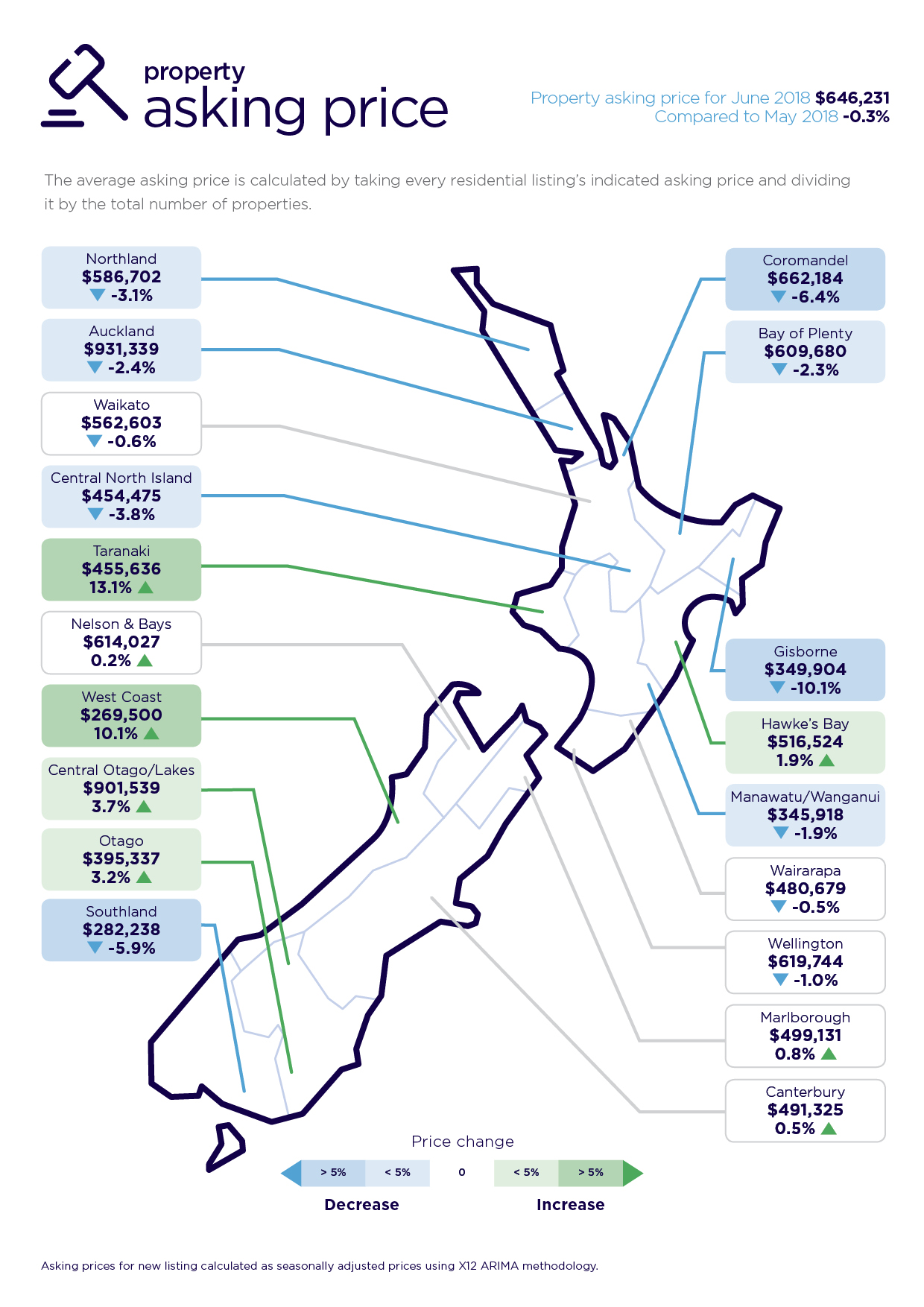

The housing market is cooling with average asking prices and the number of new listings on Realestate.co.nz taking a tumble in June.

The average asking price of all properties from throughout the country that were newly listed on the property website last month was $645,133, compared to $658,170 in May and $661,129 in April.

The national average asking price is now down 4.2% compared to its February peak of $673,659.

Average asking prices in June were down compared to May in most parts of the country, with just four regions, Waikato, Taranaki, Central Otago/Lakes and Otago posting gains and asking prices declining everywhere else.

In Auckland the average asking price declined for the fourth consecutive month to $912,071 and has now lost more than $82,000 (-8.3%) since it peaked at $994,873 in February.

It is now the lowest it has been since July last year.

In Waikato the average asking price increased slightly to $561,995 from $557,071 in May, but remained below its March peak of $575,528.

In the Bay of Plenty the average asking price declined for the second month in a row to $624,207, down by $55,152 (-8.3%) compared to its April peak of $664,652.

It is now at its lowest point since September last year.

In the Wellington region the average asking price dropped to $593,686, the first time it has been below $600,000 this year and and down by $39,212 (-6.2%) from its March peak of $632,898.

In Canterbury the average asking price dropped to $480,045 which was the lowest it has been since July last year.

