Kiwibank's interim profit rose to a record high as housing lending and net interest income grew.

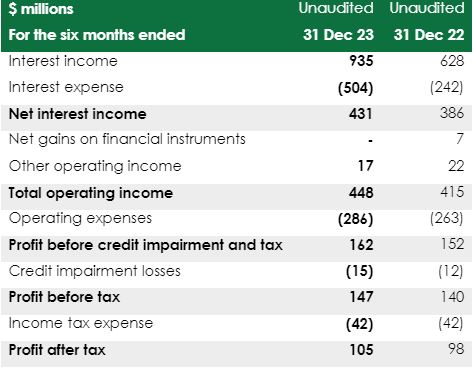

The bank's unaudited net profit after tax for the six months to December 31, 2023 rose $7 million, or 7%, to $105 million from $98 million in the same period of the previous year.

CEO Steve Jurkovich says Kiwibank's net lending grew $1.3 billion during the half-year, with home lending increasing 2.7 times faster than the sluggish overall market.

"This improved performance was driven by competitive pricing across key home lending rates, and a continued focus on growing our relationship with advisers. This resulted in strong interest for customers looking to switch to Kiwibank, and a big increase in the number of first home buyers choosing Kiwibank to achieve their home ownership goals," Jurkovich says.

Business lending was flat with businesses taking a cautious approach to borrowing in the current economic and geo-political environment, he says.

Kiwibank's net interest income rose $45 million, or 12%, to $431 million, with total operating income up $33 million, or 8%, to $448 million.

Net interest income is the difference between the revenue generated from a bank's interest-bearing assets such as loans and the expenses associated with paying on its interest-bearing liabilities such as deposits. Kiwibank's half-year net interest margin rose one basis point to 2.43%.

Operating expenses rose $23 million, or 9%, to $286 million, and credit impairment losses increased $3 million to $15 million.

Over the six months from June 30 to December 31 last year Kiwibank's credit impairment provision rose $13 million, or 12%, to $121 million. Meanwhile, loans past due by at least 90 days rose to $41 million at December 31 from $18 million a year earlier.

Over the six months from June to December last year, Kiwibank's housing lending grew $1.23 billion, or 5%, to $25.507 billion, and its gross lending increased $1.319 billion, or 4%, to $31.102 billion. Total deposits increased $1.079 billion, or 4%, to $26.835 billion.

Kiwibank's total regulatory capital rose $578 million, year-on-year, to $2.885 billion. Of its key capital ratios, common equity tier one capital came in at 11.9% of risk weighted exposures, up from 10.4%, and its total capital ratio rose to 15.9% from 13.4%.

'We don't need to jam the brakes on any harder'

Jurkovich says the key question now is when will the Reserve Bank (RBNZ) start cutting the Official Cash Rate (OCR) from its current level of 5.50%?

"The RBNZ remains focused on domestic inflation and while we believe enough has been done to get inflation back to more normal levels, it looks like rate cuts are becoming a more distant possibility," Jurkovich says.

Speaking to interest.co.nz Jurkovich said an OCR cut would help confidence in the business sector.

"And confidence would help accelerate some growth and investment. So I think a cut would certainly be good for the business banking side of things," he said.

"One of the reasons I don't believe personally we need to see a hike is when I look through our customers that are in hardship or needing to defer payments or go to interest only, they're six times more likely to say it's because they've suffered a reduction in surplus income than illness, loss of a job, divorce and all those other life events."

"And it wasn't that long ago that it was probably a third [each] around income and illness and jobs and divorce. Whereas now it's very clear to me that actually that reduction in surplus income is just showing that the brakes are on the economy," Jurkovich said.

"And then if you dig into where people are not spending their money, we've got a 12% to 14% downturn over Christmas on entertainment and recreation. So at the end of that is a hospitality business, and at the end of that is an owner, and at the end of that is someone with a home loan. So all those things, I just think it shows that the brakes are on and we don't need to jam the brakes on any harder."

"But also, to be fair, it's going to take time to get it [inflation] down into the 1% to 3% [RBNZ target, from 4.7%]. And so that's why I think a cut is less likely, but I don't think we need a hike," Jurkovich said.

5 Comments

Can the government please partially list Kiwibank and give it the capital it needs to thrive and go after the big banks?

once it's listed it will just join the oligarchy

They gave up a lot of margin to get their result. So the numbers are not as great as they appear.

That's how you grow the loan book. The size and quality of the loan book is what really counts. Banking 101.

Just moved over to KB. Found the staff to be pleasant, the process efficient, and rates sharp. Overall the experience so far has been really good - hopefully they'll have g-pay integration soon as they have now kicked-off apple pay.

If you're thinking about it, go for it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.