By Gareth Vaughan

BNZ has topped up its loan provisioning by $108 million, lifting total provisions to $776 million against a $90 billion loan book, as it settles into a world ravaged by COVID-19.

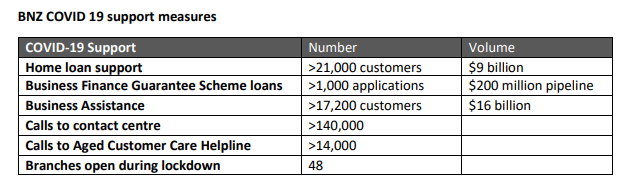

The bank also says it has provided assistance to 16,000 home loan customers and 17,000 business customers covering combined loan volumes of $23 billion.

BNZ on Tuesday posted a $183 million drop from last year's record high interim profit thanks to a software capitalisation policy change, a big rise in credit impairments and higher operating expenses. BNZ says net profit after tax fell 33% to $367 million for the six months to March 31 from $550 million in the same period of its previous financial year.

The bank said without a software capitalisation policy change that reduced its capitalised software balance, net profit after tax would've fallen $74 million, or 14%. Software capitalisation involves the recognition of internally developed software as fixed assets. The policy change increased the minimum threshold at which software is be capitalised to $5 million from $2 million.

BNZ reported credit impairments of $151 million versus $46 million a year earlier, and $68 million in the six months to September last year. The increase stems from an "economic adjustment" to the uncertainties and challenges of a COVID-19 world.

CEO Angela Mentis told interest.co.nz it was an unprecedented and very challenging time for everyone, with "a once in a hundred year public health shock that's having such a profound impact on economic and financial systems around the world and in New Zealand."

Mentis said BNZ sees the economy contracting by about 9% during 2020 as unemployment "goes towards" 10% and "house prices come off" by about 10%.

Chief financial officer Peter MacGillivray said on a business as usual basis BNZ's loan provisioning, being expenses reserved for default/bad performing loans, would've been about $43 million.

"[But] we took the opportunity based on various scenarios we've run and those key economic indicators around GDP, unemployment and housing, and we included a $108 million top up to our economic adjustment, and that then provides a total provisioning number of around about $776 million on our balance sheet," MacGillivray said.

The bank reported total operating income rose $15 million, or 1%, to $1.317 billion, with net interest income up $17 million, or 2%, to $1.051 billion. Operating expenses rose $164 million, or 33%, to $656 million.

BNZ said loans and advances grew 2% in the March half from the September half to $89.5 billion, and deposits and other borrowings grew 7% to $73 billion from $66.4 billion. At March 31 total assets reached $118.5 billion, up 9% since September 30.

The bank outlined its COVID-19-related customer assistance efforts, detailed in the table below.

"Together with the New Zealand Government and Reserve Bank, our focus has been on rapidly responding to assist our customers as they navigate this very difficult time," Mentis said.

"I have spoken to over 100 businesses. Everyone is using it as an opportunity to really look at their businesses, what is their cost base, have they moved their fixed costs to variable? I've also heard of many businesses using this as an opportunity to go digital. [And] a lot are looking at right sizing their businesses as well," Mentis said.

Capital 'strong'

MacGillivray said BNZ's capital position is strong, with a total capital ratio of 14.1% as a percentage of total risk weighted exposures, and a common equity tier one capital ratio of 11.6%. The Reserve Bank mandated minimums are 10.5% and 7%, respectively.

He also said the bank had seen "quite an inflow" of customer deposits over the last five weeks, whilst at the same time the "housing market has slowed considerably," without providing specific details.

In terms of past due loans or defaults, Mentis and MacGillivray said they weren't seeing immediate stress, and the support measures taken by the Government, Reserve Bank and banks "will cushion some of that blow across New Zealand businesses and consumers."

MacGillivray said BNZ has utilised the Reserve Bank's Term Auction Facility, which lends money to banks for up to 12 months, but just via a couple of transactions to date with one being a test. It has also used the Reserve Bank's Open Market Operation (OMO), "placing some treasury notes and government stock" into the OMO, which is designed to inject cash into the banking system. He didn't provide details of the size of the transactions.

On Monday BNZ's parent National Australia Bank (NAB) posted a 51% fall in March half-year cash profit to A$1.436 billion as its credit impairment charge ballooned to A$1.161 billion from A$449 million in the March half last year. NAB also unveiled plans for a A$3.5 billion capital raise, and slashed its interim dividend by A53 cents to A30c per share, equivalent to just 35% of cash profit.

