It appears Treasury has heeded some of the advice Housing and Urban Development Phil Twyford not so politely gave it in May, when it released its Budget Economic and Fiscal Update (BEFU).

Twyford at the time called Treasury staff “kids completely disconnected from reality,” as he believed their forecasts showed they didn’t understand how KiwiBuild worked.

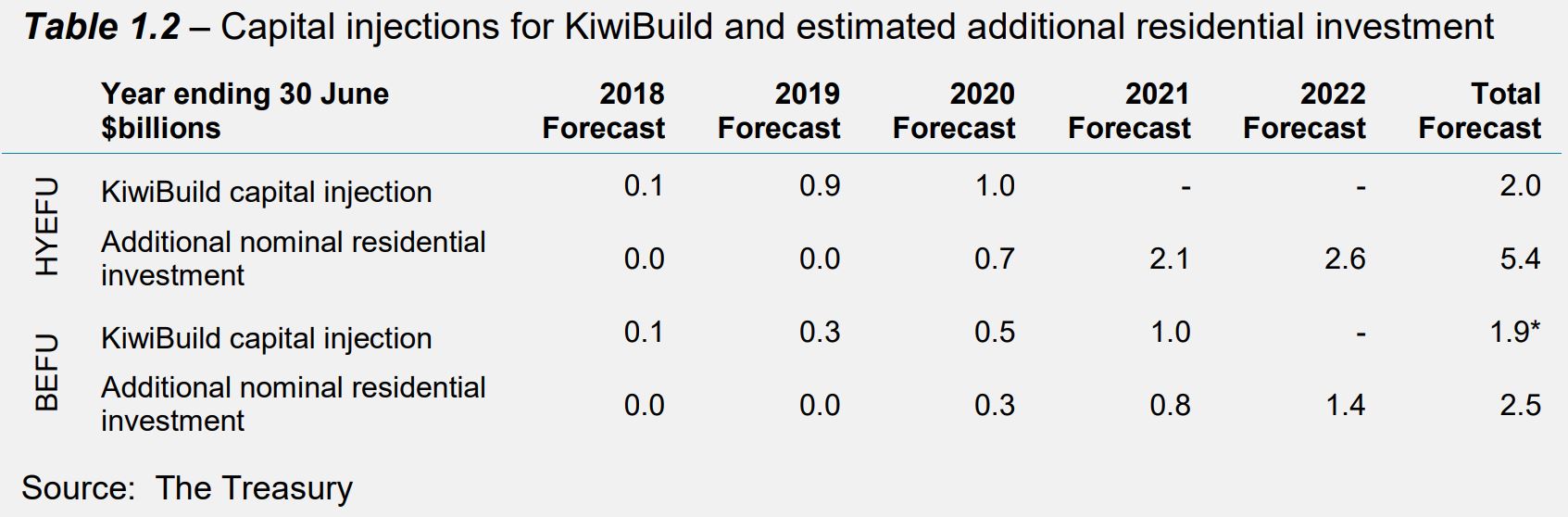

Treasury more than halved its forecast of the value of additional residential investment it expected KiwiBuild to produce, from $5.4 billion in its December 2017 Half Year Fiscal and Economic Update (HYEFU) to $2.5 billion its May 2018 BEFU:

This put Twyford on the defensive, prompting him to give interest.co.nz a Ministry of Business, Innovation and Employment (MBIE) paper that concluded Treasury used the wrong set of assumptions, so its 2017 HYEFU projections were more accurate.

MBIE said Treasury assumed the Government would have to fork out to kick-start KiwiBuild. But actually, most of the inital building was to be done by private development, underwritten by the Government through the Buying off the Plans scheme.

MBIE also said Treasury ignored the impact of houses being on-sold.

No update on Thursday

Fast forward to Thursday's 2018 HYEFU, Treasury didn’t give an update on its projections of additional residential investment resulting from KiwiBuild.

It couldn’t provide interest.co.nz with these figures either, saying the request would have to be made under the Official Information Act.

Treasury, in its HYEFU, did however revise down the amount of capital it expected the Government to inject into KiwiBuild, recognising “a larger portion of the houses to be delivered under the KiwiBuild programme during the forecast period are expected to be funded from the sale proceeds of houses rather than contributions from the Crown…

“Overall the impact of this change has improved residual cash by around $1 billion, compared to the BEFU.”

Asked to explain this, a Treasury spokesperson said in the BEFU it “was assumed the Government would invest $2 billion over the forecast period.

“With the refined information it is still expected the same amount will be invested, however some of this investment will now fall outside of the forecast period.”

So while Treasury didn’t say whether it now believed there would be more additional residential investment in the next five years thanks to KiwiBuild, it did forecast less Government investment during this time.

