The final data releases have now been received in 2025, the latest the RBNZ banking data dump. That includes their C5 series tracking the size and movements in the overall loan books of lenders.

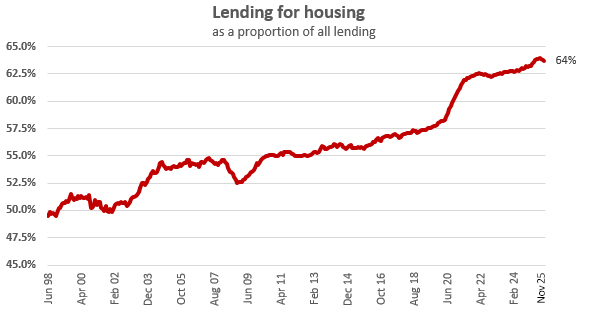

And the biggest set within that is for home loans, accounting for almost 64% of all lending, and 2025 saw this reach its record high.

Lending for housing is now at $388 bln* of all lending which now totals $609 bln.

The economy may not have grown, but our housing debt did.

Our collective ability to service this debt got easier in 2025, and our monthly home loan affordability reviews show this was true for first home buyers as well.

Lending for housing grew +5.6% in the year to November, much faster than the +3.6% in the near to November 2024, and the +2.9% in 2023. But that was less than the +7.0% compound growth in the five year period 2015 to 2020. And far less than the +21% in 2021.

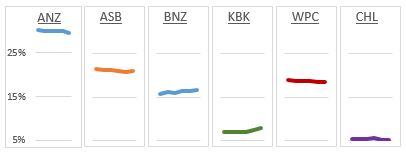

But of course, this expansion wasn't even among all banks. Interestingly, the two main banks with the smallest market share five years ago have made the largest gains through to 2025.

We have granular detail about individual banks to September 2025 from the RBNZ Dashboard.

This is a chart representation of the quarterly market share shifts over the past five years.

Only BNZ and Kiwibank are ending 2025 with higher market shares than where they started in 2020.

Mortgage market shares change slowly because of the very large embedded bases that are on fixed rates. Competition is fierce mainly because every bank knows who they lost and are able to target them to win them back. And with interest rates very little different between banks, the incentives to change have to be material to make the effort worthwhile.

In the past five years, ANZ has seen its mortgage book rise by +$26.4 bln to $113.9 bln. ASB's rose +$18.6 bln, BNZ by +$18.0 bln, Kiwibank by +$9.9 bln and Westpac by +$15.8 bln. It has been a period where "everyone wins", just some more than others.

Kiwibank's outsized drive to win mortgage share by concentrating on getting the support of mortgage brokers has helped them in the past two years (including via its captive NZHL network).

Challenger banks (CHL) however aren't really getting a look in.

* And just for the record, the RBNZ data shows the value of all residential housing is currently $1.65 tln, giving a national LVR of 23.4%. Household debt as a percentage of household disposable income has been little-changed in over 20 years. And household debt servicing is currently at its long-run (25 year) average level.

10 Comments

I use a broker and about to shift a lot of debt.

Earlier in the year I attempted to do some very small lending direct. Never again.

It’s sad that the banks give better rates to brokers than the people who don’t cost them a cent and fix online. Weird incentives.

"The economy may not have grown, but our housing debt did"

Our private debt is still up above 130% of GDP (https://www.ceicdata.com/en/indicator/new-zealand/private-debt--of-nomi…) and yet we still lend more on houses and then wonder why the economy isn't growing.

(because its drowning in private debt, and banks are reluctant to lend to real business that might increase our productivity - thus reducing our private debt to GDP (productivity) conundrum).

Falling interest rates for decades tricked people into thinking that lending more credit on housing was the way to cheap/easy riches and 'economic growth' - instead its a trap - where younger generations end up drowning in private debt and don't have the spare financial capacity to spend on things other than rent/mortgage payments, which might actually boost economic activity (other than building houses).

Totally agree. 100%

Agree 99%, but its even worse than you think.

We didn't build many houses on a per capita basis, in general we increased property prices by stifling production in the housing sector. Massive debt failed to boost house building, because we regulated the costs up faster than house prices.

Good points - agree with you. We allowed (even encouraged) excess (easy) credit to chase a limited number of homes - then wonder why we ended up with a way overpriced housing market.

Massive debt failed to boost house building, because we regulated the costs up faster than house prices.

Partly correct. Credit is created for house transactions on the purchase of houses. Credit is not created for productive purposes such as the production of houses.

But it is worth remembering it's been a very real way to cheap easy riches for most of a whole generation. The trap is a macro one , on a micro level it's amazing and you will fail entirely to convince the winners otherwise, certainly not that they're the countries problem rather than the solution.

Which generation are you referring to? I'm told a certain generation has had it so tough and now can't afford to retire? So is it the path to riches or not?

"I purchased my first house for $50,000 and its now valued at $1,200,000 but I can't afford to retire"

It's more a path to false riches - one where you suck all the future prosperity from the economy for oneself and then say 'well I'm sorted so who cares about anyone else'. eg Luxon.

“where younger generations end up drowning in private debt” - as interest.co.nz calculates, on average it’s way less than 40% of income for FHBs. Ideally it would be less, but it’s not as crazy as the headlines make out.

on average it’s way less than 40% of income for FHBs

do you have a source for his 40% of income stat?

House lending has no real skill or understanding required by the bank. Business lending is different. The banks staff have to understand your business. Unless you are buying large. Capital assets (trucks etc) they dont have the time or staff to really understand you.

There is one winner of over lending to residential housing at ever stupider prices. It's the banks profits.

Aka the billions to Straya...are we suckers?

House lending has no real skill or understanding required by the bank.

It's not complicated. The money supply is not fixed so banks can create credit to buy relatively scarce assets and prices naturally rise.

When the credit is created, the debt also represents a corresponding credit in the bank accounts of house sellers. This is excess money that can be spent into the non-Ponzi economy, particularly if the sale price requires more human labor required to repay the debt to banks compared to the past.

Up to the GFC, the central and commercial bankers thought they had discovered an infinite wealth creation machine. The non-Ponzi economy can survive because people still need goods and services outside shelter. Post-GFC, the same credit creation mechanisms were employed to ensure that the wealth creation machine didn't break.

The non-Ponzi and Ponzi economies are complementary in many ways. In terms of credit creation for productive purposes, vehicles such as private equity have boomed since the GFC. The global market value of private equity assets has risen about 636% since 2009, reaching roughly 10.8 trillion USD at the end of 2024.

https://www.ocorian.com/knowledge-hub/insights/global-private-equity-as…

dp

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.