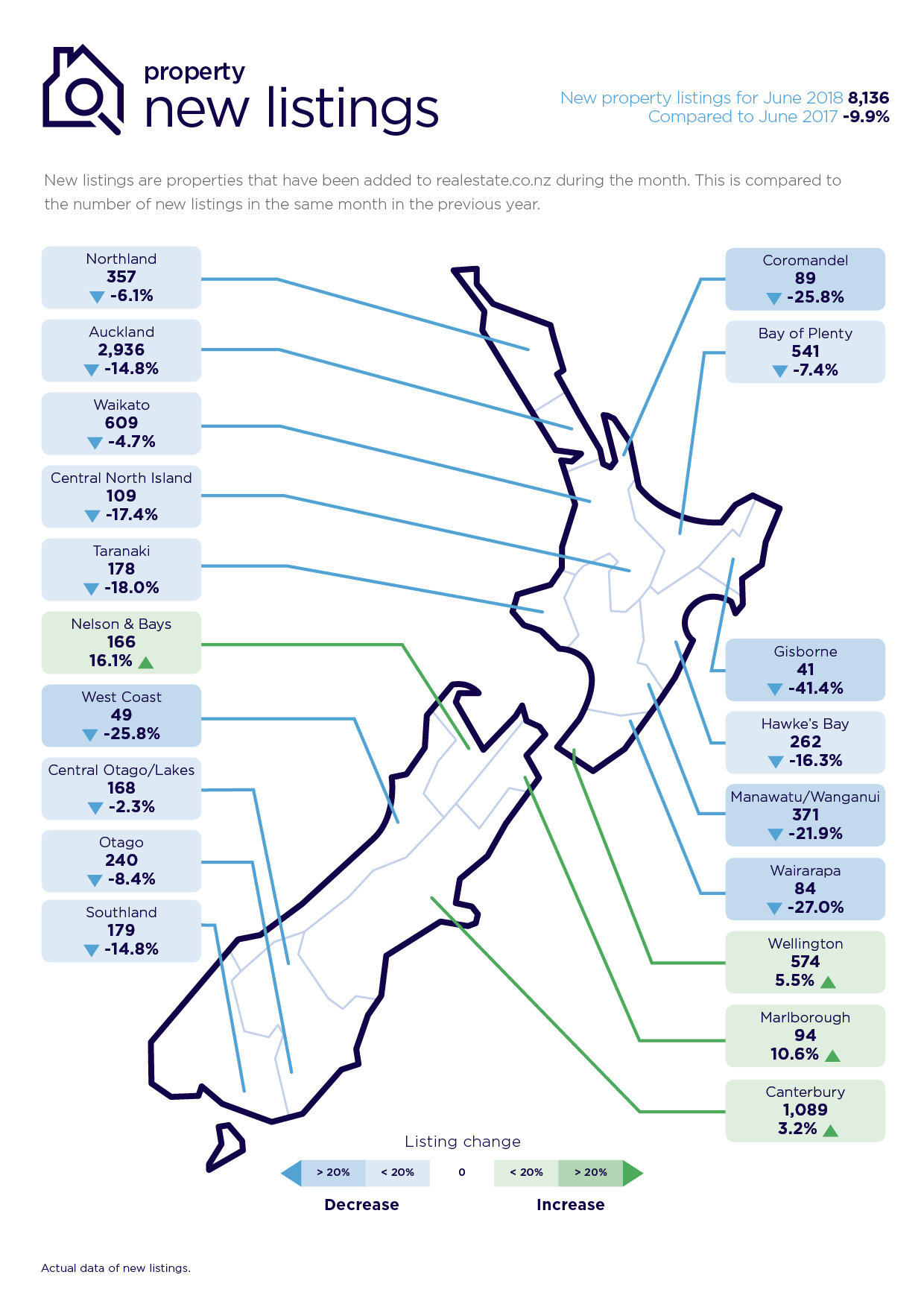

The overall decline in asking prices has also been accompanied by a drop in the number of properties coming to market, with 8136 properties being newly listed for sale on Realestate.co.nz in June, down 9.9% compared to June last year (see chart below for the regional new listing figures).

The decline in new listings combined with the fall in asking prices suggests the real estate market could be facing a chilly winter.

"Typically in winter we hibernate and this June was no exception with cold weather felt across the country," Realestate.co.nz spokesperson Vanessa Taylor said.

"The reality is that people want to sell their property when they feel that it's looking its best and potential buyers are more likely to go out to open homes."

Housing inventory

Select chart tabs

179 Comments

How come Auckland is down so much? This seems conflicting with the Auction results.

Anyhow good morning everyone! First comment! YAY

Lol, you just gave ttp a frost bite

House in West Auckland we've sold 18 months ago has gone down 18% in value ever since. (estimates according to trademe and when selling spot on)

Umm. Auckland is now dropping in price faster than Sydney's house prices, and that's before the Foreign Buyers ban. Well the good news is that mortgage rates will have to continue to drop as well.

Wouldn't be surprised to see rates drop to 2% level like they've been in the UK for quite some time.

Not sure 2% mortgages are a good thing. As we would see our debt level go up, housing demand as well probably and it would hurt the elderly a lot though since 2% mortgage rate would mean 0.5% TD rates, as you said just like the UK.

Well the options are; either ultra low mortgage rates so wage earning people can afford artificially high Auckland property prices (pumped up by foreign buyers) Or let property prices plummet.

I remember that it took a -20% crash before the 1 to 2% mortgage rates kicked in the UK.

The UK is in a unique situation where they are holding on to every last straw before the economy collapses into a deep dark recession for years to come.

Wage growth levels in the UK have been in retrograde and investors afraid of the Brexit uncertainty have been pulling out in droves. The last thing they want is a housing downturn to push the economy into a hellhole; something policymakers and bankers deem inevitable but are trying to delay as much as they can.

^^ my assessment of the UK economy is exactly the same ^^

That's why we all left... But when you look at how reckless the banks have been over here, we may have jumped 'Out of the Frying Pan into the Fire.' as Tolkein would describe things.

Yeah, seriously, has there ever been an own goal as bad as brexit? With trump in the White House the world must be starting to look like a pretty lonely place for the UK

We'll see. I still don't have much confidence that the Eurozone will look the way it does in 10 years time. It may be a lot smaller with a reduced membership of just France and Germany (maybe with Benelux nations as well), which would be fine so long as it stops them going to war with one another.

The rest of Europe is broken and only a major devaluation (return to previous currencies) will spare them from a protracted social disintegration. The political will remains to keep it all together, but watch Sweden, Italy, Spain and what the populous do over the next 5 years. Brexit may have just been the catalyst of what everyone else was thinking but were too busy with their hands out to do anything about.. As the debt burden rises we'll see if the relationship holds together.

It's a bit like an Auckland/Syndey marriage, where there is an 8 times household income, interest only mortgage to put a bit of stress on the relationship..... At some point someone may say, bollocks to this I'm off, let the banks deal with it, I want my life back from slavery. Crash bang wallop, no Eurozone.

We didn't leave the UK because of Brexit or the obvious sink hole that the economy is in danger of falling down. We left so that our kids could grow up with their Kiwi grandparents, uncles and aunts. The major threat of Brexit is not the vote itself, but the absolute hatchet job the UK government are making of the negotiations. Arrogant, fantastical, shambolic buffoonery would be my description. They are incompetent cretins.

And I wouldn't single out the EU as being any more fragile than the world political climate in general. The whole thing is imploding. Trade incentivised countries to play nicely with each other. Bugger knows what the next chapter of world politics will look like. To use a Game Theory term, it looks like the collaborative game is dying a death. All bets are off as far as i'm concerned.

The game was working fine and Capitalism could have been spared, but in 2008/2009, those that thought they knew best re-wrote the rules. No-one has faith in the system anymore because creative destruction was prevented from taking place and moral hazard was side-stepped with the bailouts. Whether they want to or not if they try the same a second time, large parts of Western society will revolt. I agree, all bets are off this time around.

Very accurate description .

Doesn’t surprise me in the slightest.

The housing market has become relatively more active at the lower end - first home buyers.........

Obviously, this pulls down average prices (both asking price & achieved/sales price).

Further, in Auckland the apartment market is flourishing - which also pulls down average prices.

TTP

Yeah if you're prepared to pay 12k a year in ground rent and body Corp fees.

It wouldn't surprise you, as you don't have a damn clue of the real world, get the heck out of your cubicle and see the world

TTP, title says "asking prices down 8.3%" not sales prices. Unless I'm missing something here, what's this got to do with FHB activity? I think its more to do with vendor chasing buyer.

Eco Birds calling the July 2017 as the market bottom is looking threatened.

Hi tothepoint,

So what your saying is, that when the lower end of the market is going gang busters, the vendors will reduce their asking prices by 8.3%? Just out of the kindness of their hearts. What an enigma, wrapped in a steaming T@#$.

MTP

TTP, if it were true FHB activity was "skewing" the figures downward, the upper end must be weak with oseas based buyers ban iminent. Can't have it both ways!

Hi R-P

For sure, heightened FHB activity is skewing average prices downward. That's simply an arithmetical matter.

Plus, we can't ignore the impact of recent increases in Auckland apartment sales, as reported on this website and elsewhere.

