The Organisation for Economic Co-operation and Development (OECD) recently released its 2026 Economic Survey of New Zealand. The OECD, like the International Monetary Fund (IMF), carry out regular reviews and this is a fairly detailed report running to over 140 pages, which you would expect, given the OECD has a significant economic database to work with.

The OECD was cautiously optimistic about the state of the NZ economy but noted that GDP growth was slower than in many OECD countries. Ongoing fiscal consolidation was needed, but the Middle East conflict may require more “targeted support”. It recommended ensuring “strong accountability through transparency of the [RBNZ’s] Monetary Policy Committee decision making”. Other recommendations included harnessing digital tools to improve health system performance and for a more affordable, secure and sustainable electricity system (which, in the long term, does not include LNG in the OECD’s view).

Not all recommendations made by the OECD or the IMF are greeted with enthusiasm by the government of the day. The Prime Minister reacted very strongly to warnings about the Government’s LNG proposals, calling the OECD’s report “a load of rubbish”.

Unlocking capital markets to drive growth

It’s Chapter 4 of the survey, which I found most interesting and relevant, as it included a discussion of our tax settings relating to the taxation of savings. This section was written by Dr David Haugh, the head of the New Zealand (and Finland) desk, together with his colleagues Kyongjun Kwak and Carl Magnus Magnusson. Dr Haugh is actually a New Zealander who started his career with the Treasury before joining the OECD. That means he has a good background knowledge of New Zealand and our challenges.

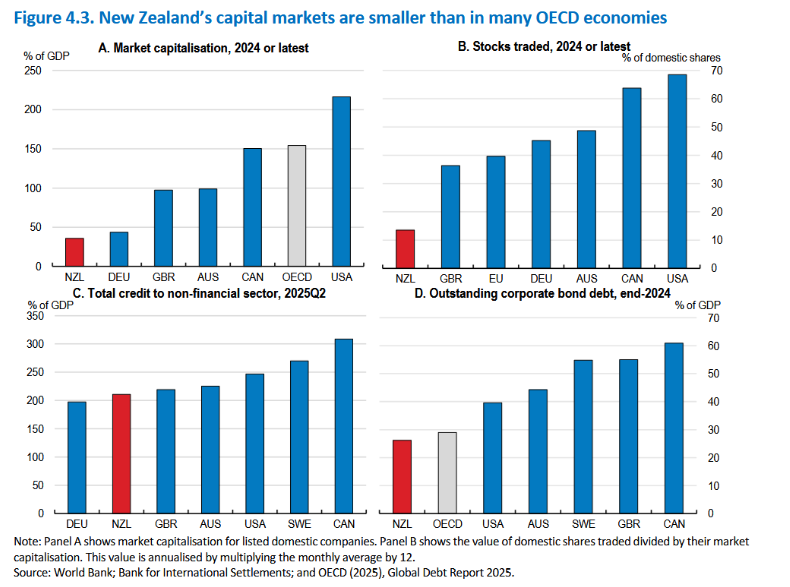

The background summary is that our capital markets remain “shallow by international standards, constraining long-term investment, innovation and productivity growth”. The survey notes that the NZX has seen no major domestic initial public offerings since 2021. That's apparently part of a worldwide trend, as many firms that might otherwise have gone to market have instead opted for a private or trade sale. A classic example would be Fonterra's recent sale of its global consumer and associated businesses, Mainland Group, to Lactalis.

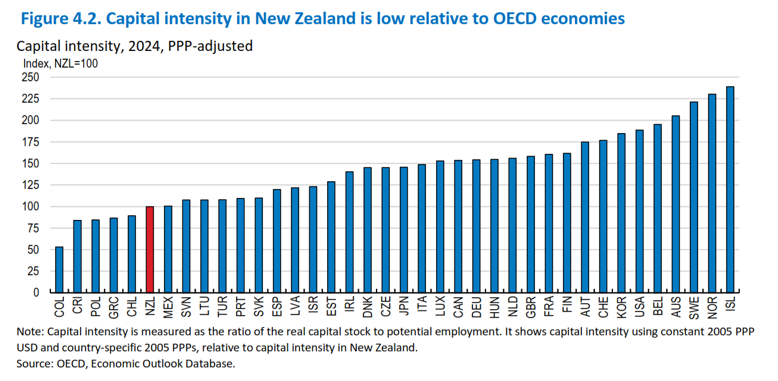

There are some pretty damning graphs illustrating the scale of the problem. Quite apart from smaller-than-average capital markets, ‘capital intensity’ or the ratio of real capital stock to potential employment is low relative to other OECD economies. In 2024, New Zealand’s capital intensity was just about 100%, whereas if you look at Israel, Norway and Australia, they're all over 200%.

