Central banks such as the Reserve Bank of New Zealand (RBNZ) posting losses doesn't matter in the way it does when commercial banks record losses, according to the Bank for International Settlements (BIS). Instead BIS says a central bank’s credibility depends on its ability to achieve its mandates and losses don't jeopardise that ability, and are in fact sometimes needed to achieve those aims.

BIS, the Basel, Switzerland-based central banks' bank, makes this argument in a new Bulletin article written by five of its staff.

"While central bank losses will affect the consolidated public finances, serving as a source of revenue for governments is not the purpose of a central bank: they exist to fulfil their policy mandates, including price and financial stability. Thus, the success of their interventions should always be judged on whether they fulfil these mandates. Unlike commercial banks, central banks do not seek profits, cannot be insolvent in the conventional sense as they can, in principle, issue more currency to meet domestic currency obligations, and face no regulatory capital minima precisely because of their unique purpose," BIS says.

The RBNZ posted an $86 million deficit for its June 2022 financial year. It attributed this to unrealised mark-to-market fair value losses of $335 million, largely on the RBNZ’s fixed-rate term loan facilities including the term lending facility established to support the Government's Business Finance Guarantee Scheme, and fixed-rate securities. The RBNZ also recognised unrealised losses on basis swaps as swap spreads returned to pre-Covid-19 levels, reversing the unrealised gains of the previous year. That followed a $107 million deficit in 2021. In the June 2020 and 2019 years the RBNZ posted surpluses of $371 million and $243 million.

BIS points out that central banks that have already announced losses related to asset purchase programmes undertaken with the aim of helping meet their mandates, include the Reserve Bank of Australia, National Bank of Belgium, Bank of England, Bank of Japan, Netherlands Bank, RBNZ, Sveriges Riksbank and the US Federal Reserve. The RBNZ undertook its large scale asset purchase programme in 2020-21 buying almost $53 billion worth of government and local government bonds off banks with the aim of lowering borrowing costs to households and businesses by injecting money into the economy.

BIS notes central banks are protected from court-ordered bankruptcy and are indirectly backed by public money.

"These provisions allow central banks to successfully operate without capital and withstand extended periods of losses and negative equity. History clearly illustrates this. Several central banks had negative equity yet fully met their objectives – for example, the central banks of Chile, Czechia, Israel and Mexico experienced years of negative capital. Between 2002 and 2021, some 10 out of 32 emerging market economy/small open economy central banks had negative equity, only briefly in many cases, but for more than 30% of the time for three of them. But throughout, financial and price stability were maintained," BIS says.

"There can be, however, exceptional situations where misperceptions and political economy dynamics can interact with losses to compromise the central bank’s standing. If there is macroeconomic mismanagement and the state lacks credibility, losses may erode the central bank’s standing, which may jeopardise its independence and could even lead to the currency’s collapse. The central bank’s credibility could also be at risk if it lacks sufficient resources to fund its operating needs, such as future earning capacity or government recapitalisation without conditional political influence."

Missing inflation targets

Like many other inflation targeting central banks the RBNZ has been battling inflation above its target range since 2021. The RBNZ is tasked with; "keeping future annual inflation between 1% and 3% over the medium term, with a focus on keeping future inflation near the 2% midpoint." Statistics NZ's latest consumers price index came in at 7.2% for the year to December.

