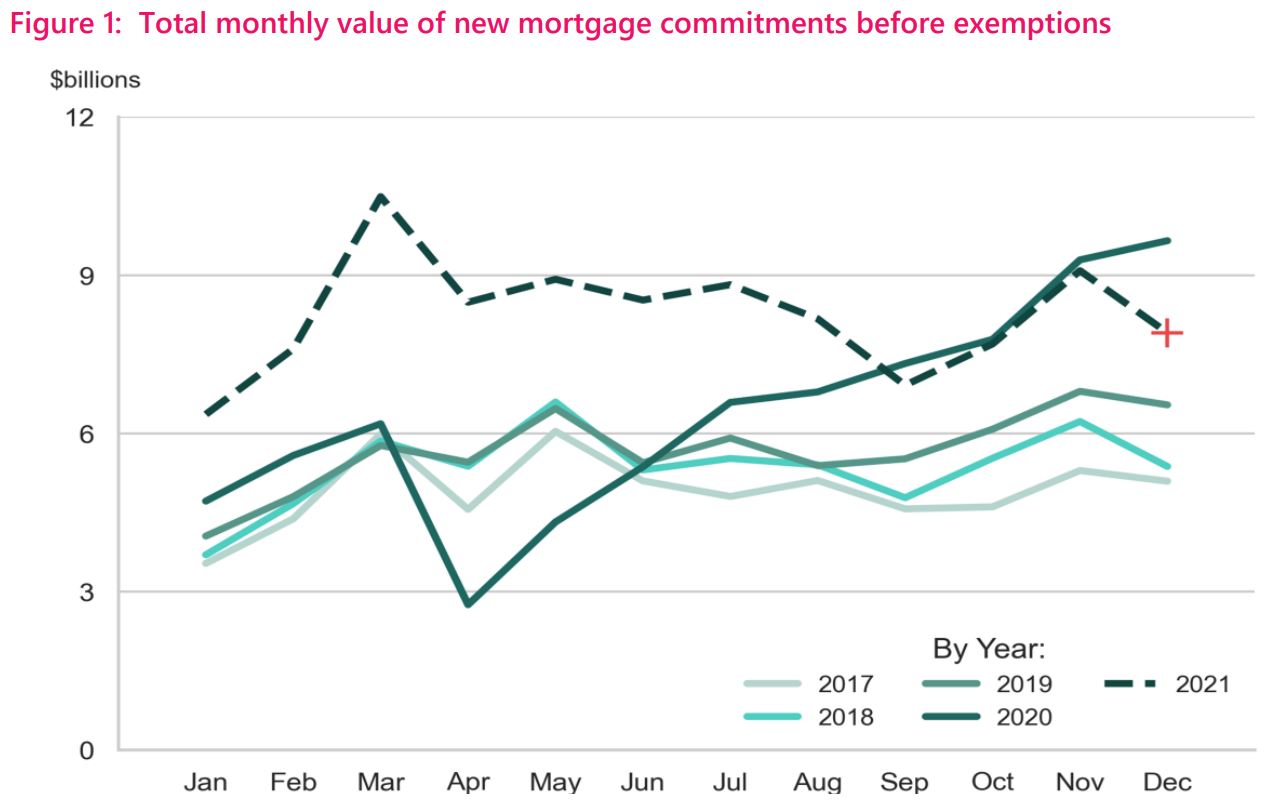

The value of new mortgages issued by banks fell in December 2021, but not by as much as news headlines of a looming “credit crunch” might have suggested.

New Zealand-registered banks issued $7.91 billion of new mortgages in December, according to new Reserve Bank (RBNZ) data.

This was 18% less than the value of new mortgages issued in December 2020, and 13% less than in November 2021.

But the value of new mortgage lending in December 2021 was still 21% more than the value of new mortgage lending in December 2019. It was also just below 2021’s monthly average of $8.25 billion.

