To support moves to a circular economy banks and other lenders will need to move away from traditional commercial metrics when assessing value and risk in their approval processes, a report from the Sustainable Business Network and Grant Thornton New Zealand says.

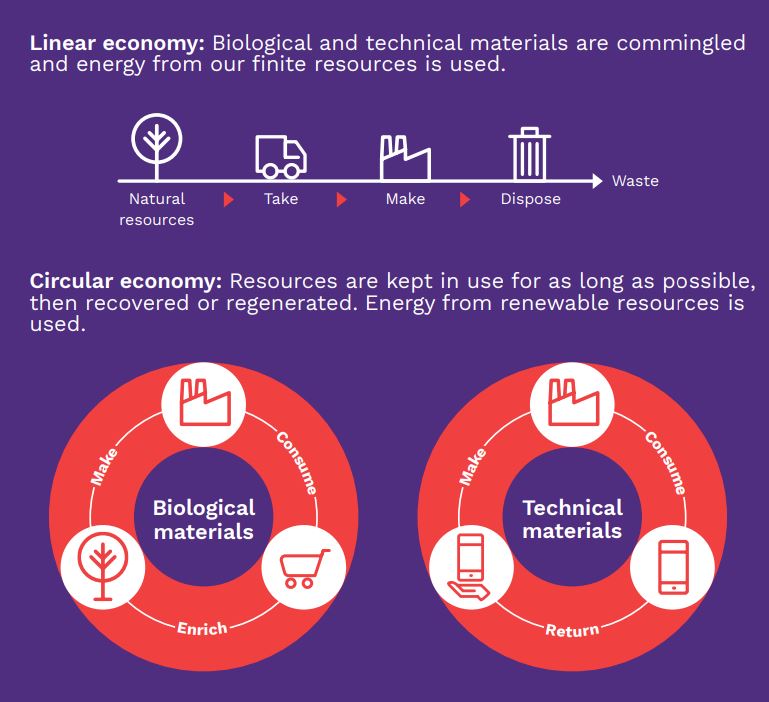

A circular economy, as opposed to a linear economy, features a focus on eliminating waste and continually using resources.

The report, The Circular Revolution Turning the wheels of our financial systems towards a sustainable future, notes in circular economies resources are never abandoned to become waste or pollution. Instead, waste is designed out of the production process and the resources we use are kept in circulation.

The government, lenders, businesses and customers all have roles to play in moving to a circular economy, the report says.

"The simple truth is we live on a planet with finite resources. Yet our consumption of these resources is growing exponentially. Without widespread change that impacts every life, and every part of living it, it will not be OK. As noted in Aotearoa New Zealand’s first ever Emissions Reduction Plan: “Approximately 45% of global emissions come from making products. Of these emissions, up to 80% are created in the design stage," the Sustainable Business Network and Grant Thornton say.

"We have a choice to make: invest in our planet or forfeit our lives and the lives of generations to come."

The report says the author's discussions with banks and other lenders revealed room for improvement.

"Most walk the talk around managing their own environmental footprint. However, this currently does not flow through into recognising the value associated with circular business models. Lenders report they are inundated with requests for sustainability funding. But they admit they lack people sufficiently trained around key circular metrics. This means they revert to traditional commercial metrics to assess value and risk in their approval process. It makes for a difficult financing discussion between both lender and borrower, and it’s a clear disincentive to move away from a linear business model."

The report says a barrier is that the approach to financing is still primarily stuck looking in the rear-view mirror.

"Banks are struggling to adapt their practices and see the future viability of circular businesses. They can’t revolutionise their practices without other parts of the system moving with them," the report says.

"Like every part of our finance system, banks are struggling to keep pace with the change towards circularity. We spoke to several that report working hard to develop more sustainable financing offers. But they are experiencing a number of roadblocks. Commonly used metrics and methods to assess the commercial viability of an idea are simplistic and narrow. A business’s past performance largely defines its confidence in the future. This is not the case for a circular business with revenue likely to increase year on year – but the need to finance the business to support this growth is vital. This is where the conversation with banks becomes difficult, because the past for a circular business is not an accurate reflection of the future. To banks, new ideas and innovation present risk, whereas tried and tested linear businesses represent stability. This is a declining model. Over time the linear business will struggle to source product. Without a future-proof alternative business model they will cease to be viable. However, banks, like other parts of the finance system, lack enough people with the knowledge and the frameworks to pivot their thinking as fast as is needed."

The Sustainable Business Network and Grant Thornton suggest banks and advisors have a duty to ensure staff understand circularity and environmental issues.

"Lending professionals need to be educated in sustainable and circular business models, supportive legislation and regulation is needed to provide more tools for assessing current and future risk associated with a circular business model, and robust measurement and ongoing reporting methods are required to provide assurance around green claims by businesses and their commitment to maintaining those standards throughout the life of the loan. On top of this the Reserve Bank needs to "unlock more capital to support the transition to circularity."

Companies Act change sought

The report also calls for changes to the existing framework for directors' fiduciary duty in the Companies Act, describing it as vague and containing a loophole for directors to disregard environmental considerations.

"While it provides directors with an opportunity to include environment as a point of accountability, this should be mandated. Many of the people we spoke to during the course of our research want environmental considerations to be explicitly included within a director’s fiduciary duty," the report says.

On the tax front the report says the Tax Working Group’s recommendations to incentivise sustainable business practices "must" be implemented. Additionally new tax measures to accelerate change, and revisiting GST for product leases, ought to be considered. On top of this there are "the levers around depreciation, certification and governance, along with easier access to new and improved grants."

Contacts featured in the report include Sustainable Business Network General Manager of Projects & Advisory James Griffin, Grant Thornton Partner, and Sustainability & Impact Lead Michael Worth, and Grant Thornton Tax Partner Denise Patterson.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

3 Comments

Reads like a marketing splurge for Grant Thornton and SBN

Lots of businesses have been doing this for years although now up against the millennials throw away attitude to products

Excellent article thanks Gareth. I find it deeply concerning that there are few comments so far, which to me indicates that the readers are avoiding thinking about what is to come, and how necessary it is to rapidly move to a circular economy. I think the adaptation needed will be crisis driven, and social and business responses likely too late and insufficient to prevent destructive outcomes to the quality of life and assets of a large proportion if not all of our society.

Yes, you are so right Nigel - comments here are invariably short-sighted and reserved for 'Houses' only ie: how to profit from Houses/ how to save and protect said Houses/ how to ward off the impact any attrition Govt and Councils policies or individual institutions will have on these Houses etc.

Essentially commentary is driven by self-interest - what is of less interest is whether we will have a planet to sustain the societies we live in and whether we will have the same geographic landscape and climactic conditions that allow us to continue to live (and thrive/profit!) from these houses.

My children are staring down the barrel of these environmental and resource threatening systemic changes - how they will all fare when it hits the tipping point is anyone's guess

My grandchildren will be building adobe houses, if they can find enough water!.... or living in house boats if there is an overabundance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.