By Greg Ninness

The Government's KiwiBuild scheme is designed to increase the supply of affordable homes for first home buyers but it may also prove a boon for residential property developers, particularly in the Auckland market.

Developers can tender to have their projects included in the Government's Buying Off The Plans initiative, under which they would undertake to produce a certain number of homes in a development for a maximum specified price, which would then be sold to qualifying first home buyers through the KiwiBuild scheme.

If for any reason the homes could not be sold at the specified price, the Government would guarantee to buy the homes itself at the specified price, or refund the developers the difference between the specified price and the price the homes actually sell for.

Where that happened, it would be the Government rather than the developer that would take the loss.

With that guarantee in hand, developers should also find it easier to raise the money to get their projects off the ground, because their financiers will take comfort from the fact that the ultimate sale of a certain number of units in a project at a certain price is government guaranteed.

The payback for the government is that this should increase the supply of new homes being built at the affordable end of the market where the need is greatest.

But there may be another reason developers would want to get involved in KiwiBuild - a potential lack of interest from property investors.

Until very recently investors have made up a big proportion of the buyers in many new developments, particularly in Auckland.

However much, if not most of that investment activity, whether the investors were based locally or overseas, has been speculative, as buyers chased capital gains rather than rental yields.

And there are increasing signs that capital gains in Auckland have now largely dried up.

The Real Estate Institute of New Zealand's lower quartile selling price between August 2016 and May 2018 has mostly remained within a very tight range between $650,000 and $668,000.

In the last 22 months the lower quartile price has only moved outside that range three times, and even then not by much.

In May this year it was $665,000 which was below where it was in October 2016.

That suggests that In Auckland, the market is going nowhere at the affordable end there's unlikely to have been much in the way of capital gains for nearly two years.

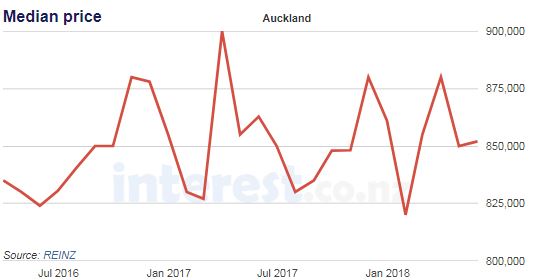

A similar trend is evident in the middle of the market.

The accompanying graph (below) shows the monthly movements in the REINZ's Auckland median price between March 2016 and May 2018.

This shows more volatility than the lower quartile price, but it doesn't show a particular direction either up or down.

If you were to run a line through it to plot a trend you would have to say it was flat at around $850,000, so there's probably not much in the way of capital gains to be had in the middle of the market either.

Which could leave investors that are willing to sign up for new projects being a bit thin on the ground, and that could see more developers turning to KiwiBuild to get their projects up and running.

But should the Government be exposing itself to financial risks by offering guarantees to private developers?

On balance it probably should, because the risks it is taking on with KiwiBuild's Buying Off The Plans scheme are probably less than it would face if it developed the same properties itself.

The Government could acquire land and hire architects and builders to develop a certain number of homes to sell at an affordable price, or it could offer guarantees to private developers to do the same job.

In both cases, the main financial risk is that there could be a downturn in the market between the time construction on the project started and when the homes were completed, which could mean the homes might have to be sold for less than expected, potentially causing a loss.

The risk of that happening is the same regardless of whether the Government developed the homes itself, or engaged with a private developer to do it.

So there is no difference in the potential financial risk to the Government whichever way it goes.

But using a private developer also has an advantage for the Government.

One of the biggest challenges facing property developers is controlling their costs.

If the Government was to develop the homes itself, it would carry all of the risks of a cost blow out.

But if it contracts with a private developer, the developer carries all of that risk, because it is contractually obliged to supply the homes at a certain price, regardless of how well it controls its costs.

So provided the Government is careful to partner with developers who have a good knowledge of the market and a successful track record, there can be substantial advantages for both parties in utilising KiwiBuild's Buying Off The Plans scheme to increase the supply of affordable homes.

132 Comments

Greg, you're going to get a lot of backlash from those with vested interest in keeping the property market/prices afloat..

The pill is too hard to swallow

Seven years ago you opened an account with the moniker “Houses Overpriced”. At that time the median Auckland house was less than $500,000. Seven years later, it’s >70% higher at $850,000. I admire your perseverance, even if seemingly misplaced given that even the COL aren’t promising historic prices.

No, I don't expect them to. At least they are not a catalyst to you specuvultures

Hope you are not including me in that perjorative term, I just have an owner occupied family home. Sucked it up in early 2009 and bought despite the then doom and gloom from B Hickey et al.

Doom and Gloomsters perform an important function in our markets by pushing out demand to sometime further in the future when that demand will either slow the rate of house price decline or increase the rate of house price increase enabling those who purchase now to either have a smaller loss or a larger profit.

"will either slow the rate of house price decline or increase the rate of house price increase"

For you apples and bananas are the same, right

Since you have mentioned it, you don't fall into that category

A well made and relevant point Rex, sadly it is highly unlikely that Houses Overpriced acknowledges your point and much less understands the position. She/he wants house price increases to be unwound not to 2011 but some earlier timeframe. If prices were to be reduced to 2011 prices she/he would still say that houses are overpriced. So it doesn't really matter what the prices are as in another seven years in 2025 Houses Overpriced will hold the same position as he/she does today and as he/she did then. He/she will be very disappointed

Tender is out for a new prefab factory in Auckland

https://www.newshub.co.nz/home/shows/2018/06/kiwibuild-promise-may-rely…

This is the dumbest idea in the history of politics. I'm not sure is this is what voters asked for. We are now underwriting private developers. Some people are going to get very rich. Anyone of thinking of building a new house or major renovation is ffd now. All building capacity will be sucked into this guaranteed money maker for the developers. I still don't understand why or why anybody would want to buy this crap state houses which is what they will become. Seriously FHB are better off renting as there will be no or minimal capital gain on these properties.

Yeah much better that we sit and do nothing, as a FHB myself I’m not particularly interested in capital gains, I’m more interested in not loading myself up with millions of dollars of debt. The dumbest idea in politics was allowing housing to become a speculative market, and not having a DTI which would have prevented people who don’t have the money to pay for a house/multiple houses to leverage.

