The week after next, both the RBNZ and RBA will review monetary policy settings and review official interest rates.

The flurry will be kicked off on Tuesday May 7 at 4:30 pm (NZT) with the RBA announcing its rate decision.

On Wednesday May 8 at 2 pm, the RBNZ will announce its decision and release its Monetary Policy Statement.

Then on Friday May 10 at 1:30 pm (NZT), the RBA will release its Statement on Monetary Policy.

This time around no-one is quite sure what will happen - except that there won't be any increase in rates. The choices for both central banks is to either hold or cut.

The 'cut' option is on the table because inflation remains low, and below the mid point of each regulator's contractual commitment.

The 'hold' option is on the table because employment is strong in both countries and current growth is at good levels.

To 'cut' when things are trucking along ok is to use up some firepower ahead of when it is actually needed - when the end of the current business cycle actually arrives. That doesn't seem likely in 2019, from the vantage point of May 2019 at least.

Despite that, an increasing number of (self-interested) commentators are calling for cheaper money in the presumption that is will help them (sell more houses, make more mortgages, encourage consumers to spend more, make government borrowing cheaper and more palatable to increase, etc. etc.).

And an interest rate cut will almost certainly bring a fall in the exchange rate, so those self-interested in higher local export prices (for them) and higher costs of imports (for others) will be wanting that as well.

Overseas, other central bank colleagues are growing gloomy. The central bankers in Sweden, the EU, Japan South Korea, and Singapore have all recently issued analysis that is on the dour side. Following them - even if our local situation is relatively healthy - might seem the safe, go-with-the-crowd thing to do.

Speaking of the crowd, financial markets are pricing in cuts for both the RBA and the RBNZ.

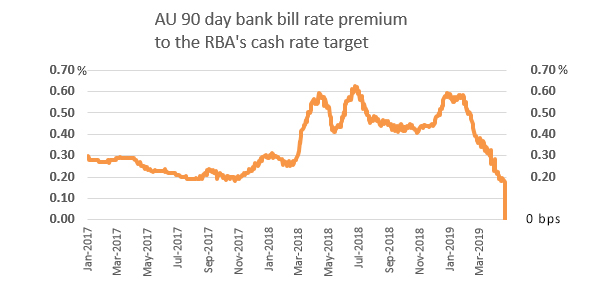

In Australia, the RBA's own monitoring of market interest rates is clear and dramatic, especially since the pre-Easter Aussie CPI undershoot.

This chart records the difference between the RBA's official cash rate target and the 90 day bank bill rate (to be precise, "Bank Accepted Bills/Negotiable Certificates of Deposit-3 months" in their series FIRMMBAB90D). The average premium in 2017 was +24 bps, in 2018 it was +45 bps and until the AU CPI in 2019 it was +41 bps. Now it is zero, and that suggests a May 8 cut from the current 1.50% by -25 bps to 1.25%. Expect the AUD to fall, even if you think this cut is priced in already.

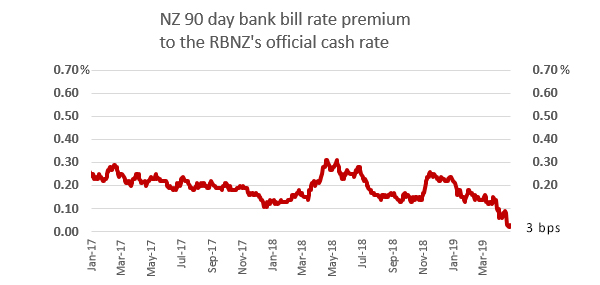

In New Zealand, the situation is less certain and over the recent years less volatile. Still, market signals here are also fairly clear, if not quite so dramatic - perhaps 'chronic' is a better description.

This chart records the premium of the 90 day bank bill rate in the RBNZ daily series over the Official Cash Rate. In 2017 this premium average +21 bps, in 2018 the premium averaged +20 bps, while in 2019 it has fallen from +21 bps at the start of the year to just +3 bps today in a fairly regular discounting. Money market traders (mainly banks?) are betting real money an OCR cut will happen soon.

And almost all that bet is because Q1 CPI came in at +1.5% (and falling) when the mid-point of the contract the RBNZ has with the Government is +2%. Markets are ignoring economic growth, high employment, and the need to keep monetary policy powder dry. They think the big gun should be used now.

And of course, the RBNZ now has its own 'crowd' - a Monetary Policy Committee to make a collective decision (and no longer the sole responsibility of the Governor). There are now seven people on this committee, the Governor and three subordinates (Geoff Bascand, Christian Hawkesby and Yuong Ha), plus three outsiders. They are Professor Caroline Saunders of Lincoln University who represents the interest of the rural export sector, Professor Emeritus Bob Buckle at Victoria University and a long-time Wellington insider, and Peter Harris who until recently was the Council of Trade Unions' chief economist. But at their first group decision, it seems very unlikely any of them will promote their independence to rock the Governor's boat. Anything but a unanimous first committee decision would be a huge surprise.

