala has been permanently hijacked.

We have put forward many arguments as to why this is not a bubble in the classic sense. I think SpaceX has it right about it being a global market now. We have even suggested different scenarios and outcomes but you just keep saying the same thing over and over again. It's like your amygdala is stuck on repeat.

Honestly, my comment above is just a truthful recollection,nothing more really.

Mark Twain had a relative well known quote. It goes along the line of 'never ague with stupid people, they will only drag you down to their level and beat you with experience'.

You possibly mean:

"Never go down to wrestle with a pig, you only go dirty and the pig will enjoy it."

"Those who believe no proof is necessary, those who don't no proof is possible" Stuart Chase.

Iran to invest over eight billion in foreign property. After our PMs hugs and cuddles with Iran's foreign minister and the usual interest from China, Auckland's property prices are set for an even steeper trajectory upwards!

Another expert trying to describe human behaviour using an equation; yep that'll work. Does he have a co-efficient for hot money escaping China, or an x-factor for climate refugees from wherever, or even a multiplier for cashed up Wall street shysters getting out of dodge. NZ housing demand is less a factor of internal 'fundamentals' (whatever that means in todays negative interest rate world), and more and more driven by international events; events that defy equation driven drivel. Hows that weather forecasting going-El nino anyone?!

"Policy makers should be concerned, given the inter-generational effects of rising house prices, the risks to financial stability and the risks that high housing prices could stunt Auckland's growth as employers struggle to find workers able to afford to live in Auckland, Phillips and Greenaway-McGrevy said."

But our super-popular prime minister, Teflon Key, says Auckland property isn't in a bubble, so it can't be.

What would these authors, whom have devoted themselves to years of research, know?

Better to follow the Pied Piper into a fourth term.

World economy is running out of steam, interest rates can't go much lower, free trade agreements will be exhausted... then what? Will we need to find life on other planets to invest here to keep bubbles inflated? Debt should be a means to fund growth industries not to create them.

There is a way to solve a lot of the problems. The not profitable state run businesses need to fail to reduce oversupply. The low interest rates are just sweeping major problems under the rug hoping to maintain jobs under demand picks up again.

It's just that politicians won't burst a bubble because they know they will lose the next election in a landslide. In NZ stagnant house prices are a better solution than bursting the property bubble and causing a financial stability problem.

Two things that would change our current environmental situation are fusion power and asteroid mining. They are both too far away unfortunately.

Some of naively thought that prices began to stagnate, but there you go, as shown in the last month, it's continuing to sky rocket again. Ron Fong Choy was right.

The big money has been made. People are starting to look elsewhere to deploy capital. There is a world outside AKL!

There is nothing about making money in this, that's just a side bonus. Chinese won't buy out of AKL. This is all about store of wealth.

Chinese money is gone. The idea they are returning is a media construct not backed with anything more than wishful thinking. Evidence is on the ground, in the collapse of Chinese junket market in Macau, in the fact that you don't have to register for IRD in Australia and Canada. Why risk NZ?

Dream on. it is all about store of wealth without being seen by the Govt back home.

And in Aus they risk having the house confiscated.

A month ago I would have agreed with you. But the evidence is there. 80% clearance rates, units and houses being sold for much greater amounts than what they were bought for at the end of last year.

This is reality. You can choose to ignore it or you can choose to accept it and vote for change.

'wishful thinking' - maybe they rang the IRD and asked how many applications are on their desk?

I don't think much of this paper.... ( I skim read thru the whole thing ).

This is their premise... ( how they define a "bubble".. )

Our findings suggest that the Auckland metropolitan area is currently experiencing a property bubble in terms of the house price-to-rent ratio that began in 2013.

I can understand that the use of rent/price or income/price ratios are helpful in the discussion on affordability...

BUT... To try to define a "BUBBLE" using just those 2 metrics is simply insane.....

There is a reason that Bubbles are difficult to see until one gets the "crash" that follows a bubble.

Bubbles are rare events.... they don't happen very often..

They label what they are trying to measure as a "Bubble" when really it is nothing more than defining when property might be "overvalued"..... or "affordable "

Has about as much predictive value as a P/E ratio in the Share market..

There is no mention in their paper about how lower interest rates affect Capitalization rates....

( rent/ price ratio)..... and yet interest rates are an important consideration...

etc...etc...