As the article states, there has been no capital gain for a while in the FHB space anyway. And yes, if you are willing to take the risk of a sharemarket crash, equities are a better place to put your money at the moment. Hell, even govt bonds are, though the return is rubbish, at least it is positive, unlike lower to middle quartile homes in Auckland.

What a terrible world where those putting money up to supply a desperately needed and currently overpriced resource make money from their endeavours. Much better the last few years where money was made by buying existing stock and sitting on it, they're the real heroes.

I’ve seen the HNZ contracts with developers, have you? HNZ is paying below market but the obvious benefit to developer is a little margin (if things go well) and a guaranteed buyer. HNZ specifies everything in the build from floor coverings and tapware to window size and placement. Naturally there are still the requirements for insulation, open spaces etc. They are good houses. The builders are not only bound by their own standards but by HNZ’s H&S and codes of conduct. So the public gets pro builders, safe working sites, and the houses we need - all at a below market price, fixed as at today’s valuations. Risk is on the developer, not least by means of significant sunset penalties.

These PP partnerships are the only viable way to efficiently get this undertaking done.

I agree. It does seem like a good deal for developers to stay in business and ride out the current view of the banks policies, where the banks are no longer willing to lend to developers on the same basis as previously, therefore to survive this market downturn, at least our government can provide some sort of guaranteed albeit lower income/profit to them, but they still remain in business.

Great policy. For those who are critical - name a better one to enable more affordable housing.

There will be positive indirect effects as well as direct effects ie. it will help drop prices of existing housing at the lower end of the market

Land tax.

It's an OK policy but really doesn't deal with the fact that property prices remain a function of how cheap and easy debt is to come by. Land tax does address the fact that land increases in value to absorb any of the productivity gains of society.

No need to introduce more taxes now, as easy credit is no longer easy to get from any bank. They have turned off their debt taps.

This policy is a total muddle. Developers could not get funding from banks as even those banks had realised the market had become so fundamentally unaffordable there was a real risk the development could not be sold at the required price ie the banks as residual risk holder were not prepared to accept the sales risk premium as reflected in the cost of finance. That was a price signal that at current land prices some new developments were basically uneconomic, and development costs (ie land costs) needed to fall to the point where these developments became bankable again. Banks were imposing discipline on developers and the market by refusing to fund developments with unacceptable offtake risk. But under this policy, the govt effectively becomes a market maker for developments which were otherwise uneconomic, it now takes the risk of a shortfall between the development cost and the market price, but it is paid a zero risk premium for that risk. The developer and banks no longer bear sales risk, the govt (ie taxpayers) now bears that risk. So rather than allow price signals from banks to influence the market (ie some developments are uneconomic at current price levels), the govt has instead chosen to underpin current unaffordable prices buy assuming sales risk at a given input price. When (not if) there is a material fall in house prices the govt (not the developers or their banks) will be wearing the shortfall between the development costs and the reduced market price. Why should taxpayers wear that risk? Affordability will not improve until land prices fall, and the govt should not do anything to interfere with that process. This policy doesn’t make these marginal developments “cheaper” or “better”, it merely means that banks and developer no longer need to price one of their key risks, and that risk is now being dumped on taxpayers as muggins of last resort. This scheme makes sense politically, but that the only basis on which it makes sense

Yes. And at the very least, this:

If for any reason the homes could not be sold at the specified price, the Government would guarantee to buy the homes itself at the specified price, or refund the developers the difference between the specified price and the price the homes actually sell for.

needs the refund option deleted. Without thinking too hard I foresee related-party scams whereby homes are "sold" for a low price, the refund claimed, then the homes on-sold for a higher price.

Excellent piece Bobster.

So just mulling – just how rigid is KB pricing – how is it reviewed.

Is there a mechanism for it to respond to a changing market – which I think could well happen?

There are a lot of moving parts to this – can $650k turn into $550k or $750k.

Who, how or what decides this?

I don’t know. Govt will effectively be acting as an intermediate buyer and seller. In a falling market there is the obvious potential for govt to run up big losses due to falls in value between project commencement and completion. I mean, that could be 24 months between the govt commitment to buy and a sale by govt, unless govt intends to sell back to back. It just seems a really fraught process and a role that govt doesn’t seem well suited to perform, all so the govt can say “look at all the houses we have delivered”? The govt should not be touching this market with a barge pole, there are indicators that a correction of some magnitude is on the way. Just let that happen, stay out of the way and keep the fiscal powder dry for when you need it to deal with a possible downturn. If some developers lose their equity, and some unviable projects don’t get built, so be it

Part of my mulling is this.

Let’s assume right now the only problem is supply – and KB attempts to address that supply – and let’s say they are somewhat successful.

So one possible outcome is that the secondary market drops in price – and FHB’s shift some of their focus there.

Does this then ease some of the pricing pressures on KB and the government moves the goal posts – the developers will still have the security of KB etc – but they may have to bend on price, and push back on the land-bankers.

Our will they simply respond to a lower price demand with increasing “rubbish”.

Very simplistic I know – but I wonder in response to a market that could undergo some marked change, which is where I think your heading – what about the elasticity of KB pricing to changing market conditions.

And thus I wonder - who, how or what decides this - 24 months is a long time at the moment in this market.

I'm pretty sure that the government already owned the land and therefore, as land prices are the main reason that house values have soared in Auckland, building on existing land already owned means they are only contracting the price of the build and materials.

With the distinct possibility of a collapse in both land and housing prices in NZ especially in Auckland then surely developers will be reluctant to build. Thus it follows that providing a measure of security to those that can get the job done is necessary. In time our nation will surely benefit.

Eh!? If a market correction is likely, why should taxpayers take sales risk? Let the market correct and the land price bubble deflate, that will do more for affordability than Kiwibuild ever could

And if the national front bench had any gumption (which they don’t) they should be hammering the govt on the “risk to the taxpayer” issue inherent in this proposal. Amy Adams is a waste of space as shadow MoF, I doubt the thought even occurred to her

For every action there is an equal and opposite reaction. .

All the damage done over 9 years, has to be unwound. .

A collapse is only a possibility. Just like a volcanic eruption in Auckland is a possibility.

Not a good reason to not build a lot more housing at lower price points.

Bobster, I tend to agree with your view. What this government will need to do at the front end is ensure that they have in place an effective framework under which they can manage cost vs utility with the necessary sanity checks. Undoubtedly there will be mistakes made, there will be unexpected outcomes and as with any state programme it will always be the middle classes that will pick up the tab. But that is nothing new, by virtue of the fact that they, by sheer demographic are the most populous, that is their function albeit not usually through choice.

