People selling their homes in Auckland appear to be dropping their asking prices to meet the softer market conditions, according to the latest data from property website Realestate.co.nz.

The average asking price (non-seasonally adjusted) for Auckland properties that were newly listed on Realestate.co.nz in April was $904,479.

That means the average asking price has declined by $48,270 (-5.1%) since March and is down by a whopping $91,822 (-9.2%) since February.

April's average asking price in Auckland was the lowest it has been since July 2017.

Average asking prices in April were also down compared to March in Bay of Plenty -2.6%, Central North Island -3.9%, Taranaki -4.6%, Wellington -4.1%, Marlborough -4.8%, West Coast -1.5%, Canterbury -3.1%, Otago -2.2%, Southland -4.7% and Central Otago-Lakes -13.7%.

Conversely, April's average asking price was up compared to March in Northland +1.0%, Coromandel +8.9%, Waikato +2.6%, Gisborne +8.7%, Hawkes Bay +5.5%, Manawatu/Whanganui +1.3%, Wairarapa +2.5% and Nelson/Bays +4.4%.

The national average asking price was $661,889 in April, down 4.3% compared to March.

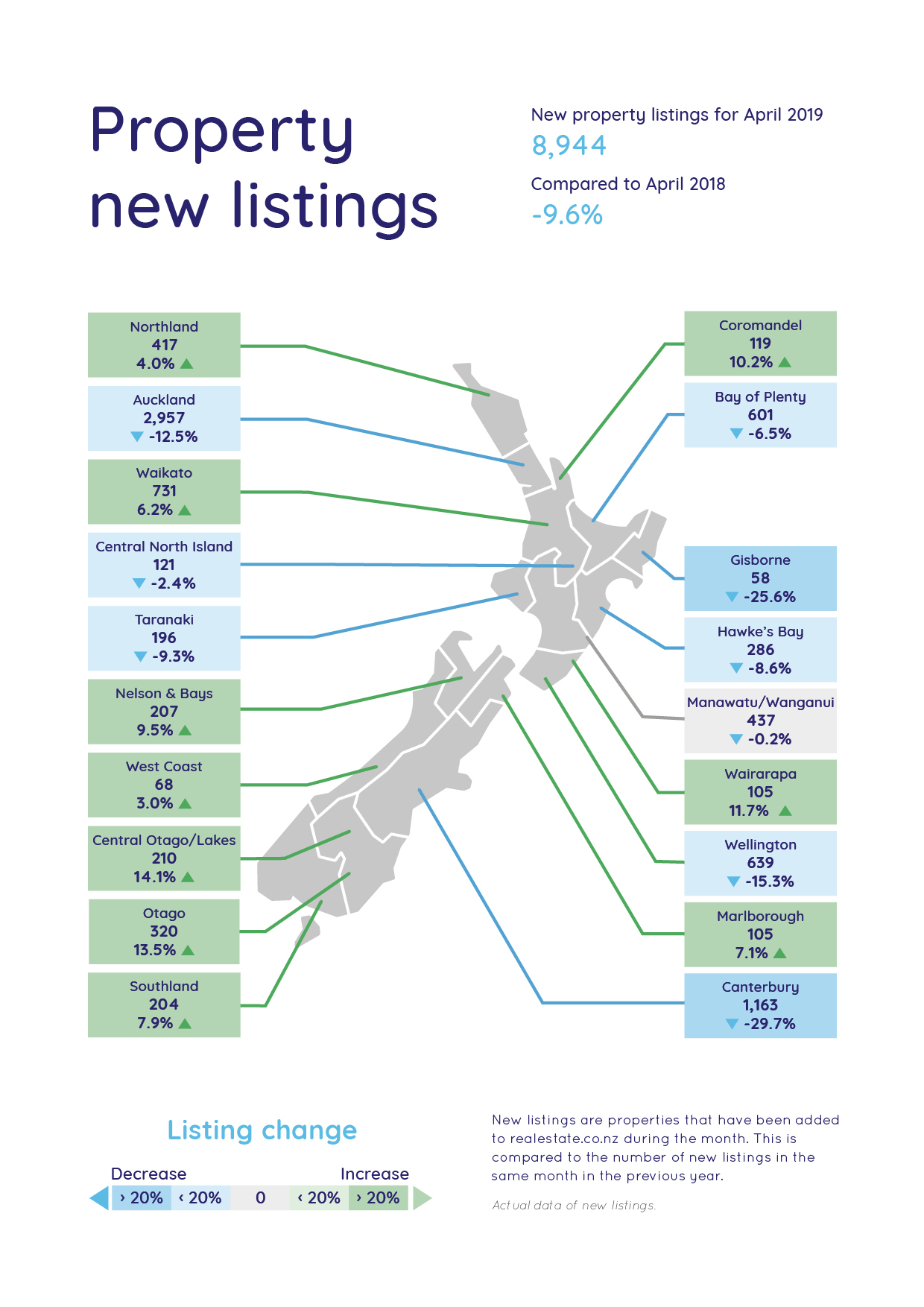

At the same time there was a drop in the number of new listings received by Realestate.co.nz in April, with total new listings down 9.6% compared to April last year.

There were more substantial drops in new listings compared to a year ago in Auckland -12.5%, Gisborne -25.6%, Wellington -15.3% and Canterbury -29.7% (see the chart below for the full regional breakdown).