Conclusion...: The analysis used in this paper is incapable of predicting anything....( If one can define a "bubble, then one can predict the imminent crash ...). and, basically, only defines affordability issues..

It is so easy to label something a bubble..... any doomsayer can do that..and they do it all the time... One does not need to use fancy statistical, econometric methodology....

Roelof, there are a number of factors that could well indicate we're in a bubble.

- Look at the outside of this website. What is it advertising?

- Pick up the news paper. Read the business section. What is the dominant theme?

- Turn on the TV at night. What shows are most often on? Home renovation and Location, location, location.

- Listen to the radio. What is it playing? Advertisements for property investment coaching.

- Go to a BBQ. What are people talking about? Their property investment portfolios.

- Watch the 6pm news. What is it is saying? Historically overly priced property.

- What are the banks talking about in their public notifications. Concerns around property prices and the high level of debt we have.

- Ask the masses if they think they're in a bubble. They deny it - and believe prices will climb forever (another classic sign).

All of the sign posts are there. It's smacking us in the face every day. Don't believe it, well nor did any of the masses involved in most other bubbles. Read the works by Robert Shiller on bubbles. We have all the classic signs and symptoms. Its just a matter of whether you want to accept them or not.

-

Look, if it were only NZers buying and selling, then yes I would agree with you that we are in a bubble. But it isn't, NZ housing is a global commodity, and prices don't care what NZers can and can't afford. It's about what the rest of the world can afford and compared to London, Beijing or Shanghai, NZ housing is cheap and even better so, it's an amazing investment where you don't pay tax on the gain! and better yet, we are "Safe".

NZ is not "safe" - sure we're unlikely to be invaded , but we're not called the shaky isles for nothing and as NZ is in an international market - events happening in other parts of the world could have a significant affect on NZ (in unpredictable ways).

NZ is only "safe" until we are not "safe"

I agree we are not so safe, we are high risk. One thing overlooked with the current euphoria is the impact of cheap fuel. This has effectively made NZ closer to its neighbours. However, this cheap fuel may disappear in the blink of an eye, effectively pushing us further away again. the last few years is an aberration......abnormal and cannot last. Get debt free while you can.

It's better than that. If the cheap oil disappears it means inflation. If they follow the script that means interest rate rises to keep CPI at 2%. Fortunately those collapsing home values are excluded from CPI.

You didn't bother to read the paper then.

"The statistical test for exuberance that we employ is rather conservative.

For example, under the null hypothesis log normalized prices yt exhibit a stochastic

trend, and the constant in (1) allows normalized asset prices to contain

a non-random drift component. Thus there need not be a long-run relationship

between the asset price and its fundamental under the null; in particular,

normalized prices are permitted to grow indeÖnitely. As shown below, price-torent

ratios across the main centres of New Zealand have experienced sustained

increases over the past two decades - particularly in Auckland - but this feature

of the data is not in itself interpreted as evidence of a bubble under our

approach. Only those periods during which normalized prices exhibit sustained

exponential growth will be identiÖed as bubbles."

Right, so you read the paper, but you didn't really understand it.

It's more than just whether the price to rent ratio is high. I'll leave you to figure out the rest.

here is a great website that shows price/income ratios in various cities around the world...

http://www.numbeo.com/property-investment/rankings.jsp

compare these with Auckland ... ( the above economic paper says 7.87 puts Auck. in "bubble" territory )

How is it possible for Hanoi to have a price/income ratio of 35..???

In theory...( the above economists ). Hanoi should have been bubbled .."out of existence"...???

What would happen to the price/income ratio in the Cook Islands if foreign ownership of land was allowed over there..??? the price/income ratio would not be a reflection of being in a Bubble ....but of far deeper sociological issues...

Issues on what is most important for the people of a society..

The real bubble is in the creation of more and more debt, to keep these asset bubbles going. The dow jones has dropped and recovered Approx 12% this year on news about fed reserve rates. The problem with low interest rates are that they are deflationary.They create overcapacity and suck disposable income into non productive bubbles. There are too many dairy farms in the world ,too many oil producers, how long will it be before there are too many houses? Too many mortgages and not enough income to service them.

