BNZ's interim profit surged 80%, helped by a positive turnaround in credit impairments, solid revenue growth and significantly lower expenses.

BNZ's net profit after tax for the six months to March 31 rose $293 million, or 80%, to $660 million from $367 million in the equivalent period of the bank's previous financial year.

The bank recorded a $17 million credit impairment write-back in the half-year versus a $151 million charge in the March half last year. Gains less losses on financial instruments used for the likes of hedging also contributed to the profit increase, coming in at $135 million versus $76 million.

Meanwhile, total operating income rose $91 million, or 7%, to $1.399 billion with net interest income up $22 million, or 2%, to $1.073 billion.

Operating expenses fell $147 million, or 23%, to $500 million. Lower expenses helped drive a massive reduction in BNZ's cost-to-income ratio, down 1375 basis points to 35.7% for the March half from 49.5% in the equivalent period of the previous financial year.

BNZ chief financial officer Peter MacGillivray told interest.co.nz the key factor in the cost reduction was the acceleration of depreciation on internally generated software in the March half last year. This led to a charge of $151 million that wasn't repeated in the March half this year.

"So on an underlying basis costs were pretty flat," MacGillivray said.

BNZ's net interest margin was three basis points lower, year-on-year, at 2.04%.

Housing lending surges

BNZ says loans and advances to customers rose 3% between September 30 last year and March 31 this year to $90.7 billion, and deposits and other borrowings increased 2.6% to $73.7 billion.

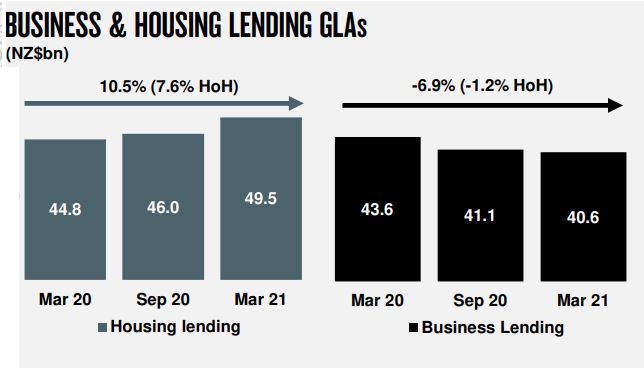

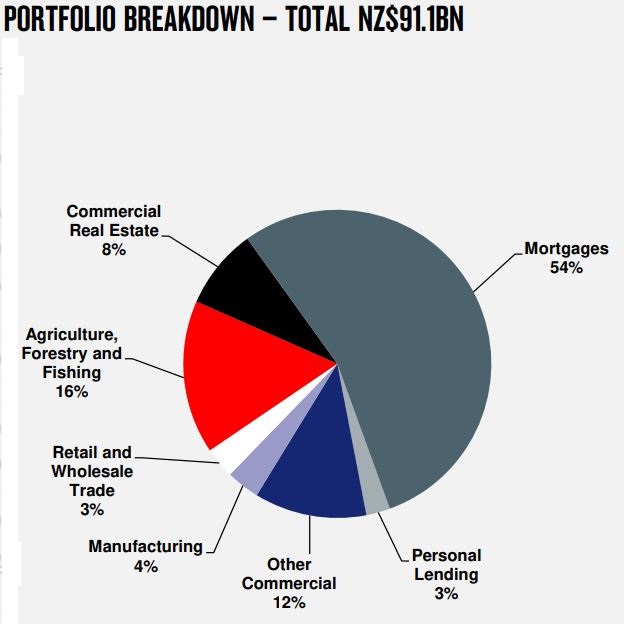

Figures from BNZ's parent National Australia Bank (NAB) show BNZ's housing lending grew $3.5 billion, or 8%, between September and March to $49.5 billion, and business lending shrank $500 million, or 1%, to $40.6 billion. Figures from NAB also show BNZ's lending to investors at 35.5% of total housing loans, up from 33.8% a year earlier. Record home loan volumes pushed housing lending as a percentage of BNZ's total lending to 54% at March 31, up from 50% a year earlier.

"We're a little bit over 18% of the investor market at a total level," MacGillivray said. "We're very comfortable with flows we have into our book, both owner-occupied and investor, and we're comfortable with the levels we've got."

"I think in terms of what we have seen over the last eight weeks is a slight reduction in some of our investor applications, which I think is a direct correlation to the government announcement...We do expect the housing credit system to slow based on the announcements from the government."