To be honest, I doubt govt has anything to add at a procurement level that will produce any greater efficiency over what the large housebulder cos could produce. The days when govt itself had capacity to itself deliver or even actively manage a large housebuilding program are long gone. It can act as client ie set the requirements and pay the bills, but the idea it can itself produce efficiency gains is a bit laughable

Thus far what this government has done is, at least in my view, made a relatively well intentioned and reasonably measured response to what was framed as a national crisis. My thoughts coming into the election were that, all things considered pragmatism and a touch of political expediency would prevail and thus far I’d argue that is exactly was has happened. There were of course a number of other less palatable options open to the coalition but as said before this government does not have a monopoly either of the electorate or of political and economic fortune and acumen hence here we are.

Bobster, again tend to agree.

It is going to be very interesting!

650k 3 bedroom shoebox ghettos squeezed in without any section and they will look like crap.

But that’s ok, we will call it Kiwibuild, because Phil Twyfird has said so

This Ministry of Housing that is going to employ 200 people is also going to be worthwhile isn’t It?

What are these 200 people going to be doing?

This COL is totally lost!

You make it sound like someone will get a palace for 650 at the moment.

As per my first post, people like you must be losing sleep and health, that things are not going to work out as the previous donkey had promised

Houses Overpriced, I have bought 4 bedroom 2 bathroom and 3 living room 8 year old 235m2 home for 477k.

4 bedroom plus 2living separate dining plus a self contained sleepout for 380k.

They are far from our best buys but what I am saying is 650k for a ghetto shoebox is ridiculously high.

Tbh an 8 year-old 4 beds 2 baths and 3 living rooms 235m2 on a land size of 500m2 would fetch around $2,500,000 where I am ^^LOLdgz^^

Compare apples with apples, ..

Were they in Auckland and did you just buy them

TM2, buying quake damaged homes. Best give full picture. It's a minefield down there. Hardly apples vs apples is it? There is only unacceptable risk in real estate when it's all been bought up by cheap and easily obtained credit. There are no bargains.

RP, yes bought 2 As is where is properties.

Both nothing really wrong with them and structurally very sound.

Insurance a formality!

Not a minefield at all, opportunity galore!

TM2, nothing wrong in your opinion. A professional pre-purchase inspection by the next owners will shine a light on their true value. As the Christchurch market slows further, picky buyers will easily give such homes a wide berth, much like they do with monolithic. Expect a buyers market for many years to come.

Rp, you clearly know very little about the ChCh housing market!

Suggest you stick to your Term Deposits and I will stick to making the real money with the ChCh investment market.

It is with attitudes like yours that restricts most people from making serious money and ensures that they need to go to work for many years.

TM2, that was a bit defensive. Was it something I said? A lot of people ripped in their straight after the quakes and spent up on these homes. Such greed. If it comes unstuck for you under the weight of a proper inspection, one struggles to extend any sympathy.

RP, sorry to disappoint you but I do know the property market and the difference from a damaged property and one that’s isn’t!

No such thing as greed when it comes to property.

People are entitled to run a business and that is what we do,

Never worried about any property inspection as we maintain each and every property, and the thing is that we don’t sell our properties as we don’t need to.

Opportunities In every market RP.

TM2, no need for apologies as I'm not disappointed at all. If there is no such thing as greed in any market then why is there fear? Only a greedy self entitled person denies the existence of such as he is the last one to recognise it. I'd say TM2 has never experienced fear in the 1987 sharemarket crash either - right?

Enjoy your evening!

those ignorant also dont realise fear.. which is the case in TM2's case....

The novice house speculator were easy prey for banks (oops sorry - "business partners") who lent the money to buy these quake damaged homes using the family homes as total security. It's nothing more than gambling by one trick ponies.

Rp, the 2 As is where is properties we have only is a small fraction of our total portfolio.

We bought them for less than their land value so I am not sure how it is a gamble??????

When your returns are double figures it is a no brainer really!

TM2, I'll gladly stick with my term deposits and watch those who created this bubble, self destruct along with it.

There has often been talk of having an online database for Landlords to report bad tenants. I think its equally important there is an online database where Landlords are rated by their tenants. Much like AirBNB. A smart Landlord leaves it up to the tenant to rate their success. Novice self entitled Landlords, such as yourself, seek to broadcast their success to the world. To the wise, you are just a byproduct of a cheap property seminar.

BTW, saying two "as is where is" properties forms only a small fraction of your portfolio is as laughable as Eco Birds and Yvils comments that their Bank Managers are their "business partners" - lol!

Get a grip on reality. Another example of more puff than real blow is DGZ below. He is leveraged on two rentals up to his eyeballs!

Certainly not a novice landlord at all RP.

Not a biproduct of any property seminars, although there are many landlords that are!

Once again you keep your term deposits and we will keep our large property portfolio that works for us!

Borrowing Capacity became worse for investors who are ''Asset Rich and Cash Poor'' in June 2017 when the banks decided to tighten their servicing calculation.

People are unable to get 10 - 11 times their income in lending like they used to... or can they? https://www.youtube.com/watch?v=9IqIAfCtmA0

^^LOLdgz^^ yes I agree with you wholeheartedly TM2 ;-)

DGZ, of course you do :) It's easy having a common enemy whos got themselves financially sorted in ways you wish you could.

you seek comfort amongst the delusional

Insurance is a formality until the house burns down.

It's not a brick and tile house then?

Exactly my point HO, Auckland is horrendously unattractive for owning property, but people just keep,on moaning about it!

It isn’t going to change, and if you are hoping that this so-called KiwiBuild is going to help then you are sadly going to be disappointed.

Last property We paid 137k for and returning 380k per week, 3 double bedrooms.

Didn’t have insurance on it but we have spent 20k on it and very solid and very liveable, fully insulated, double glazed etc.

Good night. Hard to reason with someone like you

Actually KB has the potential to change the lower end of the Auckland market a lot. Why would a FHB pay 700 for a crappy 2 bedroom flat when they could but a new 2 bedroom townhouse for 600k?

It's going to pull the lower end of the market down.

Fritz, the thing is though that the size that these 600k box’s are going to be!

