By Stephen Bartos*

This year’s Australian federal government budget combines fiscal policy – taxes and spending – with a heavy focus on better regulation.

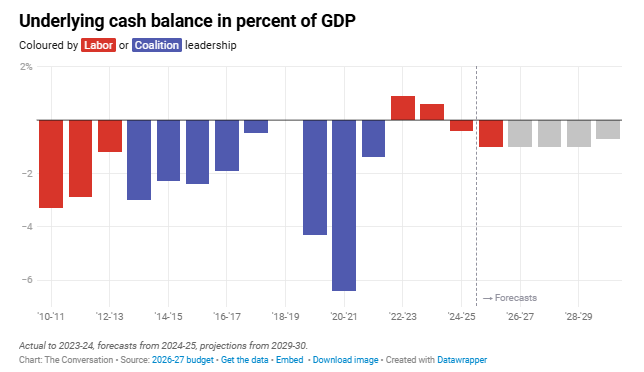

The budget deficit has fallen slightly from the mid-year update in December, to A$31.5 billion, but the budget remains firmly in deficit for the foreseeable future.

Tax reform

There are important reforms to capital gains tax, negative gearing and trusts. While the reforms are significant, the timing is cautious.

The capital gains tax discount – which currently halves the tax on gains made from buying and later selling assets – has made housing less affordable. Pre-budget rumours correctly predicted the time was ripe for this Howard-era policy to be reformed.

The discount will be abolished, replaced by an inflation adjustment for assets held for more than 12 months, with a 30% minimum tax on net capital gains. Changes will only apply to capital gains arising on or after July 1 2027, more than a year away.

The government will also limit negative gearing for residential property to new builds. This, too, will take effect from July 1 2027. The delayed start to the measures means revenue gains only kick in from 2028-29. But they are large, starting at $1.35 billion, rising to $2.28 billion the year after.

In the long term, these changes will help make housing more affordable and the budget more sustainable.

When asked in his budget lockup media conference whether this was a broken promise, Treasurer Jim Chalmers said not acting would have been easy – “easy but wrong”. Reforms will help housing access, particularly for young people. “I acknowledge this is a controversial change,” he said.

A raft of changes

Even larger in budget impact, but more delayed, are changes to trusts. A minimum 30% tax on discretionary trusts is being introduced from July 1 2028. The long transition period is for “small businesses and others that wish to restructure”.

Exceptions include superannuation funds, disability trusts, deceased estates and charitable trusts. Even so the measure is estimated to raise some $4.47 billion in 2029-30.

There is a raft of other measures to cut taxes, mostly small in budget impact and aimed at helping business. They include extending the instant asset write-off for small business, tax refunds on previous losses for small start-up companies, and expanded venture capital tax incentives.

For individuals there is a tax cut, the “Working Australians Tax Offset”, of up to $250 a year. The budget also re-announces a measure from the mid-year budget update, which allows instant tax deductions for expenses up to $1,000 for work-related expenses.

The fringe benefits tax deduction for electric vehicles is being reduced – another tax change with a long phase-in period. It starts small, in fact costing the budget $10 million in the first year, but grows to improve revenue by $1.57 billion in 2029-30.

Spending cuts

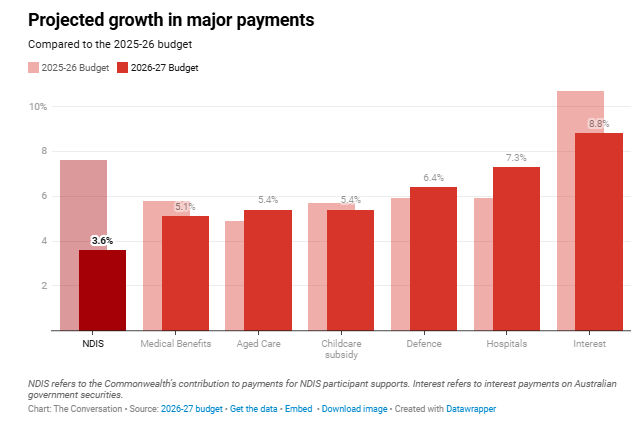

There are previously announced savings in the National Disability Insurance Scheme ($23.9 billion compared with the mid-year update, and $37.8 billion after a recent blowout in estimated costs).

Funds are also shifted between different agencies in government. There are spending increases in portfolios such as defence and social security, cuts in others like climate change and agriculture. Much of the growth in program spending was foreshadowed before the budget, such as more funding for Medicare and responses to the Bondi attack.