If the RBA cuts and the RBNZ doesn't, the NZD will rise against the AUD. But the NZD will likely fall against the USD in a collateral effect.

If the RBA cuts and the RBNZ does as well, the currencies of both countries are likely to depreciate against the USD.

Ahead of all of this however, is what the US Fed will do. They also have meeting soon and it is this coming week with a decision to be announced Thursday, May 2 (NZT). Their previous dot-plot had indicated two more rate hikes in 2019 and the stronger-than-expected US Q1 GDP result should have given that impetus. They had shown a desire for 'normalisation' and a need to build monetary policy reserves ahead of a natural business cycle downturn. But markets are picking no change from the current 2.50% Fed rate this time, partly because the Fed is under pressure from the Trump Administration with the threat of a Trump sycophant (or two) to be appointed on to their board.

The next US Fed review is not until June 20 (NZT).

19 Comments

I'm for the RBNZ holding, although I understand the counter argument. If it's about us (NZ Inc) then we should hold. If it's about everyone then who knows. It's got to be about us. They are the RBNZ after all.

The AUDNZD daily chart could be a little himalayan and have Mr Kerr calling for the meds. Q2 fuel prices on track for big rebound

Would it not be more healthy for the RB to simply stop trying to fine tune rates to control 'the economy'. An economy needs more natural feedback.

It's become an unhealthy obsession during this creeping age of central bank planning and intervention - which I believe is setting us up for a move towards central planning in other areas of the economy.

Does anyone think that the price of credit is constraining the New Zealand economy currently? Is it hampering New Zealand businesses and hurting the consumer?

If anything, it's the availability of credit that's the issue, which is all down to structural changes and decisions.

Also remember that most commentators never met a rate cut they didnt like. It's human nature.

Banks don't need traditional depositors. In fact traditional depositors in NZ are moving (at a snails pace) to 3rd party services and some into alternative stores-of-value (Gold, Silver, Crypto). Companies like Tenpay, PayPal, Goldmoney, Bitpay, etc are all eating into the payment sector.

Banks are more credit creators so they better hope people keep using the NZD, which their loans are made in. People are finding it's getting easier to hold value in other currencies and commodities. If this capital flow goes from a trickle to a flood, we'll be having a VERY different interest rate discussion.

Quite wrong. Banks really, really need depositors, either retail (like most NZ banks) or wholesale (like some such as Rabobank, HSBC). Without them they cannot lend which is where their earnings come from. And without a 'healthy' deposit (liability) base, they will lose their license to operate from the RBNZ. For any one bank, even the largest, the 'thin air' argument never holds and isn't grounded in fact.

If banks get stressed with a shrinking deposit base, they will offer more (retail or wholesale) if they wish to stay in business.

The problem is that many depositors are 'lazy', allowing banks to treat with certainty what they call their 'replicating portfolio' - that is deposits that don't seem to move no matter what the price signal.

For many reasons, there is more money around for deposits than there are as opportunities to lend, which is why bank offer rates, and bond market yields, are sinking. Even when the price of money is cheap, there are not enough lending opportunities to balance the supply-and-demand scales.

And if you think rates are low in New Zealand, just look overseas.

Part of the problem is that investors want high-ish returns for no risk and little or no work. If you have the capacity to make your capital work (and take the necessary risks), you will have a better chance of a better return. But we are in a baby-boomer world, where many think they have 'earned' the right for something-for-nothing (which is where the clamour for deposit insurance comes from - a guarantee of zero risk. It is a moral hazard.)

None of this is to deny that low returns might encourage some to take speculative risks (housing, cyrptos, gold, art, etc) thinging these could allow better no-risk, no-work returns. But this is the fringe. Either you take a fixed return for low risk, or you accept more risk to get a better return. Nothing is guaranteed.

Yes and No. I am talking about traditional depositors, mums, dads, students, etc.

A banks fractional-reserve-requirement (deposits) can be made up from private investors and large stake holders. Mum and Pop depositors are not required. Those loaning money to buy property aren't (necessarily) required to hold bank deposits, just pay interest - a way in which banks make profit.

You argument doesn't stack up. You seem to be confused between banking as a service and having a bank as your creditor [aka, being a depositor].

Z B,

"those loaning money to buy property aren't (necessarily) required to hold bank deposits,just pay interest". What does that mean? Those who lend are the banks,not the depositors. Ordinary depositors are absolutely required to provide the banks with the greater part of their funding requirements,as stipulated by the RB.

Banks really, really need depositors, either retail (like most NZ banks) or wholesale (like some such as Rabobank, HSBC). Without them they cannot lend which is where their earnings come from. And without a 'healthy' deposit (liability) base, they will lose their license to operate from the RBNZ. For any one bank, even the largest, the 'thin air' argument never holds and isn't grounded in fact.