Don't jump to conclusions about the upper end of the market and the overseas buyers' ban. The ban hasn't been tested and may well have much less impact than some people think: for one thing it's not a comprehensive ban and, in any case, there are technical loopholes in it. But, for sure, the ban has been a political platform for Labour - though it might well come back and bite Labour on the rump.

House listings in the sought-after inner-city suburbs of Auckland are scant at the moment - go look on the various websites. These properties remain in strong demand with prices as high as ever - no doubt fuelled further by the new petrol taxes. (Please excuse the pun.)

By the way, didn't Labour say it wasn't going to impose any new taxes this term if it came to power? That's what I recall anyway.

Don't get me wrong: I'd love to buy a house in Auckland's inner-city suburbs and enjoy the convenience and lifestyle that goes with it - but prices there will likely forbid that forever.......

Have to cut one's cloth to suit the budget, so now looking elsewhere.

TTP

You're missing a step in the logic here, the data series is average asking price. This could be skewed by increasing supply of lower priced property, but you are arguing it's caused by increased demand of lower priced property. How does that follow?

I'm not entirely sure how the data is calculated (happy to be corrected), but I could reasonably argue the opposite - low priced properties are being snapped up which removes them from the average asking price calculation and drives the average asking price higher than it would otherwise be.

Hi mfd,

There has to be increasing supply if the increasing demand is to become effective demand - translating into actual sales.

Given that sales volumes are up for first home buyers that's been the exact situation. Sufficient people with lower-priced properties have listed them and sold them (to first home buyers).

As long as such properties remain below the average price, the average price will fall (i.e. be pulled down).

TTP

Given that sales volumes are up for first home buyers that's been the exact situation. Sufficient people with lower-priced properties have listed them and sold them (to first home buyers).

I think these troll routines quickly turn into farcical nonsense.

Well, J.C., like or not, that's the case: a first home buyer can't buy a house that doesn't exist.

The supply/inventory/stock of houses has to be in existence if (first home) buyers' demand for houses is to become realised.

TTP

I disagree, you're pushing on a piece of string here. Higher FHB activity reduces the stock of low priced housing, which would drive up average asking price. You're now saying there must be an increased supply, not only counteracting this but actually exceeding it to drive the average asking price down. Where is your evidence?

The evidence lies in the increased sales volumes.

Sales volumes can’t increase without there being commensurate supply/listings!

TTP

Of course they can if there's an inventory, it just means the inventory gets smaller. This is exactly my point, the inventory of cheap houses would decrease, pushing up average asking price. You are not making any sense.

Hi mfd,

In the (very) short-term the inventory/stock might be (relatively) fixed but over time can increase, typically in response to higher prices being offered to suppliers/vendors - in this case through the impact of an increasing number of FHB entering the market. Thus, the inventory/stock need NOT get smaller.

Conversely, if prices fall, suppliers may provide less of the house/asset, or whatever commodity it happens to be.

This is a standard market effect - first articulated in the late 19th century by economist Alfred Marshall in his book "Principles of Economics (1890)".

Note that Marshall was one of the founders of neoclassical economics. He's credited with being the first person to describe the "supply and demand diagram" of Econ 101 but which I prefer to call the "Marshallian Cross" (in honour of him).

TTP

Prices are flat, so I don't see the mechanism. You think more lower quartile houses are being supplied purely because more FHBs are active, even when those FHBs are actually just displacing what was previously Investor demand. Demand has fallen overall in Auckland. Prices have not risen.

...But houses aren't being supplied marginally.

There is excess supply - so, sales transactions can quite easily increase without a commensurate increase in supply.

Hi nymad,

If there is excess supply (or a glut on the market) then, ceteris parabus, prices will FALL until market equilibrium is reached - i.e. the price at which the quantity of houses willingly demanded by first home buyers equates with the quantity willingly supplied/listed by house vendors.

TTP

Yes, because ceterus paribus is a logical condition in dynamic equilibrium.

Actually. No. It's not. It's a stupid confdition taught in an introductory stats/metrics class to help students understand coefficient estimates in marginal terms.

Quote elementary economics all you wish. However, your lack of understanding leaves you contradicting yourself daily.

If there is excess supply (or a glut on the market) then, ceteris parabus, prices will FALL until market equilibrium is reached

Yes. But under what time frame is the adjustment and what are the dynamic considerations.

By your own admission, you have said:

- Prices are sticky downwards

- Supply is relatively fixed in the short term

- Houses are heterogeneous

In all cases, you are correct. However, you can't connect how these factors interact with each other.

To anyone, this is just a weird argument you are trying to make. You have no idea of the distribution of transactions spatially and demographically, so have no way of knowing the true relative increase in FHB within the market.

Your argument hinges on the assumption that there is one buyer for every (heterogeneous) property and that we don't believe in isoutility.

So, tell us exactly what you mean. And give us some reliable data or theory instead of the standard TTP drivel.

Hi Nymad,

Your ego is at work again. But you don't use technical jargon eloquently - or the least bit convincingly. And it's far from clear that you have a grasp of "elementary economics".

Everything I've said is valid in the context in which it was written. (You have not disputed that.)

I've responded to numerous scenarios/synopses/arguments of contributors here over the months I've been here. Nobody (not even the best of modellers) can hope to have a complete understanding of how all the various factors/variables/constructs within a social/economic system will interact/connect in a dynamic real-world situation - but that's what makes the social sciences (including economics and psychology) challenging. One often comes within the normative realm here - still a worthy area of endeavour. And well-considered judgements are always be a fertile area for debate and on-going refinement.

In any case, as someone who's interested and studies local/regional property markets (as well as consumer psychology), I just might have a better understanding "of the distribution of transactions spatially and demographically" than various other contributors here.

It's absolute rubbish to suggest that my views "hinge on the assumption that there is one buyer for every (heterogeneous) property.....". None of what I've said implies a monopsony situation.

I remind readers that you've boasted in the past about being an econometrician and an expert in economic statistics - but subsequently, when I pressed you, you confessed that you couldn't distinguish between the cyclical and structural factors impacting on the property market........

Sorry nymad - but you're certainly no Rex Bergstrom, David Giles or Leslie Young.

TTP

TTP .......I have noted and read your comments ....spoken like a true RE agent BTW.

You talk as if the Auckland market is "totally immune" from any influence of any kind - whether local, national or international ?

So in your "learned" view are there any factors one should be aware of, when buying said real estate in the more "leafy" parts of Auckland or are prices are on an upward trajectory, indefinitely and forever ?

I just hope for your sake, that your streams of income are not all in the above market and you have other income streams outside Auckland property .......and your debt levels are low and equity is high.

Hi Crazy Horse,

Property is not homogenous. Every property is different - and they all need to assessed on the basis of their relative strengths and weaknesses.

Certainly, there are some great properties in the leafy parts of Auckland - but there are some lemons as well.

As always, working through the due diligence process is important - otherwise one could easily lose money on a dud.

If, however, one chooses property wisely and manages it prudently, then there will likely be benefits to reap over time.

By the way, I have no links with the real estate sales industry and never have. Personally, I don't warm to the industry.

Further, there are plenty of other people with similar views to me who are not in the real estate sales industry. So you need to be cautious about stereotyping.

