By Girol Karacaoglu*

“I’ve asked numerous Fed policy decision makers a basic question over the years: do central bankers believe in price controls? Do they think that the government can, for instance, set the price for automobiles? The answer, of course, is no – to which I’ve asked a follow-up. When the Fed sets interest rates, aren’t they setting the most important price in the economy – the price of money? I’ve never gotten a credible answer.”[1]

The question I wish to address is this. Is there a choice of monetary policy tools, different from the Official Cash Rate (OCR), that can contribute to enhancing the effectiveness, efficiency, and equity (including intergenerational equity) of monetary policy outcomes? One that is better suited than the OCR, in a small open economy such as that of New Zealand, which is open to the international flow of goods and services, financial capital and people, and has adopted a flexible exchange rate regime to manage its currency.

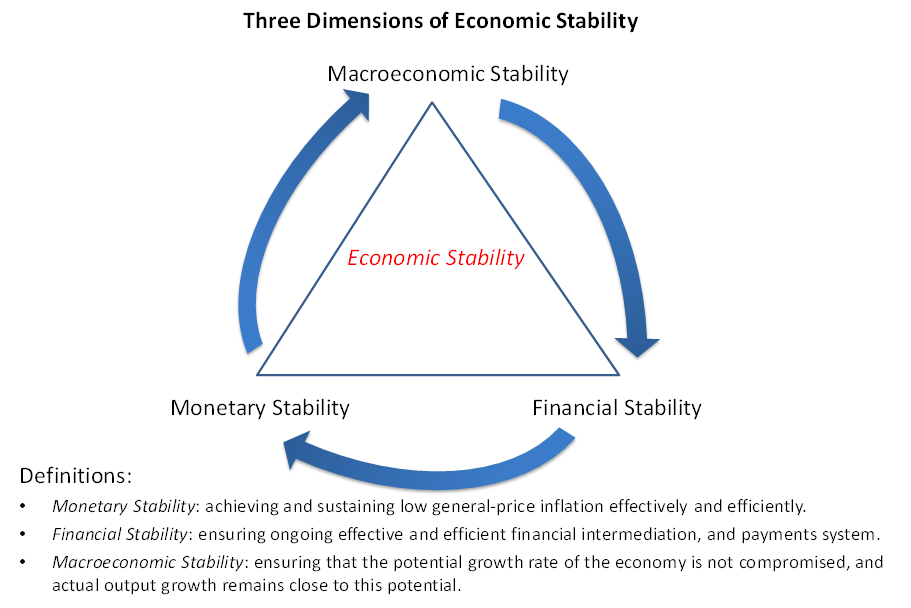

The problem with current monetary policy outcomes, certainly since the Global Financial Crisis of 2008/9, and as we saw during and following the Covid-19 pandemic as well, is that they lead to monetary, financial, and macroeconomic instability. The figure below explains what I mean by these terms.

Economic growth and prosperity are created primarily by “real” factors, such as the quality of political, economic, and social institutions; the quantity and the productivity of the workforce; the quantity and quality of the (human and physical) capital stock; the availability of land and natural resources; the state of technical knowledge; and the creativity and skills of entrepreneurs and managers.

Nevertheless, centuries of experience, as well as research, highlight the crucial supporting role that financial factors play in the economy. A well-functioning financial system helps an economy realise its potential. By contrast, as the experience of the last few decades amply demonstrated yet again, adverse financial conditions may not only prevent an economy from reaching its potential, but they can, and do, cause serious economic and social harm as well. At the core of these ‘adverse financial conditions’ is the combination of the excessive growth and misallocation of bank-created credit.

Real interest rates and exchange rates are two of the most important sets of relative prices for the functioning of a small open economy. By interfering with the operations of these relative prices, a price (interest rate) centred monetary policy risks creating a higher degree of monetary, financial, and macroeconomic instability – relative to a policy centred on quantity controls.