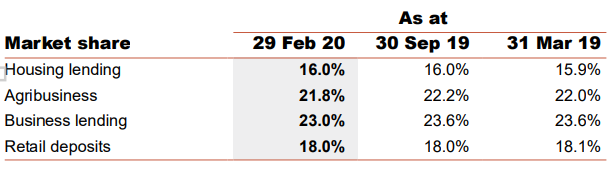

NAB said the net interest margin at its New Zealand banking unit fell six basis points year-on-year to 2.24% for the March half, with the cost to income ratio down 160 basis points to 36.2%. The table below, with NZ market shares, also comes from NAB.

37 Comments

Is still Kiwi Bank interested to buy BNZ ??

Never was. It was a 'think piece' by a journalist.

Merger would be more likely the other way around. By measures like net interest margin, cost to income etc. BNZ is a far better run company. One of the big four Australian banks could really add a lot of value to Kiwibank in a buy out situation. Not sure regulators would allow it however.

Why would Kiwibank ever want BNZ ?

Current circumstances notwithstanding, it has a rather impressive business customer book whereas Kiwibank doesn't. Possibly BNZ is the least exposed to residential housing outside of Heartland Bank, but a lot of small business lending is housing-secured.

Getting closer to a run each day.

And then what?

Property will be worthless, for starters. Who will want to swap if for 'cash'?

That house you have with a CV of $1,000,000 will be worth $10million and $zero at the same time. Schrodinger's Cat stuff....

Ditto everyhting else.

Yes I'm with you bw. Things could get out of control very quickly. The only safe place is to be mortgage free, 65 and older and own some gold, with hope that the government can keep paying super. Otherwise all bets are off with respect to the value of money, employment, wages, inflation, ability to service debt and who will be the ultimate holder of that debt.

Doesn't help the rest of us who don't that profile though does it.

No answer.

Ok. Well here's one!

At the moment we are operating a Financial System with part of it state-controlled -ie: interest rates, and part of it not ie: the other drivers of a financial system; those being

- The Exchange Rate, and

-The Trade Account.

So Fix that!

Either - Let the market set the appropriate price of % rates - scrap the OCR etc (my prefered option) or

Fix the Currency and Trade Account in a similar way the % rates.

That's an NZ$ fixed to, say, the US$ and Exchange Controls to regulate the flow of goods & services and, most importantly, Capital.

What do you reckon?

How long before the modern Bretton Woods? Late 2020?

We should absolutely be doing away with central bank interference in the markets. Scrap OCR, scrap OMO, scrap the lot. They should be a mint only.

Exactly right. In particular, constant and heavy interference with the markets by forcing artificially cheap money into the system has only created:

- the Ponzi scheme of the housing bubble

- no wealth creation, but debt creation

- systematic mis-pricing of risk (one of the main causes of the GFC)

- virtual killing of the bond market

Let the market freely discover its balance in areas such as housing, interest rates etc with no further damaging interference by the central bank. Excessive central planning does not work - yes there is room for some central economic policies, but we we should also have learned something from the collapse of economic Communism thirty years ago. The RBNZ (and other central banks) are progressively moving towards a very outdated and dangerous mode of meddling and direct intervention into the markets. It is going to be structurally damaging to the whole economy, and to a serious extent.

What they are doing is seriously unhealthy - they are trying to avoid the unavoidable: the very concept that any sound economic system is occasionally subject to recessions. And they are trading it for a progressively more and more inefficient zombie economy artificially supported by asset bubbles, where capital formation is killed, savers are punished, and as a result the economy is subject to a continuous, ongoing stagnation and lack of productivity increase.

Like this opinion

https://www.interest.co.nz/opinion/69243/opinion-there-alternative-offi…

Ah,BW that takes me back a bit to before Rodger the Dodger got his sticky fingers on the economy...fixed exchange rate, exchange controls, import licensing, etc etc... you know it might work..seemed to back then..

Those 21,000 'home loan support' applications make for a useful leading indicator to household debt serviceability. Using 2018 data BNZ had 16% market share of NZ mortgages that would imply 131,000 applications across all banks in NZ.

Things may well get very interesting come September.

source: https://www.interest.co.nz/news/93892/customer-support-home-loan-banks-…

Good point. I think banks typically give up to a 6 months window to get loan payments back on schedule.

Well capitalised

No risk

Equity not connected to dependency on assets which are in fact loans

No problem

Note: bad debt impairment tripled

After 6 weeks of virus

What happens when people start defaulting?

Banks are fine and safe unless there is a pandemic

Then not

Mark, I agree that too many people in too much debt is a risk. But purely from an individual bank perspective, this pandemic (and the consequent responses to it) would have put any banks in serious trouble regardless of the monetary policy or the level of credit creation. It affects the whole world, every single country. Even world wars have not done that. In fact wars prompt a lot of economic activities. This pandemic has brought the whole world to a halt. I may be wrong, but this is probably the first time in human history that the whole world has come to a halt like this.