TTP

Hi TTP.... thanks for the reply and I concur that in every market/area, each property is different ie good buys or bad buys etc

However, the real point of my post above, was the Auckland market in general and why you and I quote "plenty of other people with similar views to me" seem to think there is just nothing that can stop Auckland property prices from flatlining or decreasing - good properties or otherwise ?

So I can categorically say that TPP et al will NEVER entertain the thought, even a good property in Auckland, will NEVER decrease in value ? Furthermore, Auckland property is NOT affected by local, national and international factors in any way, shape or form.

I admire your optimism ..........

Hi Crazy Horse,

There are things that can cause a DECREASE in values. There's ALREADY been a FLATLINING in values over the last few months.

I've stated here BEFORE that one such case of a decrease in values could be a serious epidemic - such as the 1918 'flu' epidemic. If 10% + of the population was wiped out in such an adverse event, there might well be a significant decline in property values.

We all have to live with that type of risk - and it doesn't necessarily exert a major impact on the individual's decision-making.

TTP

I see a couple of interesting FHBer type properties in the Auction results pages.

This was new in 2007 and sold for 376k. Sold last week for 690k. 2017 RV of 795k and TradeMe middle estimate of 770k.

With a 2007 price of 376k you would expect it to sell for something like 740k. However we see a 2012 sale for 407k - astonishingly little gain for five years. One would have to assume 2007 price was too much. 407k in 2012 should translate to around 690k in 2018.

Nevertheless it seems a good buy for a freehold section and house in good condition. Does have a strange mixture of cladding though that could have influenced the price. However if this sale is an investor cashing up then they still made a fine profit of 283k gross over six years.

A ZS win/win scenario for both seller and buyer. FHBers should watch for these opportunities!

The other one is:

10 BRUNNER ROAD Glen Eden

Sold for only 660k with a 2017 RV of 820k.

No sales history unfortunately and definitely a do up which impacts price significantly. This price is only 13% above 2014 RV of 580k.

FHBers should consider these sorts of places. A do up status knocks 100-200k off the price.

29a Don Buck Road. 80sqm house with 100sqm deck!

Good for Govt coffers too.

they still made a fine profit of 283k gross over six years

@28% - 80k in tax.

Sluggy why would there be tax paid on capital gain?

TM2, of course it depends on the initial intention. IRD are monitoring more and more these days with no time frame on retrospective assessments. If one doesn't sell, no tax. If one doesn't sell then capital gains are just on a piece paper as today's good news story and are not banked.

Hi R-P,

You write, "IRD are monitoring more and more these days..."

Are you sure that's true?

I hear (and read) that IRD staff are demoralised and more focused on their stress levels, technology failures, pay, working conditions and potential industrial action - than their actual work.

In these circumstances, how can we possibly expect IRD staff to increase their productivity - including monitoring activity?

Let's hear it for our tax gatherers - decent/honourable public servants carrying out a vital role who, by all accounts, are having a damned tough time.

Please consider ticking the little "thumbs-up" icon not in support of me - BUT in support of IRD staff.

TTP

TTP, it is wrong for you to mislead others into thinking their tax obligations may be overlooked. As you should already know, IRD investigations have been provided considerable additional funding to expand their work here; https://media.ird.govt.nz/articles/property-compliance-at-inland-revenu…

What youre referring to is this; https://www.stuff.co.nz/business/industries/105107686/inland-revenue-co…

Based on that rate of return Id triple the team investigating property transactions and specuvestors.

Edit - perhaps they could outsource the investigation for a cut in the collection as with that rate of return people would be fighting for that work

Averageman, for those wanting to divest and bank gains, its difficult to navigate around CGT unless there's a strong case for an unavoidable change in circumstances. The longer one leaves it without seeking clarification, the bigger the potential surprise when there's a knock at the door. There's no mention on their website of a time frame limit for retrospective assessments.

Hi R-P,

Happy to stick with what I said above.

It's a tough job at IRD these days - and many staff are under pressure. (The latest technology issues compound matters.)

It's difficult to achieve work-life balance under such circumstances.

A little bit of empathy/compassion for IRD staff would hardly be out of order........

TTP

TTP, I also feel for IRD staff. With technological advancements in data sharing and alike, IRD will have more information spoonfed to them in a more efficient manner. In the end, less man hours will be required to monitor tax compliance. It's never easy for staff during such a transition.

Thanks R-P,

I'm with you on that one!

Happy if you'd be prepared to tick the "thumbs-up" in my post above - but over to you.

Best,

TTP

However if this sale is an investor cashing up ....

If you are an (honest) investor, you get to pay !! Hooray !!

I wonder if the next 5 years will look like your first example from 2007 to 2012. 8% increase, 1.5% per year. Could be depressing for the negatively geared.

Anyone in negative equity yet?

What are you talking about Jock... Repeat after me,

Always go up, always go up,

We're diffrunt, we're diffrunt.

Debt is your frund, debt is your frund

Re-cycle your equity, re-cycle your equity.

Always go up, always go up.

Specuvestors starting to dump the fringe and get whatever gain they can before it erodes any further. Any stats manipulation probably muted with the final rush of overseas money in their perfered zones.

Volume definetly in decline and not a suprise and speculators would perfer a hold vs sale for less that it was 18 months ago as long and the lending rates and tax washing is maintained. One is changing, will rates go up or stay down. Lots of noise about it going up but no sign of that, with most recent change a decline.

People are picking that we are at the top of the market due to the foreign buyer ban. I know some here argue that the foreign buyer ban "won't achieve anything, people will get around it" but i'm sure there's a lot of people out there holding surplus property that don't want to take a chance.

Did you read yesterday's article about banks sealing foreign accounts... more loopholes being closed

Interesting, can you post that link?

> It is now the lowest it has been since July last year.

It's almost as if seasonality has something to do with stock and pricing?

Seasonality has always had something to do with housing stock levels - and can impact on pricing as well.

TTP

Hope you've stocked up on food, going to be a looooooooong arduous winter. See you in 2020

Hi H-O,

There’s no point just looking at the figures.......

The trick is to work out what’s going on behind the figures.

TTP

Yes Ho. Don't bother looking at he number, just use your gut and crystal balls.

with regards to the last part, i guess your referring to TTP, as he may not have any after the frost bite

Bhahahaha....you mean using ANECDOTES....you are easily the most hypocritical commentor in the history of interest.co.nz. When Cameron Bagrie looked beyond the figures using some anecdotal information a few days ago you were highly critical of him.

Hi Graham Adams,

The most respected economists don't stoop to anecdote.......

Their domain is analysis - good, rigorous analysis.

TTP

You'll still be tripping over your own shoe laces when Auckland house prices are down another 10%+.

Can you provide any evidence that "Auckland house prices are down another 10%+" No you can't because it's just not true

.

Well I certainly have stocked up on everything. I work in finance, for a charitable organisation which gets it's funding from the government amongst other sources and when there is a change in government, everyone gets nervous as our jobs can be gone by lunchtime with no redundancy pay. So several pays ago, I decided to stop spending my discretionary income into our economy and now I am stashing money away to the value of about 60% of my nett takehome pay. I know others who are also no longer spending. If enough of us do this together, our economy will tank and ultimately jobs will go and house prices values will also fall through the floor. It is a self-fulfilling prophecy when people on-masse suddenly change their spending habits at the first hint of a looming recession!

