By Gareth Vaughan

BNZ's parent National Australia Bank (NAB) has provided an earlier than expected taste of what the COVID-19 induced economic downturn means for banks, their shareholders and their bad and doubtful debts.

In a surprise move on Monday NAB issued its interim results, which hadn't been due until Thursday May 7.

NAB, under CEO Ross McEwan who took the reins in December, posted a 51% fall in March half-year cash profit to A$1.436 billion as its credit impairment charge ballooned to A$1.161 billion from A$449 million in the March half last year. NAB also unveiled plans for a A$3.5 billion capital raise, and slashed its interim dividend by A53 cents to A30c per share, equivalent to just 35% of cash profit.

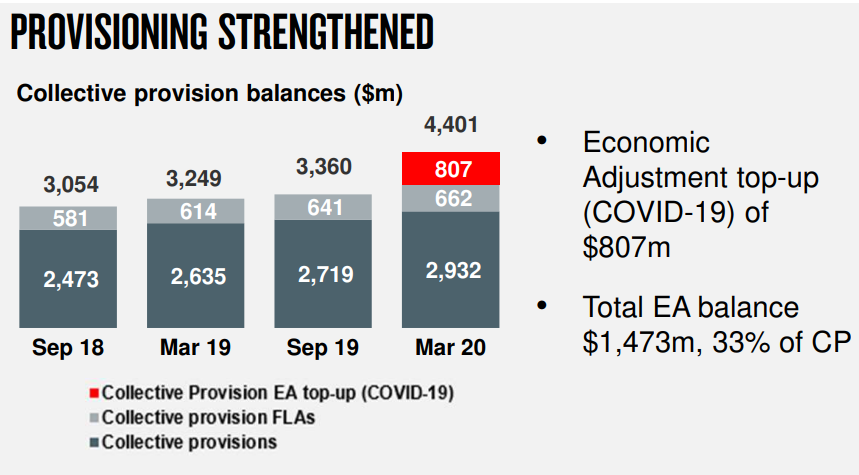

At its New Zealand banking unit NAB said cash earnings rose $30 million, or 6%, to $562 million. The rise came as net operating income gained 3% to $1.291 billion, and operating expenses fell $8 million, or 2%, to $467 million. The credit impairment charge dropped $2 million to $42 million although this excludes collective provision charges for forward looking economic adjustments due to the potential deterioration in broader macro-economic factors as a result of the COVID-19 pandemic. These were lumped in with the rest of the NAB group which recorded an A$807 million "economic adjustment" increase taking total collective provisioning to A$4.401 billion.

BNZ specific detail should be available Tuesday morning when NAB's Kiwi subsidiary issues its interim results after NZ's ANZAC Day public holiday.

Subsequently ANZ NZ, the country's biggest bank, is due to report interim results on Thursday (April 30), followed by Westpac NZ on Monday May 4. In the weakening economic environment banks' non-performing loans and provisions for doubtful debts have been expected to rise off a low base.

As previously reported by interest.co.nz, as of December 31 the three big NZ banks all had low levels of non-performing loans and loan provisions by historic standards. ANZ's non-performing loans ratio was just 0.5%. Westpac's was 0.3% and BNZ's 0.9%. This ratio covers loans recognised as impaired or where payment is at least 90 days past due. The non-performing loans ratio is total non-performing loans as a proportion of total loans.

Meanwhile ANZ's provisions, including individual plus collective provisions, stood at $505 million, Westpac's at $331 million, and BNZ's at $668 million. That's against total loans of $135 billion at ANZ, $89 billion at BNZ, and $86 billion at Westpac.

New financial reporting standard to make its impact felt

Since 2018 banks have had to use what's known as IFRS-9, or International Financial Reporting Standard 9. It replaced another standard known as NZ IAS (International Accounting Standard) 39.

This, as Michele Embling who chairs the External Reporting Board explains, means a significant shift. The old standard, Embling says, was based on events that had exactly happened at 31 March. Whereas the new standard looks at what had happened at March 31 but also looks forward, and needs to include future expectations.