Well capitalised

No risk

Equity not connected to dependency on assets which are in fact loans

No problem

Note: bad debt impairment tripled

After 6 weeks of virus

What happens when people start defaulting?

Banks are fine and safe unless there is a pandemic

Then not

What day is benefit day for some of you?

Stop worrying about house prices, it is eating away at you!

Start commenting when you know what is happening, when you have no idea it is pretty pointless.

House Prices aren't the problem, really. They are a symptom of the failure of our financial system to encourage the productive development of our country.

A house is Productive - once. When it's built. After that, it is a Consumption Item and should depreciate the way all other similar items do ( Think cars for an easy example). The newer the house, the more it should sell for relative to an older version on a like-for-like basis. Supply should not have the constraints is does just to manufacture 'wealth'.

That we have morphed shelter into a mechanism for 'wealth' creation is a poster-child of everything that is wrong without current economic setup.

Sorry mate but dont agree, unless you think rent should not exist and you either own or rent for free. Its a productive asset, just like a factory robot depreciates but still adds to economic turnover and output. Secondly, how new something is doesn't correlate to its value and sale price, a well looked after car or house that is 100 years old will sell for more than a new house or car, and definitely more than a cheaply build new house or car. New or old, doesn't matter, what matters is how people see it as valuable or useful or long lasting etc. I agree wealth doesn't get distributed as well as it should be atm globally, but to say as a human race we aren't better off than 3 decades ago is pure ignorance, the 5th, 10th, and 50th percentile of humanity lives much better today than any decade before. There is nothing wrong per say with economic setup, just with distribution of wealth, but thats just an argument of where to draw the line in the sand....

Some? Currently pretty much everyone is on some form of government paid benefit.

'Start commenting when you know what is happening, when you have no idea it is pretty pointless'

Oh the irony.

I don't see any mention of house prices in his comment - perhaps they are eating away at you, TM2?

He has been grumpy for some time. He often rabbits on about how safe property is as the owners of it are in control. Lockdown proved that theory to be absolute nonsense as the government of the day are in absolute control, not an individual or group of citizens. Time will tell us the amount but property values are sure to drop. We are going to experience fiscal conditions similar to if not worse than the depression.

Everyone will be fine as long as they have not overstretched themselves or bought in Christchurch

Can someone tell me why their operating expenses rose by 33%?

@linklater .............I re -read the article and it does not look like op costs increased by 33% , more like impairments have smacked profits

Op expenses have been falling, especially when all banks have been cutting the fat and reducing opex .

They have not opened new branches , so where are these additional expenses effecting profits ?

Its likely non-performing loans or impairments hitting profits ...............and lets not forget that provisions for bad debts have tax benefits for the Bank

Of all the banks, do you think Kiwi Bank might be the safest? As the government would save it and deposited money, Or would you split the amount in few different banks?

If you believe they are "too kiwi to fail" then they are safe. By the underlying business metrics then the Australian banks are far safer. In short keep money in Australian banks until the government have demonstrated they are unwilling to let OBR proceed, then switch to Kiwibank.

Maybe a good time to contact my local MP so he can ask the question in parliament of what the government's plan if the banks default with our money

Interesting NAB the parent has asked shareholders to stump up 3.5 billion, instead of issuing bonds. In the medium term its probably the shareholders that are the losers.

Re BNZ, they might be happy with 367 mill profit in the next 6 months, they might be happy with break even lol.

Good thing the 367 million will stay with BNZ with the dividend stops in NZ.

Even if house prices fell by 10% houses would still be way too expensive in Auckland .

Average housing costs should not exceed 1/3rd of household monthly in a best case or 50% of income in a worst case .

We need a sustained fall in house prices of 30% , and most of that can come from land prices falling

10% unemployment would seem disproportionately more than a 10% drop in house prices in my mind. A lot of rental income will evaporate in some areas, which means that some simply cannot service the debt on their investment income and it's sale time.

FYI from BNZ today:

30 April 2020

Correction to previous announcement

Bank of New Zealand (BNZ) would like to make a correction to its previous announcement entitled “BNZ: Robust and ready to help rebuild New Zealand’s economy” which was released on NZX on 28 April 2020.

Under the heading “COVID-19”, the number of customers supported by BNZ during March and April with new and restructured home lending should be 16,000 (not 21,000) and, under the heading “BNZ COVID 19 support measures”, the volume reported for “home loan support” should be $7 billion (not $9 billion).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.