An alternative, quantity-centred, and fully integrated, monetary-cum-financial policy framework, which is less concerned about active demand-management, but exclusively focused on ensuring sustained low general-price inflation as well as financial stability, offers a better chance of underpinning all three forms of economic stability simultaneously.

My primary recipe towards achieving these three forms of stability simultaneously comprises:

- An ultimate target for general-price (goods, services, and assets) inflation of (say) 3%.

- An intermediate target of aggregate bank balance sheet growth aligned with a “sustainable” nominal GDP growth of (say) 5%.

- Monetary policy instruments comprising a suite of direct quantitative controls on the growth and composition of the banking system’s aggregate balance sheet.[2]

It is equally critical that the pursuit of economic stability, as summarised above, is done in a way that enhances the growth potential of the economy. A quantity centred set of policies, with minimal interference with the operation of the relative price mechanism, is also more conducive to achieving this particular aim.

New Zealand is well prepared and equipped to move towards a more “quantity centred” monetary-cum-financial policy framework. We have been actually groping towards it, with relatively recent explorations involving macro-prudential instruments, core funding ratio, and Basel III interventions.

Well-functioning financial system

A well-functioning financial system provides the following eight functions and services, in support of the (static as well as dynamic) efficient allocation of economic resources (including savings and capital in particular), across time, geographies, and industries – thus serving as a platform for high, sustainable, and equitable economic growth[3]:

- A common medium of exchange.

- Ways of clearing and settling payments to facilitate the exchange of goods, services, and assets.

- Liquidity – for individual entities and the financial system at large.

- Low and stable general-price inflation.

- Price information that helps co-ordinate decentralised decision-making in various sectors of the economy.

- A mechanism for the pooling of funds to undertake large-scale indivisible enterprise or for the subdividing of shares in enterprises to facilitate diversification.

- Ways to manage uncertainty and control risk.

- Ways to deal with the incentive problems when one party to a financial transaction has information that the other party does not (information asymmetry), or when one party is an agent for another.

Throughout modern history, the need for these financial functions has remained stable. On the other hand, across time and geographies, the institutional settings that have emerged to deliver these functions have been extremely varied. Unfortunately, none of these institutional arrangements have been uniformly and consistently successful in ensuring monetary and financial stability.

What are the common causes for the failures of the financial system in performing the above functions consistently well?

My answer to this question is based on a conceptual framework that is firmly grounded on the critical distinction between the monetary system and the financial system.

The monetary system is a subset of the financial system – indeed it represents the core of the broader financial system.

A well-functioning monetary system provides a common medium of exchange, efficient payments services, liquidity, and a stable general-price level – i.e., essentially the first four functions listed above.

Using a sound monetary system as a platform (necessary condition), the role of the broader financial system then is to provide efficient financial intermediation (i.e., the remaining four functions listed above) - in support of high, sustainable, and equitable economic growth.

All serious financial crises throughout modern history have been underpinned by a failure of the monetary system in the first instance.[4]

The core purpose of good financial regulation is to ensure a well-functioning monetary system. Supporting, complementary, regulation would then aim to further enhance the efficiency of financial intermediation.

Necessary conditions for monetary and financial stability

Unique role of banks[5]

The design of good financial regulation towards ensuring a well-functioning monetary system, requires an understanding of the unique role that banks (broadly defined to include ‘shadow banks’) play as part of the monetary system.

There are many types of institutions that provide financial intermediation services – including equity and debt markets. What is unique about “banks” per se (defined from a functional perspective), is that they provide, in addition to financial intermediation, the main component of the common medium of exchange (i.e., money) – part of their liabilities (demand deposits) serves as the medium of exchange[6]; they also provide payments services.

As part of their financial intermediation activities, banks:

- First, create money (“inside money”) through their lending activities.

- Second, transform short-term debt (i.e., deposits collected from savers or funds raised in wholesale markets) into long-term loans to households and businesses (“maturity transformation”).

It is the first of these activities that makes banks unique among financial intermediaries – and puts them at the heart of the monetary system. These two activities, in combination, when uncontrolled and carried to excess, can make them uniquely dangerous.