They will be smaller than a so-called crappy 2bedroom flat and they will be so close to each other with no land at all.

Mr Twyford continues to change his mind on things weekly and is so under pressure and he continues to have egg on his face from the things that he says.

TM2 – in some respect – size be damned.

A lot of overpriced crappy 2 bedroom hovels are damp, cold and unhealthy – I really do believe it’s a disgrace.

And for the money you’re paying for this second hand rubbish – my God, what mad policy ideology allowed and, encouraged this to happen.

Have a few 2 bedroom flats/ apartments that are fully insulated and warm and solid.

These are very easy to rent as they suit a variety of renters.

Bought them very well and so provide excellent returns.

Good to hear - I'm referring more to the Auckland scallywags.

No, the new KB townhouses are likely to be at least as big as a crappy brick and tile flat. And likely to have at least a courtyard.

But they will be new and warm - and cheaper. Hence they will bring the market down.

This is going to be the most successful housing policy seen in the last 20 years.

They won't be leaky houses either. The governement will be steering well clear of having to deal with this again,

I think you’re right Fritz – this may well dent the secondary market – and something certainly overdue.

Quality secondary product will still price well – but junk and rubbish will again be priced accordingly.

And that will not be a bad thing.

“650k for a ghetto shoe-box is ridiculously high”

TM2 - I quite agree – unfortunately we were equally subject to nine years of what I will generously call “ridiculous” policies and lax oversight– regrettably Auckland was particularly hard hit.

However, once the horrific train wreck is cleaned up, one would like think that in a general sense Auckland house prices in greenfield developments should resemble those of Christchurch.

And until that happens – something is clearly wrong and needs to be addressed.

Another one sold yesterday in DGZ: 15 Ridings Rd.

CV $4,150,000

Sold $5,475,000 (a whopping 32% over CV)

The vendor paid $730,000 for it in 1999. ^^LOLdgz^^

https://www.uprealestate.co.nz/UPR14497

Another one sold on 20/06 in DGZ: 36 Bell Rd.

CV $3,150,000

Sold $2,885,000 (8.4% under CV)

The vendor paid $545,000 for it in 1993.

"Buyers could disregard the CV listing says" ^^LOLdgz^^

https://www.uprealestate.co.nz/UPR14468

Haha ... I am a bit confused now...

Is Greg a reporter with Interest.co.nz or has he became the official spokesperson for MBIE and the photogenic RH PT? .... or is he just brainstorming and sharing his opinion with ( and quoting) himself in an article to all readers?.... or is he advising the Gov on what to do and how to do it with a pack of delusional assumption from which he draws his own conclusions ?

Many here accuse those of us who are landlords and property investors of barking loud at the wrong tree trying to talk property prices up ?... lol, so what are the DGMs doing? ... they are talking the market down nonstop, and picking their numbers to suit and dishing out free advice to FHB while slinging mud at the "foolish" landlords !

I will ask this again, why are DGMs so nervous and worried about Investors and what they might lose etc... let them burn, dont worry !!....

I find the argument that CG is gone and the yields are poor so every landlord will be stupid to buy or an idiot to stay in such a market and keep making loses blah blah, and they are going to be hit hard when the tide goes down, and down it will when the bills will be passed .. blah ..blah ...

Greg's analysis today and hypothesis actions of what the COLs can / should or not do is chewing the old piece of fat everyday and repeating delusional dreams to pump up spirits and drum up hopes ( in my view : mislead people just like BH used to do in 2010) .

The public purse is not open for this CoLs to use for its own self serving political end or to cover their failed big mouth promises in the name of helping people get into homes - There will be a hefty price to pay for that kind of theft !! ...their Hypocrisy was well shown to us in the way they are dealing with homelessness and child poverty !

Hypnotising people with numbing articles, opinion pieces and selective Data and comments here or there can only last so long - the truth will be what they will face when they wake up and despise all the fortune tellers who lied to them .

People who have some knowledge of the building industry and have ears to the ground know that the KB shoe boxes project is going to be a disaster ... simply because they are building the wrong product ! - Time will show the amount of Gov losses and write offs when the first 100 homes are sold ... and I would challenge all reporters to keep a tab on that and let us know what happened in $$s and ccs.

FHB will not buy 60M2 for 600K or ~100m2 apartment for 650K - As I said before I have 8 FHBs around me in the family and when KB is mentioned they all laugh in disgust .... these apartments are available on the market now and not exactly being sold out fast. Who will commit to a shoe box home that will cost him about 3-4K pa extra to run not to mention all the Body Corp rules and all the restrictions which come with it.

Raising people's hopes by spinning the obvious and kicking the can down the road is nothing new , however, it has always ended up in tears as lying cannot last forever and deceived people will eventually wake up to the fact that they have been taken for a ride.

You're absolutely right, people realise they've been taken for a ride for 9 long years

The 8 members of your family laugh in disgust.. they have your dna, can we expect any better from them

Keep fighting hard to keep the ponzi going.. your days are numbered

Eco bird, whats your take on what’s happening in Australia? Sydney is at 10x income, Melbourne at 8x (Auckland is 8x or so). Household debt is about 200% income (we are 170%). The banks and regulators have recognised that mortgage lending has not necessarily all been prudent lending (that is somewhat understated). So the banks have clamped down on lending, particularly interest only and high multiple lending. And this credit reduction has caused prices to fall. We don’t know how far they will fall.

Do you think there are any lessons for us in what’s happening over there? Or is this just something that happens to other people? Even though our overall levels of household debt and price to income levels are broadly similar, and their banks are also our banks, do you think this credit crunch will be solely an Australian phenomenon?

Auckland is 11x. .

I have made it clear many time before, I do not and cannot compare the NZ housing market to others - there are lots of differences on both macro and micro levels and I am not privy to all these details and drivrs.

I know my market and our fundamentals and drivers.

When someone needs a home or investment, he/She will not gives a toss to credit crunch, household debt, and all the rest of the fancy vocabulary.

They Go and look for a property within their budget and Ask a bank to lend them money to buy. Whether that is 8x, 9x, or 12x that is an issue between them and the Lender because everyone if different and the lender will decide if they can service the loan. History is full of examples and dates ...2004, 2009-2011 etc.

RBNZ , and I suppose RBA, are so far satisfied that their banks are solvent and have passed few stress tests to make sure they will stay that way - the banks are not going to shut shop because there is a credit crunch ... and Who are we to judge or second guess the RBNZ?

