Key officials have acknowledged that profits have been a major source of inflation in Europe – a realistic position informed by facts, rather than by the economics of the 1970s. Now that they have embraced a new analysis of what’s driving inflation, the policy response should change, too.

In recent months, the European Central Bank, the OECD, the Bank for International Settlements (BIS), and the European Commission have all published studies showing that profits have accounted for a large share of inflation. But the coup de grâce for doubters came on June 26, when the International Monetary Fund tweeted: “Rising corporate profits were the largest contributor to Europe’s inflation over the past two years as companies increased prices by more than the spiking costs of imported energy.”

What took so long? As ECB President Christine Lagarde told the European Parliament on June 5, “the contribution of profits to inflation … had gone a little bit missing,” because “we don’t have as much and as good data on profit as we do on wages.” Policymakers failed fully to appreciate the “transmission of the cost-push that was suffered by many corporate sectors into final prices.” But now, the problem has come clearly into view. While some sectors “have taken advantage to push costs through entirely without squeezing margins,” Lagarde explained, others have gone further to “push prices higher than just the cost push.”

Firms have been able to hike prices for two reasons according to Lagarde: mismatches of supply and demand where bottlenecks have prevailed; and the coordinating effect produced by recent mega-shocks. As Lagarde put it: “everybody is in the same position, we are all going to increase prices.”

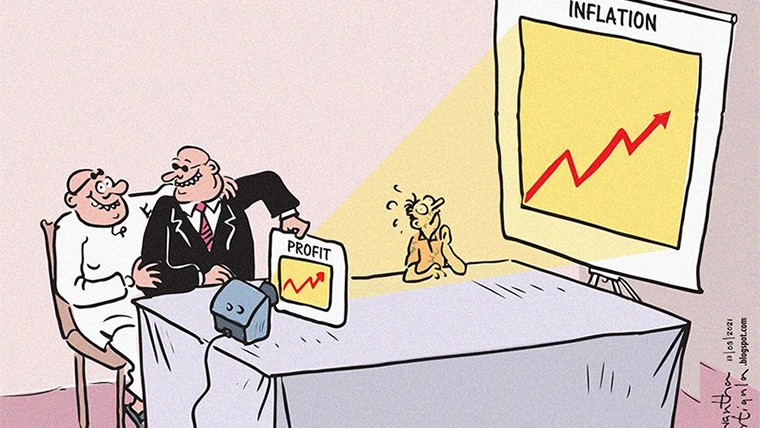

This “sellers’ inflation” happens when the corporate sector manages to pass on a major cost shock to consumers by increasing prices to protect or enhance its profit margins. Of course, not all firms have won equally. The bottom line is that sellers’ inflation results in an increase in total profits. The same simple truth led Adam Smith to warn, 250 years ago, that profits can drive price pressures.

Some may counter that protecting margins against cost shocks is normal corporate behavior, leaving no reason to rethink today’s inflation. But no one denies that firms aim to protect or even expand their margins (hence, “greedflation” is a misnomer). Rather, the point is that, by historical standards, firms today have been spectacularly successful at doing so. Isabel Schnabel has pioneered this kind of inflation analysis at the ECB, and when she was recently asked whether today’s inflation was really driven by profits, she did not mince her words: “If you do the macro decomposition, part [of inflation] is driven by profits, full stop. It’s a fact.”

Consider the comparison with the first oil price shock in 1973. Back then, as the IMF shows, it was labour that managed to protect itself and fend off the shock; beyond oil itself, the increase in prices was almost exclusively driven by rising unit labour costs, and profits fell. Today, by contrast, the IMF finds that profits account for 40% of inflation and, along with import prices, have replaced labour costs as the main driver. Moreover, as the BIS confirms, real wages have fallen more than they did in past inflation episodes. “Workers have so far lost out from the inflation shock, … which is triggering a sustained wage ‘catch-up’ process,” explains Lagarde.

Where are the ECB, the IMF, the BIS, and other leading institutions getting these ideas? They certainly do not come from old assumptions based on the Phillips curve, output gaps, and monetary easing. Perhaps my own widely covered work played some role, or people are simply taking a fresh look at the facts.

Whatever the case may be, it helps little to get the diagnosis right if the therapy remains ineffective or even harmful. As matters stand, the standard prescription for addressing inflation is still to hike interest rates, even though doing so implies higher unemployment and heightens the risk of recession and financial instability. The IMF suggests that, “Europe’s inflation outlook depends on how corporate profits absorb wage gains.” But there is no direct channel from rising interest rates to margin compression. An increase in borrowing costs has already increased financial risks and, if anything, reduces firms’ ability to absorb wage increases.