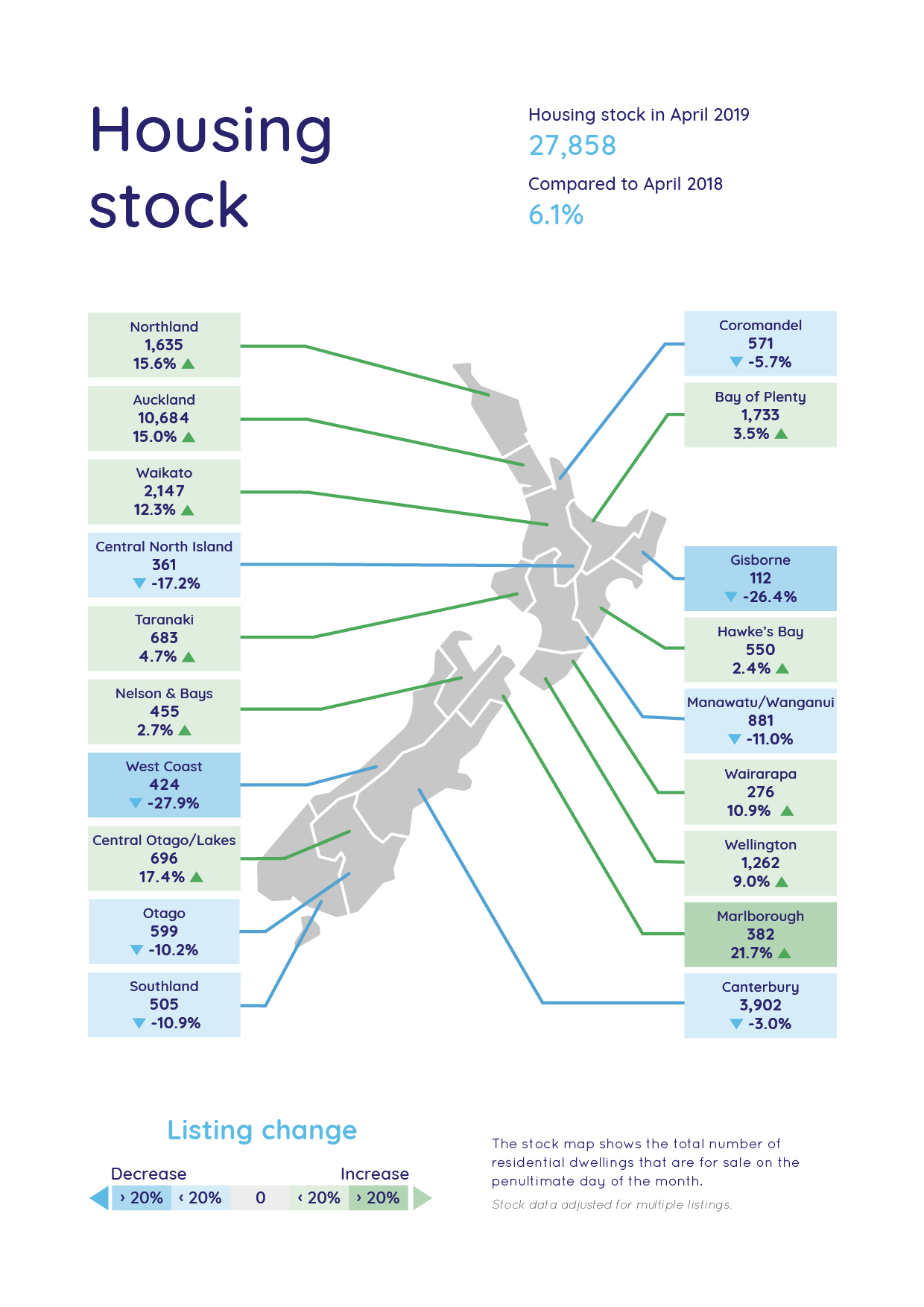

However even with the overall drop in new listings, the total amount of stock available for sale on Realestate.co.nz at the end of April was up 6.1% compared to a year earlier, while in Auckland total stock was up 15% and in Wellington it was up 9.0% (see chart below).

Those figures suggest the market is continuing to turn in buyers' favour as it heads towards winter, with prices easing and higher stock levels giving them more choice.

"We have left behind the frenetic market of 2014 to 2017 where asking prices spiralled dramatically upwards, largely underpinned by fierce competition and an increase in local and offshore investors," Realestate.co.nz spokesperson Vanessa Taylor said.

"We've now had two years of stable pricing with a dip in average asking prices in the Auckland region this year.

"New listings in the region fell in April and compounded with properties sitting on the market for longer, buyers aren't under the same purchase pressure.

"The current Auckland market is not the new normal, it's the old normal which was prior to 2014, when there was time to negotiate and ensure that if you sold your house, you also had your new home lined up.

"If you sell your house for less than CV, in this current market it's highly likely that the home you're purchasing will also sell for less than CV," Taylor said.

The comment stream on this story is now closed.

84 Comments

Is it any better reading if we consider median asking prices instead Greg?

Spruik that.

Lower asking prices, buyer's market. Good time to buy, get amongst it.

Hey wait a sec, the average asking price has declined $91,822 since the market peak, and I seem to remember you encouraging people to buy back when it was $0 to $25,000 down. I think this decline has got a way to go yet...

Despite my username, trying to time the market perfectly is a terrible strategy when it comes to property. Property is a long term game. Come back to me in 5 - 10 years time and lets see how much prices have risen since my buy recommendation.