I've noticed a steady decline in average temperature since the start of the year, if this trend continues I predict December will have an average temperature of -10 degrees Celsius.

Auction brought forward to 10am this morning. It has a CV of $2,400,000 and rumour has it that the vendor received a pre-auction offer of close to $3,000,000. She can't refuse, can you?? Got to love DGZ ^^

https://rwremuera.co.nz/auckland/remuera/9a-komaru-street-19168707/

Hope you didn't forget your sanitary pad

HO, Still insulting others instead of discussing issues...

Will you wait till the rush hour finishes at 1.30pm DGZ or will you start walking now?

what a weird layout, two dining rooms, dont the kids eat with the parents or maybe one is for the help.

also whats with the midget bath looks 2 inches deep.

not to mention the many floor levels, looks like they like the stair exercise regime.

if i was her i would take it can not see many buyers liking this layout

It's not about the house. It's about the location / zone.

That bath is weird as hell. Distorted photo? Optical illusion? Nefarious plot to kill granny when she tries to climb out?

You talking about the sunken bath? I don't like where the kitchen is, off in a corner of the house separated from everything else

This house has been sold under the hammer in the auction room this morning.

Update - it went for 10.5% over the CV at around $2.65M.

It doesn't matter if you dislike the sunken bath or hate the kitchen being at a corner. Good properties in good zone close to the city are still very desirable.

So much for the $3mil pre-auction offer huh?

I did say close to $3M but it was a guess. $2.65M may sound cheap to you but it's still a lot of money.

$2.65mil is obviously not cheap. But it's also nowhere near $3mil. It's nearer 2.5.

Well $2.65M is obviously very average in this area. If you round it off to the nearest million it would be 3 not 2. This one is what I call not cheap... https://rwremuera.co.nz/auckland/remuera/46c-eastbourne-road-18880235/

Double-GZ - I'd really be keen to know what your obsession with expensive property in the Double Grammar zone is???

If you are not a RE Agent, then why are you so obsessed about it?

If you are not a property professional, it seems a rather odd obsession

It's just a hobby simple as that - why is it so hard to understand?? A RE agent I am not but there are plenty who live around me. I only report on what I see around me...

Double-GZ what are you going on about? You boasted that there was a pre-auction offer of near $3million, when the CV was $2.4mil. The house sold MUCH closer to its CV than it did to your exuberant $3mil.

Dude, we know how you love your postcode, we love you for it and it amuses many of us no end. But this house didn't sell near $3mil and you're just going to have to live with that. Have faith, another sexy bit of DGZ property porn will be along soon to perk you up, real soon.

Ok it's not $3M and you win, happy now gingerninja? My next focus would be this one with CV $2,275,000. The vendor paid $1,020,000 in 2011. How much do you think it will go for? Auction this coming Saturday onsite at 3pm ^^

https://rwremuera.co.nz/auckland/remuera/12-brookland-place-18724521/

Don't be a sour puss Double-GZ I was only teasing.

I don't have your specialist DBZ love or knowledge but at a guess 12 Brookland will go for around $2.3-$2.35... what do you think? It would be higher but the kitchen and bathrooms are a bit cheap and dated.

This location is not as attractive as the previous one and it's at the end of a downward sloping cul-de-sac. I know the street was a flood zone over 15 years ago but the issue was resolved by big underground storm water drain built probably right in front on this property on the main street. The internal layout of this house also looks weird, like it was hacked around by some DIY builder in the past. My guess is below CV, say somewhere between $1.9M and $2.2M but you never know what Mr JQ can do with his magic wand ^^

Whether it sold for $2.65mil or $3.0mil hardly matters: it still shows a big dollop of confidence in the Auckland housing market.

TTP

Gingerninja - my understudy Point Made (TPM) told me that she's thinking of buying that section in Wellington (Brooklyn?) that you were looking at a few months back. I thought I should tell you, in case you are still interested in it. TTP

TTP Nope. Definitely not interested. We don't want to to stay in Brooklyn because we've moved our kids to a private school and Brooklyn doesn't have a bus route there. Brooklyn is a lovely suburb though. Gorgeous views, quick journey into the CBD, lovely community.

It's a pretty decent section too and it would be hard to overcapitalise on it with a decent sized house with those epic views. Good luck to him!

Brooklyn Beauty for you gingerninja? http://www.justpaterson.co.nz/property/JP1279/8-bruce-avenue-brooklyn/

It's a beauty that's for sure.

Just noticed the website has been updated with a SOLD sign. https://rwremuera.co.nz/auckland/remuera/9a-komaru-street-19168707/

How is ''asking price''even a catergory in any survey.

I could ask 1 million for my 500k house and i'm quite prepared to drop asking price by 8%.

The Briscoes pricing method.

Haha at this point TTP will start to attack the messenger, the grammar , syntax, anything but admit that his precious property market has finally peaked ....

watch carefully he will soon starting saying "I told you so......"

With all due respect, IT GUY, the market as a whole peaked around Oct/Nov 2016 - or at least that's what I understand.

Since then (about 20 months ago) it's been relatively flat - which is what I've said time and time again.

Time you got a grip on reality.......

TTP

TTP I might have to agree with you so far - it looks like the classic NZ housing market slowdown rather than the bubble pop that most of us were expecting.

A decent recession about now could change things though...

Thats EXACTLY when the market peaked, I know someone who sold at Auction in November 2016 and they have not looked back.

Auckland peaked 2016 but plenty of places peaked well after that or have yet to peak. Wellington ran hot in 2017 and started cooling more recently.

There are very little "Asking prices" in the new to market and >$1M as the majority of these are either sold by Auction or by Neg ... so these will be outside these figures... asking prices usually come out when they pass in auction and sellers are in a hurry to get out.

Actual Median, and average, actual sale

prices are what matters .. so be patient.

And July numbers are only 29 sleeps away :)

you're talking about being patient..

but you dont have patience when it comes to KB?

I agree, actual sales prices are much more interesting. However,

"In Auckland the average asking price declined for the fourth consecutive month to $912,071 and has now lost more than $82,000 (-8.3%) since it peaked at $994,873 in February."

If the average asking price is close to $1M, I do not understand how you can claim that houses going for >$1M are excluded from the dataset. A significant number of million dollar houses must be in there to allow such a high average.

Additionally, the trend can still be relevant unless this exclusion of high priced homes is a new thing, if the composition is stable then your argument would make no difference to the trend. So, are you arguing that high-priced houses used to have asking prices and now they don't, and this is reducing the average asking price? I've not seen any evidence of that.

There’s a real reason for these mostly nationwide falls and it’s just the beginning. Permanent departures up 10.4%. In the month to May 5818 permanent departures alone (Interest.co.nz). I see a repeat of 2001 shortly after Labour got in last time. This turned into a mass exodus in the following years. Everyone dumping their houses, businesses and other assets and taking their net worth with them. Get ready people, this is just the beginning. There’s a looooong way to slide. We’re in for a NZ the way the voters wanted it. Socialist, Labour, NZ First (whatever they stand for now) Green extremists. What the heck were you thinking of.

I wonder where they're going?

Uber drivers in Noosa if my experience of the last two weeks is accurate.