The central bank is the banks’ bank. The banking system is defined as the central bank plus all financial intermediaries that bank with the central bank. Collectively, these institutions provide the stock of money in circulation – their liabilities are what we use as the medium of exchange (i.e., money). Most of money creation occurs through the lending activities of banks (“inside money”). And it is direct access to central bank (high powered) money, under prescribed conditions, that places the banks in a central position in the provision of liquidity for the financial system at large.

Ensuring a well-functioning monetary system.

What outcomes should we aim for?

Good financial regulation, aimed at achieving a well-functioning monetary system, should aspire to the following outcomes – which can be jointly defined as “monetary and financial stability”:

- Ensuring low and stable general-price inflation.

- Minimising the likelihood of bank failures.

- Minimising the (economic, financial, and social) damage caused by bank failures, should they occur.

What should we control?

Root causes of monetary and financial instability have always had four closely related ingredients in common:

- Excessive growth in money and credit.

- Misallocation of credit.

- Excessive risk taking (incl. excessive “maturity transformation”).

- Misaligned relative prices (incl. inter-temporal prices – i.e., real interest rates and exchange rates).

The intersection set between the range of policies that will help achieve monetary and financial stability, is the set that will control the growth and composition of the aggregate balance sheet of the banking system.

We must control aggregate bank-balance-sheet growth, as well as its composition, and the degree of mismatch between the maturity of banks’ assets and liabilities.

The growth of the banking system’s aggregate balance sheet should be aligned with the long-run growth target for nominal GDP - the sum of the potential real growth of the economy and a modest inflation target.

Separate, but complementary, policies would further aim to reduce the incentives for excessive risk taking and ensure that all material consequences of risk taking are internalised (or privatised).

Three aspects of the regulatory environment, over the past two decades at least, have sowed the seeds for both monetary and financial instability – as well as gross inequity.

- First, excessive growth in the aggregate balance sheet of the banking system, underpinned by artificially low official (central bank) interest rates.

- Second, the misallocation of that credit, in favour of real estate.

- Third, an implicit or explicit underwriting of the risks taken on by the banking system, by the government (on behalf of taxpayers).

One of Rajan’s[7] conclusions is that the 2008-09 global financial crisis was partly a consequence of the short-sighted political response to growing income inequality in the US. A populist credit expansion policy, underpinned by excessively low official interest rates, allowed people, but only temporarily, to enjoy consumption possibilities (including home ownership) that their incomes could not have supported on a sustainable basis – eventually leading to the financial crisis which caused pain all around the world when interest rates started rising again.

In addition to inequities, excessively low interest rates also sow the seeds of financial instability by directing the excessive credit created by the banking system to the wrong types of investments (such as real estate) – what Austrian School economists refer to as ‘mal-investment’.

And when excessive banking system balance sheet growth supports long-term lending funded by short-term deposits or wholesale-market borrowing, the financial system at large becomes vulnerable to severe liquidity (and eventually solvency) crises.

How can we implement these controls effectively and efficiently?

It is essential to implement such controls effectively and efficiently so that the financial system’s most productive contribution, that is efficient financial intermediation (while controlling for the significant negative externalities associated with excessive lending to real estate and consumer finance), is not compromised. This requires minimum interference with the relative-price mechanism, once adequate controls (through appropriate capital and other quantitative restrictions on the aggregate growth and allocation of bank credit) are in place. These risk weights imposed on the composition of the banking system’s aggregate balance sheet would reflect macroeconomic and social risks, not the private risks faced by banks.

Price movements (when they are free from interference) are the most important information sources we have in guiding resources to their various forms of deployment across geographies, industries, and time. As Hayek[8] argued compellingly eighty years ago, only market prices can aggregate knowledge that is dispersed among millions of people and not given to any one person or a small group of people in its entirety.