DGM mentality: Market flat - don't buy, the crash is imminent. Market falling - don't buy, you'd be stupid to catch a falling knife. Market rising - don't buy, this ponzi scheme is unsustainable.

Usually I'd agree about timing the market, and NZ and Australia have had a great run, but we also have to recognise bubbles when they happen, because they can do a lot of damage. This is one. The market fundamentals have been right there to see, since it rose into the severely unaffordable range internationally.

I agree that overall (un)affordability, i.e. median multiple [https://www.interest.co.nz/property/house-price-income-multiples ], strongly indicates the AKL market has quite a way to fall. Hard to know what it's going to fall back to though - even if it only came back to around 7.5-8 that'd see the market falling another ~10%.

I think we need to assume it’ll finally fall back to within a “normal” range in world terms (shock, horror, we’re not different after all), so we should bargain on more than another 10%.

I'm not sure Auckland will get down below 5 ("severely unaffordable") anytime soon. Hard to know what the new "normal" is going to be. The world isn't the same as it was 30 years ago. Maybe Auckland settles in somewhere around 6.5, who knows. But that's more like a 25% drop from now, which could be pretty messy. I imagine the government would try to stretch that change out as long as possible.

I'm on the sidelines, cashed up, trying to wait this thing out. But trigger finger is getting itchy :-)

I'm in exactly the same boat. We went to about 30 open homes/auctions on the North Shore since the beginning of the year. What I saw was that sellers are still in the "denial" stage of the market crash. Made the decision to wait for another year at least. Remember, markets that go to high then go to low, so I'd like a couple of months of price rises before I commit.

