The Reserve Bank (RBNZ) is reminding financial markets it could increase its weekly bond purchases to put downward pressure on interest rates.

Furthermore, a negative Official Cash Rate (OCR) remains on the table.

Government bond yields in New Zealand and other parts of the world are rising, as financial markets are betting on an improving economic outlook lifting inflation sooner than previously expected.

NZ Government bond rates

Select chart tabs

This is occurring as central banks around the world are continuing to deploy loose monetary policy in an attempt to lower interest rates to boost inflation.

Battling financial markets, the Reserve Bank of Australia in recent days upped the pace of its bond buying in an attempt to lower bond yields.

RBNZ Assistant Governor Christian Hawkesby told interest.co.nz the RBNZ was “watching markets really carefully.”

Asked whether ramping up bond buying for a short time via the Large-Scale Asset Purchase (LSAP) programme was something the RBNZ would do, Hawkesby said: “We’ve observed the price action, which has been pretty volatile over the last week or so.

“There have been pockets of dysfunction, I think, along the way - not just in New Zealand, but in Australia and the US as well.

“There is a lot of talk of thinly liquid conditions. So we do have that optionality; so we can scale up the size of the [LSAP] programme, if we think that would be appropriate.”

By this Hawkesby meant the RBNZ could increase its rate of bond buying within the LSAP’s $100 billion limit.

“We know that we can’t control the level of the long-term yields - they’re driven by a number of factors. But we can look at how they’re moving around relative to other comparators,” he said.

The RBNZ hasn’t upped its bond purchases in recent days. It’s continuing to buy $570 million of New Zealand Government Bonds a week - fewer than it was buying when it launched the programme last year.

Because Treasury is issuing fewer bonds than it planned to when the LSAP was launched last year, Hawkesby said the RBNZ was getting close to the cap (outlined in an indemnity provided by the Crown) restricting it from buying more than 60% of New Zealand Government Bonds on issue.

“We are getting towards 40% to 50% of some bonds on issue,” he said.

“The good thing about the current situation is, now banks have had time to get operationally ready for a negative OCR. That means that we’ve got more tools in the toolkit if we did want to provide more monetary stimulus.”