"What we have with IFRS-9 is called an expected loss model where you take into account expectations of future loss and economic conditions. What might happen with unemployment rates for example, which is one of the biggest determinants of wealth," says Embling. She spoke to interest.co.nz on Friday, before the NAB results were released.

This means IFRS-9 is more forward looking than the old standard. "Which ideally means that losses are recognised sooner rather than later," Embling says.

The banks are expected to develop estimates based on the best available information about past events, current conditions and forecasts of economic conditions. When assessing forecast conditions, they should consider both the effects of COVID-19 and the government support measures in place. Payment deferrals for borrowers doesn't mean those loans should automatically be considered to have suffered a significant increase in credit risk.

The External Reporting Board is an independent Crown entity tasked with preparing and issuing accounting standards and audit assurance standards. Embling, who also chairs PwC NZ, says international guidance is relevant in NZ too.

This includes:

"It is likely to be difficult at this time to incorporate the specific effects of COVID-19 and government support measures on a reasonable and supportable basis. However, changes in economic conditions should be reflected in macroeconomic scenarios applied by entities and in their weightings. If the effects of COVID-19 cannot be reflected in models, post-model overlays or adjustments will need to be considered. The environment is subject to rapid change and updated facts and circumstances should continue to be monitored as new information becomes available."

And:

"Although current circumstances are difficult and create high levels of uncertainty, if expected credit loss estimates are based on reasonable and supportable information and IFRS-9 is not applied mechanistically, useful information can be provided about expected credit losses. Indeed, in the current stressed environment, IFRS-9 and the associated disclosures can provide much needed transparency to users of financial statements."

'A lot of subjectivity because things are uncertain'

So what is this likely to mean in practice? Embling suggests volatility.

"The challenge is this is the first time the standard has been tested because we've had this benign credit environment for 10 years. Banks' losses have been quite miniscule, compared to the size of their books," she says.

"And now we've got this significant volatility coming through, or potentially significant volatility, in economic factors over the next wee while...you should expect more volatility going forward."

"The key areas to look at will be the results as they're reported and what's coming through, but also the disclosures around the key assumptions that have gone into anticipating those losses because it's somewhat of an art as opposed to a science," says Embling.

"The disclosure piece from companies in this reporting season is going to be really important because there's going to be a lot of subjectivity because things are uncertain."

IFRS-9 is a response to the Global Financial Crisis (GFC) and criticism that banks were too slow to recognise the deterioration in their loan books and therefore record losses, Embling says.

"The losses eventually came but they were delayed. And so as part of the review post the GFC, the standard setters globally looked at the relevant standard of how you provide for impairment losses on loans and receivables including mortgages."

In the wake of the GFC the big five banks - ANZ, ASB, BNZ, Kiwibank and Westpac - had combined 90-day past due assets of $1.4 billion in the first-half of 2009, compared to pre-GFC norms of between $300 million and $400 million. Interest.co.nz first wrote about the potential move to an expected loss model in 2011.

BNZ was an early adopter of IFRS-9 in 2014, with ANZ and Westpac adopting it in 2018. Instead of the September year balance ANZ, BNZ and Westpac have, ASB and Kiwibank have a June financial year. That means they reported interim results, for the December half-year, in February and won't report June year results until August.

Pay cuts for BNZ's top brass

BNZ says its executive management team, including CEO Angela Mentis, will forgo the short-term at risk components of their pay packages, which could have accounted for up to 50% of their annual take home salary for the 2020 financial year. Chairman Doug McKay says BNZ's board will donate 20% of their directors' fees for the next six months to charities.

Meanwhile, in a letter to NAB shareholders McEwan and chairman Philip Chronican say, across the 70 years of experience in banking they share, they've never seen such an immediate and deep impact on the economy and health of the global community.

