This year we have regularly discussed Inland Revenue’s increased activities in the crypto asset investor space including the introduction of the Crypto-Asset Reporting Framework (CARF). In our view Inland Revenue is increasingly aggressive with its activities in this space.

$36 billion and counting

The latest demonstration of this focus is a media release “reminding investors of crypto-assets that they need to get tax compliant now, so they don’t end up with an expensive surprise down the line.”

The media release includes several interesting stats which reveals why Inland Revenue is paying so much attention to this area. According to Inland Revenue it “has identified 355,000 unique crypto-asset users in New Zealand undertaking around 57 million transactions with a value of $36 billion.”

Now, all those numbers are very surprising. Inland Revenue doesn't specify the period involved, but the fact that there's 355,000 crypto investors, basically one in fifteen of the population, is something that probably surprises a lot of people. The volume of transactions is again fairly extensive, but the sheer value is quite extraordinary.

Naturally Inland Revenue, particularly with the government finances under pressure, will be very keen to make sure all these investors are following the rules correctly. We're therefore seeing some fairly aggressive enquires, and there are a number of significant crypto related cases we know are before the courts which, by Inland Revenue's own account, involve tens of millions of dollars.

You are not invisible…

This bulletin sets out Inland Revenue’s approach. It reminds people that CARF is now in force and Inland Revenue will match information received CARF to tax returns and follow up on any discrepancies. The bulletin also observes

“…despite popular thinking, people are not invisible on the blockchain, and we have the tools and the analytical capabilities to identify and expose crypto asset activities.”

Reinforcing a development I reported recently, the bulletin continues:

“A first batch of letters has now been sent to people who would normally have their tax assessed automatically and who Inland Revenue knows have traded on one or more crypto asset exchanges.”

This is highly unusual. As people may be aware Inland Revenue is about to start its annual automatic assessment process, which between now and the end of June will process the year-end tax for over two million taxpayers churning out refunds or assessments of unpaid tax.

What this letter is pointing out is, that many people who are crypto asset investors are also salary earners subject to PAYE and therefore normally do not have any reporting obligations and they might think they've slipped through the cracks. This letter makes it clear to such persons that the auto assessment process will not apply to them. Inland Revenue has information about their crypto activities which they will need to report.

What to do if you receive such a letter?

A lot of people may be shocked when they look at their myIR accounts or open their mail to see such a letter. It may well be the first time they're had to engage directly with Inland Revenue. You're basically being asked to complete and file a tax return. I suggest that anyone who receives these letters should talk to a tax advisor and make sure you meet the obligations.

Do not put your head in the sand. In the present space we're seeing quite a bit of what you might describe as more forceful efforts by Inland Revenue across all activities - investigations as well enforcement debt collection.

This latest media advisory letter for affected crypto asset investors is part of this new landscape.

Fiscal drag, the tax system’s “dirty little secret”

Marc Daalder of Newsroom has published a story about the effect of inflation on the amount of additional tax that's been paid over the last 16 years. As I told Marc this is one the tax system’s dirty little secrets.

Marc’s story refers to a report prepared in December 2025 by Inland Revenue for the Minister of Finance, Nicola Willis and the Minister of Revenue, Simon Watts. The report was part of the commitment made in the National-New Zealand First Coalition Agreement to “…assess the impact inflation has had on the average tax rates faced by income earners.”

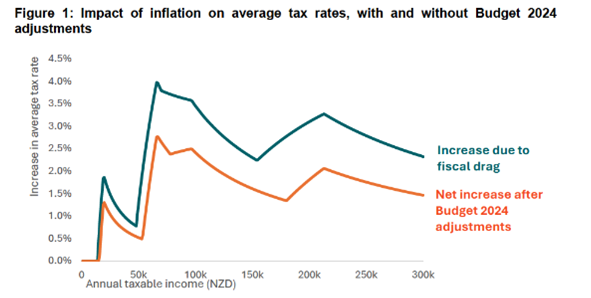

This brief report provides information on the inflation since 2010 when we last had a major reset of tax rates. Between then and the 2024 Budget nothing was done in terms of adjusting thresholds or tax rates other than introducing a new 39% tax rate on income over $180,000 in 2021.