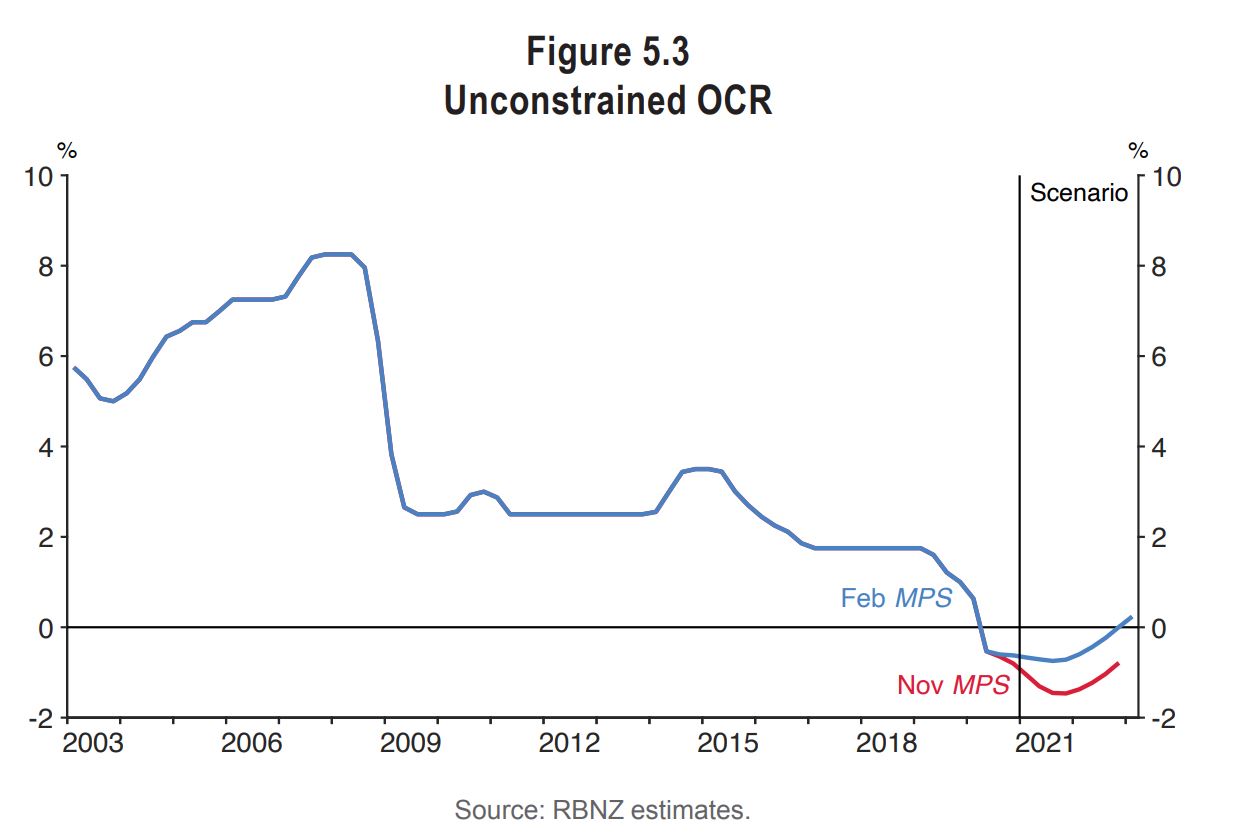

In its quarterly Monetary Policy Statement released last week, the RBNZ adjusted its unconstrained OCR projection up from its last statement released in November.

The “unconstrained” OCR measures the level of stimulus needed to meet the RBNZ’s inflation and employment objectives, considering all its tools at play. The current use of a low OCR, LSAP and Funding for Lending Programme are equivalent to the OCR being at -0.5%.

Asked how one reconciles this projected rising unconstrained OCR with the RBNZ’s dovish comments, Hawkesby stressed the central bank is still dealing with “scenarios” in an uncertain environment.

“If lending rates rise in a way that jeopardises our ability to achieve our mandate, then we need to do something about it in terms of the actions we are taking and the settings we have in place,” Hawkesby said.

Keane: RBNZ wouldn't want to 'battle the market'

Sean Keane - founder and managing director of Triple T Consulting, which advises central banks and other regulators - maintained the RBNZ wouldn’t want to “battle the market”.

He didn’t see the RBNZ suddenly increasing its weekly bond purchases just in response to higher bond yields. Instead he would expect the RBNZ to wait and observe the situation before acting.

Keane maintained that there were two things that would trigger RBNZ action - dysfunctional markets or financial conditions preventing the RBNZ from meeting its targets. In other words, a stronger dollar or higher bond yields leading to higher mortgage rates.

Keane said the market misread last week’s Monetary Policy Statement, so now the RBNZ is reminding it the economy is a long way from “normal” and still requires an enormous amount of assistance.

87 Comments

Nz needs lower interst rates like i need a hole in the head.

Throwing their toys out of the cot lol. RBNZ cannot beat the world bond market forever.

If overseas buyers can dobetter elsewhere demanding for NZ bonds will dry up

NZ business needs higher interest rates like a hole in the head.

Zombie companies are they?

Max is explaining it for long time. https://www.rt.com/shows/keiser-report/516913-wealth-gap-cantillon-effe…

True, low interest rates for real businesses yes yes yes. Unfortunately we all know where most of the stimulus has gone - to residential housing speculation.

Yes, low interests for real businesses. Actually, we could put a tax (say 2 to 3% p.a.) on interests paid by unproductive property specuvestors, and use this money to provide tax incentives to real businesses, especially the ones oriented to the export markets.

Some might sink, others swim. But property is the Untouchable

The world has been in a downward spiral with decreasing interest rates so what difference will slowly rising interest rates make ? The party is over its time to start raising rates and for people to start thinking rising not falling rates and plan accordingly.