I have a young family member in Sydney who is looking to buy something to settle down there - He is complaining that the market is red hot and prices are exhaubernt compared to Auckland ...Prices are Not falling according to him, maybe he is looking in posh suburbs .. but people are buying ..I don't know who and how but life goes on ...

I guess it is wise to stop predicting what will or not happen depending on our intolerance of the numbers you mentioned above - we don't know, maybe 9x will become the new normal regardless if you think that some people will never be able to afford it and that wages are not catching up with house prices , what's New there ?- We won't know , until late, how long will inflation remain this low in NZ, and so will interest rates ?

it amazes me when I anecdotally hear about 25 - 30m2 apartments in Japan, but does that shock the Japanese? or someone would be thankful to be able to afford even that? ...Hong Kong's prices were unbelievable 15 years ago, they still are, does that shock them at all now? Not at all .. moreover, have they stopped building and selling ? NO ...did the markets over there Crashed? NO, well maybe corrected at some stage but they are all up to unimaginable numbers - even in China !!.

So, I have no answer to your formula and I never bother counting other people's chooks... there will always be a correction when markets get out of control, but we tend to forget that house prices are Not referenced to average wage or benchmarked to the lower quartile of earners.

Apparently these represent less than 30% of total house buyers and they can only afford a certain price category ... so not an overwhelming power to turn tides - there will always be stock for these buyers and that stock gets cheaper with time ( small, old and do ups , apartments etc) just the natural evolution in housing and you note that in the interest.co.nz affordability report things are getting better.

People used to start in a 2 bdrm unit and a carport in the past and 3 bdrm 90m2 when they are have a family , folks used to squeeze themselves in what was available and mansions were few and far in between ... today, people like space to spread ...100m2 is tiny, 160m2 is small, 200m2 is adequate, 250m2 is comfy, and 350+m2 is luxury. Obviously Prices follow the trend.

Given all the above, will the market crash in AUS, or in NZ .. No, I don't think so - Are we losing some of our quality of life and things we used to take for granted , Yep we sure are !

Will this squeeze continue ? ..I think it will, with few venting sessions every now and then to relieve pressure (a recession perhaps) This is how cycles worked so far ( the devil is in the detail) and I do not see any reason why it will not continue in future.

Did I expect that my house would quadruple in price in 18 years, No I didn't, but it did ! -- everyone in my neighbourhood who bought or built at the peak of the Y2K crisis has done well ... will these houses double again in 10 years? ..lol, I believe they will, but you are welcome to disagree ...

Eco Bird - "I do not and cannot compare the NZ housing market to others as hint's of a bust gives me night terrors. Solace is in my denial. I will continue to sleep under the same "One Roof" as my beloved "business partners" till financial bust do us part"

Those who fail to learn the lessons from history are doomed to repeat them.

This is partly why property market price cycles occur - those market participants who recently entered into the market and have never experienced a large downward price cycle, who are highly leveraged and have chosen not to study sufficient history to learn the lessons subsequently then repeat them. They may not even understand the lessons of history - after all, only a very small proportion of the population of the country have ever heard of, or understand the term "credit bubble". To fully understand that term requires a high level of understanding of macro-economics. Many people who are caught up in asset price bubbles don't know they're in an asset price bubble until after the fact - look at past asset price bubbles.

Property market cycles are long term in nature - the last property market price crash in New Zealand was in the late 1980's and early 1990's in commercial real estate. A book has been written by Olly Newland about that experience. Many of today's highly leveraged property investors were not around then, or were too young to know what was going on in the property market firsthand.

The result of large financial gains in the market by many highly leveraged property owners in this property price cycle, results in a high level of confidence and many people will only learn through personal experience firsthand rather than learning vicariously. The problem with learning through firsthand experience is the financial loss and pain, emotional and psychological misery it can cause to the individual and other family members, not to mention the loss of time required for recovery. Some people never recover. I recall a story of an individual who lost all their wealth (and more as they were highly leveraged) in the 1987 stock market crash, and as a result, they committed suicide, leaving the surviving family members in financial and even more emotional and psychological turmoil as a result of the loss of their loved family member.

All that is a preaching of someone who has missed the boat by the looks of it and trying to cling to any excuse to feel better.

History does not lie, the facts that careless people have lost their easy gamble money along with their shirts means nothing to the rest who didn't.

People who bought property anytime since then are counting their blessings - apparently you are not, and still busy reading macro economics.

Funny that you quote Olly Newland , very selective reading I see... lol ... Olly is one of the wealthiest landlords who made his fortune from property over the last 40+ years and he now advises people on property investment !!

It is meant to be merely an explanation of why there are market price cycles and how they can go to extremes for those who are unfamilar with market price cycles and interested in such matters.

After all, why have investors in financial markets repeated the same mistakes from previous financial market bubbles and subsequent crashes such as the Dutch tulip bubble and the South Sea bubble, the panics of 1825 and 1907, the crash of 1929, the nifty fifty price bubble, the 1987 stock market crash, the Tequila crisis, the Asian Financial Crisis, the internet bubble of early 2000's, and the global financial crisis of 2007/ 2008?

You essentially get a different group and / or a new generation of market participants, who have never experienced a price crash - a different group of people from those who went through the firsthand experience of a price crash and potentially psychologically traumatised for life - there were stories of families who experienced the 1929 stock market crash staying away from the stock market for the rest of their lives, and similar stories of individuals who experienced the 1987 stock market crash having stayed away from investing in the stock market due to that experience..

Hence a new generation of market participants, are free to learn those financial lessons firsthand again. You do get a small proportion of the population who learn vicariously about financial market crashes - they are typically in some university courses on investing, but for most professional market participants it is "on the job" training. Also many retail investors do not get formal training on investments. It is interesting that does not happen in fields of science such as medicine - the knowledge learnt previously is passed on vicariously and improvements are built on past knowledge discoveries - imagine if medical scientists had to relearn the knowledge firsthand each time before they could make scientific improvements - scientific progress would be very very slow. Then again, in the field of medical science, amateurs would be not be in this field - compare that to investing in financial markets, and property markets where investment newbies and inexperienced people are constantly entering the field.