I very much doubt anyone here has tried to tackle what is going on in this paper regrading the models that Phillps and McGrevy have done. It's much easier to fall back on throwaway arguments that people digest daily through the media. The irony is that the paper itself tests for "market exuberance". This is an interesting development in itself.

So within two days , we have Retirement Dianne , get on the ladder young person (or is that I have a house to flog to you), Maxwell as a way to improve your retirement outcome , followed by an academic Phillips who is trying to fit his life works into a housing market with a couple of algebraic equations .I have a computer programme to sell, if you follow my instructions a housewife will earn an additional $20000 for two hours work a week.

Welcome to the complex

The trash can of history is filled with Auckland property bubble predictions. Here comes another one...

Real example. Brother just sold his place last week. CV 700, sold for just over 1 mill. Chinese buyer for his son. Apparently still has another 10 mill to spend.

There's our brighter future right there.

Renting from foreign landlords - the kiwi dream.

The Kiwi dream is so last century. It's a globalist world now and you have to take a global view. Describing those landlords as "foreign" comes mighty close to being hateful under this new paradigm.

Must be our "marxist" education in New Zealand schools.

Absolutely. Marxism is a globalist ideology. We thought we defeated it but it continued its long march through the institutions and has managed to conquer us practically without a shot being fired.

Admit it. You are Jeremy Wells road-testing parodies of mindless burble for future episodes of 'Like Mike'.

Can you refute anything I am writing?

The long march through the institutions:

https://en.wikipedia.org/wiki/The_long_march_through_the_institutions

Refute an extremely weak stub with zero evidence that any of that happened outside the writings of 70s student radicals? Well, if we're going to have a wikipedia-off, you could start with the references from your own stub, which show that it's much more complex and "highly contested" than you pretend.

https://en.wikipedia.org/wiki/Rudi_Dutschke

Even the Socialist Worker, with their obvious bias, writes it off as dead and buried.

The only sources treating it as a real thing are in the business of scaremongering right-wing propaganda, such as WorldNetDaily.

OMG the Marxist conspiracy is in the very soft-furnishings of our homes!

https://www.marxists.org/archive/morris/works/1884/fabrics.htm

Is it time to panic yet????

tl;dr

Are you are a Marxist Kakapo?

No. I'm a Sagittarius.

Have a read of this article, particularly the comments section and tell me it's all rosy out there. Please, I dare you. http://www.ft.com/intl/cms/s/0/020b064c-ecfe-11e5-bb79-2303682345c8.htm…

It's paywalled. Can you give a synopsis or copy and paste? Commenters are notorious whingers as we so often observe here so i wouldn't put too much store in that.

If you register, you get 5 free articles a month and they don't spam! Basically, the Chinese are now laundering their money through cash purchases of foreign business. The commentators stories of doing business with Chinese business also very worrying.

Commentators quote -

Dear FT,

You should be rushing and ringing the town fire bell. Chinese government strategy is simple:

1/. Keep RMB strong, west is distracted - both in Europe and USA. Use the time to move as much money out to China keeping RMB high artificially,

2/. The exchange rate mechanism based on nations underlying economic value is broken. Chinese know that West will not admit mistake and go to gold standards. So fair exchange rate is what China believes West wants - to keep everything unruffled.

3/. Use printing press to buy Western assets with high cash flow. Those cash flows will be used to strip out the value of western assets. In five years China will own 50% of the western assets, purchased by stripping the western assets of their free cash. Chinese banks will then move in to recapitalize those western assets and the game goes on....

Wake up call:

A visit to the offices of one of the largest oil company in Beijing, China, owned by Chinese government, gave some insight. On the top floor were many big rooms with board room style tables, huge chandeliers, thick red carpet and mahogany furniture. Attended meetings for 5 days straight in one of these meeting rooms. But in those five days didn't seen any other meeting being held in any other room. Fancy furniture but lunch was pizza boxes.

Wandered down to the third floor where procurement offices were supposed to be functioning. On the entire floor there were less than half a dozen people. When queried pat came the reply they are visiting other projects.

This government owned oil company executives did all communication using gmail addresses. The project manager kept three mobile phones. How would one be able to trace anybody or anything back? The German company selling them expensive machinery - in tens of millions of dollars - was nervous. It wouldn't accept bank guarantees of Chinese banks. Finally after lot of negotiation the Chinese offered bank guarantee - of BOC and that too issued in a German city - this was acceptable to the Deutsche Bank office.