Not Uber, old trick.. it's now Ola

Allears - have you got anything between you?

I don't sense it from the rave.

We are living 13 years past peak conventional oil. We have twice as many people on the planet as there were in 1980 - all wanting more. And every resource is being tapped at more than sustainable rates, increasing exponentially in most cases. Not only that, but we used the best, first. So the available quality gets sequentially worse. Atop that, there is maneuvering for access the 'what's left'.

Yet you think it's going to matter who is in control of parliament. A bit like a Titanic passenger complaining about getting a red deck-chair, methinks.

Hi Allears,

No such luck for you, I'm afraid!

The housing market is far more resilient than you believe.

TTP

As my comment and real facts show, it’s not about housing price falls. It’s about a general turnaround in NZ’s economic fortune. Those who get out now are the real winners. Cash up and get out before your net worth falls more. Immigrants generally bring little financially into NZ compared to NZ’rs leaving permanently. Have you stopped to look at NZ’s falling $ lately. People cashing up and leaving SELL NZD$ and buy currency of the country they head to. Someone selling up and leaving is usually also a highly motivated person, a producer, poss employer, someone who NZ can least afford to lose. NZ is entering a crisis and you need to be aware of the real facts. This isn’t ‘fake’ news. It’s real and it happening around you right now. “Isn’t she lovely” won’t save NZ from the mess she’s creating.

Allears, but where isn't in or near crisis? Things are looking gloomy and unstable across the globe.

Gingerninja

You are a great commentator, however I don't share your pessimism.

Equally, I don't share the rabbid and irrational optimism of the Property Nutters here.

I think the reality is somewhere in between - there are plenty of headwinds ahead, things might be a bit volatile over the next few years, but the world seems to find a way of getting itself out of these holes.

Who knows if there will be a financial crisis in the next few years? There are some warning signs, but a crisis is far from certain.

I think the takeaway is that people should be cautious in these times, but not be too fearful of risk. Some of us - like me - have made bad financial decisions in the past based on overly pessimistic predictions from 'experts' that never came to pass.

Fritz I didn't mean to come across as pessimistic but I just personally don't agree with Allears that people should necessarily be fleeing NZ for elsewhere. I mean, if you have a great opportunity, sure, grab it with both hands but everywhere looks as risky as everywhere else. Don't flee NZ just in case there's an apocalypse. Markets are increasingly globally synchronised anyway, so I don't think there is cause yet to get our chicken lickin on (about NZ).

It's not about a psychological state for me anyway. From my perspective, change is the norm and the only predictable factor. Things can go up, down, sideways or just stay where they are for a time. So you should take the risks you can afford to take and be sensibly diversified so you can adapt to the inevitable changes. I agree that being too cautious or too risky is a bad play.

Hi Gingerninja,

But not in the sprawling metropolis of Palmerston North, I hear...... (-;

TTP

Could someone please advise us how they come up with the asking prices when so many don’t actually have an exact asking price.

I note the article says that Canterbury asking price is down, where in the stats from last month the average price is up!

With all the things that this government is bringing in to hinder landlords it is not surprising that some landlords are wanting to bail out.

Reality is that it is going to badly backfire on the government as the private sector rentals will ask more for their rents due to the governments meddling.

With the standard of state houses, people will need to pay the increase as who would want to rent a state house??

have you suddenly woken up.. didnt bother to ask this question over the last decade... why, prices were on the up and you were very happy..not so much now, eh.. poor lad..

HO, I have asked the question previously!

Never answered .

I'm not sure exactly. I found a snippet in the latest Trademe release footnotes:

"The Index uses an “80% truncated mean” of the expected sale price to calculate the average asking price. This excludes the upper and lower 10% of listings by price, and averages the expected sale prices of the remaining properties."

I'm not sure if they take an 'asking price' even from listings without a public asking price, I think they still have an estimate in the background to allow them to appear in the right filters. My assumption is, they cut out the most expensive and cheapest 10%, and simply average the asking price of the remaining central 80%.

As for disagreeing with average price, for one thing asking price is a leading indicator while settled price is lagging, so there's a couple of months difference which means month-by-month they may not agree. Secondly, both datasets are noisy and in Christchurch essentially bouncing around zero, the basic trend is flatlining prices.

It is true that not all properties listed on Realestate.co.nz have an asking price, such as those being sold by auction. However when a property is listed for sale on the website the vendor enters an approximate price expectation (which is not visible to viewers). That's so the property will be displayed when prospective buyers use the price range search field to locate properties they could be interested in. Where there is no actual asking price, that is used as a proxy.

Thanks for the clarification, Greg.

TTP

Very Good, and we all know that houses are usually listed in lower price brackets to avoid frightening the horses and maximise exposure by getting more attention and views, especially when the real reserve price or neg price is high.

Hence, this Asking Price indicator is rubbish all together and means Nothing - other than serving as another piece of Fat to chew on until the real numbers come out.

Enjoy the empty debate :)

The trend is undeniable

Pretty sure some here will deny it.

Double post

Yep. Also undeniable is this legislation proceeding under urgency https://www.parliament.nz/en/pb/bills-and-laws/bills-proposed-laws/docu… which is on track to be law in July 2018.

One criteria is stated as "New Zealand permanent residents that are ordinarily resident in New Zealand. At the time the persons enters an unconditional contract for sale and purchase, they have a permanent resident visa and have resided in New Zealand for the last 12 months and are present in New Zealand for at least 183 days in that period".

They will be required to sell if they cease to live in New Zealand...empty homes in over priced Auckland anyone. Interesting the last report on the submissions and advise tab was related to the Ti Ari development being unhappy with the wording and being able to sell the house and sections to international big wallet types.

Perhaps the IRD should have a team focused on this and make sure any cashing up are taxed the full amount.

Falling house prices are just the ‘symptom’ of the disease/illness. The real problem is the economic downturn that’s infecting the nation. It’s always the result of socialist control in any nation. There are no ‘false facts’ or ‘fake news’ here. It’s real. Socialist governments like this one have a vested interest in keeping the poor, poor. It’s their voter base. Every time one of them sees the light decides to stop being a ‘dependant’ and comes across to the ‘other side’ by becoming independent, someone who takes responsibility for their own life, then the socialists, lefties, extremists lose a vote. Without their voter base they out in the cold again. There’s a good reason the ‘Left’ is called Left, and the ‘Right’ is called right. There actually is no money-tree or mythical fairies at the bottom of the garden. But when you’re baffled why your life seems to be without success and envious of those that ‘have’, it’s so much easier to believe in myths and fantasy. Fundamentally that’s the difference between Left and Right in all nations. When that nation voted to be governed by those who believe in mythical money-trees and fairies at the bottom of the garden then that nation is in for a fall. First symptoms in this case being it’s citzens protecting their interests by cashing up and leaving, business loss of confidence, and falling house prices.

So don’t focus on the symptom, deal with the disease. Socialism, laziness, complacency, dependency, and lack of responsibility for one’s own life success and failure. Get rid of the disease and you get rid of the symptom.

Hmmm......house prices in Australia are falling and yet they have a liberal/national right wing Government. You were soooooo close to a perfect model to explain house prices movements. So close.