GenerationXY, keep looking my friend. Honestly, you never know. I was also minded to just wait another year, and then happened upon the perfect house and got it $100k below the valuations (4.5% below the RV). The herd might still be in denial phase, but some sellers are capitulating, so just keep an eye out.

I have been pulling all the property listings on one of our large auction websites every day since last year, and this trend has been apparent for a while. Plenty of properties have been listed for 150+ days, and often go from being listed as "For Sale by Auction" to "Tender" to "Enquiries Above $x" over time. On many of these listings $x decreases every month or so, sometimes by eye watering amounts. Clearly there are some "motivated vendors" out there.

I spoke to an agent yesterday in Auckland who has an owner who has been topping up an interest only mortgage by $90 a week for the last 2 years, this potential client now wants to list, but is worried about doing so because he has a neighbour that has just reduced a very similar house, with a newer kitchen, to a level that is 115k less than my guy’s client bought his for in 2017. This is one of the reasons, beyond winter, that we will see listings rates slow down and people get stuck, for some they will carry on and just suffer the weekly losses, rather than take a bath on the capital hit in one go, negative or reduced equity to trade will trap many others.

Hi Joe, would be useful, n'est pas? if RE NZ could quite new listings per day figures for each month of year, with a back catalogue.

HC per day rate been declining since January. 7.5 pd to 5.4 pd is quite a big % drop. And its still going down

Indeed Mike. That and the rates of withdrawal.

In Christchurch houses are now selling not just below 2016 prices, but 2013 prices. The longer you wait, the more you will lose.

https://www.qv.co.nz/property/157a-ilam-road-ilam-christchurch-8041/228…

On the bright side he got to claim back about $6,000 off his taxes!

"The current Auckland market is not the new normal, it's the old normal which was prior to 2014, when there was time to negotiate and ensure that if you sold your house, you also had your new home lined up"

I believe the prices are slowly returning to the "old normal" levels prior to 2014 - 2017 buying frenzy.

I believe the prices are slowly returning to the "old normal" levels prior to 2014 - 2017 buying frenzy.

Which is not a big deal anyway, but the impacts on consumer spending will be the most important factor to watch. If it all turns to custard, that will be more critical than house prices.

No I think this one is going to be quite abnormal. Well normal in terms of a deflating bubble, but we haven't seen that in NZ for a long time. That's why we have to look to other parts of the world where it has happened, to see how it could unfold here. It's happening in Australia as well, a bit ahead of us.

Asking has fallen by approx 10% .

Houses from peak has fallen by 10% to 20% and many who bought in last few years and now planing to sell are selling at loss and some who are unable to hold and bought at rediculosly high price earlier are bleeding.

Any further fall from here on, will trigger unthinkable.....for many...

Dont worry there is more to come! that I can promise you!

Agent Tothepoint, what's your take on this? Are vendors somehow miss-reading your steady, oscillating, resilient market or are they practicing the gumption to deleverage now with equity in tow? More see the option of deleveraging now rather than after your predicted post 2021 "upswing". To be bluntly honest, it looks much less harmful on their finances. There's a growing selection of prime properties being discounted. Here's one such example; https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

Buyers are struggling to get finance. Cashed up buyers have vanished!

Here are the actual realised losses on eight North Shore properties bought and sold in the last two years. You'd have to add marketing, and conveyancing costs though. https://www.youtube.com/watch?v=A12eOT0ayBM

Just a blip. Ashley Church says the past mirrors the future and house prices double every 7-10 years. He's the honcho at a property group so he must know.

Just checking.... are you being ironic?

House prices double where every 7-10 years?

it does help if ones time scale pre-dates financialisation bubble printing from 2008 on and also goes back a little further than 1987. Yes there was history before then....

House prices go up because banks advance more debt (sorry, loans) as people stay in debt longer and therefore pay back MORE at a lower interest rate.

Not trying to be ironic, but perhaps being facetious.

Question - how is Church qualified to talk with authority on the housing market? From a bit of a google search he seems to have had a range of generic managerial/ CEO type roles. He doesn’t seem to be an economist. Not that economists talk much sense...