What is fiscal drag

Fiscal drag is what happens when thresholds are not automatically indexed to inflation. Income growth even if just for inflation only can result in more income being taxed in higher tax brackets and therefore increase average tax rates. The analysis focuses on individuals rather than families and solely considers taxable income. The report considers the increase in average tax rates due to inflation across the various income distributions and the amount of additional revenue from this increase in average tax rates and the distribution of individuals impacted by these higher tax rates.

The report concludes, unsurprisingly, that fiscal drag has increased average tax rates and therefore tax revenue since 2010. Annual inflation measured by the Consumer Price Index between 2010 up until 2024, i.e. the period, the 14-year period in which tax thresholds did not increase averaged approximately 2.5% per annum.

Average tax rate rose by 2.55 percentage points

The Inland Revenue report includes a table showing the inflation-adjusted thresholds for the 2010-2024 period. (The 39% threshold introduced in 2021 has also been inflation adjusted).

|

Rate (%) |

Current |

Inflation-adjusted |

|

10.5 17.5 30 33 39 |

0-15,600 15,601-53,500 53,501-78,100 78,100-180,000 Over $180,000 |

0-19,323 19,324-66,249 66,250-96,614 96,615-212,939 Over 212,940 |

According to the report overall fiscal drag has increased the average tax rate by approximately 2.55 percentage points without the Budget 2024 adjustments and 1.65 percentage points when including them.

Most people will think the greatest increases in average tax rates will be for people on higher income. But listeners who have heard me bang on about this topic for many years will know the greatest impact is in fact lower down the income scale than most might think.

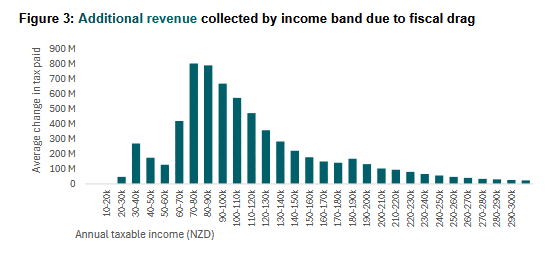

In fact, the biggest single increase is for individuals earning between $70,000 and $90,000 in 2024.This is because this group had a greater share of their income shifted into the 30% bracket because of the 12.5 percentage points jump in tax rate from the lower 17.5% bracket. According to the report the threshold for the 30% rate which was $48,000 in 2010 should have risen to $66,249 by 2024, over $18,000 higher.

Consequently, the additional tax revenue collected by fiscal drag in annual taxable income reported is nearly $2 billion for people earning between $60,000 and $90,000.

Even taking account of the 2025 Budget changes, the report estimates fiscal drag’s additional revenue increased tax revenue by approximately one percentage point of GDP or over $4 billion annually. This number is higher than I had expected.

Don’t expect any changes in the Budget

It will be interesting to see if there’s any fallout from this report. The fiscal pressures for the government are such that there is no chance of any threshold increases happening in this year’s Budget. In fact, I don't think a new government of any hue will be in a position to introduce increases any time soon.

European Commission report on wealth taxes.

Last episode we spoke with Tax Justice Aotearoa, who had published their tax policy statement for a fairer, more transparent tax system. Coincidentally, this was released at the same time as a monster report published by the European Commission Wealth taxation including net wealth, capital and exit taxes.

The report itself has two volumes and runs to over 450 pages which I am still digesting but fortunately there’s a 17-page executive summary. The foreword to the executive summary notes:

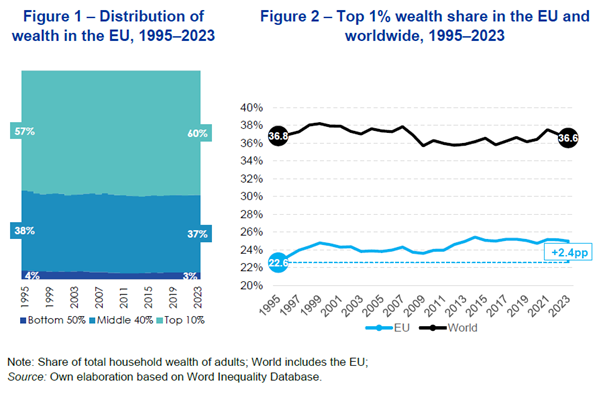

“The report is set against a backdrop of rising concern about the distribution of wealth in Europe, the erosion of taxes on wealth and wealth transfers over recent decades, and renewed fiscal needs in the wake of multiple crises. Over the past three decades, private wealth in the EU has grown substantially and has become more concentrated among households at the top of the wealth distribution.”