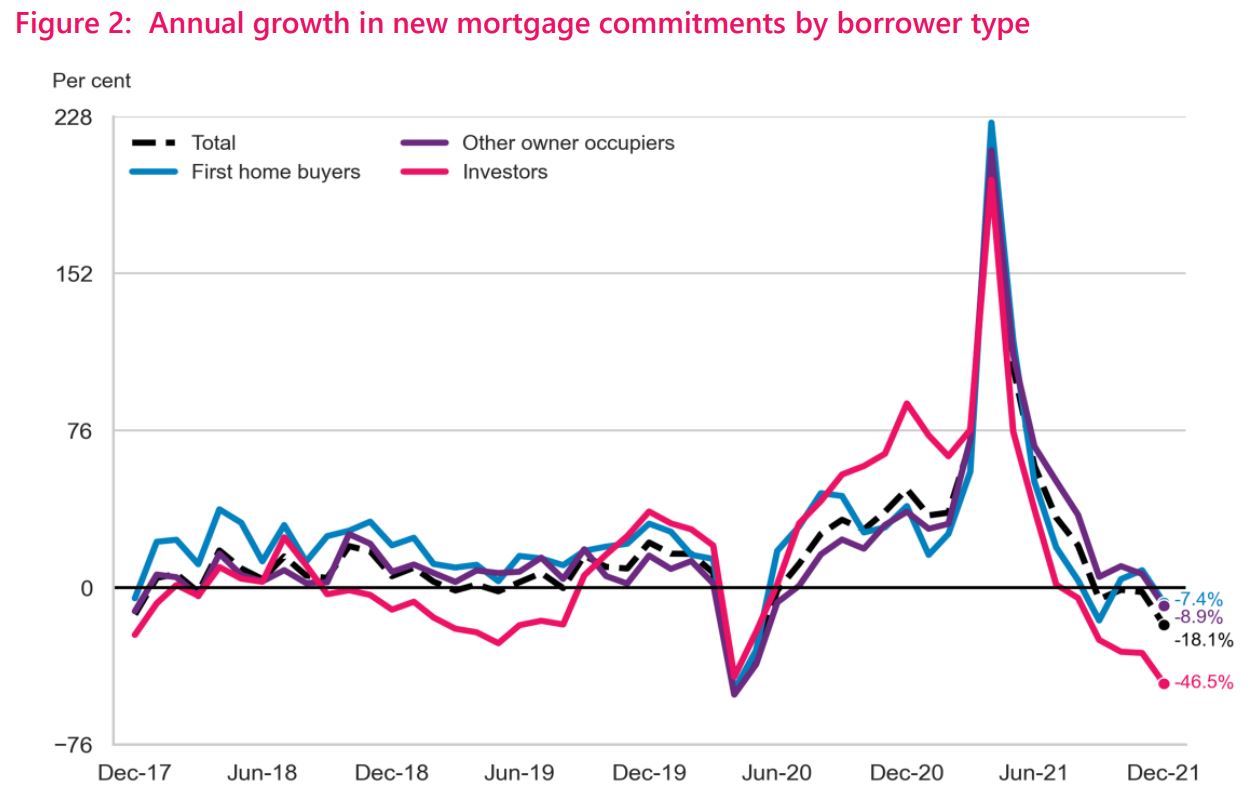

Both the annual and monthly falls in mortgage lending were led by drops in lending to investors.

The RBNZ recognised, “There is often a seasonal fall in new mortgage commitments in December months due to mortgage lending turnover slowing down in the lead up to Christmas and fewer working days for lenders.

“In the current market, a variety of other factors could have influenced the fall, such as rising interest rates, loan-to-value ratio (LVR) policy tightening, and the introduction of the Credit Contracts and Consumer Finance Act (CCCFA).”

CoreLogic Chief Economist Kelvin Davidson said it was difficult to know the extent to which CCCFA changes, which kicked in on December 1, tightened credit conditions when there were a number of other factors at play.

Lenders are (among other things) required to ask more questions of prospective borrowers under the CCCFA. This new law has seen aspiring homeowners make news headlines for having their loan applications declined.

The situation has caused such a stir, Commerce and Consumer Affairs Minister David Clark has asked the Council of Financial Regulators to review the law change.

However, first-home buyers accounted for a greater share of new mortgages commitments in December 2021 than they did in November 2021 - 19.8% compared to 19.1%. This was close to their record of 20.4% reported in June 2020.

The share of new loans to other owner-occupiers and investors fell slightly to 62.6% and 16.6% respectively.