Can we expect CWBW to post a thread advocating a "hands off, let the market take its course approach"? I doubt it.

As I have seen in other threads, self-serving housing specuvestors claim that they are in favour of a "free market", very conveniently "forgetting" that in NZ we have just the opposite, with landlord subsidies, a taxation regime tilted in favour of the housing Ponzi, monetary policies that are killing price discovery and appropriate risk pricing, and a RBNZ that is actually fighting free markets with increasing desperation.

It is time that we adopted free market principles in this area, by removing subsidies and favourable tax treatment of housing speculation, immediately stop all forms of money printing, let interest rates find their free market equilibrium levels, and let the housing Ponzi deflate now before it is too late: the bigger the housing bubble, the higher the risks that it takes the real NZ economy with it, once it bursts.

Its pretty clear we're well past the point of wise policy.

If it were a free market anyone could just pick a spot and build anything on it. Its the opposite, rigged in every aspect

They are only interested looking after the affluent section of society.

essentially printing more money which will inflate house prices further.

Only if it's possible to borrow.

General view now is that there is no link between QE / LSAP and residential house prices. The housing market boom is the result of low interest rates, market confidence in continuing low interest rates and house price growth, and high rents that incentivise buying even at daft prices. Noting of course that high rents are often subsisided by Govt who were also dumb enough to commit to continued house price growth!

Government loves subsidising rent, in fact they encourage it, with high house prices creating more tenants. To them, it’s fiscal spending (getting money into the system). The force (government+rbnz) is all about pushing newly created money into the sick patient. And when people say who’s going to pay for government debt, just ignore it. Debt is only used to justify and give meaning to a fiat currency.

I would dispute this as it's different for every jurisdiction. My understanding is the RBNZ lends money to banks at low rates. In NZ the risk weighting set by the RBNZ for bank loans is high against businesses and low against residential housing. Ergo they lend all of that loaned money into residential housing. Yes, interest rates are the main driver, but if the banks had different risk weightings, you would see them loaning more money to businesses and less money to specuvestors, sorry FHBs.

Not quite. When banks lend money they literally create it out of thin air and swap it for an 'IOU' from the borrower. This means the borrower has some cash, and the bank has an IoU (thus the balance sheet of the bank remains in balance). This is how 90% to 95% of cash enters the economy. So, banks do *not* borrow money from RBNZ to lend to borrowers. Nor do they rely on peoples' savings to make loans (a common misconception).

RBNZ do set rules on capital adequacy - the ratio between cash / assets held by the banks and total loans out (and at what risk level / LTV etc). However, banks are lending for residential mortgages because there is huge demand for mortgages from apparently credit-worthy customers. Businesses aren't demanding credit despite low interest rates, because they borrow money when they are confident in getting a return on their investment (the interest rate is almost irrelevant).

All banks have to have a current (reserve) account at RBNZ and keep enough money in that account to settle transfers between banks daily. RBNZ pays 0.25% on bank balances in this current account. When banks buy bonds from the Govt, RBNZ takes money from these reserve accounts, and gives interest-earning bank bonds in return (a swap), and when RBNZ buys bonds back from banks (aka QE or LSAP) they put cash into bank's current accounts and take the bonds back. LSAP / QE has led to banks having huge amounts of 'cash ' in their current accounts at RBNZ. You can see the impact of this in the RBNZ balance sheet: https://www.rbnz.govt.nz/statistics/r1

Great question regarding the 60% limit on bond purchases. Classic how Central Banker Hawkesby went straight to; 'the banks are ready to implement negative interest rates' lol, totally cracks-me-up.

His deadpan, yet indignant response to bond traders not taking their lead from Central Bankers was pretty comical too.

Yes. They believe that they're as powerful as puppeteers pulling strings.

Orrogance you say?

Interestingly so did ever master of nearly ever social order in history - until the people realised they were being screwed, evolved their thinking (or at times regressed to darkness) and moved forward to a new social order and set of rules (and rulers).

Nothing to see here... Move along.

“There have been pockets of dysfunction, I think, along the way - not just in New Zealand, but in Australia and the US as well.