CEO Angela Mentis told interest.co.nz BNZ's housing market share was about 16.23% as of March.

Mentis confirmed BNZ has dipped into the Reserve Bank's Funding for Lending Programme (FLP), using $1 billion for a "Good to Grow" scheme. She said this is to provide "additional continued support" to businesses. Mentis said BNZ has also used its full allocation of $1.5 billion from the Business Finance Guarantee Scheme, supporting more than 1200 business customers.

BNZ's FLP admission confirms ANZ is the only major bank not to have accessed the FLP.

BNZ's not paying NAB an interim ordinary dividend, and reported a total capital ratio, as a percentage of risk weighted assets, of 16%.

"We'll reassess that [dividends] at the full year. NAB has got over $10 billion invested in New Zealand so it's important they get a return on that, but we'll assess that at the end of the year," MacGillivray said.

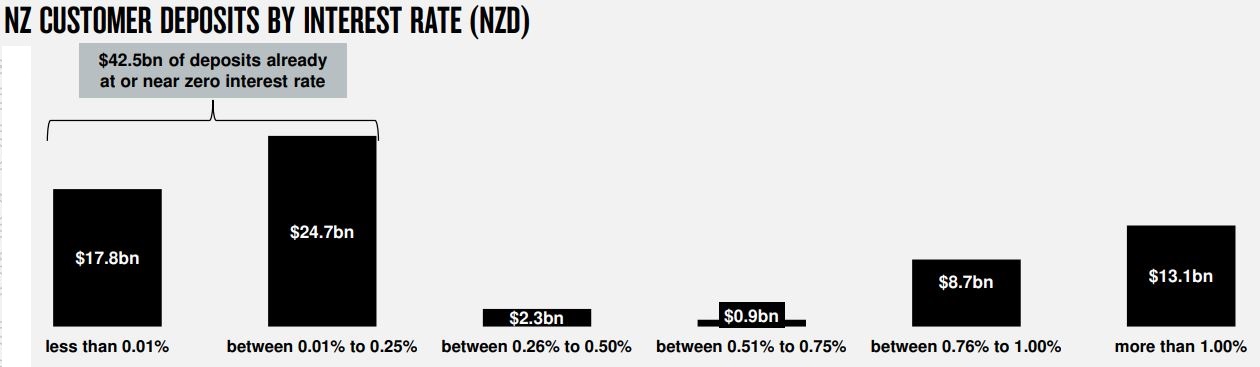

$42.5 billion of deposits at or near zero interest rates

The charts from NAB below include one showing BNZ has $42.5 billion of deposits at or near zero interest rates.

Mentis said it's important for savers to have a "financial health check conversation" with a BNZ banker, to help ascertain what their goals are, what the right products are for them, and the right way to achieve their goals.

(Note, GLAs is gross loans and advances).

6 Comments

Banking is a licence to print money in more ways than one. Warren Mosler describes banks as " public/private partnerships, established for the public purpose of providing loans based on credit analysis. Supporting this type of lending on an ongoing, stable basis demands a source of funding that is not market dependent. Hence most of the world’s banking systems include some form of government deposit insurance, as well as a central bank standing by to loan to its member banks".

https://www.huffpost.com/entry/proposals-for-the-banking_b_432105

WTF is it not time we got better TD rates and the $100k insurance thrown in for free ?

Exactly. According to the Reserve Bank, the new capital requirements mean banks will need to contribute $12 of their shareholders' money for every $100 of lending up from $8 now, with depositors and creditors providing the rest.

A pedantic but important point - the bank will have to hold $12 of capital (inc financial assets like bonds) for every $100 they loan out. Banks never, ever lend out their deposits or 'contribute' cash to loans from deposit accounts - they create new money with every loan. So if a bank lends you $100,000 the amount of money in their reserves doesn't change a cent. They just add $100,000 to their financial liabilities and an IOU for $100,000 to their assets (i.e. balance sheet expansion).

Banks are making hay out of their 'death pledges' which are ensaring more and more housing FOMO Kiwi's at nosebleed prices, while they return virtually nothing to deposit holders. What a sick situation. I'm taking to steps to wind down the amount of cash I have in the bank.

Yea im going to convert mine to a USD stable coin and deposit it with Nexo, celsius or blockfi and earn 10% pa on it. no point keeping any more $ in NZD than i need too.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.