David, you are far more knowledgeable about this than me, but I'm going to take you on here. Most salary earners in NZ hold their income in retail banks. If a salary earner was asked to be paid differently, say cryptocurrency, you could imagine the strange looks and impression it would create. The retail banks have deposits mainly because they're the primary institution by which their income is received and distributed. The 'thin air' argument you refer to holds if we apply the commonly held belief that banks hold an equivalent amount of deposits as loans, not the capital requirements that you often refer to when discussing the argument that the banks are fully funded.

Great points J.C.

“Or you accept more risk to get a better return”

I think this is part of the problem – desperation has encouraged many down this path with the result that in the end too many have taken on far too much “more risk” to achieve only a marginally “better” return. Risk/reward consequently may be well out of step – some of those in the game may not fully realise this yet.

Central Banks have gone too far in trying to hold this current fabricated risk/reward model together – the ship is now creaking and buckling under the weight– constant intervention notwithstanding.

“Nothing is guaranteed”

Apart from the ‘Fed Put”?

Yes, the 'Fed Put' and the plunge-protection-racket seem to be relentless .. and is sustained due to the 'money market's' constant flight-to-safety, aka buying US Treasury Bonds - brought even when the US causes the problem. Simply 'put', the US is exporting its inflation globally.

Unfortunately for most readers, you're paid in NZ Dollars, dollars which comparatively have lost value .. Even before inflation, Even after a generous term deposit rate. As a store of value the NZD is slowly losing ground to products offered by 3rd party services and yes, eventually, maturing crypto markets.

‘’The bond market is much larger than the stock market.

In the U.S. alone, bond markets make up almost $40 trillion in value, compared to less than $20 trillion for the domestic stock market”.

https://www.fool.com/knowledge-center/5-bond-market-facts-you-need-to-k…

I’m sure you understand the bond market is where the big boys play – and where manipulation comes to the fore. If it lets go and falls to any significant extent the losses will be horrendous – the Central Banks really have created a noose for themselves – and investors.

Banks are not intermediaries of loanable funds: facts, theory and evidence - Michael Kumhof.

scarfie,

Who still thinks that banks don't create money?

As MMT'er Warren Mosler says (who made a LOT of money using his MMT insights and spent his life in banking), banks make loans and create deposits. Then they worry about reserves. The person on the loan desk doesn't worry about the bank's reserve position when they make loans they just worry about whether the borrower is a good bet. And if there aren't enough reserves in the system the central bank will supply them cause otherwise they lose control of interest rates .

The Governor would be wise to keep his powder keg dry , and do nothing until the global economy shows some clarity as to its direction

The US long term / short term rate curve has inverted , and this is an early sign of looming recession

Boatman,

But doesn't your second sentence answer your first sentence?

We, most of the world are entering a new economic phase.. Not that has happened before.. ie Japan

Low growth..and dropping interest rates.

The ;normal; way to increase growth is by dropping interest rates to the middle income section, to promote more spending (disposable income) and therefore more production...and or tax breaks, again increase spending/ disposable income.

But this time around its not going to work.

Any tax break or interest rate drop to the bottom section of the 50% middle income section of the population that is already on rent and income substitutes doesn't increase disposable income.

Tax break to the most of the rest of the middle income , most just pays off a few more bills / debt.

The same applies to interest rates.. Even thu HP on goods is cheaper , the middle section of income earners are simply borrowing more and that very quickly reaches a stagnation limit before and growth or stimulus to growth eventuates, at best very short term.

Also the current tax take is not large enough to to give a significant larger enough stimulus to the economy. Even the Government talks in 100s of dollars per yr..

A core problem is some much of multinational taxation on profits going off shore is being avoided.. Then throw in huge sections of our NZ business being operated tax free, be it by Treaty, trustee, or 'non profit.

This not being sorted in previous decades now make tax breaks to stimulate the economy impossible.. a joke.

The core issue is for a stable economy and society approx 50% of the national wage / salary/ bonus income bill should go to the 50% of the middle income earners.. with not substitutes required anymore for the lower middle section. This then also increases the tax take..

Growth drops as the 50% of the national wage bill moves out of the middle 50% because disposable income also drops.

This is a huge section in numbers of the population that can afford to buy/ replace lounge suits, fridges, cars/ restaurants, all the stuff that the nation produces to have growth.

Since this section has got out of the 50/50% wack so far, any stimulus from the normal tax break/interest rate drop is little more than catch up on day to day bills... And therefore will not work.

If the wage bill is not fixed.. ie adjusting the income balance , rather than redistribution by say taxation, the long term outlook will be further deterioration of the middle income 50%, much of it becoming unemployed.. moving into what should be the bottom 25% (of which the bottom middle already is.)

And a recession.

This is not just a NZ , or Japan issue.. the same situation is in Aussie and most of the western world.

Its not Rocket Science...

Destroy the main consumer , the disposable income, which we have been for the last 40yrs, and that destroy disposable income, no disposable income, products (even houses kiwibuild) become unaffordable, growth stops, unemployment...

Doesn't matter what banks/ RBNZ does, it not going to make any difference .. its now a moot point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.