“There is a lot of talk of thinly liquid conditions.

Exactly: dealers in the US are hoarding US Treasury securities. Hence they are prepared to lend cash to access pristine US Treasury collateral at 0.01% at the Secured Overnight Financing Rate window.

{kind=link}

That condition of illiquidity is reflected in the significant demand at the RBNZ bond lending facility window.

[Fed's] MR. FISHER. In summary, I want to mention that, as I said earlier, most of these variations that have been suggested are very un-Bagehot-like. And what I mean by that is, twisting [or QE] entails purchasing assets that investors are fleeing toward, not assets that they are fleeing from. Link

What is it with Christian Hawkesby & Geoff Bascand, they both take unusually large gasps of air when they're delivering their message. Look to me a little bit uncomfortable with what they're saying?

I've noticed that as well. To me they're trying to show confidence, as though they've answered these same old questions before. A subtle form of arrogance.

“The good thing about the current situation is, now banks have had time to get operationally ready for a negative OCR. That means that we’ve got more tools in the toolkit if we did want to provide more monetary stimulus.”

{kind=link}

too much intervention to keep rates low. for WHAT???

Bit pot-kettle-black in stating other players are dysfunctional.

Central Bank to Market: Please stop pricing in any sort of recovery in the future...ever

These financial guys either don't have a clue or they have been told to lie. All currencies are deflating against btc, it's just that price inflation hasn't hit us yet or the supply chain breakdown etc.

Investors should now go all in on real estate!

As NZ struggles to devalues its currency, there are no better vehicles to hedge against inflation than real assets.

This chart shows the effectiveness of investing in real assets (including estates) during times like these. The longer you wait the harder it'll become. Act now!

All into the Ponzi bubble!!

Beetroot, is that you?

Remind everyone how many rental properties you own please?

Irrelevant comment

Do you drive your Aston Martin with personalised plates to the food bank - or is it best to keep it out of the sight of the poor people?

Could be a Renault?

Must have sold his Aston Martin (he’s got the pics including gloating on his FB page).

Think a cross between the Zohan and the wolf of wall st.

Oh you're friends with him on Facebook?

No but I know who he is.

I agree with the logic, but not everyone gets invited to the party - only those who already hold property to leverage against. Being born in the wrong decade really militates against that.

This is why I think younger people are going to walk away from the current system and create their own new world. See what's been going on with reddit/GME and their desire to take down wall st/hedge fund/s. Power to the people.

Actually NZ real estate performs terribly in inflationary environments.. But hey, nice try!

Fat controller printer go brr

I wish the central bankers would just bugger off. There shouldn’t be an arm wrestle between markets & these unelected eggheads who seem to have been given the power to ‘play God’ by unleashing a tsunami of money creation on a helpless world.

I'm joining the call to get rid of Orr, and he can take Christian Hawkesby out for a permanent lunch when he goes.

They have the cheek to point out dysfunction. I know where the dysfunction is - between their ears if they think the economy is at risk for lack of cheap finance.

Tax Payer to Govt: GET THEM OFF MY PAYROLL NOW.

Problem is we live in a democracy yet we don't get to vote for monetary policy - yet it is in many ways far more powerful than fiscal policy #stupid

Monetary policy is out of the hands of politicians for a reason. How would the public meaningfully elect someone into the role, anyway?

If we can vote of things like taxation and spending then voting for interest rate and inflation settings seems on the same terms/level to me. Don’t see the difference.

Globally central banks have become cult like organisations that no longer appear to represent the best interests of younger generations (and in some respects retirees).

In NZ you can vote on and discuss almost anything, as long as you don't touch the housing Ponzi.

That is out of bounds, and left to the whims of an incompetent, un-elected bureaucrat at the helm of the RBNZ, who can happily ignore the wishes of the majority of the population and even the instructions of the Minister of Finance, as he thinks he knows better.

Central Bankers make me think of the French monarchy just before the revolution.