Regulatory reform

Past budgets have been mostly about tax and spending. This budget also includes a sweeping package of regulatory reform.

Some of this is in a “productivity package” that includes abolishing nuisance tariffs, faster environmental approvals, streamlining border biosecurity, and making it easier for businesses to engage with government.

A risk for the federal government is many of the elements of the package rely on the states and territories – including reform to the national electricity market, harmonising retail tenancy regulation, and simplifying building regulation.

While this is all highly desirable for improved productivity, history tells us states and territories can hold the Commonwealth hostage. They can demand additional payments or other policy concessions before they act on reforms. It is a risk.

The government has also released a list of 14 legislative reforms to reduce regulation on businesses and households. They are wide-ranging and diverse, from higher reporting thresholds for large companies, through reducing barriers to small bank mergers, to reducing bereavement costs for families.

Better regulation is closely aligned to the productivity agenda. In addition to the reforms aimed at reducing the burden of regulation the government has promised further reviews aimed at better regulation.

It also promises, under the heading “single national market” a set of clear and consistent rules across federal and state governments. Again, progress will depend on the cooperation of other jurisdictions, which is not guaranteed.

In summary, the budget is workable. It includes valuable tax reforms, wide-ranging spending well-targeted to areas of need, and a more comprehensive regulatory reform than in most budgets.

However, there are significant risks. The NDIS savings estimates rely on compliance working. The economic forecasts assume global oil prices start to fall from mid-2026 (just weeks away). The regulatory reform agenda relies on state and territory cooperation.

As the treasurer said in his budget speech: we live in a time of “extreme uncertainty”.

![]()

*Stephen Bartos, Professor of Economics, University of Canberra.

This article is republished from The Conversation under a Creative Commons license. Read the original article.

8 Comments

The Aussie boomers delight - Commonwealth Bank - down 7% not long after market opening.

Why is it a potential bellwether (despite the evidence that CBA trades at a material premium to most large global-bank peers on P/E)?

Ponzi exposure: Boomers benefitted from property price rises and held long-term mortgages and deposit relationships that entrenched CBA’s position in household banking.

Income and dividend appeal: CBA’s reputation for stable profits and franked dividends makes it attractive for retirees seeking reliable income, reinforcing boomer investor preference for the bank’s shares.

Phoenix. Yeah, that elevated PE is why I don't own them but by not doing so I've missed the ride over the last 5 years. Cant complain though, ANZ has treated me well over recent times. I'd add to your list of features making the banks attractive, the way in which they act as a proxy investment across the wider business spectrum ( well, in theory anyway).

Phoenix. Yeah, that elevated PE is why I don't own them but by not doing so I've missed the ride over the last 5 years.

CBA's stock price has appreciated 60% over P5Y. Super funds are overweight CBA largely because of their large scale, benchmark-driven allocation mechanics (index tracking and closing underweights to major banks), concentrated domestic equity exposure, and a need to deploy large flows into the largest-cap ASX names - which mechanically boosts CBA’s weight in their portfolios.

Yep, that mechanical allocation process of passive funds theoretically an argument in favour of active but increasingly they also largely follow indexes with not much deviation.

AFR gets their piece in:

Anthony Albanese argued that unless something was done to address intergenerational inequity in the housing market, social cohesion would continue to fray and more people would vote for the Greens or One Nation.

But every argument being made now and in the next few weeks could have been made before the last election – and carried.

Pauline Hanson’s outfit received 40 per cent of the primary vote in Farrer on Saturday, in large part because voters have had a gutful of such disingenuous behaviour

Team Albo has been a godsend for populist politics. On One Nation, they're even getting support in Western Sydney from ethnic enclaves - Chinese, Vietnamese, Middle Eastern.

https://www.afr.com/politics/federal/meritorious-or-otherwise-2026-budg…

I saw that they even grandparented existing negative gearing arrangements so their claims of addressing " intergenerational inequality" for younger voters will be seen as typical hypocrisy.

Yes. It's nonsense. The boomers are shrieking, but the younger demogs are really no better off as far as I can see.

And younger people can't even really go full degenerate on crypto as they will get stung in those mkts as well. Most will not be able to find comfortable tax-free moats - too much of a hurdle, except for a few.

She has a point.

If this is all about housing for young people then why are all our other assets being included such as shares , commercial property , industrial property what’s that got to do with housing ?

- Pauline Hanson (X tweet https://x.com/PaulineHansonOz/status/2054152577663795619)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.