Does anyone know?

It's one of the great mysteries of our times.

Don't worry property investors, just follow the bitcoin holders and HODL

Hold on for dear life? probably a good idea. Ya know how the rollercoaster ride always starts with a long steep climb... what comes next? isn't it usually a vomit inducing (for some) plummet or corkscrew? :)

Investors don't need to sell if they can carry the current mortgage. Interest rates as low as 3.65% (and they WILL fall further). Rents skyrocketing (and they WILL shoot upwards and upwards more than anyone expects).

If you can explain the extent to which rents will rise, I for one would be interested. If you can't, I can assume you're trolling.

Immigration is into record number territory with the Dec-18 to Feb-19 (the most recent data points) being the highest seasonally adjusted months ever.

We are very likely to see rent increases.

Hi Unaha-closp

Did you know that between 2002 and 2007 Ireland saw very similar population growth (immigration) to the rate NZ has experienced in the last 5-6 years, even as they busted immigration continued to grow for years but the market tanked by up to 60% in some areas. Oz added 100k more people last month, and have been growing people rapidly over the last 18 months but still prices continue to fall. Few dollars a year more in rent doesn’t seem to be happening there, but capital values have been going backwards dramatically - it will be a less comfortable place for the later arrivals to the party and i’d Expect them to shout the loudest over the next few years. Personally I wouldn’t rely on immigration for this one, with Sydney and Melbourne deflating, Melbourne and Brisbane cheaper than Auckland on a median (average home for a family basis), and Welly more expensive than Brisbane too, the back door to Oz could become a temptation for some who might now qualify for a trip over the ditch. It’s often very difficult to arrest a falling market driven primarily by the credit impulse.

Joe, all true and yes I am aware. But unlike Dublin or Melbourne or Brisbane (or even Sydney) - Auckland has spent the preceding boom building 40-50% less homes per person than those cities. So what I am predicting is a short term increase in rents. Followed by a big problem.

I hate to burst your bubble on this one too but the ‘we’ve not been building enough’ is also a myth well spruiked by the mainstream. Building consents have been running at over half that of Sydney and Melbourne for several years now. The relevance being that Auckland’s population is only 1/3 the size those cities. The chief economist of Auckland City Council provided the information on this at 11 minutes into this post.

https://youtu.be/NhcSnscqQZk?list=PLtOkGwwIgTJGsFbpttce0Bj3wWQAAh9RE

Joe, I follow DFA and you have strange ideas on Auckland housing supply. Look at the left hand side of the graph shown at the 11 minute mark, it is indexed to 2002 and therefore does not show an absolute number of consents. The graph shows Auckland is lagging miserably behind on building. (Actually the graph hides the true extent of Auckland's failure by indexing to 2002, if it were accurately adjusted for population it would look much worse.)

If you want good raw data this site (interest.co.nz) publishes consent numbers regularly and corelogic publishes similar data for Aussie.

Good point. The Auckland housing consents over the past 20 or so years is effectively an Inverted Bell Curve, but population growth is consistently plotted upwards at a 45 degree angle during that same period.

Dp

Immigrants with decent incomes? Or immigrants (often being exploited) with low incomes? One group might push up rents, the other group will just push up overcrowding levels.

Exactly. Much of our 'immigrants' are students or low skilled workers. Unlikely to push rents up too much.

Mind you, don't dispute the notion that ongoing high levels of immigration will put 'some' upward pressure on rents.

Something has to give with aggregate population pressures.

Bit of both. We have low unemployment and immigrants have higher workforce participation than NZers.

Certainly there is some upwards pressure on rents (immigration, tax changes, etc). But there will also be downwards pressure as the market falls because savvy investors will be able to buy cheaply to (re)enter the market. Those investors will be able to undercut others who have previously paid higher prices for their rental properties.

Momentum.

Well let's apply some Hoskingesque "common sense". If house prices fall at current IRs and rents, the ROI should improve, right? Therefore, there is no need for rents to rise. I haven't accounted for "momentum", but keeping it simple.