Asked what he made of Treasury's updates in HYEFU, Twyford said they better reflected how KiwiBuild operated: “One being that Treasury have now factored in capital recycling.

“The second is that they’ve factored in the fact that through the Buying off the Plans initiative, many of the KiwiBuild homes Kiwibuild is building don’t require the Crown to draw down on the KiwiBuild appropriation.”

Twyford didn’t take the opportunity to link changes in the HYEFU to Treasury’s summation of KiwiBuild in the BEFU.

How a potential property market downturn could affect KiwiBuild

Elsewhere, in the ‘Specific Fiscal Risks’ section of the HYEFU, Treasury updated its view of KiwiBuild’s potential risks.

“Changes in the housing market and economy may have an impact on the costs of delivering 100,000 homes and associated revenue recycling,” it said.

“If house prices fall, Crown underwrites may be called, and the value of land and buildings held by the Crown might fall…

“The Crown also faces general commercial risks associated with development and with implementing a large and evolving programme.”

Asked by National MP Andrew Bayly in Question Time on Thursday, what the forecasted cost of underwriting private developers through the Buying off the Plans scheme was, Twyford said the net cost was expected to be zero over the first three years of the programme.

“The target for the Buying off the Plans programme over the 10 years is to achieve a net zero cash cost of the underwrite.”

Twyford said his risk modelling, under a number of scenarios, indicated the cost to the Crown could be between $300 million and $700 million over 10 years.

“The Crown will always have the flexibility to reshape the programme if there are material costs over the first few years,” Twyford noted.

“There was no change in the HYEFU to the forecast cost of underwriting private developers through the Buying off the Plans programme.”

Bayly also asked Twyford what he thought of the other comment Treasury made in its ‘Specific Fiscal Risks’ section of the HYEFU: "To achieve programme goals, there may be a need to change policy parameters and provide support to developers and/or homebuyers.”

Twyford responded: “Well, every time Treasury does a HYEFU or any of the other economic statements that it's responsible for, it considers upside and downside risk scenarios.

“The member's referred to just one scenario, which includes the possibility of house prices dropping, but I would note that neither Treasury nor the Reserve Bank nor the Government believe that house prices will drop.

“House prices have stabilised in line with our policies, and on this side of the House we think that's a good thing.”

9 Comments

1) Can Kiwibuild - its middle class welfare.

2) Manage the immigration rate down to a sustainable level aimed at maximizing gdp/capita growth

3) Fix the RMA - its implementation is broken. Land use has to be freed up.

4) Put the Kiwibuild funding into Housing Corp + Urban Development Authority / Community trusts & get some housing for the poor built so they don't have to live in garages.

5) Legislate so that it is a crime for central and local government to have people homeless or living in garages. This should focus some funding in the right areas.

Nos 4 and 5 should be uppermost, a no-brainer.

OK we get some future high density low income areas BUT we get homes where needed.

Private landlords get pressures from a lot more social housing and ......

.....market prices for existing housing stock will lower thus allowing those first home buyers a great deal more choice rather than try to get one of the new ones in a ballot.

Sad for landlords. So what.

A sideline benefit is that investors will have to get more interested in other investment types.

I’m not convinced kiwibuild is welfare - the houses aren’t subsidised are they?

As for building state houses, if they were to build the 100000 that kiwibuild is meant to deliver at say 500k each, that is gonna cost $50 billion.

1 is false. Its developer welfare. Buyers aren't being subsidised, its the developers and RE agents* who are getting the benefits.

2, 3, & 4, Yep couldn't agree more.

5. You're dreaming. They would never pass that law, and even if they did its unworkable.. one person living in a garage and which MPs/Councillors get charged? All of them?

* why are there even RE agents involved with KB house sales? They sure as hell won't be working for free, so if they were knocked out of the picture then there is an instant $30k(?) per house saving.

Surely the MBIE can come up with a standard contract and a staff member or two to show the houses on Open days for far less than the RE agents take?

5. Legislate so that it is a crime for central and local government to have people homeless or living in garages.

This is a great idea and could solve homelessness in Auckland overnight. This could be achieved easily by imposing heavy fines, possibly imprisonment, for home owners and renters that use garages in this way. Vagrancy laws are probably already in place for street dwellers and just need to be enforced. Facilities for offenders could be setup on offshore islands or possibly the central plateau.

Just make it a crime to be homeless. Mandatory minimum sentence of 3 years imprisonment. Set up a turnstile at the prison gates because as soon as they’re released they’re committing a crime again.

While I applaud your idea for its efficiency and cost saving it seems a bit harsh. We should wait until the next day, when the crime has actually been committed, to make arrests and ensure convictions.

Now why doesn't it surprise me that you think this way....

Dammit Poe....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.