Sooner or later something will give, last week America's largest coal company warned the market of cash crunch and possible bankruptcy. It is badly affected by falling coal and steel prices.

So with China's domestic consumption of coal already having fallen more than 30%, it is BUYERS BEWARE. Canaries have stopped singing.

wait until the TPPA is signed anybody will be able to buy anything no restrictions OIA becomes redundant

World's happiest countries:

1. Denmark

2. Switzerland

3. Iceland

4. Norway

5. Finland

6. Canada

7. Netherlands

8. New Zealand

9. Australia

10. Sweden

http://www.telegraph.co.uk/travel/galleries/The-worlds-happiest-countri…

I guess you have to pay a lot for a house in the super-city of the world’s eighth happiest country.

The people I see in Auckland each day aren't happy. The look depressed, stressed and tired. They're stuck in traffic worrying about the size of their mortgage, hearing news about a potential bubble that could blow apart the value or their main asset and the economy.

I'm my mind, this isn't happiness.

And that's just Auckland. What about the dairy farmers in the regions? Are they happy right now?

Thats because someone stole their future.

Look, we're all in this together now. There is no ours and theirs.

The future has been determined. It looks something like Brazil or Soweto unless Trump becomes President.

This is so distressing to read. I am in London, but we are planning to return home within the next couple of years. What has happened and what is going to happen?

"This is so distressing to read." Don't take any notice. Auckland is really happy and buzzing. We're all millionaires now.

I suspect Independent_Observer is only happy when he is unhappy (lot of Kiwis like that) and BTW he is one of the people going around making people anxious about the "property bubble".

Z.S. I have read the report. It seems feasible. I trust Phillip's credentials and his experience as an economist. There is a distortion in the market. How many people, who are mortgaged to the max. and in debt, will potentially have their lives ruined if there is a collapse in house prices? I am thinking of fhbs in particular.

Zach - you still don't get this. You're only a millionaire on paper. Sell all your portfolio and I'll say yes you're a millionaire. Well done. But the thing is is that everyone will need to sell at the same time to cash in the gains they've made over the last 10-15 years. What happens if everyone sells at the same time? Well then there is no under supply. There is over supply and the property market crashes. No one is really better off than when the prices inflated dramatically. All we've ended up is with a society in debt up to their eye balls. Its madness. And the problem has been created by people like you. A cancer of NZ society. When did we all become so greedy? When did we stop giving a toss about each other, about our kids and their futures?

Listen, everyone is not going to sell at the same time. What you propose here is preposterous under the current conditions. A mortgage is the same cost as rent but has added benefits.

If everyone sells all their gold at the same time the price of gold will plummet and so on.

Cash in the bank is only money on paper as well you know. AndrewJ says don't trust the banks - where are you going to put your money? Under the mattress?

Fact: Most Aucklanders are not relying on recent capital gains to fund their lifestyles. Most houses have small or no mortgages.

When did we stop giving a toss about each other, about our kids and their futures?

When it became clear they wanted me to look after the entire world's kid's futures and I realised what they asked was impossible.

Gold 'is' money

Gold is not money. Try buying something at the dairy with a sliver of gold.

Remember when silver crashed? Gold can crash too. Gold earns no interest.

KOTOK: Gold Has Just One Of The Three Characteristics Of A Functional Currency

I'll take gold off you, what do need? Remember when the Aussie dollar was $1.08 to the US$. Money in a lot of the world also earns no interest. Gold also is not debt backed like what governments say is legal tender.

If it's not money then why do Central Banks behave like this?

http://www.zerohedge.com/news/2016-03-19/how-venezuela-exported-125-ton…

Gold is absolutely money. Even without the old gold standard many governments are still hoarding gold as a hedge against the huge amount of debt many of these governments are carrying.

Listen to this interview which puts forward the case for gold as an international currency beyond the dangers of mountainous debt and devaluation by QE.

https://app.hedgeye.com/insights/49747-rickards-why-gold-is-going-to-10…

Where do you "goldbugs" keep your gold? I remember back in the eighties when people found out that their gold was just worthless bits of paper.

Also in September 2011 gold was worth 1800 USD an ounce. It is now worth 1255 USD an ounce while property has almost doubled in price in that time. Your gold hasn't even earned interest or provided a home for someone.