It is interesting to see investors in the Auckland property market choosing to ignore, or consider irrelevant, the recent house price crashes in other countries from the GFC, such as Ireland, the US, and Spain as well as other significant property price corrections in Toronto in the late 1980's, Sweden in the 1990's, Norway in the 1990's, Finland in the 1980's, Japan in the 1990's, Hong Kong in late 1990's, and Singapore in the late 1990's.

One reason cited by property investors is that they don't understand the property market dynamics of those overseas markets in order to make a comparison to the local market. Another reason cited by property investors is that the circumstances in those other markets are different to the property market fundamentals in New Zealand - frequently citing different property demand and supply dynamics - such as population growth, immigration, foreign investment by non residents, different economic sector dynamics, different building regulations, different construction approval procedures, different availability of land, different cost of land, different costs of development, different costs of construction, different local government and central government policies on housing, different macro-prudential measures imposed by the central bank such as LVR limits, debt to income ratios, different lending criteria and loan underwriting standards by banks, etc.

Perhaps, this time is different …

Only for those who understand macro-economics - http://www.nber.org/papers/w13882

Why on earth do people think that We were taken for a ride for 9years?

Thing is that we are going to need immigrants from the right countries because there are many that are not going to put up with nillness of this COL and are leaving!

The reason you don't understand is that you have your head stuck in the mud..

“Why on earth do people think that we were taken for a ride for 9years?”

TM2 – I’d never expect you to leave your beloved Christchurch, and I respect that.

However – if you were in my shoes – having being born and raised in Auckland – and subsequently experienced what has happened – you too might become a bit annoyed.

But don’t take my word for it - come up and stay for a few months – soak up the success of the last 9 years – you might be surprised at what this so called success looks and feels like.

Auckland is a fantastic vibrant city hence large numbers of people want to live there and houses are expensive. Christchurch is a cold hole with next to nothing going for it hence it has a very small population and extremely cheap housing. Anyone could be a landlord there. The Boy could not foot it in Auckland as there are no “ as is where is “ properties there.

Gordon, you are a jealous and angry man!

Suggest you get a hobby!

Gordon does raise a valid point about your hyperventilating over a portfolio of "AIWI" properties. Hardly a portfolio worthy of envy. You're only one skilled property inspection away from it all unravelling if you have to divest for liquidity purposes. It's not a position I would want to find myself in that's for sure.

You've also labeled me bitter, twisted, angry and even hobbyless so, just to clarify, I have several well funded hobbies and lead a peaceful and relatively hassle free existence. After decades of long hours and financial sacrifices, I believe I have earned the right to enjoy living my life, rid of what was at times, a daily grind.

Given the current risk ridden environment globally, I value having chosen term deposits as my source of income. I wasn't always into term deposits. Up till early 2015, I invested in a mixture of shares and high yielding corporate bonds through several managed funds. Knowing I had enjoyed one hell of a good run, I just knew when to call it a day. Investment property is not so easy to divest from and besides, homes are for living in, not speculating on.

RP awe have a portfolio of rental properties in which our As is where is properties comprise approx 5% of it.

The properties were bought at less than the section value so hardly a risk to seasoned investors!!!

The Boy you are being ridiculous as always. I live in a city far warmer, far more vibrant and relevant than your poor town. Why would I be jealous of you and your pathetic as is where is shacks. The values in my city are higher than yours as people actually want to live here. You are actually the angriest person on this site especially since Labour took power. Phil told us this morning the first Kiwibuild homes will be finished in September. Remember they only had to build one to beat Nationals record. You are lucky they don’t have to build them in Christchurch as that would really accelerate your dropping house values and rents. Go put some more wood on the fire and put a rug on your lap and loosen up a bit.

Oh oh. .you have now upset the boy. . You used the KB word in good zest

Gordon, don’t give a rats if you live in a warmer city, with more traffic, more unaffordable housing, more crime etc.

We make an excellent living from safe and profitable investment in housing.

We go to bed when we want and rise when we want. We travel whenever we feel the urge.

Our financial position is extremely sound and our Business Bank Manager states that we are by far his safest borrowing customer, somthat says something doesn’t it?

Not angry at all regarding the COL but annoyed that sommany are blindfolded by the nillness of them.

The change in rental rules by this COL will not affect us one iota.

As for the KiwiBuild homes, it is a. Total non event and to say that the first ones will be finished in September is a cop out. They were devised by the previous Government and watch this space as Twyford goes from one disaster to the next.

Have a great day, as I am and always do in Chch, the city of opportunity!!!

Ooh anger boy anger. .. pressure climbing. .. heart thumping. . Oh no..

Check the spelling mistakes. .. take long deep breath. . And say aloud. .

Kiwibuild is great. . Kiwibuild is great. . Kiwibuild is great. . Kiwibuild is great. . Kiwibuild is great. .

Now you will feel better

Take a sip of your medicine and repeat. .

Kiwibuild is great. . Kiwibuild is great. . Kiwibuild is great. .

Nillness. Does that word exist ? I can see why you are a real estate agent. Just another old boomer who thinks he is shit hot because he was born after the war and could buy a few as is where is shacks in poor old Christchurch when they were cheap to buy as there was no competition for them. Now angry as values and rents drop steadily but surely. And guess what it is Labour’s fault so really angry they are in power. He needs to get used to it and to changes coming in property laws that will decrease the value of his crappy portfolio even more. Diversify diversify diversify.

He's hyperventilating. . Don't aggravate him any further. . He might pop

Gordon, once again, not an agent now at all.

Not an old Boomer either!

Rents and values holding up extremely well!

Gordon very envious? Yes.

Not a crappy portfolio at all Gordon!

Go on Gordon, take up my challenge to you!

no that’s right, you are full of BS, and you know it!

Not worth discussing anything with most on here as they are just doom and gloom and will never be financial due to their outlook on life.

Leave you to it, can’t be bothered with negative people who are jealous of successful people.

I know you will respond with more BS but that is what you are all about Gordon!

Go on take me up on my challenge to you?

I know you won’t because you are scared of meeting anything head on aren’t you?

Or will you? No you won’t!

You name the amount Gordon, make it worthwhile for the 3of us!!!!!

Hi THE MAN 2

You are correct: there are a large number of doom and gloom merchants here......

They never become rich - and nobody ever becomes rich listening to them.

TTP

We would rather be what we are, than have pests like you'll amongst us..

Hi The Thickest Person, where have you been..

Searching for a RE agent to get rid of your rotten boxes?