Someone else is telling him what to do, Orr can you really be that ;;;;;;

It seriously looks like we're approaching the end of this long debt cycle. It appears we're now stuck in a very nasty liquidity trap!

John Maynard Keynes, in his 1936 General Theory,[1] wrote the following:

There is the possibility...that, after the rate of interest has fallen to a certain level, liquidity-preference may become virtually absolute in the sense that almost everyone prefers cash to holding a debt which yields so low a rate of interest. In this event the monetary authority would have lost effective control over the rate of interest. But whilst this limiting case might become practically important in future, I know of no example of it hitherto (JUMP FORWARD NOW TO 2021...)

No matter what central banks do - there are no good outcomes. Do nothing and yields rise - system breaks under debt load. Drop rates further and more debt is created which cripples the economy further.

#monetarypolicyisbroken

ps..the question becomes, who and what is going to save us from this unsustainable governance and policy setting/s?

The name's Bond, Junk Bond

Another answer to that question is - No one.

I know it; you know it and worst of all, they know it.

All we don't know is 'when'. That's what this is all about - buying time. But it's futility writ large.

Nothing can stop what's coming now - nothing. And it's going to be horrific.

But the clue as to 'when' might be when those we all know that are far closer to the Centre of the Universe (supposedly the Central Bankers and associated insiders) start selling - firstly their speculative art; secondly their investment real estate and finally, their hard-core stocks, shares and other assorted assets.

Everything.

Yes although capitalism is a relatively new concept for humanity if you want to look really big picture - let alone concepts like QE and inflation targeting.

Fiat currency is simply a concept that could be destroyed if the majority people decide it no longer serves their best interests - and it appears there are more and more people moving towards that space now.

Feels like western society (and it brings with it - good/bad) as we've known it is at the precipice of something very new.

Some really clever operators are starting to ask some unsettling questions.

As I suggested, 'when' is the only thing we and they don't know.

The chief investment officer of Magellan says investors face having “their shirts ripped off” by a number of risks lurking behind the rosy picture of a speedy global recovery. ....“There is no margin for error in markets at the moment…The risk is foreseeable, and there’s enough evidence to tell you it’s foreseeable and there are some clear warning signs at the moment,

https://www.investordaily.com.au/markets/48817-what-hamish-douglass-is-…

ASX falls as bond yields rise after(this afternoon's) RBA meeting

https://www.afr.com/markets/equity-markets/asx-falls-0-4pc-as-bond-yiel…

China sounds warning on asset bubbles

https://www.telegraph.co.uk/business/2021/03/02/markets-live-latest-cor…

Those with vested interests are rushing around telling everyone that interest rates can't rise. Yet history doesn't agree with that viewpoint.

If they don't rise it means we're have deflationary issues (pushing rates negative) while debt spirals out of control. Or we do have inflation and rates rise which as Magellan say will destroy financial markets (and many property investors).

Probably depends on age and experience and whether one is starting a ponzi training scheme/blog

Good thinking. Human nature - people talk, warn buddies

I think sooner rather than later central banks will be forced to cede to reality and lift interest rates even if it means debt defaults, at least they'll still have something to work with. Private assets will shrink and so will debt, and with it money but the govt still has enough to hand out and RB can go brr again. The lesser of two evils

“We know that we can’t control the level of the long-term yields - they’re driven by a number of factors. But we can look at how they’re moving around relative to other comparators"

Errrm, maybe go and tell that to Japan who have held long-term bond yields at next to nothing for many, many years - taking down anyone daft enough to have a go at them. UK have done the same recently - with some subtle legislative reminders of their unlimited ability to finance market interventions.

The NZ strategy of showing weakness or deference to the market is plain dumb - like lying on the floor and asking to be kicked.

> pockets of dysfunction

Read: "markets pricing risk according to the real world, rather than the world we would prefer to exist"

LOL - I was about to write something exactly along these lines, when I came across your comment :-)

(Comments from Telegraph in London this morning)

The Chinese have worked out the problem and know they are on the verge of a financial crisis.

They have been making all the classic mistakes everyone has been making during globalisation.