Yes but go back over a longer period of time and don't forget to convert it to NZ$ and you will see that since early 2000s it has increased in value about 4 fold. The date you picked was during the last financial crisis when gold had peaked as it was regarded as a safe haven . The idea is to provide a defence in difficult times against devaluing currencies. Indeed there is no income from it but it is better than negative rates of interestif we are approaching another financial crisis might it not spike again and safeguard your savings? The goldbugs as you call them certainly think that is the case. I hold no gold but would use an etf if I wanted to do that.

https://app.hedgeye.com/insights/49747-rickards-why-gold-is-going-to-10…

So if you bought 200K of gold in 2000 it would be worth 800K now? If you bought a two bed B&T unit in my street in 2000 for 200K it would be worth 800K now. But, don't forget, rent. That unit would have earned about 300K in rent making the 200K 1.1 million. But imagine if you used the rent to finance another unit next door. That would have turned your 200K into 1.4 million...and two families would have homes...in a nice street.

@ zachary smith Lol...that says more about the Akl housing mkt than it does about gold .

Akl housing now being suggested as the safe haven of choice in times of world economic turbulence LOL . What next?

I know right? I'm laughing too. But I honestly believe there is a good reason for this occurring. It is because New Zealand is one of a handful of very special societies (Look at those top ten and see the common denominator) and Auckland is its super city. Millions of newly wealthy Indian and Chinese people believe this reality even if you don't.

@ zachary smith

That article was published on 19th April 2013. Anybody who bought gold at that time would have made a fortune in the intervening period to date.

Not if you bought gold in 2011!

What, wait, gold in April 2013 was 1392 USD an ounce. It is now 1255 USD. That's a disaster! Is my information wrong?

Please explain..

http://goldprice.org/gold-price-history.html

You are wrong. You have forgotten to take into account the US$ to NZ$ Rate since 2013. . In NZ$ terms it has risen from NZ$1550 in April 14 to currently fluctuating around NZ $1900.

As a matter of interest I am not a gold bug and hold no gold.

If I wished to physically hold gold it can be physically bought through an etf with ticker SGLN on LSE. The share price equates to 0.02ozs gold. It is a full replication etf and It is physically held for the shareholder

As a matter of interest I am not a gold bug and hold no gold.

Like a beautiful flower that is colorful but has no fragrance, even well spoken words bear no fruit in one who does not put them into practice. - Buddha

So it wasn't that the value of gold increased but that the exchange rate changed that produced a profit?

@ zachary smith

Oops, didn't like my reply then? :-).

Well it didn't seem like it was gold increasing in value that produced the profit so it seemed a little deceptive.

Also, i liked your reply as it afforded me an opportunity to launch my Buddha quote at you in the hope of eliciting a touché.

@ zachary Smith

No deception involved it is all a matter of global economics. I think you would find the following webcast very informative. It requires a little perserverance as it is slow to get started and the economist promotes his book but outside that there is some very interesting and educational stuff.

https://app.hedgeye.com/insights/49747-rickards-why-gold-is-going-to-10…

@ zachary Smith

No deception involved it is all a matter of global economics. I think you would find the following webcast very informative. It requires a little perserverance as it is slow to get started and the economist promotes his book but outside that there is some very interesting and educational stuff.

https://app.hedgeye.com/insights/49747-rickards-why-gold-is-going-to-10…

@ zachary smith You are wrong. You have forgotten to take into account the US$ to NZ$ Rate since 2013. . In NZ$ terms it has risen from NZ$1550 in April 14 to currently fluctuating around NZ $1900.

As a matter of interest I am not a gold bug and hold no gold.

If I wished to physically hold gold it can be physically bought through an etf with ticker SGLN on LSE. The share price equates to 0.02ozs gold. It is a full replication etf and It is physically held for the shareholder

ZS, most dairy owners in our area are of Indian descent, I'm quite sure they would exchange some gold for some bread and milk.

Zachary there are other things to invest in apart from property. Just saying if we keep being selfish and not allow FTB's to eventually gain a home there will be repercussions.

1) We'll either have to export our young or they'll remain at home until their in their late 30's.

2) The birth rate will drop further, as most well educated and professionals couples will choose not to have children, since there's too much pressure on them to keep saving, to be able to afford a home or even the high cost of rent.