The Boy once an agent always an agent. You show absolutely no empathy for those less fortunate than you and those who are younger than you starting off. In fact you are nearly as unempathetic as DGZ/Zach and that is saying something. What they talk about is totally irrelevant to 99.99 per cent of New Zealanders but at least you talk about houses at the very low end of New Zealand values as you are in poor old Christchurch. This site would be better off Without both of you as you do not care about your fellow man.

Whoever set the bar for affordable at 600k was grossly uninformed about the wages in this country. Even 300k was a tough ask 5 years ago for people and if they had been trying to save all this time they would be further from obtaining a home now then they were back then.

Australia upcoming fire sales !https://www.youtube.com/watch?v=6-8c5tH_9Qw

Great post! As an ex-banker, I have been closely following the Australian Royal Banking Commission and their court antics. I can vouch for the fact that bankers are excellent sales agents and we targeted our existing customers for other financial products through creating fear (we call it FOMO) today. Every single person that came into our branch was a (potential sales target). Bank staff got paid 5-10% of their annual salary paid on top if they hit their sales targets, set by the regional sales managers. We were no different to used car salesmen and we had great oversea's holidays based on our performance. If you couldn't meet the sales targets, you were "managed out". Today, nothing has changed. Bank staff are still well equipped to sniff out a potential target to increase the banks profitability. Property Investors were the easiest to target with the perception that they were the least amount of risk. But today, these same property investors might actually be the biggest risk, especially when they have signed contracts for the first five years on interest only terms. These investors started appearing in 2012 and some of them are now being faced with the end of their interest only terms and now their loan contracts include a catchup of "deferred interest payments" of the last five years. Essentially this now means in some cases an increase of loan repayments designed to ensure that the original loan will still be repaid in full by the end of maturity, therefore loan repayments in many cases need to increase 30-40% to ensure that the bank still receives all of the debt before the term loan end date is reached. We sold you a "Liability" but on our books it is "OUR ASSET" and you should never forget that.

Auckland, in Australia, with the AU$360 Billion in pending interest only mortgages reverting to principle in the next 2-3 years, there's considerable downside potential in prices. Concerns have also being raised about how it's now much harder to refinance one's way out of trouble due to more bank scrutiny.

Plenty of interest only loans are due to revert to P&I here in NZ so watch this space.

Meanwhile back in Auckland, a Ponsonby villa was passed in after only one vendor bid placed @ 2.6m, CV 2.8m. https://www.stuff.co.nz/life-style/homed/latest/104827812/family-sellin…

Granted that the family are in no hurry to sell. There was once a time it would have fetched 30% over CV based on capital gain/development potential. Things have certainly changed.

They were not happy with 2.6m. Holly crap. What has the world come to

Eh? article says CV of 2.6mil, and one VENDOR bid of 2.4mil. So really no bids. Maybe having Rod Duke as a neighbour put the buyers off?

Pragmatist, thanks for pointing out my error :-) True, no bids indeed.

This place would have been unlikely to ever get 30% over 2017 RV. Maybe 2014 RV of 1.750M. The thing is it is a do up. This means you can knock a couple of hundred grand off right away.

They should offer the house to the NZ Fire Service as a free fire training drill and let them burn it to the ground. No expense in demolishing it then and the land price would easily increase once they shovel out the remains on a wheelbarrow.

Thank goodness it's not in DGZ *phew*

I recently went to couple of DGZ property auctions, one passed in at near CV at Mt Eden, another Mt Eden sold at CV. Both houses were bought about 5 years ago and both funnily were $1m over what the vendors paid 5 years ago (homes.co.nz). I think you are pretty safe in DGZ mate. I'm still roaming hoping to pick a bargain. Haha

I read the state housing planned in Herald today and some are in same development as Kiwibuild. I'm not sure why FHBs will want to live next to loads of state houses. Now the CoL has dropped P testing, I can't imagine buying a shoebox in this kind of areas.

Yeah man it's location location location. Did you see my posts yesterday on the sold prices for 15 Ridings Rd and 36 Bell Rd?

I see one house in Glenfield in the auction results page that sold for 880k in March yet sold last week at auction for 840K. It sold for 390k in 2007 so 800k is around about its value.

Still, first sort of distressed sale I have seen in the pages.

No sorry I didn't. What they sell for

As above...15 Ridings Rd.

CV $4,150,000 Sold $5,475,000 (a whopping 32% over CV)

I think a government backed developer bought it. New kiwibuild housing coming to your neighbourhood soon.

Gordon, I am very supportive of people that want to get ahead in life.

No I may not be empathetic to people that do nothing at all to improve themselves, and rely on NZ for their lifestyle, and I see a lot of that!

It has got nothing at all to do with when you are born, it is to do with attitude and willingness to learn and work.

Gordon I know you will reply, but in your reply once and for all, are you up for my challenge to you, as you never answer my challenge!!!!

So what about the many people that work very hard in key roles in society who simply can’t afford the silly bubble prices?

In your view, is that just ‘too bad’ - the ‘law of the jungle’?

I would think most people would want to get ahead – it’s just that for a variety of reasons some don’t – but you can’t simply ignore them.

We should also be careful about enabling a ”working poor” environment – it’s not something that we really want.

The US is a rather good (or should that be bad) example of what happens when the market rules and any repercussions, good or bad, are left to sort themselves out

At the extreme – do you really want to live trapped in a gated community – nervous about stopping at a red light in a dodgy neighbourhood and enjoying all the other thrills and spills of a have / have not society?

NZ is better than that – historically I think we’ve done “empathetic” reasonably well – and as a society I think we have been better for it.

If people work hard then they can afford to buy in Auckland!

No it won’t be their dream home, but progressing up the property ladder to your so-called dream home is about taking steps.

We bought our first home prior to marriage, did it up and sold it. Made money and bought again, and sold that and made money.

Have renovated many houses and worked a job and then renovated after work till,early hours in the morning.

Always made good money and always had goals to focus on.

We had several children and my wife never took any time off from working and we worked as a team.

Nowadays most of the generation live for today and aren’t prepared to work additional jobs or be prepared to take chances.

We were self taught so Gordon don’t damn well tell me that we were lucky to be born when we were!!!

It comes from being prepared to better our financial position and now we have a net property portfolio worth many millions and it did not get given to us, it came from hard work!

Sit on your butt and do nothing and that’s is what you will get!!!