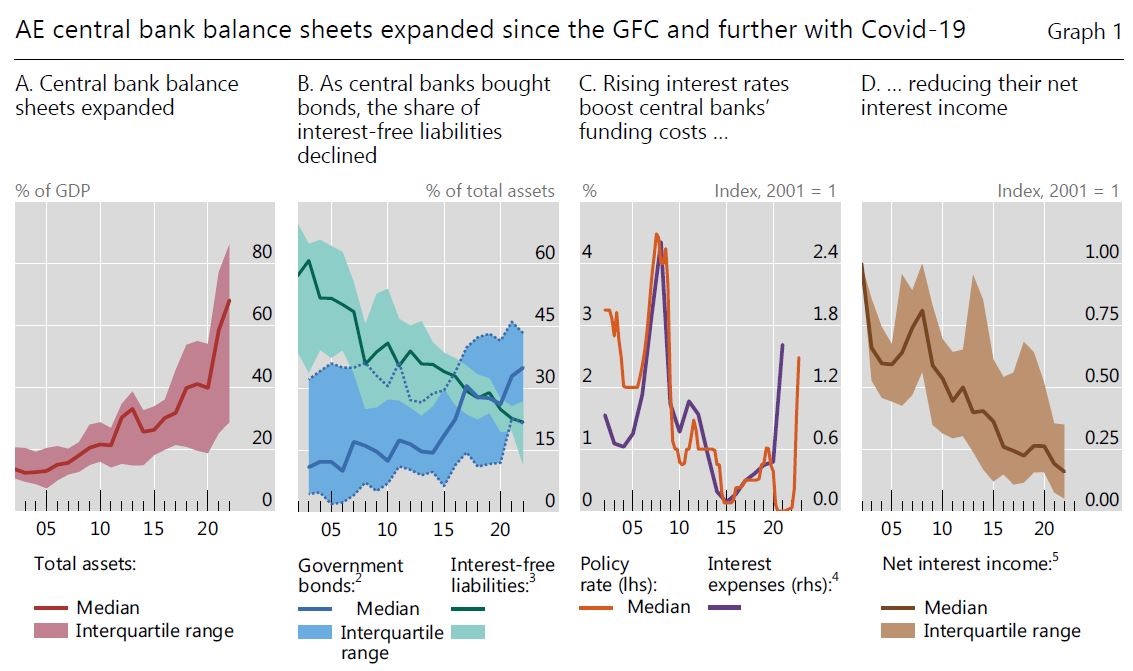

BIS says rising interest rates are reducing profits or even leading to losses at some central banks, especially those that purchased domestic currency assets for macroeconomic and financial stability objectives.

"Central banks have increasingly deployed their balance sheets in recent decades as a tool to pursue macroeconomic and financial stability objectives in support of their economies. After the Great Financial Crisis, some advanced economy central banks used asset purchase programmes or other lending programmes to achieve their policy aims [such as the Federal Reserve]. Others introduced such programmes during the Covid-19 pandemic [such as the RBNZ]. These were funded mainly through interest-bearing commercial bank reserves, resulting in a declining share of interest-free liabilities. In doing so and to pursue their policy objectives, central banks took financial positions, which influence their profits and losses as a by-product," BIS explains.

"When central banks increase interest rates to curb inflation, their net interest income declines, since a large portion of their liabilities is linked to policy rates. Asset valuations also decline with rising bond yields, putting further pressure on profitability for central banks using an accounting treatment that recognises changes in market values in calculating net profits. Reflecting these dynamics, some central banks have recently reported losses, and more are expected to follow. In some cases and depending on accounting approaches, losses are sizeable and can result in negative equity."

The RBNZ has typically paid an annual dividend to the Crown with these reaching $510 million in 2015 and $430 million in 2018. However no dividend was paid last year or in 2020.

Financial independence part of 'need for independence'

BIS says a central bank’s balance sheet position, composition and inherent risk exposures affect its income.

"Its reported 'accounting income' is calculated by applying the relevant accounting approaches. From there, rules for profit distribution to the fiscal authority are implemented. A typical central bank holds foreign and domestic currency securities on the asset side of its balance sheet, funded largely with banknotes in circulation and commercial bank reserves. Traditionally, a central bank’s primary source of income is 'seigniorage,' the net income earned on assets funded through currency issuance, a non-interest-bearing liability. But income can also be driven by the impact of interest, market yield and exchange rate fluctuations on net interest income and asset valuations... The increasing use of asset purchase programmes by many advanced economy central banks has raised government bonds as a share of assets. Correspondingly, the commercial bank reserves used to fund these asset purchase programmes have come to dominate central banks’ liabilities."

"To conclude, a central bank’s credibility depends on its ability to achieve its mandates. Losses do not jeopardise that ability and are sometimes the price to pay for achieving those aims. To maintain the public’s trust and to preserve central bank legitimacy now and in the long run, stakeholders should appreciate that central banks’ policy mandates come before profits," says BIS.

"Central banks are public institutions, but there is broad consensus on the need for their independence to pursue price and financial stability mandates without interference from governments, whose priorities can conflict with those mandates. Achieving that independence has multiple dimensions, with a wide range of degrees and models across jurisdictions. Financial independence - when a central bank has sufficient operational and financial resources to fulfil its mandate without influence - is one of these dimensions."