3) Retail stores for electrical and home products will start to close, since people will be more inclined to save their money - this is already happen.

4) Quality migrants will start to recognise that New Zealand's larger cities are becoming unaffordable and will therefore look to move else where in the world - This again is already starting to happen, as word gets around via social media. So we'll be just left with the huddled masses to take in.

5) The crime rate will go up due to people feeling discontented with their situation - i.e., Not having a hope in hell of owning their own home!

6) And eventually house prices will drop as we will/are hitting saturation point - People will just will not be able to afford it. And even the wealthy Overseas Investors will hit saturation point, it's happened before in Japan and it's currently happing in China.

The "Its all about me" started years ago and it applies to everything not just property. Greed is rampant in the property market, you as the SELLER have control of who you sell your property too, so true Kiwi's could control the property market but when it comes to money just about everyone will sell to the highest bidder no matter where they are from.

Hi Big Bunny. We moved back to Akl a few years ago and it really is a great place to live. It feels less remote than it used to be, more vibrant despite the usual drawbacks of a popular city - traffic etc. We haven't bought a house and are dismayed at the prices but everything else has been so much better than the UK - the schooling, doing business here, lifestyle, attitude of the people. I actually believe the housing market peaked last year and will get easier over the next 1-2 years but just an opinion and maybe wishful thinking. Good luck to you.

Thanks buzby, much appreciated. I am still worried about what may happen in the future.

One thing I notice,being someone that has spend considerable time in both London and AKL,is that the differential in the "quality of life" between the 2 cities is decreasing all the time. AKL is rapidly losing its charm and people are starting to look elsewhere as a place to bring up their family etc.

We went back to Auckland for a holiday a few years ago and loved it. We did notice the air quality though. I read an article in the NZH from 2011 which stated "The WHO data put Auckland's air quality in the same league as Tokyo's and worse than New York's". Driving in some parts of Auckland feels like driving in London. Also the density of housing - the level of infilling is unbelievable. What happened to the tree filled sections I loved playing in as a kid? The quality of construction of some new builds looks very poor - the house equivalent of a school prefab.and on a tiny section. It seems like everyone wants to cash in on the housing boom, to the detriment of quality of life.

We can do without the swearing thanks. Here's our commenting policy - http://www.interest.co.nz/news/65027/here-are-results-our-commenting-policy-review

Cheers.

Is "get knotted" acceptable?

Cheers.

Yes.

Thanks. I will watch my f's and c's from now on. Regards,

The people I see in Auckland

That's called anecdotal -"Based on casual observations or indications rather than rigorous or scientific analysis".

The reason they don't look happy is because they have reached peak happiness. Apparently after a certain point you don't get any happier. We see this in the phenomenon of rich people not being any happier than someone on the average wage.

Might pay to bounce that idea off your mental health worker this week

A study by Princeton economist Angus Deaton and famed psychologist Daniel Kahneman that analyzed surveys of 450,000 respondents revealed:

The magic income: $75,000 a year. As people earn more money, their day-to-day happiness rises. Until you hit $75,000. After that, it is just more stuff, with no gain in happiness.

SMH, this is too easy....

if it will make them feel any better they should contemplate " i don't have an asset (something that puts money in my pocket) if i think rationally, really its a monstrous liability (something that takes money out of my pocket) its the bank that has the asset as I'm am slaving my life away to make the payments to keep the banks asset going for thirty years"....

did you read the article it was for tourism, and most of the places mentioned are in the south island, nothing to do with Auckland city or its houses.

Here you go then. Much, much more than just tourism and from the UN too.

For your reading pleasure. It's very detailed:

WORLD HAPPINESS REPORT 2016

http://5c28efcb768db11c7204-4ffd2ff276d22135df4d1a53ae141422.r82.cf5.ra…

another Saturday night in your happy city

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11608747

ZS is just Bernard firing off comments to keep this site ticking over. No one could be so pro property as Zach and really exist. Do not respond to Bernard's comments.

No one could be so pro posting as ZS and really have a life don't you mean?

Nonsense, he is a worthy successor to the much-missed ZanyZane, who was also hilarious, and believed in aliens and humans and dinosaurs living together. I won't hear a word against him.

