Kiwibank's annual profit surged 34% as the bank's income rose 20%, easily outstripping an 11% increase in expenses.

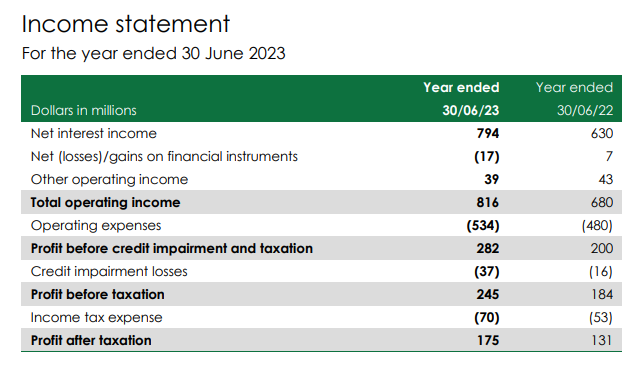

Kiwibank says June-year net profit rose $44 million to $175 million from $131 million last year, its previous highest annual profit.

Net interest income rose $164 million, or 24%, to $794 million, helping lift total operating income $136 million, or 20%, to $816 million.

Net interest income is the difference between the revenue generated from a bank's interest-bearing assets such as loans, and the expenses associated with paying for its interest-bearing liabilities such as deposits.

Kiwibank didn't report a net interest margin (NIM). However, interest.co.nz calculations suggest the bank's annual NIM was 2.49%, up from 2.16% the previous year.

Operating expenses rose $54 million, or 11%, to $534 million, with staff pay plus higher IT and systems costs the main contributors. Loan impairment losses more than doubled to $37 million from $16 million.

Kiwibank CEO Steve Jurkovich says annual home lending growth of $1.1 billion came at a rate equivalent to 1.5 times overall market growth, following a strong first half that slowed as the housing market cooled and interest rates rose.

Jurkovich says "significant action" has been taken to support customers struggling with higher living costs.

"Our teams have contacted thousands of customers to discuss the options available to them – whether that’s extending loan terms, reducing payments, going interest only, or providing short-term cash injection to help get on top of their finances. Feedback has been overwhelmingly positive, with customers telling us they felt a sense of relief that we can provide them with meaningful support to take some of the stress out of their day-to-day lives," says Jurkovich.

Meanwhile he's "extremely pleased" with Kiwibank’s business banking performance, saying it has grown its market visibility, and "stepped up" to support Kiwi businesses when many lenders were pulling back.

"While business banking growth of $900 million was impacted by lower business confidence and general market uncertainty, we grew faster than the market, demonstrating our commitment to the New Zealand economy," Jurkovich says.

"With 100% New Zealand ownership and all earnings being retained, New Zealanders have an asset that is growing in value which can have even more impact in the banking market."

Kiwibank's total gross lending rose $1.965 billion, or 7%, to $29.783 billion. Of that, $24.248 billion is housing lending.

Total credit impairment provisions rose to $108 million from $75 million a year earlier, comprised of $103 million of collectively assessed provisions and $5 million of individually assessed provisions. Meanwhile, past due but not impaired loans rose to $157 million from $115 million, with $94 million home loans and $50 million stemming from corporate exposures. Impaired loans rose to $8 million from $2 million.

Total deposits from customers rose $1.54 billion, or 6%, to $25.756 billion, with term deposits up $1.71 billion to $14.617 billion.

Total capital at June 30 stood at $2.566 billion, up $337 million year-on-year. At the end of July, Kiwibank's parent company, government-owned Kiwi Group Capital, subscribed for an additional $225 million of common equity share capital issued by Kiwibank, thus boosting the bank's capital.

As of June 30, Kiwibank's total capital ratio, expressed as a percentage of risk weighted exposures, was 14.3% versus 13.6% a year earlier. The Reserve Bank mandated minimum is 10.5%, but will rise to at least 16% in 2028.

34 Comments

Where does this profit actually go?

Same as every other bank, reused as internal capital or a dividend to owners. Unlikely to be dividend from what I understand. Maybe they're looking to do another blowout on some IT....

nact will make them pay a dividend , they will need the money to fund some of their promises, hopefully they wont do a solid energy and overload it with debt to make it crash

I think Act's proposing to slash the public service bloat in Wellington. Should free up some cash. ChatGPT does a better job than most of the back office staff I run into at council.

I really hope to see Seymour taking on the PSC portfolio and getting the free rein to clean up the public sector from the inside-out.

Should free up some cash.