Also, high house prices were the symptom. The disease was an economy built on ever increasing debt and immigration with anemic productivity growth.

Don't forget Australia also has State government which can pass statewide laws such as buying and selling properties. Recently QLD Govt added extra stamp duty of foreign buyers.

Victoria state govt is Labor.

The magical money trees are called Westpac, BNZ, ANZ et al.

They will lend against pretty much any old dog box without actually checking to see if the dog box they are lending against is actually a dog box.. Often it's a chicken coup and the hens are now coming home to roost!

Stop it. Just put your feet up in this "Quiet corner of Remuera"

https://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=12…

It has the leaky look and hate aluminium windows frames!

or you can have this across the ditch for roughly the same price or less.

https://www.domain.com.au/28-first-street-camp-hill-qld-4152-2014231495…

Yes it does but buyers are buying into the area rather than the house itself. Probably good for a developer to snap it up and bulldoze the house and rebuild.

It's a total crapper and has been on the market since Adam was a boy. It has that delightful feature of monolithic cladding where it goes down below ground level. Suggest you buy and put your feet up Dgzlol^^

Remuera is overrated.. Remu/Parnell used to be my hood

Look CM you can definitely still ditch Auckland without your pay going backwards, but if you're in Sales, Marketing, Call Centre, Cust Service, Admin, IT, Transport, Logistics, Science, Legal, Advertising then you're probably a lot better off in Auckland ^^

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

I actually earn more now than I ever did in Auckland. It's a numbers game. More immigrants in Auckland competing for wages which actually pushes down salaries. I had alot less people to compete with in my new town, virtually no immigrants and I just got another decent payrise to my delight.

"It was devastating, but we faced up to it," says Bill. "It was a long process, and our house underwent the absolute Rolls-Royce of remediation and re-cladding before it got the all-clear.

"The good news is that 18 years later, the place is better than ever and we haven't had a single hint of worry since," he says. "It's truly as dry as a bone."

MmmmmmHHHHMMMMmmmm.

Rolls-Royce of remediation? From my memory it doesn't even have a cavity. Looked pretty shoddy.

I'm not sure what data you are basing this on, please feel free to enlighten us. I note the currently US Government, which strongly disassociates itself from Socialism, is currently borrowing an enormous, and growing, amount of money.

https://www.stuff.co.nz/national/politics/96756247/Is-National-really-b…

https://www.forbes.com/sites/realspin/2016/11/07/trump-is-right-about-o…

http://politicsthatwork.com/blog/which-party-is-better-for-the-economy…

http://www.primeeconomics.org/articles/taq30tk04ljnvpyfos059pp0w7gnpe

The Auckland housing market topped out long before labour took office and the boom was based mainly on myths and fantasy in the form of a speculator fueled ponzi and mythical Chinese money

Canada, UK & Australia are all starting to crash, we wont be far behind and if we push interest rates down further our dollar will further devalue meaning large inflation for imported products.

You see where this is going, a recession is almost inevitable even before the global debt crisis explodes

So foreseeable so it would only be a muppet that spent tax payers money like a drunken sailor on pay day, right?

Just getting the counter-cyclical fiscal stimulus in place early.

They should double down then and make it even better. I follow a save for a rainy day with no debt strategy, which is why I'm ready and waiting to pick up the discounted spoils when the Coalition of Cultural Marxists tanks the economy. Giddy up.

.

I'm with you. By hook or crook, I am taking a personal part in bringing this false economy down to it's knees. I stopped spending my discretionary income about 4-5 months ago. No debt here either, own house outright. 60% of my take home pay is now being stashed away, not just for a rainy day. I am expecting a storm!

Yeah so let's just hope and wait for the recession and debt crisis to explode. Ain't you clever.

Good advice Double-GZ.

Agreed. The cost of continuing to pretend and extend only serves the banks and their global owners.

Unfortunately most governments ignore the need for sustainability and a balanced approach.

The lessons from the GFC were never seriously considered and the only rescue was stimulus, instead of working on fundamentals and building a robust approach. Quite the opposite has happened and debt has ballooned out of control.

National claimed we had a rock star economy but in fact it was just growth based on immigration, selling our housing on the international market and an increase in tourism. None of those thrive in a recession.

If we were truely a rockstar economy we would have innovated and grown our GDP per capita.

When the foundations are in BS, its likely the structure will sink... gurgle gurgle gurlge

Sad but true

If selling houses and tourism doesn't survive in a recession , then what do you reckon does please ?

Your views are very pessimistic, however, it is common knowledge that when S hits the fan then everything slows down and could come down to a halt in some cases and industries ...so the Foundation you are hoping to build can be the first to collapse then...

The "BS" ( as you called it) is what will pay the $520M+ pay rise to the nurses ,and similar amounts to follow to everyone else standing in the queue atm, it is where the $3B Shane Jone will be splashing around for the next 3 years etc etc etc.

So please, lets get a bit real and let's stop using big silly words like GDP/capita , sustainability, and productivity ... because none of these will matter when there is no money in the till ....

As for productivity, the entire world is struggling to find a definition for the damn thing and how to apply it with all the AI, technological challenges and trade wars !!

.

Well excuse me , but your comment is anything but Pragmatic !!

No, I chose NOT to acknowledge such a dreadful thing as printing money !!

For starters , NZ is not that stupid to print money to pay anyone !! .. I suspect that you could be so naive or ignorant of the damage that that could cause ! ... then you can really kiss affordability goodbye.

NZ would be told off by the IMF and every other lender in the world the moment they just think about it !!!

So let's get real and put emotions aside, we cannot create money out of thin air in NZ .. our economy is a spit in an ocean and we would most certainly kill our export industry and economy by doing that ...and send property prices to 7th heavens --- printing is devaluation and inflation leading to a recession, I bet you already knew that too.

No one is forcing anyone to buy overpriced shaks .. Rents are what they are .. exuberant or otherwise paid to landlords, Iwis or HNZ or whoever !! that is how the market is shaped today ...

Nine months after voting for change and this CoLs who were supposed to "correct the housing market " are still floundering around and have no clue of what to do next - they gathered 400 industry specialists to brainstorm the next move " thrash it down " as they said in 3 days - under the auspices of his Holiness, the RH photogenic PT, God bless his cotton socks, hi-vis and helmet...

https://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=12…

This "Summit" is the mother of all Scandals .... 1st of July came and gone, PT is yet to make these huge rockstar announcements about KB he promised months ago.

we ended up with a "Summit" to consult with the real expert in industry ( apparently after all has failed miserably) ---- Now , if that is not BS, incompetence, and mismanagement ? I don't know what is !!

Running Housing and Transport Ministries is anything close to running Oxfam with crocodile tears and sweat talk !!

Makes you wonder .. what if this GoLs and noobs had inherited a huge deficit instead of the huge surplus they have now ??

.

Yes, I have broken my own rules ...

but you are right , I shouldn't have replied to your stupid post in the first place - I promise not to do that again, no matter how silly your comments would be.

Innovation.

If you are a speculator on Auckland properties and Bitcoins, you need to get out now!

There we have it, a message from the PRC with instructions to cease gambling and return home.

Or failing that - declare your tax position to the IRD.

Question to the Doom and Gloomers is why do you think that a Capital Gains Tax needs to be brought in when you are saying that prices are going to continue to drop.