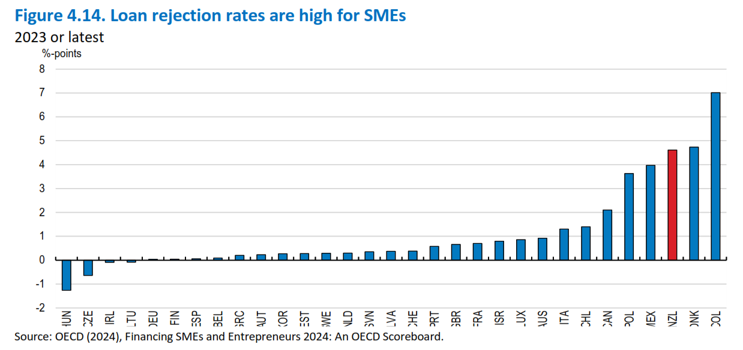

There's also a sideswipe for the Australian banks, with the OECD saying “costly bank lending dominates, with OECD analysis of lending margins showing they're about twice the international norm”. With the main banks preferring mortgage lending, SME loan rejection rates are high.

There’s a fairly blunt assessment of why our capital markets are underdeveloped – the decision in 1975 to cancel the Third Labour Government’s compulsory superannuation scheme:

“The decision to abolish the private pension saving schemes in 1975 and replaced it with a publicly funded universal pension at age 60, significantly hampered the development of New Zealand's capital markets by reducing households' incentives to accumulate private pensions, depriving capital markets of a key source of long-term domestic funding.” [page 98]

Developing public equity markets – the Swedish example

There’s a very interesting discussion about how Sweden “has developed one of the most dynamic and inclusive equity markets relative to its economic size in Europe and across the OECD.” A key element of this is the Investment Savings Account, or an ISK account. There are over 4 million ISK accounts, with half the adult population having an ISK. These have helped channel household investments into listed equities. Britain’s Individual Savings Account is a slightly similar product. The recommendation is that we consider introducing a non-retirement New Zealand Equity Savings Account.

Raising household savings through changes to KiwiSaver

The report notes our retirement savings are fairly inadequate by world standards. In September 2025, the value of funds under management in KiwiSaver was $141 billion or 32% of GDP. By comparison, in Australia, the assets under management exceeded A$3.6 trillion or 133% of GDP. Furthermore, the average Australian retirement pension plan value is NZ$130,000 or nearly five times greater than the average NZ$28,000 in New Zealand.

The survey notes that withdrawals are allowed to buy a first farm or first house, which, together with increasing withdrawals for hardship (these have doubled from $100 million a month in 2023 to $200 million a month in 2025), slows the accumulation of funds. The OECD questions the purpose of withdrawals for first farms or houses. It suggests that if the policy objective is to support low-income people into house ownership, then a separate instrument would be more effective. The OECD also recommends not creating any further exemptions.

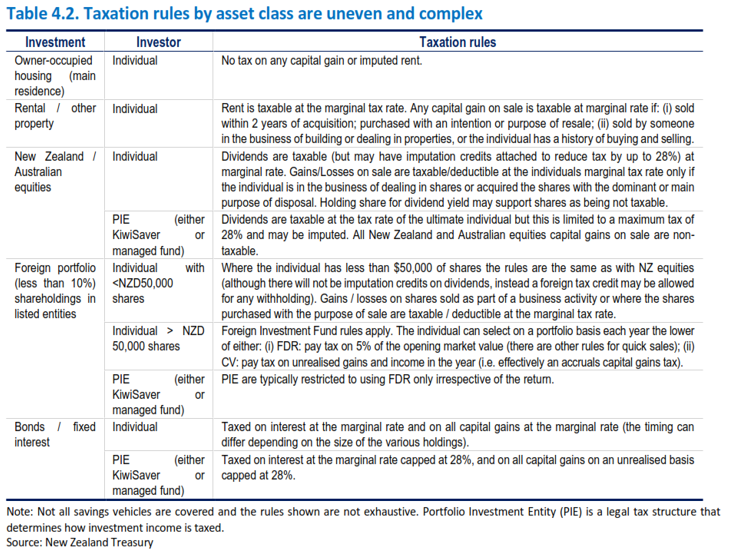

‘New Zealand’s taxation of capital income and savings is complex and uneven’

The survey then discusses the taxation of capital income and savings, which it describes as “complex and uneven, with housing taxed lightly relative to financial assets and especially pensions”. Our corporate income tax at 28% is noted to be amongst the highest in the OECD. Taken together, these settings:

“…distort household and firm investment decisions and suppress the accumulation of private pensions and other long-term financial savings, which is a critical issue not only for capital market developments but also for retirement income adequacy.”