We're talking a ~$10b deficit they wish to close. That's $10b out of your pocket and mine. That is the same as increasing tax by $10b to cover the hole.

If National came in and started talking about re-aligning spend to things that matter for the good of the nation, then I'd listen. But a psuedo tax increase (cut in spending) is specifically targeting ignorant voters who truly believe it's their money to begin with.

Imagine you have two job offers, one offers $100k, with $40k taxed. The other offers $110k with $50k taxed. Either way you're getting the same shitty deal.

The only way for blue and red to survive in the future is coalition together, I reckon we'll see it within 2 decades.

I've heard some countries try to lift economic productivity to bring in more taxes from higher worker wages and successful enterprises. Not even a remote possibility as long as there is bipartisan support for housing speculation and mass migration in this country.

Well done Labour fantastic investment.

Now its time fund everyday kiwis into Kiwi build homes.

This is how Singapore do it very successful 90% of there people in their own homes Fantastic.

No crime either.

Should we be happy about it?

You prefer if they made a loss?

How about paying a better interest rate for depositors, all of them?

In fact I would go so far as to suggest if KB was able to beat the market by paying at least the OCR for on call accounts and much more for others, they'd pull more customers (savers) and all their business. under a fractional model they'd still be profitable even with the higher cost of capital. They'd certainly win a lot more support!

Better than that money going to Australian banks and their shareholders

a lot of kiwisavers have a piece of the aussie banks mine has a lot invested in CBA (asb) westpac woolworths NAB and ANZ check out your kiwisaver if you have one and you will see the fund manager has picked those things making a fortune in NZ

Better 100% of the profits stay in NZ rather than a few % come back in dividends. NZ investors' proportion of CBA shares is tiny.

no I would just prefer to see some titles saying e.g. "some other company (or better companies ) in non-banking-insurance-real-est industry made huge profit(s)"

Otherwise I am reading it - local bank instead of 4 overseas banks made fortune on increased interest rates payed by average NZ families , which otherwise would go into real economy and support local business/education/travel opportunities and better way of living

nobody is preventing you from buying shares in such banks

House prices and rents have siphoned off Kiwis' disposable income

Great News! I would love to see Kiwibank taking more and more market share from the big 4 Aussie banks. At present billions of dollars pa are being repatriated to Australia in banking profits.

The stronger Kiwibank are the more of this money can stay in NZ.

Air N Z. Billion dollar turn around.

Easy to make a profit when you can just triple your prices!

Try making a profit with cheaper prices, like Air Asia X.

Profit is an ugly word nowadays

now national can sell 49% of it so the rest of us can jump on the bandwagon and get some of it

No, keep 100% Government owned = 100% bullet proof.

I have all my $ in Kiwibank. Wouldn't touch another bank until deposit insurance kicks in.

Whys that? You think the govt would bailout Kiwibank if it got into trouble?

depends which government , one side would the other would not blink and sell it

The gov will bailout Kiwibank or any of the 4 Aussie banks if they got in trouble. Probably the smaller banks too.

They do for AirNZ every other week.

Good result from KB. And they can do this with their call savings rate at 4.5%. So why cant ANZ and ASB offer more than 2.8% on their call savings accounts???

Aussies - "no surprises there."

7% return on capital is respectable given above system growth. There is still no evidence whatsoever of any meaningful credit stress. We need KB to step up and grow faster, they need to hire well and go for it.

Good result KB. Well done all round. No more IT fumbles please. A decent website is your front office these days.

Good result. Ploughed back into further growth I hope. (Not if NACT get's the reins it won't.)

In looking at interest.co.nz list of mortgage rates on a regular basis, I often see Kiwibank's carded rates lower than the big four Aussies. Anyone else see this?

I've never been a mortgage customer of Kiwibank. Every time I've tried to move my mortgage business to them I've been rejected due to their serviceability requirements. Though the Aussie banks never have a problem.

I wonder if Kiwibank is cherry picking customers and building a high quality book. Or are their carded rates the best they'll do? (Unlike the Aussie banks who will often drop below their carded rates when faced with a bit of pressure / competition.) Anyone know? Or care to guess?

I don't have any particular insight, but my mortgage has been with Kiwibank since purchasing in 2019 with 70% LVR, and about 3x DTI. I haven't had any problems with them other than an incorrect overpayment fee which was reversed after a message on the website.

We negotiated a small discount to carded rates, but that's getting harder as the mortgage dwindles following some overpayments between fixed terms (or maybe I'm just pushing less hard as the potential savings get less significant).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.