As some Wall Street analysts have observed, “price over volume” is now a widespread corporate strategy. Instead of lowering prices and boosting volume, many companies are making up for lower volume by boosting prices; in this environment, targeting lower demand is unlikely to halt inflation.

Large corporations have learned that they do not have to pick up the bill for big cost shocks like the pandemic or Russia’s war in Ukraine. Nor do they even have to adapt. Like big banks during the 2008 financial crisis, they have been folded into the culture of bailouts and buck-passing. But such behavior will not make the economy more resilient. We should recognise the recourse to higher interest rates for what it is: a strategy to dump the costs of inflation on to labour (by suppressing wages), on to social programs (through austerity), and on to future generations (by discouraging investment).

Gita Gopinath, the IMF’s deputy managing director, was certainly right last month when she argued that, “If inflation is to fall quickly, firms must allow their profit margins … to decline.” But achieving that outcome requires a new strategy aimed at disciplining runaway profits, incentivising investment, increasing productivity, and encouraging firms to make money the old-fashioned way: by selling more products at fair prices.

British Prime Minister Margaret Thatcher famously declared that “there is no alternative” to the unfettered market economy. In fact, the past year has taught policymakers that there are many alternatives. In Spain, for example, a creative all-of-the-above approach has yielded an inflation rate lower than the ECB target while the growth in unit profits was more in line with unit labour costs than in other OECD countries; and in the United States, oil released from the Strategic Petroleum Reserve helped counter inflationary pressures.

Getting the analysis right is a crucial first step. The technical economists and the political leaders at international and European institutions must now follow through with the other foot. We need policies that follow from their new understanding. Short of that, it would be safer to pause rate hikes and do nothing than to launch yet another round of monetary tightening. Sometimes taking a step back is the best way to move forward.

*Isabella M. Weber, Assistant Professor of Economics at the University of Massachusetts Amherst, is the author of How China Escaped Shock Therapy: The Market Reform Debate (Routledge, 2021). Copyright: Project Syndicate, 2023, published here with permission.

12 Comments

Sellers will price at the maximum the market can bear. The only effective counter is an open market or for the government to become a supplier and constrain pricing.

See also: why richlisters in New Zealand own supermarkets

or are trying to unload them

That's the building. It was in the news somewhere as recently developed.

Every company wants better profits margins every quarter for the similar product. Where does this end?

The loaf of bread has not changed in 100 years but it's now costs $10 rather than cents.

Humans are a dumb species, we call ourselves intelligent..

And the biggest contributor to profit led inflation in NZ is the Govt owned Air New Zealand. I don't see the Labour Govt doing anything about reducing Air New Zealand's obscene profits, and passing on lower ticket prices to New Zealanders.

"We should recognise the recourse to higher interest rates for what it is: a strategy to dump the costs of inflation on to labour (by suppressing wages), on to social programs (through austerity), and on to future generations (by discouraging investment)."

Which is why our whole wrong-headed neoliberal monetary policy set by an 'independent' body needs to be tossed out.

And setting monetary policy returned to politicians to use in an integrated fashion along with fiscal policy.

What has also changed is the cost of manufacturing, in China and similar countries. So you have widgets costing $5 to manufacture, ending up retailing at $50. If that cost goes up to $6, does it justify rating the retail to $60?

When governments throw money around like confetti and central banks lower interest rates to the lowest levels ever (inducing an asset bubble) consumers go crazy with their spending. Too much money chasing supply chain constrained goods means sellers can increase their prices. It's a two sided equation. High interest rates and flat GDP growth will see the the ship right itself but it will be 2-3 years of pain. You can't drink champagne all day and not expect a hangover the next.

Spot-on!

The free market has been the basis of wealth in all developed countries. It is only academics with no practical experience, like the Greens, who believe the basis of wealth is to take it from those who work hard and succeed, and give it to those who are not motivated.

Isn't that what PAYE does? No thresholds though , off every single dollar we earn.

Foxes caught in chicken coop blame hens for laying too many delicious eggs.

The cause of inflation is definitely not related to central bankers printing money, say central bankers. It is in fact caused by excessive profit taking of companies extracting massive profits from the market, say central bankers. Where this money came from that allowed businesses to extract massive profits from the market is completely irrelevant, say central bankers.

Absolutely no need for central bankers to take any blame - yolk dripping from their mouths.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.