Kiwibank's half-year profit surged 53% as income, boosted by a strong rise in net interest income, jumped.

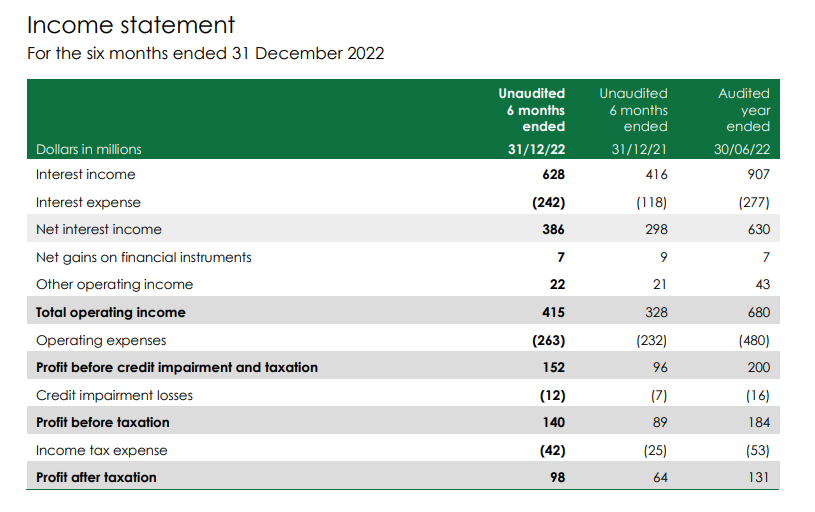

Kiwibank's unaudited net profit after tax for the six months to December 31, 2022 rose $34 million, or 53%, to a record high of $98 million from $64 million in the first-half of its previous financial year.

The bank's total operating income rose $87 million, or 27%, to $415 million, with net interest income up $88 million, or 30%, to $386 million.

Net interest income is the difference between the revenue generated from a bank's interest-bearing assets such as loans and the expenses associated with paying on its interest-bearing liabilities such as deposits.

Operating expenses rose $31 million, or 13%, to $263 million. Loan impairments increased $5 million, or 71%, to $12 million.

CEO Steve Jurkovich said Kiwibank grew home lending by $600 million, or 1.5 times banking system growth, during the first half, as it continued deepening its relationship with mortgage advisers and grew its own home loan specialist team.

Lending growth to businesses came in at $500 million, which was 4.2 times banking system growth.

“Being 100% New Zealand owned is a key reason why New Zealand businesses continue to choose us,” said Jurkovich.

As of December 31, Kiwibank's gross lending sat at $28.975 billion. Of that, $23.822 billion was housing lending, with other term lending at $4.155 billion. Total credit impairment provisions were at $75 million.

Kiwibank has seen no significant increase in home lending defaults within normal seasonal levels Jurkovich said, adding this could change "over the following period" and had been reflected in the bank’s loan provisioning. He said the second half of Kiwibank's financial year, the six months to June 30, would likely be dominated by the impact of higher interest rates, rising inflation, and recent extreme weather events in the North Island.

“Banks have to be able to be resilient to significant shocks, tougher market cycles and conditions. We are ready to do that,” Jurkovich said.

“Right now, our team is focused on providing customers with access to the information and tools they need to make informed decisions. We continue to encourage customers to contact us if they need to discuss their situation, and we’re contacting customers directly who we think may need support,” said Mr Jurkovich.

“The exact support we can offer will depend on personal circumstances but could include reducing repayments to the minimum regular amount, restructuring the loan, extending the loan term or temporary interest-only repayments.”

Kiwibank will make an initial donation of $250,000 to the storm recovery effort, he said, in addition to support it has already provided through the donation of generators to isolated communities.

As of December 31, Kiwibank's common equity tier one capital ratio, as a percentage of risk weighted assets, was 10.4%. That was unchanged year-on-year. Total capital stood at $2.307 billion.

13 Comments

Kiwi bank - where the branch wont change your business account name and sends you home to phone in and then wait for hours to get through (3 tellers and no other customers at the time)

Needless to say, person involved has now switched banks.

Probably 3 well dressed mannequin.

Got the opposite problem with ANZ, can't do a term deposit without visiting the nonexistent branch.

To"improve customer service"(according to their email) the ASB closed most of it's branches the other year, and the local ATM does not work half the time; Kiwibank the same, closed to improve customer service presumably.

Most banks are the same these days, no walk-ins you’ll have a make an appointment for everything and they don’t care.

I suppose they ain’t fast food restaurants can’t just walk in to a restaurant and expect a table.

Based on how the commerce commission works, there seems to be collusion on not competing on price.

So heading into a RBNZ engineered recession with almost 29,000 million loaned out, with only 75 million put aside for non recoverable loans. What could possibly go wrong.

Kiwibank are most likely to get a government bail-out if needed, so why bother?

All the banks are more likely to get bailed out than any individual citizen or resident.

Owned by the Govt!

Should be driving the industry with high TD rates and lower Mortgage rates.

53% is theft as a public servant...

Bit like Air NZ s greed!... Bailed out twice to 2 billion and still screwing us!

Wankers

Record profit after profit.

Great job done.

I’m actually really happy to see their success. I hope they continue to take market share out of the main Aussie banks and improve their service offering along the way.

Just a shame so many billions are heading over to Aussie at present. Much better to keep it in the NZ economy.

The largest shareholders in the big 4 are us banks so profits heading way way offshore.

Inflated profits.....lol.... Inflation everywhere...lol ... Hike the rates...Raise the costs...Put the prices up ,We have to bring down inflation!!!...lol....They are laughing all the way (not to the . . . .) but at the . . . . lol Whose making the Capital gains now ? ....lol , Hard not to view it as RE gone bad ...bait them with low rates and slam them with hikes, devalue their assets but keep them on the hook.... Nothing will change in RE until oversupply is reached...rate hikes wont create more affordability only an excessive supply can achieve such. Those in mortgage prison can expect more shenanigans . Bottom line is taxpayers will be left to kick the can down the road and put humpty back together again..... (critical view)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.