In short, the way our tax system has distorted savings has had long-run consequences. This is something I've been saying for a long time and it’s also the view of the International Monetary Fund.

Increasing the accumulation of pension savings by reforming the taxation of savings

The OECD’s view is that the taxation of savings needs reform to allow greater accumulation of pension savings. The survey notes only seven of 38 OECD countries tax the investment income pension and only three, New Zealand, Australia and Türkiye, have a tax-tax exempt system (TTE). The most common system operated in about 17 out of 38 countries is an exempt tax, which is what you see in the UK and America, which allows the accumulation of more funds within the fund that eventually gets taxed as a pension.

The critical disadvantage of our TTE system is that it penalises the accumulation of long-term financial retirement assets, sharply reducing compounding returns relative to the exempt-exempt-tax systems used by many other countries, such as the UK and the United States.

The OECD bluntly concludes:

“The TTE system for financial savings combined with light taxation of housing in New Zealand… makes the overall system one of the most housing-biased tax systems in the OECD. This bias has been capitalised into higher house prices, larger new dwellings, lower ownership rates amongst younger cohorts, and a worsening of New Zealand's net international asset position, reflecting reduced domestic financial capital available for firms.”

The OECD notes that because pension savings compound over 40 years or so, lowering the tax burden on returns “substantially increases long-run private wealth accumulation”. So, does that mean switching to the common exempt-exempt-tax approach? Not quite. An argument against such tax incentives, and one I share, is that the benefit of such savings is mostly captured by the wealthy who would be saving anyway, and tax incentives don't lead to significantly increased savings. Another issue with tax incentives is, as Finance Minister Nicola Willis pointed out, they are extremely expensive.

Auto-enrolment and KiwiSaver

According to the OECD, many of these concerns are indirectly addressed by an auto-enrolment system, i.e. everyone would be in KiwiSaver and therefore automatically contributing and saving. UK evidence is that within such auto-enrolment schemes, savings do not fall or rise in response to tax incentives and other private savings are not reduced to offset the diversion into tax-preferred schemes. Furthermore, the strongest benefit of such a change would be for low and middle-income households, who have limited discretionary savings anyway.

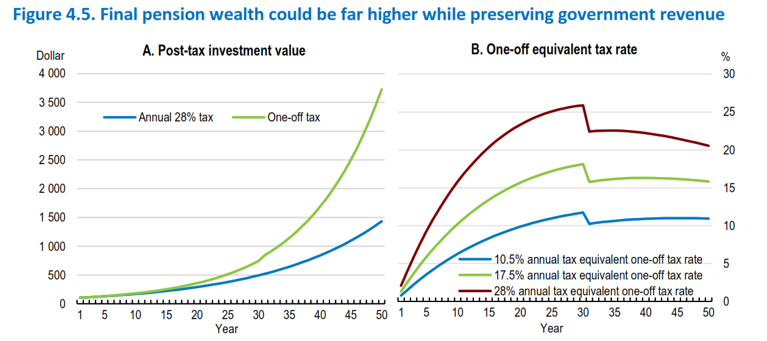

Removing or reducing tax on KiwiSaver returns would operate primarily by allowing greater compounding and unchanged contribution patterns, generating substantial increases in total retirement wealth. In other words, directing the incentives there towards the lower-income earner is an approach I fully support.

The survey includes an example illustrating that if this approach is adopted and coupled with a withdrawal tax, the post-tax pension value is twice as large by age 65 compared with the current annual taxation approach.

Overall, there’s plenty of food for thought in this survey. We’ve had a long period of stable policy settings in relation to savings, but we have problems with productivity and access to capital for start-up companies. New Zealand actually has a fairly vibrant tech sector, but as this paper notes, a lot of small tech companies go overseas to get funding because they can't get it here. I’ve advised on a few such situations, and I’m always surprised the investment capital isn’t readily available here. This OECD survey should therefore provoke plenty of debate amongst politicians and analysts alike, but I fear it will get drowned out by the noise around the coming general election.

The latest National Climate Change Risk Assessment is not a pretty read

More or less simultaneously with the OECD report release, the Climate Change Commission released its National Climate Change Risk Assessment (NCCRA) for 2026. This is the first one that's been produced since 2020 and is not pretty reading. It identifies the 10 significant risk areas “where focused action would make the biggest difference.” In short, this means increased infrastructure spending, particularly in relation to water infrastructure. The NCCRA warns that without immediate action, water infrastructure could be the “first climate risk to reach an extreme severity level within the next 25 years”.