"Given the uncertain outlook, we are taking proactive steps to further strengthen our balance sheet. These actions are intended to provide us with sufficient capacity to continue supporting our customers through the challenging times ahead, as well as assist to manage through a range of possible scenarios, including a prolonged and severe economic downturn," NAB says.

"We have increased collective provisions for forward looking economic and targeted sector adjustments by A$828 million to A$2.135 billion. We are also bolstering our capital base, today announcing a fully underwritten institutional [share] placement of A$3 billion and non-underwritten share purchase plan targeted to raise approximately A$500 million, increasing our proforma common equity tier 1 capital ratio to 11.20%."

"The difficult decision to reduce our interim dividend by 64% to A30 cents per share is equivalent to a further A$1.6 billion, or 37 basis points of common equity tier 1 capital," says NAB.

NAB expects Australian Gross Domestic Product to fall 8.4% by September from where it was at last December, and not recover to pre-COVID-19 levels until early 2022. It expects Australian unemployment to peak at 11.7% mid-year, before recovering somewhat to 7.3% by December 2021.

The chart below comes from NAB's results presentation.

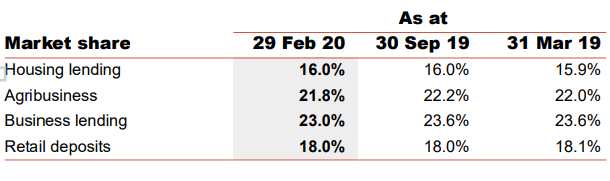

The table below, from NAB, shows its NZ market shares.

NAB's results release is here, and its investor presentation is here.

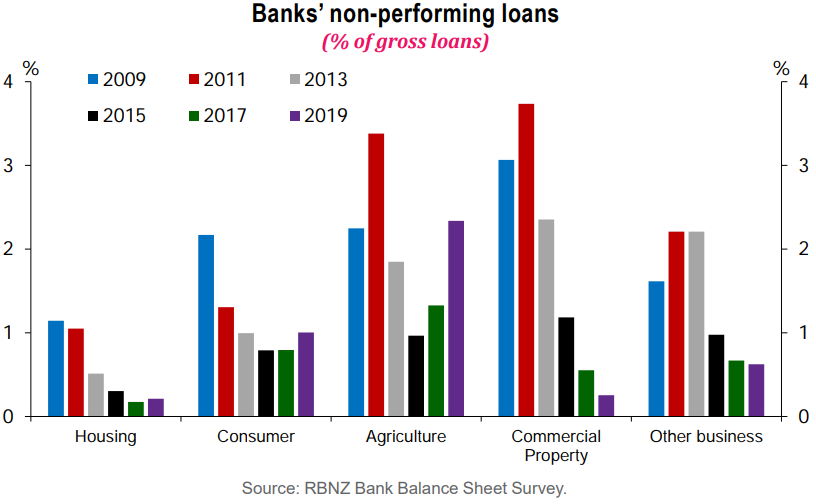

The chart below comes from the Reserve Bank of New Zealand and covers NZ banks.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

28 Comments

Here is something worth thinking about in terms of their house price assumptions

1) Base case - house prices fall 10%

2) Severe downside case - house prices 30% over 2 years. - " House prices would fall 20.9 per cent this year and another 11.8 per cent in 2021"

Page 20 - https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/1h...

Meanwhile the public in NZ are being reminded that there is an underlying housing shortage in NZ by the property promoters and those with a vested financial interest.

A reminder for all potential owner occupier buyers and current owner occupiers - choose your scenario and act accordingly.

Which will the owner occupier regret most:

1) missing out on future potential gains in equity?

2) potential loss of their savings invested as the initial deposit for purchase of the house or even potential negative equity?

For owner occupiers, a reminder of the impact of leverage (it amplifies property price changes both on the up and down):

Scenarios of financial impact of leverage on equity, assuming an 80% LVR for owner occupier, for a recent $100 property purchase, $20 initial deposit, mortgage $80.