They released the power of finance, which is the power of debt.No one realises the problems that are building up in the economy as they use an economics model that doesn’t look at debt, neoclassical economics.

As we head towards the financial crisis, the economy booms due to the money creation of bank loans, as it has before.

The financial crisis appears to come out of a clear blue sky when you use an economics that doesn’t consider debt, like neoclassical economics, as it did in the US in1929 Japan in 1991 and Globally in 2008.What’s wrong with neoclassical economics?

1) It makes you think you are creating wealth by inflating asset prices

2) Bank credit flows into inflating asset prices, debt rises faster than GDP and you eventually get a financial crisis.

3) It confuses making money with creating wealth, driving the economy into a Great Depression.

That's a pretty nice summary of what a lot of people have seen coming down the line.

The problem is no one knows how long central banks/governments can keep the ponzi going.

There now you see, even the Telegraph is being dysfunctional.

Central bonkers remind bond buyers that they have a checkbook with more zeroes on the end than anyone can imagine. Their fingers are holding the pen, ready to sign and they are staring them in the eye in an epic stare down. As bond buying happens in a currency the bonker controls, the bond buyer realises they cannot win... the bonker doesn't realise that as he wins, the country/people he is supposed to be working for, loses.

Go negative, we are so close, might as well see what happens.

Geez, it's looking pretty crazy out there. All I know is high interest rates have never done anyone any good, as it sucks the life blood out of the economy. I say let things settle at where they are and who knows it might all turn out alright.

YOLO!

Describe to me what exactly that means dago

YOLO 1. acronym for You Only Live Once,meaning to engage in impulsive or reckless behavior with this sort of rationalization:

We’ve been YOLOing all night.

2. "Yes OCRs Lowering" - Orr

I'm with you - lets hang a minus sign on it.

I'll be down at the beach watching the Big Wave come in.

So now we are describing legitimate market forces as ‘pockets of disfunction’ because the resulting rate movements don’t fit the Bank’s narrative?

The free market is well and truly dead. This is now a rigged market economy and ideally you were born prior to 1975/1980 (ish) to benefit from it.

Market can be irrational, but when responding to that RBNZ being hawkish? general public started to sense of their inept, fighting the irrational with more extreme irrational measures.. slowly and surely, this subconscious picking up side, will eventually create confidence issue. They still cannot feel that yet at the moment.

Some of us are actually old enough to remember when the role of Reserve Banks was to protect depositors and savers from the speculative activity of banks. Now they are coconspirators in defrauding anyone with deposits or savings.

Post the year so far.

The greatest irony is Hawkesby is completely oblivious to the fact that he, his RBNZ colleagues and international central banking counterparts are the dysfunction.

The Central Bankers are are criminal cartel working to enrich asset holders & impoverish everyone else.

If you cant see you hard earned $$ that you traded your precious time for loosing value before your eyes, then you need to pull your head out of the sand.

Opt out of their centrally controlled system where the government prints money and gives it to their rich friends, and the poor get screwed.

Buy Bitcoin, no one controls it, it is available to everyone and they can not censor your transactions or dilute your portion of the 21 million coins that you own.

https://chrisgimmer.com/bitcoin-reserve-asset/#:~:text=Portability%3A%2….

Hawkesby is living proof that there is at least one true-to-label dish on the RBNZ's "menu of available tools."

Moreover, how can any mere mortal hang her hat on the prophesying of a banker who clearly doesn't understand French cuffs? Any self-respecting acolyte of this profession wouldn't be caught dead with those little pairs of elastic balls that come with the shirt holding their cuffs together. It is a sacrilegious disgrace to the legions of financial entrepreneurs whose business it is to extract surplus value wheresoever it may be.

On the topic of cajones, if they're worried about the currency, why not just call a spade a spade and directly intervene? Surely fiat is better parked in some gold reserves rather than encouraging government largesse and property speculation at the expense of savers. Both these latter erode the link between hard work and reward which is a central pillar to a civil society. If they don't understand the ramifications of eroding this pillar, they are either willfully negligent or deliberately obtuse.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.