Keeping it simple, stupid just like the Hosk and the Church

From an Agent: sellers drop prices because Agents tell them response is no good and market has moved down.

Also, please note 35% roughly of property on RE NZ is OTM over 90 days already and gets virtually ZERO attention from buyers. In addition, around a quarter of what is listed as a "house or apartment" is NOT. it is in fact a blank piece of land with option to build on. Not really accurate description then is it? Also, endless repetition of nonsense about a buyer market - please cease. Buyers are delaying or waiting for price falls. Hence, sellers and buyers going down in number due to lack of confidence. This is a deflationary mindset and is why people are constantly trying to deny realist, because admitting the truth entails stopping rhetorical non thought out mantras about all being fine. The market in Auckland is OVER stocked with stuff a lot of people do not want or cannot afford, or both. The market is still overpriced and will be for a while (2 years minimum). RE NZ is in fact admitting that real prices, those that people are asking for right now, are down 9% in 2 months. So much for the idea that Auckland prices cannot fall.

On the weekend I went to the first open home of a property on my street that had just listed - there was only one other person who turned up. I didnt count because I was just a nosy neighbour. And who knows, maybe the other person was as well. Even the recently listed properties are getting no attention. And this was a property in the sub $400k mark too.

Greg, the website's own report shows slightly different numbers for the average asking price in Auckland ($899,916 vs the $904,479 you wrote). Is the difference due the inclusion of 'not newly listed' properties in the former figure?

Also, it might be worth mentioning the year-on-year price change:

"The region’s average asking price fell 4.5% to $899,916 compared to the prior month and 5.8% compared to the same month in 2018."

The price figures on their website are seasonally adjusted. We prefer to use the actual figures in our reports.

.

Repeat after me: Credit drives house prices. The RBNZ capital requirements are going to drive prices over the next 2 years as the big four rebalance their assets to better align with existing capital levels.

Why have reductions in the LVR not spurred lending? Banks don’t want to lend more.

Why are markets with housing shortages and increasing rents seeing price rises flatten or reverse and total properties on the market increase? Because banks don’t want to lend.

Everyone loves to claim a “building boom” in Australia caused prices to dive (ignoring that the uptick in building was largely only in Sydney). Yet prices are now falling across the country. Why? Because banks lending criteria changed.

Same thing is happening now in NZ.

True, but at a certain point you need credible borrowers.

comment of the day IMO

Yeah. It's true that cheap credit has driven up supply, but it only goes so far.

In Aus some are blaming the Hayne Commission for choking credit by spooking the banks

--as if you are not, inevitably, going to reach a point some day when people simply cannot afford the credit being offered.

Without any intervention, how long would it have taken?

Would mortgages have been pushed out to 40, 50 years to finance 20x income prices? Life-long debt peonage as a perfectly reasonable, middle-class way of life?

As someone who is quite new to the world of finance, the stupidity of some public commentary seems mind-boggling.

For argument sake : house price may or may not fall but one thing is defenite that are not going up in near future so is a dead market unless rental income is attractive to investment, which may be possible in regeions but defenitelly not in Auckland.

Now the reality : House price will fall and by how much can be debated. Already 10% to 15% down in Auckland in many area ( and in some places in Auckland upt to 25% down ) and if it goes another 10% to 20% from here, will be blood bath for many speculators and so called investors (Unless are able to hold for for few years ).

Few are still in denials about the downward trend. Fooling themselves. If they are investors and believe that market may turn upside anytime soon - Good Luck to Them along with our sympathy.

During the top of the boom the Herald had articles every week about 20-something year olds with impressive property portfolios who built their 'empire' on debt. I wonder if we will be getting the same coverage of these speculators as they go into negative equity, then bankruptcy during the next few years.

That's an edition of the herald I would buy

Losses are magnified too. A 50% reduction in price reverses a previous doubling. 33% down wipes out a previous 50% gain.

Seems like an appropriate story to post this chart again.

Akl residential listings since Jan.

{kind=link}

Well done for keeping tabs on that.