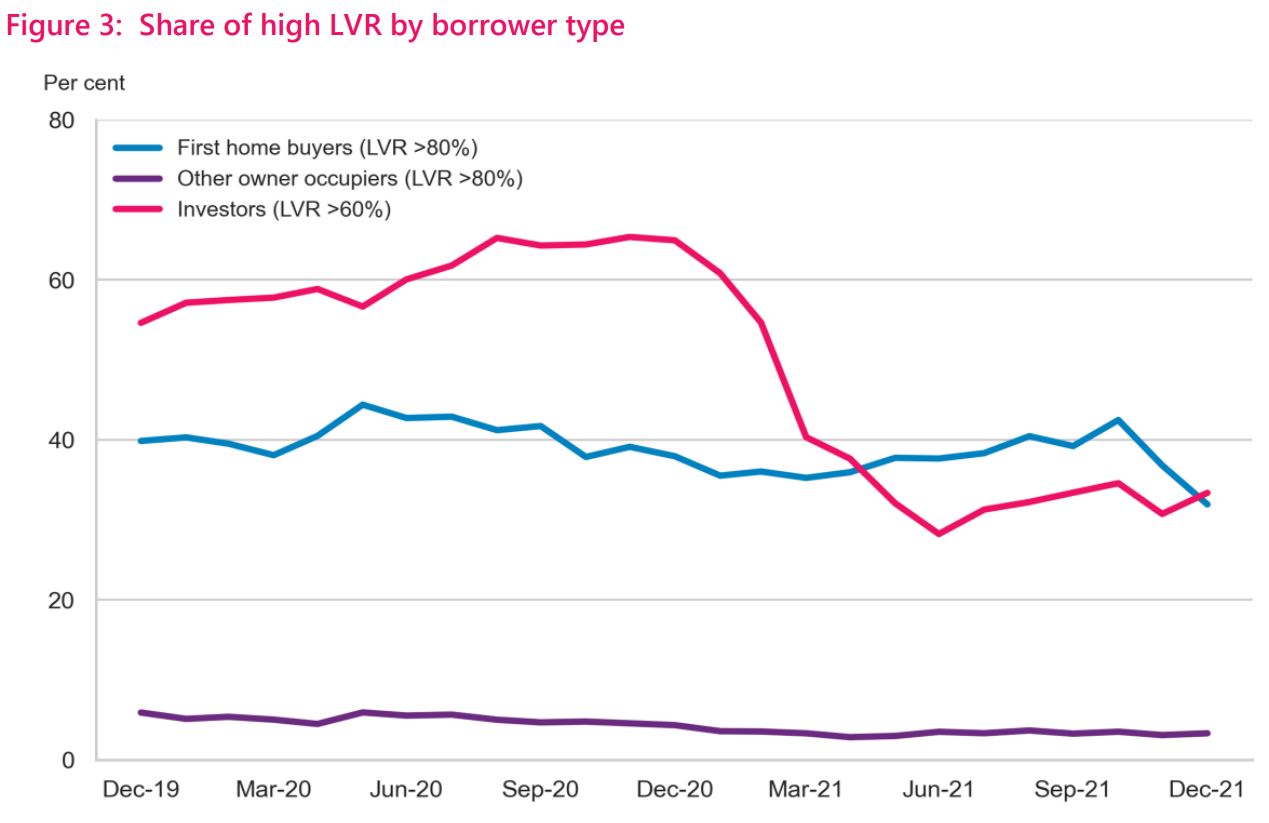

Nonetheless, first-home buyers with small deposits struggled under tighter LVR rules. The share of high-risk or high-LVR lending that went to this group fell in December.

Only 31.9% of new mortgage lending to first-home buyers went to those with deposits of less than 20%. This was the smallest portion since mid-2018.

Under LVR rules that took effect on November 1, 2021, no more than 10% of banks’ new mortgage lending to owner-occupiers can go to those with deposits of less than 20%. Previously this allowance sat at 20%.

In December, 9.1% of all new owner-occupier lending went to borrowers with deposits of less than 20% (after exemptions). In the months prior, this portion sat at around 11%.

Davidson suspected this portion could fall to 5%, as banks give themselves a buffer to avoid breaching the 10% limit.

29 Comments

Housing market has peaked. I'm ready to make the call.

Not a crash mind you.

$7.91billion is a whopping amount for a mere month…..