The regularity of natural disasters has been increasing. According to the NCCRA stat, about 97% of the estimated $33 billion of government expenditure on natural hazards since 2010 was spent on responding to and recovering from disasters, with only 3%, i.e. a billion dollars, spent on risk reduction.

What happens when the insurers withdraw cover?

Whether or not you accept what's driving climate change, it is happening. The NCCRA notes that 556,000 buildings with a combined replacement value of $235 billion are currently exposed to inland flooding. Insurance premiums are rapidly rising, leading the OECD’s economic survey to note “climate-change-induced rises in insurance premiums make inflation control more difficult”.

Quite apart from rising insurance premiums, my concern is that at some point, the insurers are going to dictate what happens with such properties. If the insurers start withdrawing cover, and that's now coming into general discussion, people will look to the government to help because if they can't get insurance on their properties, the banks won't lend against that. This also ties into what the OECD was saying about the high dependency on property ownership for savings.

The NCCRA notes that if we keep allowing the current pattern to continue, of simply accepting damage will happen and then repairing it afterwards, this will drain funds away from core services such as health and education. Over the past 15 years, we’ve spent on average $2 billion a year, or roughly 0.5% of GDP, on climate mitigation and recovery, and things are only getting worse.

All this comes back to a long-standing argument I've been making here on the podcast and elsewhere: that climate change is going to drive changes in our tax system by way of having to increase revenue to fund these changes. There’s been plenty of debate about the long-term fiscal sustainability of New Zealand superannuation, but the impact of climate change is an immediate and growing problem.

This is a long-term issue where you really do hope that all the major parties in Parliament accept the need to address this and move accordingly. But as we've seen with the superannuation debate, that's not likely to happen.

The Australian Budget

Finally, across the ditch, the Australian Budget was handed down on Tuesday, 12th May. There had been a lot of speculation beforehand that there would be changes to ‘negative gearing’ and the taxation of capital gains. This speculation was correct, but the extent of the changes has taken people by surprise.

Negative gearing is what the Australians call the ability to offset losses from residential property investment against other income. With immediate effect, any new investors will now only be able to offset losses from purchases of ‘new builds’. (Rather like our previous interest limitation rules.) Taxpayers with existing rental properties will still be able to offset their losses against other income. In other words, they will not be subject to what we term ‘loss ring fencing’.

The capital gains tax surprise

Presently, Australia grants a 50% discount on the amount of a capital gain for individuals, trusts and partnerships if the asset in question has been owned for more than 12 months.

This 50% discount will no longer apply for any gains realised on or after 1st July 2027. Instead, there will be a cost-based indexation, i.e. based on retail price, which was the rule between 1985 (when Australia introduced capital gains tax) and 1999. There will also be a minimum 30% tax rate on capital gains.

This is a significant change, and it’s expected to result in a rise in payable capital gains tax. Pre-Budget speculation focused on gains from residential property investment, but this change will apply to all asset classes.

A potential silver lining?

Now, the interesting thing if you're a New Zealand resident and you've got a property investment in Australia, this change may be beneficial. At present, New Zealand tax residents are subject to Australian capital gains tax on disposals of Australian-situated property, but because they are not Australian tax residents, they do not get the 50% discount. (Australia is frequently quite sneaky in how it taxes non-residents.)

This change may mean that New Zealand investors subject to Australian capital gains tax on Australian properties may actually be better off. We'll need to see the details on that, but it's perhaps a silver lining for everyone.

On that note, that's it for this week. I'm Terry Baucher and thank you for listening. Please send me your feedback and tell you and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Friday 15th May – it has been edited for brevity and clarity]

2 Comments

people will look to the government to help because if they can't get insurance on their properties, the banks won't lend against that.

The government should not be responsible for bailing out risky properties from acts of god, for good reason. The Chch quakes had the EQC with a fund built up to buffer this, which no longer exists, and the current govt seems averse to ever considering building another to help with future events. Therefore it is a buyer beware situation, as it always should have been. It will be difficult for some who have had their properties rezoned or recategorised, as the modelling for this has ben in question in parts of the country already, but some will definitively lose out with certainty.

Seems it has been a long time since people realised that they have to be diligent with choices to best protect themselves from risks, o they will bear the consequences. The govt cannot be a backstop for poor decision making, or increased prevalence of natural disasters in certain areas.

Andrew Coleman's proposal for changing the KiwiSaver tax regime is worth a read:

https://www.interest.co.nz/public-policy/130335/new-zealand-tax-podcast…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.