Keeping this in mind, we should target aggregate (consumer- and asset-price) inflation for monetary stability – not just consumer-price inflation. Inflation control is a means to an end (strong, sustainable, and equitable economic growth) – and not an end by itself. High and variable inflation reduces the information content of relative price movements. Therefore, which inflation we focus on and how we control it matter critically.

The question arises: should the control instrument used, in controlling the growth and the composition of the aggregate balance sheet of the banking system, be a price (e.g., the official, central bank, interest rate) or a set of quantitative controls (e.g., capital and liquidity ratios, reserve requirements, and additional quantitative controls on the growth of the banking system’s aggregate balance sheet)?

This is a classic question in Economics; the seminal paper was written by Weitzman[9], although not in the context of financial policy.

We need to move away from a price (interest-rate) centred monetary policy implementation regime. We need to control the growth of the aggregate balance sheet of the banking system, by direct quantitative controls such as capital, gross leverage, and reserve (incl., settlement cash) ratios – and not through changes in the official interest rate (i.e., the OCR).

A complementary tool used, for example in New Zealand, and which is directly targeted to controlling maturity transformation, is a minimum “core funding ratio” requirement on all registered banks. This is the ratio of all funding with residual maturity over one year, to bank lending.[10]

Wouldn’t such direct controls create economic non-neutralities and inefficiencies? Not if we do not interfere with the credit-allocation decisions of banks either directly or indirectly (e.g., through price controls). The only restrictions that are justified on the overall growth and allocation of bank credit in the economy are justified on the grounds of reducing the major macroeconomic and social negative externalities created by the growth and composition of the aggregate balance sheet of the banking system. The larger systemic risk resides in encouraging banks to focus on making profit through excessive credit creation and maturity transformation, rather than through efficient financial intermediation.

A price (interest-rate) centred monetary policy violates the first principle of a good regulatory regime - the protection of the information content of relative (including inter-temporal) price movements. It also contributes to financial instability by affecting the mix of saving and consumption, and by directing credit to the wrong sectors and to people who cannot afford it. Finally, through its influence on the level and volatility of the second most important relative price for an open economy (the real exchange rate), it also causes serious harm to the real economy (i.e., macroeconomic instability).

Transition management

Regime change needs to be signalled well in advance of implementation, and implementation should be very gradual and timed so that it follows the return of the OCR to its “natural” (long run equilibrium) level – which may take some time.

All the required tools to implement a greater focus on the overall growth of the balance sheet of the banking system and its broader structure, as key ingredients of monetary policy implementation, are already in existence – they are part of the arsenal of the RBNZ’s tool kit for ensuring monetary and financial stability.[11] The only change that is required is a change of analytical framework and mindset on the part of policymakers.

[1] Allison, J. A. “The Real Causes of the Financial Crisis,” Cato’s Letter, Winter 2012, Volume 10, #1.

[2] See Turner, Adair (2017). Between Debt and The Devil – Money, Credit, and Fixing Global Finance, Princeton University Press, for a detailed articulation of the last two of these three bullet points in particular.

[3] Merton, R. and Brodie, Z. “A Conceptual framework for Analysing the Financial Environment,” in: D Crane (ed), The Global Financial System: A Functional Perspective. Harvard Business School Press, pp. 3-12, 1995.

[4] Cooper, G. The Origin of Financial Crises. Harriman House, 2008.

Hayek, F.A. Prices & Production and Other Works. Mises Institute, 2008.

Reinhart, Carmen M. and Rogoff, Kenneth S. This Time It Is Different – Eight Centuries of Financial Folly. Princeton University Press, 2009.

[5] Godley, W. and Lavoie, M. Monetary Economics – An Integrated Approach to Credit, Money, Income, Production and Wealth. Palgrave, 2007.

Huerta De Soto, J. Money, Bank Credit and Economic Cycles. Mises Institute, 2006.

Keen, S. Debunking Economics. Zed Books, 2011.

King, M.J. “Banking: From Bagehot to Basel, and Back Again,” The Second Bagehot Lecture, 25 October 2010.

King, M.J. “Twenty Years of Inflation Targeting,” The Stamp Memorial Lecture, Oct 2012.