As I read this article, the radio in the back ground is playing Peter Gabriel's Don't Give up.. and it goes

Don't give up

'Cause you have homes

Don't give up

You're not beaten yet

Don't give up

I know you can make it good

Though I saw it all around

Never thought I could be affected

Thought that we'd be the last to go

It is so strange the way things turn

Drove the night toward my house

The place that I was bought, on the lakeside

As daylight broke, I saw the sign

For sale signs had popped up all around

Don't give up

'Cause you have homes...

Beautiful

Where are our resident spruikers?

What are their views?

This is the most pleasurable page on the internet right now. Such enjoyment.

How on earth Realestate.co. can state that asking prices of houses has dropped is very hard to fathom.

When so many properties are by negotiation, deadline sale or auction, it is impossible to be accurate as to asking prices!

Pure guesswork at best!

No, they have to have a hidden price in the background so the search feature works properly. Otherwise people searching for $600k houses would get swamped with $1m+ properties. Thats how they know the asking price.

I can confirm that.

Indeed. To avoid having to converse with a dropkick real estate agent one may just narrow the price bracketing until their top secret little number is revealed.

It's quite strange that in New Zealand the price of something for sale is a closely guarded secret. That and real estate agents thinking that their egotistical mugshot is some kind of promotional material.

Except for those scum real estate agents who put a house in the $1.2m-$1.3m search range, tell you to your face at the open that they're wanting something in the $1.2's, then you go to auction and bid only to find out the vendors want $1.6m. Underquoting is illegal in Australia, it should be here as well.

There's one like that in my watchlist. Came up in a search with the max price set to $800k, it was an auction so no price indication.. Then when it failed to sell at auction it got thrown on the market for $930k. Why bother advertising it in the $800k buyer range when clearly the seller is not going to accept anything close to $800k.

Same happens in Wellington. I saw a house in the 1.5-1.7 mil bracket on trademe. Its late 2018 RV was $1.55 million and when I called to arrange a viewing, I was told they sellers wanted mid to upper 2 million something!!!!???? The house has sat on the market since November 2018. They had it go to tender initially, and got nowhere near what they wanted so put it back up for sale by negotiation. So they are also in denial about what the market consider fair value for the property, as well as using shady search function tactics.

So,in other words, not accurate at all in regards to asking prices!!

Unless there is a marketed price it is not accurate!

Last year houses were going near around asking or may be 2 to 3 % lower but now when the asking itself is 10% lower and houses are going 5%to 10% plus lower than the asking indicates that the house is much lower than 10% fall in asking.

If the fall between Feb to April surprises few, wait till July and all FHB, who have controlled with their buying decession will be most happy.

Though writing is on the wall but still Wait and Watch.

Notice how the AKLD asking prices are plummeting but the median and average are dropping only slowly?

Thats because those properties still cant sell !!!!

Brace yourselves we've run out of fuel at 20,000 feet...........................

Matter of time ......

Yeah, vendors are getting real , like this one for instance

219 Gills Road, Albany

Enquiries Over $1,950,000 (2019-05-01)

$2,350,000 (2019-04-12)

$2,850,000 (2019-02-14)

Offers over $2,950,000 (2019-01-25)

SOLD!

.

Wow, what a difference 90 odd days make.

1/ coniston Avenue bought in 2015 for 771, now sold for 700

"House prices never go backwards, NZ is different to everywhere else."

"Well, they're not really going backwards, just a few cheaper houses have sold which has brought down the median."

"Look, it has only gone down 0.5%. Now is a great time to buy."

"I can't see it going down as much as 5%. It will start to recover during the March buying frenzy."

"The data must be wrong, it appears to be continuing to go backwards."

More to come......

Wheeze OK, Wheeze OK....take deep breaths...Wheeze not like other Countries, we can borrow to the cows come home and the chickens come home to roost. Them foreign buyers got nuffin on us.....we can dig deep, our pockets is deep......now where is my inhaler.? Just borrow...oh that was an a Methamphetamine kick......hope it don't get into our Water......I heard a rumour it already has.....rumour must be spreading....Wheeze OK.....weeeeeeeeee.

Please remember it is Friday......and I am a realist...not a dreamer.....I do however think there is an addiction to many things...these days.....the waters will need testing, frequently.....but heavily borrowed munny....never. Wheeeeeeeeeeeze OK.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.