BNZ's half-year profit rose 7.4% as income rose and expenses fell.

BNZ's net profit after tax for the six months to March 31 rose $49 million to $709 million from $660 million in the six months to March 2021.

The increase came as the bank increased operating income 7.1% to $1.498 billion, with net interest income up 7.5% to $1.154 billion. In contrast operating expenses fell $11 million, or 2.2%, to $489 million. Gains less losses on financial instruments such as hedging products were up 13.3% to $153 million.

Costs fell after BNZ was able to release a $35 million holiday pay provision booked in the September half last year. The provision release follows a Court of Appeal judgment in a broader Holidays Act case featuring Metropolitan Glass.

The bank reported a credit impairment charge of $21 million versus a write-back of $17 million in the March 2021 half.

BNZ says lending, boosted by home loan growth, rose 7.8% to $97.8 million, and deposits and other borrowings increased 9.1% to $80.4 million.

Mortgage serviceability test rate under review

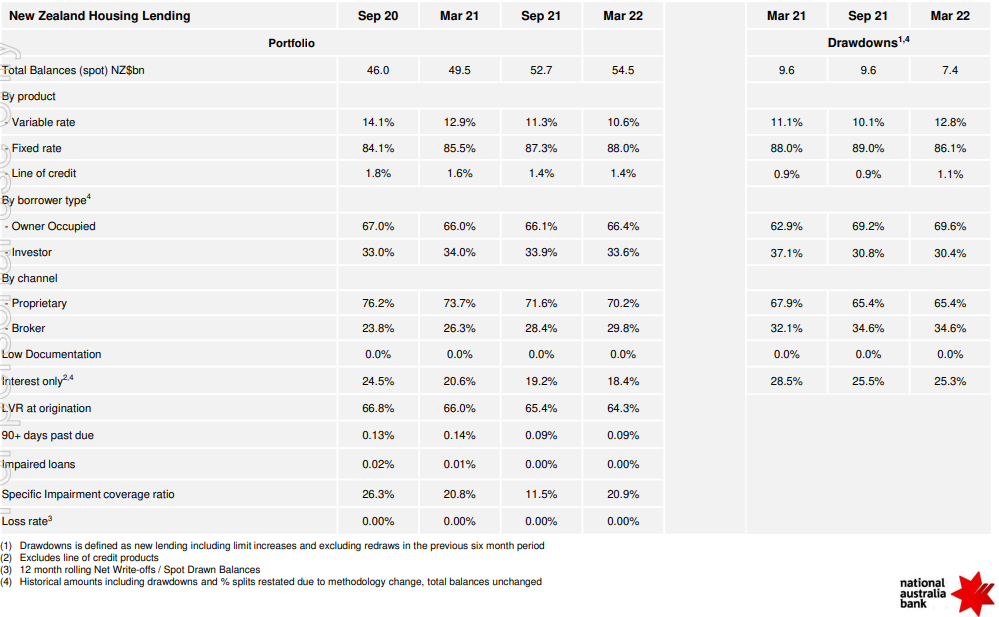

Year-on-year BNZ's housing lending grew $5 billion, or 10%, to $54.5 billion at March 31. Housing comprises 55% of BNZ's total lending.

Disclosures from BNZ's parent National Australia Bank (NAB) show BNZ's home loan portfolio had an impaired loans ratio of 0.00% at March 31, with just 0.09% of the portfolio at least 90 days past due.

BNZ's serviceability interest rate, the rate it tests mortgage applicants' ability to repay at, is currently at 6.75%. CEO Dan Huggins says this is under review and he expects it to increase, possibly as soon as next week. After increases this week, ASB's now at 7.35% and ANZ at 7.15%.

NAB says BNZ's overall housing portfolio is well positioned for the higher living costs and rising interest rates being felt by customers, with 46% of BNZ's housing book running ahead of scheduled repayments. Additionally its own loan-to-value ratio speed limits are lower than those applied by the Reserve Bank.

BNZ's half-year net interest margin dropped two basis points to 2.02%, and its cost to income ratio fell 310 basis points to 32.6%.

NAB reported a 4.1% rise in half-year cash earnings to A$3.48 billion. NAB's interim dividend is up A 13 cents to A73c per share, giving a payout ratio of 68.3% of cash profit.

NAB's return on equity rose 20 basis points to 11.3%, with its net interest margin down 11 basis points to 1.63%. NAB's Common Equity Tier 1 capital ratio rose 11 basis points to 12.48%.

BNZ's home loan book

*The links below take you to BNZ's statement and others from NAB.

2 Comments

So they're making money over fist, but applying a higher stress test rate, cause you know, some silly customers may have borrowed too much.

If there's one thing we can all be thankful for during these tough times for many New Zealanders it's that the banks are making record profits and the finance minister is pushing to put in a bank protection insurance scheme to keep them in gravy at a cost to taxpayers should job losses happen.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.