LSE Report. The Future of Finance. 2010.

[6] Knowles, John; Austin, Laura; Kerr, Lewis (2023). “Money Creation in New Zealand”, Reserve Bank Bulletin. Vol. 86, No. 1.

[7] Rajan, Raghuram G. Fault Lines. Princeton University Press, 2010.

[8] Hayek, F.A. Prices & Production and Other Works. Mises Institute, 2008.

[9] Weitzman, M.L. “Prices vs. Quantities,” Review of Economic Studies. Vol. 41, pp. 477-91, 1974.

[10] Hoskin, K., Nield, I. and Richardson, J. “The Reserve Bank’s New Liquidity Policy for Banks,” Reserve Bank of New Zealand Bulletin, Vol. 72(4), Dec 2009, pp. 5-18.

[11] Knowles, John; Austin, Laura; Kerr, Lewis (2023). “Money Creation in New Zealand”, Reserve Bank Bulletin. Vol. 86, No. 1.

*Girol Karacaoglu is Adjunct Professor at the Wellington School of Business and Government (VUW). He retired from his role as the Head of the School of Government at VUW at the end of June 2022. He came to this role from the New Zealand Treasury, where he was Chief Economist. His current research interest is in public policy - an integrated approach to economic, environmental and social policies towards improving intergenerational wellbeing.

18 Comments

Great article! Only I disagree with "the creativity and skills of entrepreneurs and managers". It should be "the creativity and skills of entrepeneurs and leaders".

We should be rethinking fiscal policy.

A lot to chew on here, but the core broadening recommendations:

- that the type of inflation targeted be broadened to include asset (e.g., houses) as well as consumer inflation, and

- that the policy instruments used to control the growth and make-up of aggregate bank balance sheets be broadened beyond simply setting interest rates

are just common sense.

Granted that this guy used to be chief economist at Treasury, it's a shame that there aren't more informed and nuanced thinkers influencing the direction of NZ monetary policy.

Lots of quality thought here. Add in a healthy dose of industrial policy and we might be getting somewhere. Now, where are the commentators like this when the media are having clueless discussions about monetary policy?

Muzzled. :)

But what it shows more than anything, is the disjoint between the hard sciences, and economics. Ecologists - and there were some in that Department, in his tenure - could have told him that we are an overshot species, done on the back of too-rapid draw-down (of parts of the planet). Physics folk - I walk weekly with a retired Energy Prof - could tell him about entropy. Anthropologists cold tell him about the total collapse of value of ALL historical currencies - and (Tainter is the best at this) point out the link to depletion.

The basic problem is our to-date failure to index our tokens (money) to reality (the planer we're laying bets on). 'The Market' has zero ability to ascertain ultimate Limits; it's essentially a bunch of ill-informed lemmings. Economic Growth cannot remain un-coupled from material/energy throughput forever; it's the temporary abeyance that fools folk into thinking it can be (plus offshoring real production/pollution). And Economic Growth is the bottleneck-source of all our problems, which at this stage may well overwhelm us as a species.

It is possible he knows this - the information has been put under his nose - and is doing the Overton Window thing; pulling but not hard enough to break the rope. If so, fair enough. But if he's still back in the dark ages - still advocating economic growth - then this is merely a facilitating discussion, not a final one. Ultimately, for money to remain a store of wealth, 2% inflation isn't enough. It has to be indexed to real stocks, real flows -and I've long advocated the Joule. And we need to be past interest-charging (usury). Other cultures are, some outlaw it (and for good and obvious reason; not enough local resources to support a series of 'doublings').

Bhutan. Gross National Happiness.

Hahahaha. Here's the money. You slowly pay me back over 10 years. Don't worry, the amount in 10 years will be worth less than it is today, but I'll take the loss because I like you :)

That's going to happen to everyone who forwar-bet; kiwisaver, anyone silly enough to think that an artificial proxy was a permanent guarantee, on the basis that it had temporarily been a partial one.