TTP

It is, but what matters is growth, and growth is relative.

TTP - let's not forget the golden rule in the NZ real estate industry "What goes up, must always go up"

Peaked in NZ. Not a chance.

This is the only hobby of kiwis, buying houses.

They will just keep on pumping all the money into the houses.

The best thing kiwis look forward in a weekend is open homes. They start lining up for those from Friday.

This is an obsession now.. If one wants to go a thesis, I can give you a good subject, " the excitement of a kiwi couple when they go up look for new open home".

They run around like chicks to every corner of the house and land around it ( no land these days in New coops) so excited. Sometimes might have to tell them to calm down.

detecting a bit of casual racism there, eh... not to mention your user name.

I'm sure many pundits would argue that years of low quality migration has added to the fire.

Interdsting. One then wonders why are the vested interests (brokers, agents, etc) are all screaming from the heavens about the CCCFA?

These figures will reflect sales from October and November in all likelihood. There's a lag in there.

Jenee - FHBs are only a greater % because investors have fallen off a cliff!

But, the data is a bit contrary to the narrative around the CCCFA - one might have expected the FHB numbers to be down more than they are if CCCFA was having such an impact.

Maybe there was huge FOMO late last year, and although the total mortgage approvals for FHBs held up OK, maybe mortgage application numbers were much higher?

Yes, but investors falling off a cliff is old news/been the trend since the RBNZ tighten LVRs right up for them. But perhaps it's best I make that clearer in the story.

How hard could it be for some sort of limit to be imposed on investors? A limit of say 3 houses, would be a great place to start. ( I know many with 7+)

Goldilocks scenario. Not too hot, not too cold.

I have a feeling people will lose a bit more than their porridge

Investors have left the building

Ideal time for FHB to climb on the latter as housing teeters on a precipice

It's not that good but it's not that bad, so why cry on mortgage lending growth and rules.

Let FHB cobble together big deposits to keep the market go up and up.

We only have 25,000 Plus homes advertised on Trademe now, was 19,000Plus a week or two back.....sad to see such a poor selection, that are way over priced and in locations that no one wants to locate to.

The average punter needs a home to live in, not a ramshakled heep of junk, or an over priced and under funded millstone around their neck for the next 30 years.

There are some Life Sentence Blocks, but nil return on acreage and nobody to pick a bucket or two of rotting crops is not a job for life, I would Want...Thanks anyway.

Even a few Mortgagee sales to set the ball rolling again.......may be miss construed as a bargain.

I am so surpised we have 50% rental Houses, that burn a hole in a renters wages, but surprisingly Most are not owned by the Big Dipping Banks....as yet.

This Dodgy Business of NZ Houses, on shaky plots and low lying Sea Scapes and ex Tourist Destinations and Tumbledown Shacks, not to mention, unseasoned Timber and Leaky Buildings is going to prove a point, when a Real, Real Estate Evaluation comes to the Fore......Covid has shown how real-istic real estate Motels and Flop Houses are so needy, by the Needy.

Buy a home to live in for life, not an Investment Plot that was initiated by Clowns who run our OCR Debt up to the Hilt......Leverage is so easy, to get, or used to be the only Game In Town for InvestMent Purposes. I often wondered why the Banks pushed that mularky....

It was to Fulfill the dreams of Investors.......and Share in the Screwing of Term Deposit Holders and Savers...

Some hopes now.....Covid will see the Prices Rising Daily..........to put a meal in yer Mouth......Not a stupid low down initiated Blood Bath in Initiated Mortgages.

The Devil is in the detail...It aint just NZ that is plunging its Toe in the Dyke....but theirs is called Red Sales in the Sunset.........and over priced, Pumped and Dumped. rinse and repeat.........Sharemarket...Trash.

DUH!...Thanks for the Catch-Up. See ya....but not a Penny, Nor a dime....will change my Mind....Fraud is Fraud. 1987 crash....Printed Munny is not Funny....when the truth hits the Internet, plus or minus a little exchange rate. Daft, but so True. Screw you folks....and they just did again. NZ drops....more than Savers GET......in Banks.

Sad eh....

Happy New Year......Covid not withstanding.

reading this is like reading an insurance contract. They are all technically words, but strung together in such a way as to befuddle the reader.