What is concerning the EU is that the top 1% in the EU have increased their share of total household wealth faster than their counterparts globally.

“This trend is notable because global top-wealth shares have stabilised in recent years while the EU continues to witness an upward drift. These patterns underscore the broader economic context for the present study. Wealth concentration is becoming a structural feature of the European economic landscape, raising questions about how existing tax frameworks can ensure fairness.”

A question of fairness

The European Commission echoes what Tax Justice Aotearoa and other tax fairness advocates are saying. If the tax system is building in unfairness, then what are the downside risks of perceived unfairness? If wealth is not being taxed relative to income, what are the social impacts of that?

The report contains some very interesting analysis, for example it notes that the very wealthiest, the top 0.01% in the EU have grown less rapidly than their peers in some non-EU countries. This apparently reflects a smaller role for high-growth firms and more redistributive systems. “These features temper the emergence of extreme fortunes, even as the top 1% continue to pull away from the rest.”

The available evidence here also points to the wealth gap between the richest 1% and the rest increasing substantially.

What is a wealth tax

The report analyses all wealth-related taxes such as net wealth taxes, recurrent taxes on unrealised capital gains which are a response to the “distortions created by realisation-based capital taxation” (our Financial Arrangements regime is an example of such a tax). Non-recurrent realised capital gains tax – which is the “classic” capital gains tax which arises only on a realisation event.

The report notes, unsurprisingly, that non-recurrent taxes on realised capital gains form a core component of capital income taxation in all EU member states, although their design varies substantially. The report notes the empirical evidence indicates that higher capital gains taxes can reinforce lock-in, (i.e. holding on to assets to avoid a tax charge) and capital gains tax cuts might have positive impacts on certain investment transactions.

The report notes, and this is also an issue, if not THE issue in our tax system, the central limitation of the various EU capital gains tax regimes s incomplete coverage. Unrealised gains are heavily concentrated among high wealth households, and realisation-based systems enable strategic timing of sales.

There's a section on inheritance and gift taxes, noting that their share of tax revenue and private house increased in a number of European countries, and large inheritance is very important in the formation of very high net wealth, including among billionaires. In other words, billionaires are inheriting or being created by inheritances, which may be not as ideal.

Apparently, 17 member states and some other European countries have inheritance or estate taxes. The report notes

“Looking forward, simulations suggest that the revenue potential of inheritance taxation is likely to grow further as the volume of bequests increases with the “great wealth transfer” from older to younger cohorts.”

This is referring to the transfer of wealth now happening as the two richest generations in history, the Baby Boomers and Generation X, are now starting to pass away leading to a great wealth transfer of trillions of dollars to their descendants. Naturally, tax authorities and politicians are seeing this huge wealth transfer and thinking, ‘we might want some of that to meet rising costs of superannuation and ageing’. Similarly, taxpayers will take steps to mitigate the effects of taxation

Behavioural responses to wealth taxes

The report comments that “Behavioural responses and institutional design are central to understanding the performance of inheritance and gift taxes” The empirical evidence points to strong incentives for tax planning. For example, the UK’s Inheritance Tax applies at 40% to estates worth more than £500,000. That concentrates the mind wonderfully so there's a lot of Inheritance Tax planning as a consequence. Conventional economic theory has tax as a deadweight cost and inhibitor of activity

On the other hand, according to the report the tax effects on wealth accumulation, labour supply and entrepreneurship appear generally modest.

“Available studies suggest that inheritance taxation can be designed in a way that preserves its progressivity and revenue potential without triggering large real economic distortions, provided that enforcement is effective and legal avoidance channels are curtailed.”