Every Empire was based on more and more energy/material through-put. All peaked. All retrenched, all failed. All their currencies are collector-worth only. This time, for the first and only possible time, we ran the play at global scale.

Not a single mention of RBNZ's "Quantitative Easing" actions and the implications if any - find out more.

Second, transform short-term debt (i.e., deposits collected from savers or funds raised in wholesale markets) into long-term loans to households and businesses (“maturity transformation”).

Banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source.

Monetary supply targeting was used in the 1970s and 1980s and was a complete and abject failure. Move on.

You need to be a bit more specific, or risk coming across as an ideologue.

Failure how? And probably as importantly, for whom?

Because I'll tell you something for free - if 'money' is issued with no regard as to the physical limits of the underwrite ------------ that's a ponzi. Which puts advocates of same, in the Madoff class.

Just sayin....

my understanding is that Central Banks evolved away from using "quantitative" Monetary tools because its actually quite difficult to properly use quantitative tools,( let alone find really reliable quantitative measures) , , to manage inflationary pressures.

A Famous quote by a Canadian central Banker in the 1980s ..." We did not abandon the Monetary aggregates, they abandoned us "...Gerald Bouey

https://www.rbnz.govt.nz/-/media/7996ce9b71f24f02b54b3f00ea6cd719.ashx?…

Having said that.... our current inflation targeting policy framework has been shown to be , somewhat, flawed.

The idea of targeting the money supply is dumb as... But directing the flow of credit towards productive enterprise, whilse ensuring more equitable distribution of wealth has some merit.

In my moments of pondering.... If I was..."King for a day", Id take away the private banking systems ability to create credit.

Id increase money supply thru a. Universal Basic Income.... Maybe also , infrastructure investment.

In regards Capital formation....Id allow the marketplace to determine things.... eg.. entrepreneurs, venture capital etc. Id use policy incentives to kinda guide things, somewhat. (I don't trust a bureaucratic system that "allocates".)

These rJust a couple of ideas, that come to mind...

To put a label on it ., I favour a kinda social/market economy... a bit like Germany had post WW2.

Thanks for the article, Girol

I can't comment on the main text, but it can be argued that it wasn't Weitzman that invented the Weitzman principle in "Prices versus Quantities." William Poole, who became the Governor of the St Louis Federal Reserve, got there four years earlier in a paper called "Optimal choice of monetary policy instruments in a simple stochastic macro model " (The Quarterly Journal of Economics, 84(2), 197-216.) I'll bet dollars you have read this! This paper has the same idea but applies it to whether a central bank should target interest rates or money quantities. He, and to some extent the rest of the profession, chose interest rates - the paper was fairly instrumental in the change of Federal Reserve policy a decade later.

These days many monetary policy experts (like yourself) try and find ways of doing both eg setting interest rates and using restrictions on some classes of borrowers or suppliers to further control monetary or credit aggregates. Supermarkets (and cinemas) worked out this combination years or decades ago - you can set prices and place limits on how much much some people can buy at these prices.

Hope all is well, andrew

Just quietly, I wish you would comment on the main text. ;-)

I believe in the "primary recipe" section they're suggesting NGDP targeting (which is what market monetarists have been suggesting for a while), not using aggregate supply growth, but spending targets.

NGDP 5% = 3% inflation + 2% growth, if growth is low inflation is higher, and if growth is high inflation is lower.

You just have the central bank by more treasury bonds to boost spending next quarter when NGDP drops below 5% and vica versa.

It's pretty much settled that it's mostly fiscal policy, not monetary policy that drives inflation, which is why quantitative easing does nothing to boost it, but COVID stimulus instantly got the world almost in to the double digits.

So it makes a lot more sense for the CB to provide base to the treasury for a UBI than control the OCR.

And I'd much rather the tax payer, and not borrowers were bailed out during recessions.

I might even go as far and say the CB should control tax rates as a way to decrease spending, thought treasury bond purchases should be okay way to increase spending.

And replacing income taxes with an LVT for good measure.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.