This was 18% less than the value of new mortgages issued in December 2020, and 13% less than in November 2021... but the value of new mortgage lending in December 2021 was still 21% more than December 2019.

This statement is correct in the nominal sense.

However, accounting for inflation, the overall rate for comparisons are as follows,

(Changes in December amounts)

2020 / 2021 -22.679%

2019 / 2021 12.514%.

Therefore the growth and decline of mortgage lending is over and understated based on the reporting numbers.

The effect can be seen in this chart. The use of nominal numbers masks the real growth rates of mortgage lending and coupled with an anomaly year distorted the trend. This leads to faulty assumptions in mortgage growth and wolf crying on impending apocalypse.

The real growth rate is much more gradual than many proclaimed and 2020 being an anomaly, we should expect the numbers to return to its long-term mean (ie. we don't have an issue to begin with).

So that brings up the question, what's the motivation behind CCCFA?

New Zealand-registered banks issued $7.91 billion of new mortgages in December, according to new Reserve Bank (RBNZ) data. This was 18% less than the value of new mortgages issued in December 2020, and 13% less than in November 2021. But the value of new mortgage lending in December 2021 was still 21% more than the value of new mortgage lending in December 2019. It was also just below 2021’s monthly average of $8.25 billion.

“Ultimately there’s no natural income streams to be able to service and repay loans. What you have is capital gains which are contingent on the game continuing. So it’s a Ponzi scheme. says Werner. - https://wire.insiderfinance.io/richard-werner-qe-infinity-707e2c627e03

He uses the term 'ponzi'. Some people here don't like that.

December is quite early to judge the credit crunch effects of the CCCFA so far.

The majority of kiwis want housing prices to fall. Interesting poll tonight. Now all we need is a political party that campaigns on this and delivers their mandate, a reserve bank that gets paid for more than cocktail parties, and a realization that the average kiwi house is a dump, and buyers that should think about moving to other countries, where they are more than cannon fodder for the capital class.

Yet again I heard the excuse tonight from a politician that we shouldn't complain about inflation because it is happenning in other countries. Well if we had interest rates we wouldnt have inflation, because money would be worth something and people would say no to ridiculous prices and gougers would go bankrupt.i dont vote in other countries. I vote and live in this one and with inflation at 6%..interest rates should be at 8%?. This ain't rocket science, just a lot of elites getting paid a fortune to screw things up.

Jim

Are you referring to seven house Luxon, four house Bridges or another politician??

I'm fairly sure the last politician to suggest that house prices should come down was Meteria Turei.

Taint just the House prices that need to come dowm...

Calls for price freeze on essential items as cost of living skyrockets (msn.com)

Putting a roof over yer head is one thing...

Putting a meal on the Table ...another.

This inflated, inflationary Prices are going to see a lot of weight lost and more people on the Dole.

Those Politicians and Bankers who Prey on the Housing Market and the Taxpayer funded Benefits endured, does not a Covid endured Policy fund-a-mental make.

Screwing Peter to Pay a Jacinda/Robinson/Orr inspired Regime is not what the Country needs. Nor a National Rip off Artistic future.

When Sanity gets back to normal....half the citizens may need a Bail-out.

When and if sanity does not prevail, then them Kitchens for the poor and weary, may need to be extended to us Mere Mortals... who aint got a Brass Razoo....but a Super Super Superior Intelligencia that put all their Trust in a House...

Rentals be blowed. Tax the Speculators to high heaven.....Let them eat Humble Pie......and see how they like it......when all is said and done.

Funds are to be respected....as long as we may shall live......Stop conning the Middle Classes. This is not a Communist State but it appears heading that way.

Monopoly will always be the game of this world. Own more properties, the wealthier you will be.

NZ has not even closed to peak. We have just started the game. The gap between rich and poor will continue to widen. I've seen what it has done in many places, NZ is following the same course.

I remember for over 17+ years that I would "wait" for the crash. That crash never happened. If I only had not listen to myself, perhaps I would've had at least 1 property fully owned by myself.

For those who want to wait, all the best, but it will only go higher...

Truth be Told....How can you tell when a Polytician is Miss-Leading.

PM 'absolutely refutes' that high spending led to record inflation (msn.com)

Check it out......Record it for next election...

Duh.

Yet...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.