Updated with Monday's swap rates.

Bond market sharks are circling. They can sense inflation blood in the water.

Today (Monday), benchmark NZ Government bond rates are rising sharply. The 10-year is up 10 basis points (bps) from Friday, and rising. The two-year is up 13 bps so far.

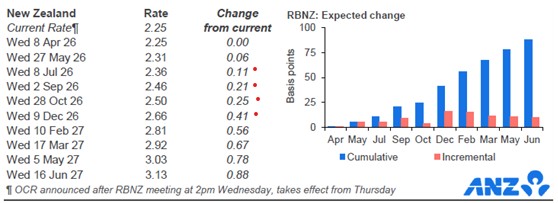

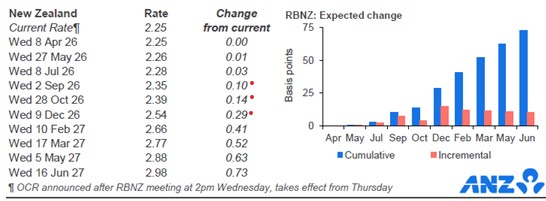

We started the day with financial markets pricing in a much more elevated chance of multiple Official Cash Rate (OCR) hikes in 2026.

Based on market pricing, there is now half a chance of a July OCR hike now. After today, that chance may have risen.

Compare that to a week ago, when only one was priced in.

It doesn't take a rocket scientist to understand why investors are demanding higher yields. Chaotic US policy-making, wars of distraction, and geopolitical realignments are making things very much more risky.

And New Zealand is at the tail end of that whip.

The frenzy today is clear with the two-year rising faster than the 10-year.

And it isn't just New Zealand.

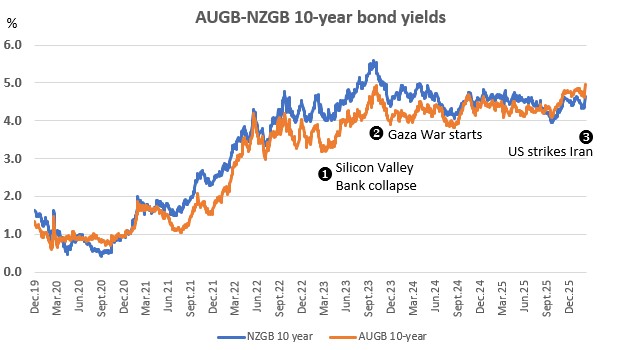

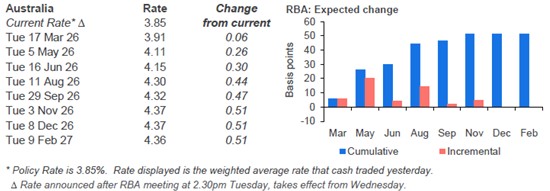

In Australia, these shifts are happening too, and they are actually more pronounced there.

Today, their 10-year Australian Government bond is up 12 bps and their two-year is up 11 bps - so far. It is very fluid.

Making things more interesting is that Aussie benchmark rates are higher than Kiwi ones. This isn't usual.

But now the Aussie 10-year premium is more than 35 bps. For the two-year it is a massive 106 bps.

This is signaling that Australia has a more pressing inflation risk problem than New Zealand. The Reserve Bank of Australia policy rate, the cash rate target, is likely to move sooner than in New Zealand, maybe as soon as May. (The RBA's cash rate is at 3.85% versus the OCR at 2.25%).

Of course, it isn't these rates that drive our home loan money costs. It is swap rates.

So check back at about 5pm today to see how these have moved. We suspect, by a notable amount. They have certainly moved up recently after the last OCR review.

Update: The one year swap rate rose +6 bps to 2.79% Monday, and the two year rose +18 bps to 3.30%

Daily swap rates

Select chart tabs

Then again, volatility is rarely stable. Inflation expectations have only been rising since Trump's adventure. And with supply chain disruptions compounding commodity price rises, the cost of imports seem unlikely to hold (or decline).

A look at history (Global Financial Crisis, the pandemic, as examples) shows what is at risk for borrowers pre-crisis. Post-crisis falls only happened because public policy leaders decided to shovel the taxpayer balance sheet at the problem. You might be brave to assume that would happen again.

5 Comments

I'm going to be like a broken record but I still can't get my head around central banks constantly ignoring >3% reported CPI data and always expecting imported deflation to save them instead of just raising rates - like we should have at the last review (in my opinion).

I guess it is 30 or so years of recency/confirmation bias that is deceiving them into such thinking. "We can just do nothing and we'll import some more cheap foreign made goods and that will lower living costs..."

I personally think this is naive thinking if you look at rates over 100+ years of data - and not just one's own life experience. Do they study history at the RBNZ? Or do they just set policy that is going to be good for their own net worth - ie lower rates providing the 'wealth effect' to the economy via property, share, bond prices. (I'm trying to get my head around this obvious bias they have towards lower rates, instead of higher rates when needed).

Raising rates at the last review, given CPI outside the mandated band and trending up, and the risk of a Middle East conflict, would have put us in a much better position now, than we are going to be. It is likely that we will be behind in a rate hiking phase that could well now need to be much more aggressive and lengthy than it could have otherwise been.

they are bombing oil refineries which can take months/years to rebuild, they can only be rebuilt once the bullets/bombs stop falling and it's safe to bring in the boys.

if they look through $150-200 oil, we will need Paul Volcker style fed rates to stop inflation.

Swapa chop chop. Lock n load rates are going to have to rise. Oil shock, job losses, Priivate credit shocks, and the Orange Swan adopting gun boat diplomacy.

How many black swan swans do ya need..?

Its multi Swans, black, white, orange and brindle!!!

Sorry to say, leverged spruikers, the riskiest ARM mortgage market in the world, is only whats available in NZ ........ AND ITS ABOUT TO GO WILD!

its probably wise to accept that offer..... be quick

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.