You are the Man. That's exactly what I did too. Even 15 to 20 years ago Auckland was affordable as my income was a lot lower and same for the wife. There were times when we got under real interest stress especially when she had the babies. Had we not bought a house, we would be 10 times worse today. People don't realise how hard you have to work to get the dream life. Unless your daddy is rich, you have to make the money yourself. Regardless of what people say here, my advice has always been to buy in good locations and they will go up as Auckland gets more people. There is tons of jobs out there and more people are still needed. The good location suburbs are always desirable and move up in price

If you are telling the truth The Boy which I doubt you could not do the same today as you are uneducated and would not have the income to get the loans. It would be even more impossible in good areas such as Auckland. You are a lucky old boomer like myself if what you say is true. As said previously anyone can do what you say you have done as values are so low down there are in such a small town. Just imagine what you could have achieved if you had the ability and income to live in Auckland. You would be in the rich list . After all you are so obviously in love with money. Do you have a hobby. Do you think of anything other than making money. Have you ever done any voluntary work for anyone or a club? Those who shout loudest are often not telling the truth. The pathetic name you use on this site speaks volumes.

Gordon, if you don’t think I am telling the truth, then take me up on my challenge to you!!!

If you won’t then do not call me a liar, as I am not!!

As for being uneducated, you haven’t got a clue!

I am not an old Baby Boomer either, what age would YOU call a boomer?

Don’t care if I was on the Rich List or not, that doesn’t worry me at all. What is important to us is that we have the financial freedom to do what we want when we want and all thru our own work ethics.

Have set ourselves and our children up financially for life now and that is reward enough for us.

You might think you are Father Theresa with your writings for people with little finances, however you would be far better offering them your financial genius in regards to your large share holdings Gordon.

Challenge still on offer, but we all,know now that you have not got the guts to take it up, because you know you will lose!!!

All you do is talk about money and how much you have got. Have you ever done anything for anyone without counting the cost? Do you do any voluntary work? I have my doubts. Have a go at looking up “ boomer” on google. Or get someone to show you how to do it. It is spelt b o o m e r.

Gordon, it is a site designed to help people make financial decisions!

That is what the property investors on here try to do, by giving their advice on what people can do.

What this site does not need is doom and gloom merchants talking about things that they don’t know about!

That is not helping anyone to make financial decisions!

The advice that many have given negatively about property investment has cost people a helluva lot of money!

The people who I would take notice of are the people who have been financially successful rather than People who are moaning and groaning about not being able to get on the property ladder.

It is still possible to buy a home in NZ , as I have said it won’t be your dream home but if you want something bad enough then make it happen.

Do nothing and you will end up with nothing and that is what I see all the time from people,that talk the talk, but never walk the walk!

No, you guys are not helping people make financial decisions, but working your butts off to keep the housing ponzi afloat..

So what are you saying? Do you want to see the housing market crash and economy in recession and people jumping off the buildings before you're happy HO? Wake up!

DGzzzzzzzz, it's comic you telling a wise man to wake up - ha-ha-ha:)!

That's your interpretation of our comment....

Wake up dude from your delusional dream

He’s I have helped a helluva lot of people,improve their financial position, but only the ones that want to.

I have been a cub and scout leader if that is voluntary work.

Haven’t helped out at a soup kitchen yet though Gordon.

Chessmaster, there are many on this site that just expect everything to just fall into their lap.

Reality is that there will a,ways be people that make good decisions and others that make poor decisions or even none at all.

From being a landlord with more properties than we actually need, we see so many people that come and view our properties.

Many have 3 or 4 kids and Many have stories that they tell us, including of woe!

Many ask what the bond amount is and they faces go expressionless, and you can tell that they will be stretched getting the bond.

If they haven’t got the bond you know that you are generally going to,have trouble with them at some stage so we don’t bother.

We do give people chances but we generally cover our butts.

I didn’t tell these people to have 3 or 4 kids so that they will never be able to save enough money for a deposit on a house.

We have worked hard to get where we have by working after work for many many years and weekends when others are at the pub.

I get annoyed at the ones on here that blame others for where they are currently financially!

It is all to do,with the decisions you make.

If you want to get ahead today it takes 2 incomes generally, and if you aren’t both prepared to bring in income then damn well stop your moaning!!!

TM2, you do say the darndest, self describing things. Yes, there are many here who expect endless capital gains to fall into their laps! The age of self entitlement has led us to where we are today. Now, the glory is slowly fading away. It's what happens next that will truly test the "intelligence" of the self entitled.

Reality is that there will a,ways be people that make good decisions and others that make poor decisions or even none at all.

I wish I made the good decision to be born to working parents to working parents with steady jobs at a time that houses were really cheap.

Come off it dude, admit you just had a lot of luck. I mean you write like a 10 year old, do you really think your own talent was the contributing factor for you?

So many of the property spruikers on this site who think they are clever seem to have forgotten the simple fact that in some parts of New Zealand people are paying ten plus times income to buy their first homes. Some of the aforementioned who think they are pretty special probably bought their first home at three to four times income. Even with the difference in interest rates it was a lot easier. Us boomers are certainly the lucky generation.

EXACTLY!! I'm not even a boomer, I'm Gen X, but my first house cost $112k and we negotiated it down from their asking price of $122k. At that time interest rates on our loan were 14.75% and about 3 times our double income as far as DTI limits allowed. I was 21 at the time. My life definately translated into the meaning of "mortgage", which is derived from "The roots are mort (death) and gage (pledge)". But we also had secure jobs, were young and our income was rising rapidly each year due to inflation, which helped reduce the debt very quickly. Today, we have a very different economic environment. Today, one cannot expect our wages to increase so dramatically as to reduce our debt burden, so 30 years of housing debt is a very long position which may end up being re-priced over a longer period if our banks start to fail.

It does introduce an incentive for the government to sort out the tangled web of regulation that makes affordable house building in this country quite impossible. So, there is probably some merit in the idea, certainly worth a trial. It does appear to change the incentives in a meaningful way, which is what is required. Make development more profitable and development will come. Yes, I know it's messy, but trial and error beats pontification into a cocked hat.

Having said that, these supply issues are but secondary causes, the primary one being that the private sector has reached or exceeded maximum debt carrying capacity, which only the leaves national and local government to take on the required extra debt. All inflamed by the country's lunatic immigration and foreign investment policies which continually add petrol, tyres and sofas to the bonfire.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.