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

8 Comments

More spin in the same vein, this time from the BIS head. He is right the goal isn’t to make profits, but that is just distraction designed to avoid accountability for large losses and whether the risk assumed was ever warranted or even ex ante analysed. Link

Like many other inflation targeting central banks the RBNZ has been battling inflation above its target range since 2021. The RBNZ is tasked with; "keeping future annual inflation between 1% and 3% over the medium term, with a focus on keeping future inflation near the 2% midpoint." Statistics NZ's latest consumers price index came in at 7.2% for the year to December.

Deep macro insights: you ready? Powell: I got inflation wrong for 2 years but now I see disinflation ahead. Market: woooaaaa the guy said inflation down buy buy max bidding. Link

So what do we do when we have big losses and central banks that act in defiance of their mandate?

why do we accept a target inflation rate of 2%. it is theft of the future by fiscal irresponsibility... 2% inflation is just the same of 7% or 15%. the only difference is that it appears benign for longer. eventually they all go parabolic.

we lost our way in 1970 when we allowed currencies to unpeg from gold. since then we have lived in a compounding inflation environment from which there is only one way out.

why can't people see that deflation is good for them. things should cost less as manufacturing costs decline. this need for constant growth is only required because we have constant inflation. however deflation is off the table now as we have too much debt. deflation eats debtors...

people will say that the great depression was deflationary and look what misery occurred then. the big issue was central banks and governments got in the way of the correction and turned a short term crash into a 15 year feed back loop.

the opposite was tried in 2000. we had a bubble in stocks and to prevent losses we blew a bubble in housing and to prevent losses we blew a bubble in everything. what is next? eventually you run out of bubbles to blow.

the narrative is how badly the boomers have managed things... when in reality all we have done is reacted to the environment. the environment has not been a free market for more than 20 years... so you can't complain when people do what they can to survive.

sadly there is no happy path.... we missed our chance to prevent this 30 years ago. none of our governments were prepared to tell the people the truth as they can't get or stay elected if the do and that is all a politician really cares about

A post of good thoughts. The question of 'why is deflation bad' is smart. Reality is that if the value of your labour is increasing and your currency is increasing in purchasing power, this is positive.

Love it, hate it, or agnostic about its existence, the ol' rat poison came into existence as an antidote to the continuous manipulation of money. Do people really believe we can just expand the money supply forever without any consequences? We're at the point now where it's becoming clear whether or not the financial industries can deliver on pensions for the boomers. And the central banks will need to act accordingly. In many ways, it's entirely predictable.

Banks. Banks are given the right to print money, so that they can lend into the economy. Without them lending, they make no money and they are the sacred cows in the inflation spiral. Our leaders and financial kingpins come from banks and go to banks when finished in government As such the banking lobby and hence support for a debt based economy, is by far the most powerful driver in government policy. The creation of money by the banks is inflation. Once addicted to a debt based economy, the RBNZ tries to moderate it it to 2%, but the unpalatable reality is it cannot stop. This is why in times of angst such as covid, everything is done to keep money flowing, 64 billion was printed as a result of covid to keep the lead boat from sinking. The economy cannot tread water on zero inflation, we either have inflation or we sink to the bottom of the global sea.

Personally I would love to see zero inflation and the associated mega crash that it would bring. The system is unsustainable as is and as such a cleanse gives the opportunity to build back better and more sustainably.. But this is a global system and we will not be able to go there without everyone else going there too. But like all unsustainable systems, it will happen at some stage and the longer we kick it down the road the bigger the disaster will be.

Notwithstanding folk advocating against more equitable taxation of earned/unearned income, to one point.

But in the rest, yeah. We need to start factoring in our Reserve Bank and govt sector management of these market matters into our broader looking at and discussion of wealth transfers and welfare. At the moment they're too disconnected.

For example, it makes zero sense for people to screech about the poor receiving a paltry increase while via monetary intervention we've transferred far more in handouts to asset owners. It smacks of being unaware.

great question to ask. some of the losses is from central banks take over toxic assets from the commercial banks, governments or the public. the real challenge for central banks would be the ability to fulfill its international payments I'd say. If this has issues, central banks will go bankrupt.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.