An Interesting question is, why did the alleged bubble (I use 'alleged' because many common taters seem to be casting nasturtiums on the notion that there IS one) start around 2002-3?

The answer is depressingly simple.

The then Labour Gubmint, seized by the age-old conviction that Someone's Gotta Do Something, introduced a guaranteed housing loans scheme for which the chief qualification was:

"Can you fog a mirror?"

This had the effect, happy happy joy joy for sellers, of sliding a floor under house prices at that loan figure, irrespective of condition, age, or location. In Christchurch prior to that time, it was possible to buy small houses in unfashionable suburbs for well under $100K. I know, I got a call one bright Friday from SWMBO to say. 'I've bought one' - $47K IIRC.

Nek minnit, the dopey Gubmint decrees that it will loan $100K in Christchurch. Welcome Home....

Instant result, all house prices in Christchurch start with a 1 and contain six digits.

I think the equivalent in Auckland was $350K.

Universal pricing signal......Oh, and we sold the shack after a little tarting up, for a six digit number starting with 1.

Multiply that by the effect on every 'fibro shack in Ranui' - a delicious phrase I have unabashedly stolen from another common tater, and there you have the Genesis of the Bubble.

Good Intentions by an economically illiterate Gubmint.....

A very basic 'fibro shack in Ranui' starting price is now 650K . 650K is the new 'affordable'. It seems to me that the price is set by the rent. There used to be a correlation between rent and price that worked out at something like 500K house costs $500 a week to rent. It's been like this in Auckland for as long as I can remember but things seem a bit out of whack now. Ponder this typical Ranui listing. CV of 360K but advertised 80% over that.

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

Yet another real estate listing promoted by Zachery Smith. I hope Chaston is charging him for the adverts.

so a typical listing is taking more than 8 months to sell now? that place has been listed july.

Yes you are right. I was in a it of a hurry and didn't check the listing date so it is not so typical. I was just looking for a house that looked typically Ranui and had a price.

Good memory there Waymad, but don't forget the 9/11 2001 Greenspan Plan effect which went global, and the Lord of the Rings effect that followed later here also.

Disappointing headline - it's only a property bubble in terms of the house price-to-rent ratio.

Apparently "...The price-to-rent ratio can fall by house prices falling, by an increase in rents, or by some combination of these two channels. Household incomes ultimately place an upper bound on the amount of income that can be spent on housing costs..."

However renters must be smarter than Yale academics as they have found another approach - increase the number of households per house (just like they do in other big cities) - http://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=115…

there is NO bubble! Auckland prices set to continue climbing. Iran is about to invest over US$8 billion in global property. And with Auckland houses seen as being a sure thing, I'll bet my house, a big chunk of that arrives here!

http://realtywired.com/2016/03/16/iran-to-splash-up-to-8b-on-global-pro…

100k immigrants a year, mostly coming here, prices will be up 30% over the next 18 months..

Auckland property is what it is and the usual market forces have no bearing here! Sucks to be a FHB, but hopefully the full force of the disenfranchised will be brought to bear against the National Party and John Key over the next year... but I somehow doubt it!

After all, he is the kind of PM, most people would like to have a beer over a bbq with!

@ General Hubhub

Do the maths. An $8 billion property investment from Iran is tiny amount when spread worldwide....only 4000 properties globally taking an average of $2mill per property.

Auckland property is going to keep going up while we have low interest rates, high migration, lots of foreign buyers entering the market and while the rest of the world continues to turn to crap with Pollution, weather events (droughts etc), Terrorism and other problems.

Auckland is rated one of the safest and best cities to live in on planet earth. Not sure if many of you on here have traveled around this world much in recent years but New Zealand is heaven compared to so many other countries.

A global recession may halt prices for a while but then there will be an even bigger boom after that. I remember in 2011 people were saying prices were going to go down and look at things now. Globally investors are buying up housing in liveable safe cities as that is becoming one of the next most precious assets for many.

I couldn't have said it better myself. This is exactly right IMHO.

That was around the time of the last election and national were 50/50 to get back in. Next election will be interesting as to what policy's get throughing up

I am in Auckland this week for conference. Heaven? keep telling yourself that guys. Moving to Sydney 7 years ago was the best thing we ever did. Enjoy the winter!

I thought Sydney was awful last time I was there. Too crowded and we have better Chinese food here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.