A) Scenario - property price rise:

1) property price rises 5% to 105, mortgage 80, equity 25, so 25% gain in equity value from 20.

2) property price rises 10% to 110, mortgage 80, equity 30, so 50% gain in equity value from 20.

3) property price rises 15% to 115, mortgage 80, equity 35, so 75% gain in equity value from 20.

4) property price rises 20% to 120, mortgage 80, equity 40, so 100% gain in equity value from 20.

5) property price rises 25% to 125, mortgage 80, equity 45, so 125% gain in equity value from 20.

6) property price rises 30% to 130, mortgage 80, equity 50, so 150% gain in equity value from 20.

7) property price rises 35% to 135, mortgage 80, equity 55, so 175% gain in equity value from 20.

8) property price rises 40% to 140, mortgage 80, equity 60, so 200% gain in equity value from 20.

9) property price rises 50% to 150, mortgage 80, equity 70, so 250% gain in equity value from 20.

10) property price rises 100% to 200, mortgage 80, equity 120, so 500% gain in equity value from 20. (i.e if they believe that the property price doubles every 10 years)

Remember, the owner occupier must be able to hold on under ALL economic environments (including any potential significant reduction in household income).

B) Scenario - property price falls:

1) property price falls 5% to 95, mortgage 80, equity 15, so 25% loss in equity value from 20.

2) property price falls 10% to 90, mortgage 80, equity 10, so 50% loss in equity value from 20.

3) property price falls 15% to 85, mortgage 80, equity 5, so 75% loss in equity value from 20.

4) property price falls 20% to 80, mortgage 80, equity is zero, so 100% loss in equity value from 20.

5) property price falls 25% to 75, mortgage 80, equity is NEGATIVE 5, so 125% loss in equity value from 20.

6) property price falls 30% to 70, mortgage 80, equity is NEGATIVE 10, so 150% loss in equity value from 20.

7) property price falls 35% to 65, mortgage 80, equity is NEGATIVE 15, so 175% loss in equity value from 20.

8) property price falls 40% to 60, mortgage 80, equity is NEGATIVE 20, so 200% loss in equity value from 20.

I'm an owner occupier of the only property I own. I am mortgage free as well. The 'equity' value I have in my property is meaningless as it is relative to all properties. So if the value of my property falls, it will for all, (assuming market events, not localised natural events). The people who will be impacted are those who are leveraged, essentially still paying off a mortgage. All my life the advice I have received is pay off the mortgage, so i did through hard work, saving and no real lifestyle. COVID19 is exactly the type of event that the advice was foreseeing. I had friends who suffered during the '87 crash, and I recall the value of my property then fell as well. But I was newly married and with a young family and just continued as normal and by the time we did sell to move (from AK to Whangavegas) the prices had settled into a range that still gave us a deposit for another home.

Wonder if there are a few folk hoping they can offload quickly to someone else and let them take the loss instead.

Broken link above, so reposted here

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/1…

Ag stand out performer on non performing loans projected drop in dairy payout next season puts it as most vulnerable. Market share next to business highest share of loans . Housing may be easier to support by government via job support schemes etc but business and agriculture more difficult.

Shane Elliott (ANZ Group CEO) reported about a month ago that 18% of SMEs have requested payment deferral on loans while residential is only 5%.

During a recession return on capital becomes less concerning than return of capital.

Dictionary:

Nab - 'to take something suddenly, or to catch or arrest a criminal'

Both of these descriptions are very apt!!!

Wasn’t it the NAB CEO who made an absolute ass of himself with his rotten to the core attitude while being questioned during the Australian Banking Royal Commission?

Former CEO.

"The difficult decision to reduce our interim dividend by 64% to A30 cents per share is equivalent to a further A$1.6 billion, or 37 basis points of common equity tier 1 capital," says NAB..