Any CGT will be GRANDFATHERED so no tax will ever be gathered!!!!

CGT is another way to bring the gain/profit in line with other forms of investment like shares, business investments etc.

It should be mutually exclusive from status of current house prices

Simply because a CGT doesn’t reside as some sort of arbitrary injection dependent upon the state of the market.

What are you thinking TM2?

Things just moving along really – always interesting nevertheless.

As I’ve mentioned before – in my mind simply the result of various key drivers of this market either being weakened or one way or another being removed – so not particularly surprising I would have thought.

However – another factor is now pushing its way through the crowd - the economic cycle.

The below is obviously US centric but it could be argued that the US is still the growth engine of the world.

“The current economic expansion began in June 2009 -- or 8 years and 7 months ago. If this one makes it to 10 years old next summer, it'll be the longest in U.S. history.”

They’re not called economic cycles for nothing.

You can bang on about the government’s policies if you wish – but in the end we may find that greater forces simply do not care.

Has someone got a link to the start of year predictions on property prices? I think I said down 10% this year for Auckland, but can't totally recall.

Let’s take it a bit further Fritz – where do you see prices in 2 or 3 years’ time.

Yes – so many factors and so many variables and all wrapped up in uncertain times – 10% is a start, but still won’t cut it for many.

However – it seems as though finally the majority of self-inflicted wounds are being addressed.

If the government stays the course – and the world doesn’t fall off an economic cliff – would it be that ridiculous to suggest that house prices for many will once again be reflective of the wages and salaries of most New Zealanders.

I certainly think they should be – yes, always difficult and a bit of a struggle or compromise to achieve home ownership– but not the absurd proposition that currently presents itself.

All good across here in the sunshine.

Petrol $1.30

Elec 20c kWh

Building materials half NZ cost

New 4 bdrm house on land $400k

CGT on only 50% of profit after 1 yr.

Far fewer bludgers

Oh, and 300 days of sunshine per yr.

Bail out now fellow Kiwis while there’s still seats in the available lifeboats. Let the Socialists and dependants suffer their own self imposed fate.

lol. I tend to agree with your humourous post. But I'm in a good position now, so I don't need to bail out, but I am likely to encourage my 21 year old daughter to bail out, as soon as she finishes her Honours Degree. hehe

-

REINZ compares "new listings" to June 2017 but "asking prices" to May 2018. It's a shame we don't have an "asking price" comparison to June 2017, in my opinion, it's always best to compare the same calendar months.

I left NZ more than a year ago with my partner and our kiwi daughter. We were a bit fed up by the housing situation. Although happy to rent due to making economic sense (as I thought NZ properties we're and are ridiculously overvalued) it was quite annoying to wait for the pop and to get my salary improvements swallowed by rent hikes.

Also we wanted to go back to Europe and being closer to families.

So we chose Spain, my country, specifically Malaga where I got a good job offer as Software Engineer. I was gonna make less money than in NZ obviously but moreless with a similar quality of life considering rents and prices.

The situation was way better than what I was afraid of. Now my salary in Spain is greater than what I was making in Tauranga (and I was making 80k when I left). But the biggest difference? Housing..

We rented for a while by the beach a modern 3 bedroom apartment with swimming pool for 1250 nzd a month. In Tauranga we were paying way way more for just two bedroom basic unit hot in summer and cold in winter.

Things were so good that we decided to look to buy something. We had some good savings we never got to use in NZD and Banks were hungry to lend money to low risk borrowers with good stable jobs with 20% deposit.

So we bought last year a 3 bedroom attic apartment built in 2003 with big terrace, a small balcony and a huge 90sm sunroof in a community with gardens and swimming pool where we pay 80 EUR per month in community charges (for swimming pool maintenance, gardener, etc.) and on the top of that I pay around 700 EUR a year in council homeowners tax.

The price was 180k EUR. Compared to the prices we were used to see in NZ this was a bargain. Beach is 10 min by bycicle and schools, doctors, big supermarket and public transport on the same street.

Conditions are also good. Euribor (currently -0.118) + 0.85%. Lower than inflation rate!

on 15 years mortgage for 90k EUR.

The thing is that the price of my home is a reasonable 3.7 times the household income (which is only my income for now).

We miss some things from NZ, mainly friends we left there, but looking back it was the right choice and we're glad we didn't make anything crazy in NZ like buying a house we could have bought simply because we had enough savings for banks to enslave us).

I don't know how things will be. Spain's economy was destroyed by a property bubble and prices on average were estimated to have fallen 60% since 2007. Now there have been increased in very specific areas (Madrid, Barcelona, Mallorca, Málaga where I live..) and they have recovered some ground up to -20% in some places since 2007.

But I talk to people here that bought at the peak. It's not nice at all.

They're still paying huge price on houses that are worth half now. The lucky ones were able to keep paying thanks to the low interest rates because of the EURO zone. The unlucky ones lost their homes.

Now the investment in property is gaining pace because rents are scarce and competition with holiday rentals is high. Some cities are banning residential apartments and Air BNB to protect prices because it's creating a social mess so prices could suffer soon even if interests are still low. Some others are waiting and seeing, but buying is now a better option over here.

My advice to young kiwis is: do not buy. Prices in NZ are way way inflated. China and emerging economies have an excess of savings flooding property markets and inflating them because productive economy is not profitable enough. But that will change. Don't make the mistake of buying expensive borrowing a huge amount of money at the historically lowest interests ever.

And don't desperate. I see Europe doing much much better. We for instance are looking constantly to expand the company with software developers and we cannot find enough. Depending on your profession English language could be enough in most of European countries.

Or sit on your hands because NZ property bubble has burst. It's just not so obvious yet the same as we didn't know that in Spain until 2008 that actually the peak happened in 2007.

Stay calm, save and enjoy your everyday life :)

Really good post and definitely one for all first home buyers to read. This could just as easily be a story from Ireland, large parts of US, Most of England beyond the SE. Greece, Cyprus, Perth, Brisbane etc and shows the risks of buying the bubble. Most of NZ will go through an adjustment over the next 2-5 years.

I hope so! Because I won't be giving up any of my future earning potential to the banks, just to help my child buy an over-valued shitbox. That is exactly what the banks want from us parents, to keep their shareholders happy.

I hope Chessmaster doesn't see this post, he will unleash so much butthurt and keyboard rage.

Málaga is gorgeous. Is Spanish your first language then?

Thanks. Yes, I'm originally from North of Spain but we wanted to move to a place in Spain where opportunities for English speakers and foreigners are abundant and where job opportunities are more international and speaking English was a competitive advantage in IT. And..the sun of course :)

My wife is welsh she lived in Spain for a long time, we love Spain, she lived in San Pedro just an hour from Malaga, we go back all the time to see her friends, love it there. I like Tarifa near Gibraltar and will be going to Tarifa to do some kitesurfing next year.

Wish you all the best.

Tarifa is great. Beautiful coast, enjoy it!

Your story should be highlighted as compulsory reading for all. Well done and thank you for sharing your story. You deserve a happy and prosperous life without all the debt.

Thank you. Very kind from you!

Glad you guys found it interesting

Don’t let eco bird read this, it will make him very grumpy

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.