Westpac New Zealand's annual profit rose 69% helped by a big turnaround in loan impairments.

Westpac NZ's September year net profit after tax rose $381 million, or 69%, to $931 million from $550 million in the year to September 2020. Last year's annual profit was a 43% drop off the back of rising loan impairment charges.

A major factor in the big increase this year was a $404 million turnaround in loan impairments from a $320 million charge last year to an $84 million benefit this year.

Westpac NZ's net operating income rose 8% to $2.463 billion, and its operating expenses rose 7% to $1.132 billion. Net interest income was up 9% to $2.118 billion.

The bank's net interest margin rose three basis points to 2%, and its cost to income ratio improved 45 basis points to 45.96% from 46.41%.

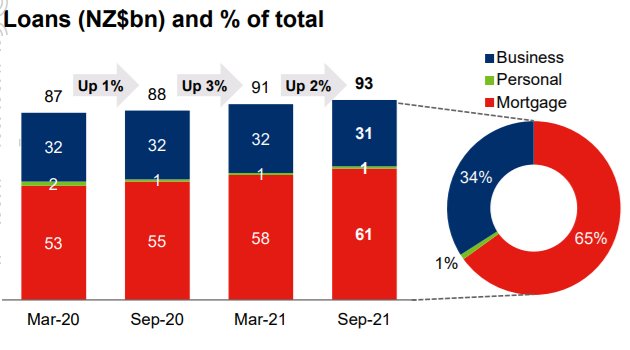

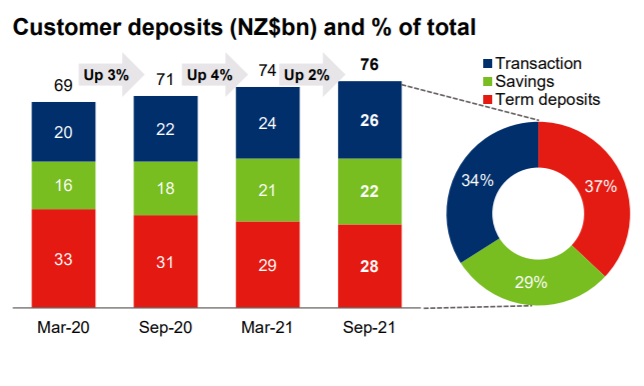

Home loan lending grew a net 10% to $60.9 billion with Acting CEO Simon Power saying Westpac NZ's home loan growth had been about 0.9 times system growth. Customer deposits rose 7% to $75.9 billion.

Power says how customers are faring against the backdrop of Covid-19 and restrictions related to the virus is very sector specific and very geography specific.

"At a general level small businesses and other businesses have been better prepared for Covid this time around and so we haven't seen the demand for facilities and lending that we necessarily saw in the first big lockdown [last year] looking for headroom," Power says.

"What we have seen is transaction accounts and savings accounts with higher levels in them than this time 12 months ago helping prepare businesses for any need for reserves to be used."

As a general statement Power says businesses are better prepared now than at the onset of the pandemic.

"But sector by sector we're definitely seeing stresses starting to emerge in the hospitality, accommodation and tourism areas and we're keeping a very close eye on what the medium term outlook might be for those sectors in particular," Power says.

Nonetheless Westpac NZ chief financial officer Ian Hankins says the hospitality, accommodation and tourism sectors typically don't have large debt.

"You won't see big exposures across our [lending] portfolio in that space. But still a lot of them are in pain and the focus is to do what we can to support them," says Hankins.

Power says funds under management in the Westpac KiwiSaver Scheme increased 14% year-on-year, to $9.1 billion with the average Westpac KiwiSaver Scheme balance up 16% to $23,717, helped by strong financial market performance.

“Last year we increased our lending provisions to $657 million to reflect the economic outlook from expected COVID-19 impacts. The economy has performed better than expected and, as such, our lending provision levels have reduced to $525 million, representing 0.6% of our total lending portfolio," Power says.

Figures released by Aussie parent Westpac Banking Corporation show Westpac NZ customer numbers dropped 10,000 to 1.33 million in the September year from 1.34 million. Branch numbers fell to 116 from 143, and ATM numbers were down to 464 from 495.

Power says customer numbers have been "flattish" year-on-year.

"We've been working hard with existing customers to deepen those relationships with them. We're keen to make sure we're growing the franchise and that's very much a focus for the year ahead," says Power.

Westpac Banking Corporation announced an A$3.5 billion off-market share buyback alongside the group's 105% increase in annual cash earnings to A$5.352 billion. Westpac's also paying out A$2.2 billion to shareholders through a final dividend of 60 cents per share.

Meanwhile the Westpac Banking Corporation also said; "our New Zealand business is reviewing its processes for some products relating to the requirements of the New Zealand Credit Contracts and Consumer Finance Act 2003. The outcome of this complex review is uncertain and could result in customer remediation, regulatory action and litigation."

The charts below, covering Westpac NZ, come from the Westpac Banking Corporation.

9 Comments

nice

For a country with just 5,200,000 people, that's a super-profit.

Westpac (and the other NZ trading banks) ought to be forced to pay a "social dividend" back to the community.

TTP

nice

nice

While the Government and RB are screwing the general public so comprehensively, it is good to see that they have their priorities right and are looking after the banking sector so generously.

in 2019 when full data was available the 4 big banks profits combined was equal to over half that of the top 200 companies combined. It seems to me that this is obscenely disproportionate compared to what they actually contribute. All they really do is just keep track of money via computers.

AS John F Kennedy said

"Those who make peaceful revolution impossible will make violent revolution inevitable"

I think that the increasingly violent Anti Vax protests have more to do with the governments total failure to look after the well being of our people and instead favor sectors such as banks and the wealthy. Affordable housing and immigration is at the core of most of these issues.

We are headed on an ever steepening path to something like an unstable violent South American banana republic. Best thing for young and possibly even older people is to get the hell out of here while you can.

"get the hell out of here while you can."

Where to? ALL the financial markets of the world are controlled by the Collective of Central Banks. (eg: Draghi, ex-ECB chief now Italian PM - not by popular mandate but by appointment) There is nowhere that is exempt from their clutches. I could have settled in quite a few countries, but I emigrated to New Zealand, as it looked like 'the last place on Earth' that stood a chance of remaining fair and equitable. And look how that's working out!

Nope. I'm afraid we're all in the same leaking boat and our economies will go down together.

Iceland? (bit cold, but interesting)

They gave the world banking system the fingers. It was tough for a few years but now they are fine.

Australia are far tougher on the banks. (not enough) and governments are far more loyal to their citizens. For all their drawbacks, there is a real matey fraternal loyalty across Australian culture, (except for Sydney where it is dog eat dog and every man for himself)

Apparently, 20% of Westpac's outstanding mortgage debt was written in 2021. The year of the Covid crisis.

It's unclear if this includes refinancing.

Very interesting Twitter thread.

https://twitter.com/AvidCommentator/status/1454967473216757764

Were not Westpac NZ threatening to leave New Zealand less than a year ago?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.