How much of this reduction is due to a credible RBNZ policy restriction?:

“To further support the stability of the financial system during this period of economic uncertainty, we have agreed with the banks that during this period there will be no payment of dividends on ordinary shares, and that they should not redeem non-CET1 capital instruments,” Deputy Governor and General Manager for Financial Stability Geoff Bascand says. Link

Does anybody claim to have evidence of actions undertaken by the "Term Lending Facility (TLF)" mandate?

"What we have with IFRS-9 is called an expected loss model where you take into account expectations of future loss and economic conditions. What might happen with unemployment rates for example, which is one of the biggest determinants of wealth," says Embling.

What happens to this wealth expectation formula when 60% of bank lending is extended to one third of creditworthy households to undertake residential property speculation, rather than creating credit for GDP qualifying enterprises which employ people?

Two thoughts

1. It doesn't matter how many standard deviations your credit model is working when the event is potentially like the great depression

2. The business model is/was completely focused on property as loan collateral. So a genuinely large correct and all bets are off

This old boys banking club is going to bring the world to its knees with its ineptitude. Just because their daddy was a rich masonic banker should not mean they automatically get to be one. We need to get rid of the class system becoming more and more entrenched in NZ. Everybody should be given an equal opportunity. Nepotism is the scourge of this planet and enables incapable buffoons to think they are above us all.

LOL- Just because their daddy was a rich masonic banker should not mean they automatically get to be one.

I was approached to join the masons, in the James Cook Hotel piano bar, Wellington, which I was attending as a stockbroker, with others and our clients in the early 80's. I have a modest family background.

I've a close mate who is a mason, but I never talk about it with him. He is gradually staring to see how the world really works. He preferred information source seems to be TV, but has found Max Kaiser at least.

Absolutely not important story. Even one news is not reporting on it. No news.

A word of caution before drawing conclusions. NAB has been the long-term underperformer of Australasian banks because they have a lower level of operational efficiency than rivals.

That said given the declining margins and wider economic environment every bank will be looking to cut non-revenue generating staff and delay future projects.

The ozzie banks could be toast. The royal commission exposed them our RB has talked tough and done squat, except fuelled it further with interest rates. The banks have been caught pants around ankles and bent over. The OBR is a crap piece of legislation for depositors. Any suggestions....kiwi bonds, piece of dirt, cash or blind faith?

Iron, well gun iron and precious iron. Silver gold. All three precious metals

When you weigh up the risk of an OBR event against the interest on savings after tax - cash in a safe deposit box. Or for no cost at all, you could deposit it in a TAB account - no interest, but no OBR either :-).

Can't believe at a time like this the government aren't rushing through that deposit guarantee scheme.

Me too, because Bridges appeared to have mentioned it in his parliament speech. I suspect a lot is being done in the background on it. It needs to match Australias at least IMO as 50k not enough per bank. Mo NZer should ever lose savings in a bank. Maybe they expect worse news to come over time and will announce it when it does

On the whole I'd rather not have tax dollars backing bank deposits just at this moment given the way banks have been run for the last few years. Why take the risk at this moment instead of waiting to see how it pans out for depositors?

Many will just take their money out and put it into lower risk things or keep it eg in their own safe

But who would pay for it Kate? Or would savers be happy to receive the risk free rate, say short term kiwi bond (0.50%) as opposed to the 2.5% they’re currently receiving on a TD?

If you’re happy to receive the risk free rate then after adjusting for inflation, it’s already losing purchasing power (although deflation may help that)

We're hiring. We increased turnover about 60% in the 2020 FY. Our cashflow is barely interrupted by Wuflu. Wipe the floor with our competitors on marketing. Highly qualified and loyal staff. Been around nearly 5 years. Still can't get a bank to lend to us for further growth.

Banks don't like risk.

They like Government backed lending. Like lending to buy and sell houses from each other.

Most of the Aussie banks pivoted towards Residential lending over the last few years, as it involved far less capital then agricultural lending, thus far greater ROI. It will be interesting to see if BS11 arrives in time.... If memory is correct NAB's retail mainframe is actually in Australia..... a fact that does not give the RBNZ a lot of bargaining power in an emergency situation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.