This whole section probably merits a podcast of its own.

The mobility effect of wealth taxes and Australia

The report also covers a set of taxes referred to as “exit taxes”, which if a person migrates may trigger a tax charge on exiting the country. (America applies one such tax to anyone renouncing its citizenship). According to the European Commission, broader research on mobility suggests that high wealth relocations are rare and movements are more influenced by preferential regimes in destination countries than by exit taxation itself.

I agree with that analysis. The biggest concern I have about introducing a wealth tax in New Zealand is this mobility effect. That's because Australia has an extremely favourable regime, the Temporary Residents regime. My worry would be that people would migrate to Australia, because as long as they don't become Australian citizens, then non-Australian based investment income and capital gains should remain outside the Australian tax net practically indefinitely. (By contrast our Transitional Resident exemption is time limited). The capital flight risk is one which has to be analysed because investors and migrants do look closely at preferential tax regimes.

Overall, this is a fascinating report, and it reflects growing interest worldwide in wealth taxation. The issues identified in the report as a cause of concern about the long-term effect on social coherence of extreme wealth accumulation are relevant here and this report will add to that debate.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

10 Comments

Fiscal drag is the ultimate stealth tax. It's a deceptive mechanism that allows the government to quietly extract wealth and expand its reach without ever having to face the political backlash of an open tax hike. But fixing the brackets misses the deeper issue, because all taxation is, by definition, coerced theft on a grand scale.

It is a violent extraction of wealth backed by the threat of force. Unlike a business in a free market that must earn your dollar through voluntary exchange, the state simply demands your property under the implicit threat of violence. Fiscal drag is just a clever, cowardly sleight of hand to make that theft a little quieter.

Good news, there are still countries out there with virtually no tax collection - Libya, Sudan, Somalia, Haiti. Perhaps you could try your luck there, although unfortunately none of them are ideal climates for a snowflake.

Equating a free market with a war-torn failed state is a total misunderstanding of the argument. Places like Somalia, Libya, and Haiti aren't suffering from too much capitalism; they are suffering from the violent collapse of statism, where competing warlords act as localized mafia governments.

You still get 'taxed' there—it’s just called protection money or a shakedown at a checkpoint by the local militia.

Telling someone to move to a war zone because they point out that taxation is forced extraction is like telling someone who complains about a mugger to go live in a prison as well as being a ridiculous economic argument.

A friendly way to address past bracket creep would be to let it stand, but set a 0% tax rate on the first $20,000 of income, as it is in Australia and Britain, I think. The higher rates (17.5%—39%) would need to rise to collect the same revenue.

Please explain why Marxists think progressive income tax is fair. Its obvious to others that "fairness" requires proportional / flat income tax regimes.

"From each according to his ability, to each according to his needs" K.Marx 1875 is a blatant appeal to envy theft.

It's a recognition that the first, say, $10k you earn in a year is far more important to your quality of life and survival than the 20th $10k. I earn a decent wage such that my tax rate only really effects how much I invest this year, or what holiday I go on, rather than whether I can afford to provide my family with food and heating this week.

Okay, KKNZ2025, here's a flat income tax rate for you:

50%

tempered by a flat $500 tax-free universal basic income for everybody 18 and over, and $250 a week for everybody under 18.

Cheers, Tovarisch!

"The problem with socialists is they eventually run out of other people's money" Maggie Thatcher

And conversely the problem with capitalists is they only want the best for all until it tangibly negatively impacts them, then will do all possible to preserve their own wealth and influence legislation, regulation to suit this. Two sides to the same coin. They key of course is finding balance.

Currently the Dutch are implementing or have implemented an unrealised CG on certain assets. Don't recall which assets. The French introduced a wealth tax which only lasted a few years. Seemed to recall Gerard Depardieu went off to live in Russia because of tax.

We already have unrealised capital gains on certain shares. The Greens appear to be raising an extra $88bill in taxes in their proposed budget. I'll be interested to see which economists or other financial advisers have drawn it up for them. I doubt whether CS or MD have ever used a spreadsheet. That probably goes for quite a few politicians.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.