It appears the Crown will start offering loans to small-to-medium-sized businesses.

The COVID-19 Response (Taxation and Other Regulatory Urgent Measures) Bill, passed under urgency on Thursday, authorises the Inland Revenue Commissioner to grant businesses loans under a “Small Business Cashflow (Loan) Scheme”.

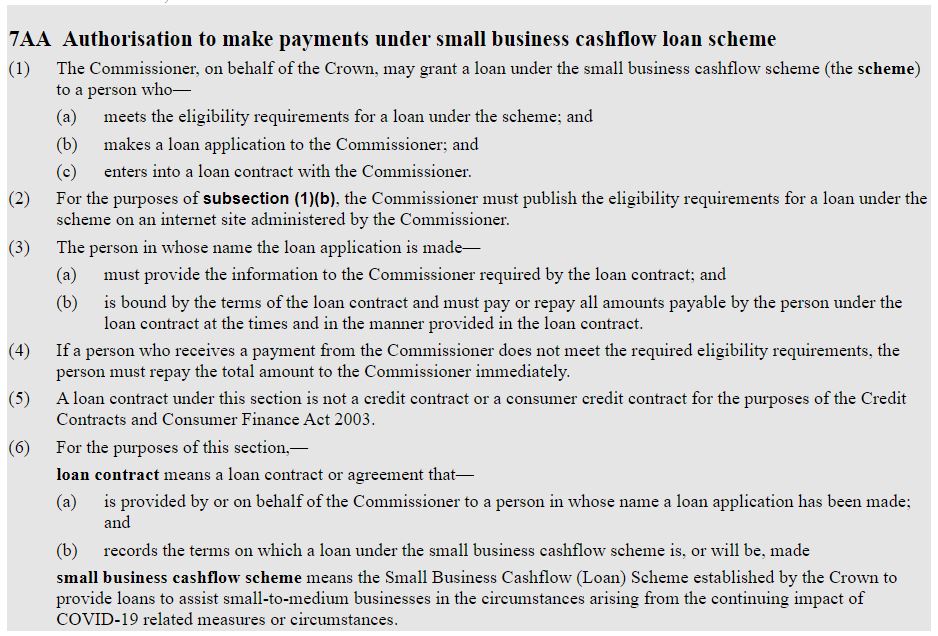

The Bill says the scheme will “provide loans to assist small-to-medium businesses in the circumstances arising from the continuing impact of COVID-19 related measures or circumstances”.

Revenue Minister Stuart Nash says the Government will make further announcements and provide more detail on Friday.

It hasn't at this stage revealed an eligibility criteria, the size of the loans, their terms, the interest rates that will be charged, and how credit risk will be assessed.

The Inland Revenue already administers student loans. In the US, a loan scheme for SMEs is overseen by the Federal Reserve.

The Small Business Cashflow (Loan) Scheme is distinct from the Business Finance Guarantee Scheme, through which taxpayers are underwriting 80% of individual bank loans to eligible SMEs.

While both Finance Minister Grant Robertson and Reserve Bank Governor Adrian Orr have urged banks to lend courageously to businesses under this scheme, banks will ultimately lend according to their own criteria and within their own risk appetites.

Banks can also only lend to businesses under the scheme if those businesses have exhausted other options with their banks.

Banks that are members of the New Zealand Bankers' Association wrote $5.9 billion of new business loans between March 26 and April 29.

To put this figure in context, there was $118.0 billion in business debt owed to New Zealand-registered banks as at March, according to Reserve Bank data.

Here's a snippet from the Bill:

By way of background, here's the eligibility criteria for the Business Finance Guarantee Scheme, launched on April 1.

Businesses must be New Zealand-based and have had turnovers of between $250,000 and $80 million at the end of the 2019 financial year.

The loan can only be used to meet urgent liquidity or bridging financing needs due to COVID-19 disruption.

Loan proceeds can't be used to cover capital assets/projects, distribution of dividends, on-lending outside the borrower's group, or to refinance existing debt unless it was advanced on or after March 16, 2020.

The maximum amount banks can lend to each business under the scheme is $500,000.

The maximum term for each loan is three years. Different banks will have different rules regarding terms.

The scheme only covers new lending.

Property development, property investment and agriculture are among the businesses excluded.

Borrowers can only take out a loan under the scheme if they've used their bank's existing facilities (other than credit cards, trade finance and other types of finance specified by banks).

If a loan is for $50,000 or more, the bank must use its best endeavours to obtain security from the borrower under a general security agreement.

Participating banks include ANZ, ASB, BNZ, Heartland Bank, HSBC, Kiwibank, SBS Bank, TSB and Westpac.

Note: Interest.co.nz previously reported an incorrect figure for average monthly new business lending by banks. The story has now been corrected.

71 Comments

Zoombie loans now available.

Did the bank say no if so no problem just call IRD for easy money.

Also coming soon house loans for any house the bank does not want to loan on.

Welcome to the bail out everything world.

Sobering thought, we where already extending and pretending. Shouldn't lending be left to banks? I wouldn't have thought IRD would have much experience in that field.

The State continues to try and get involved in every aspect of our lives, make decisions for us, keep us safe, insulate is from failure, pick us up when we fall, from cradle to grave. The State needs to step back, be responsible for defence, law and order and the justice system and allow the citizens to get on with living their lives and taking responsibility for the decisions they make. The State should guarantee our freedoms not stifle them. Other than that, what’s the whole point of life.

Quite right, in its purest form.

The biggest impediment to that is the cost, availability and creation of money.

Strip banks of those rights and see what % rate any business has to pay to stay afloat.

If that's not done, as it hasn't been, then every other item you may take issue with is a direct result of that failure. That is why we find ourselves where we are today. Our lives are held hostage to the Financial System.

The more they interfere the more control they get and like you say we have less control in our futures and I think they are starting to get a taste more power/control.

I believe Jacinda is obsessed with it and how she is portrayed overseas to the she will put us back to level for just to prove a point.

Also they say we are Covid19 free on media which is a lie but yet most media outlets are reporting how perfect everything is here.

Next front page for Time magazine anyone.

Feel your pain. When should we open for transtasman travel, I think that's the next risk the govt is ignoring. They say will go ahead under level 2 just in time for the ski season I suppose.

The generations in charge across all areas of government (not just the one or two young folk with high profiles) have so much of their money in property that the free market simply has not been allowed to apply to house prices, for one. Young people have been told it's all about personal responsibility and responsible choices, but housing has been a sacred cow protected from this.

Great post Homer

Actually, Mr Simpson, no.

There is an obligation to future generations, and not just of this species.

That is at odds with your statement, indeed what we need now is a Commissioner acting on behalf of future generations, and funded advocacy for their rights in the likes of the Environment Court.

Properly weighted (how many future generations versus just your selfish one?) that would just about stop all 'development' dead.

Which would just bring the inevitable forward a tad :)

The banks wouldn't even think about giving an interest free loan. I'm going to draw down the full 100k in my business then chuck it all into bitcoin and watch fiat burn to the ground.

Hopefully the definition of a person is a living breathing person, not a "legal person". I.e. there will be recourse from loan defaulters through personal guarantee, not just fold the company and run leaving the tax payer out of pocket?

That's a giant "NO" from me, thanks. It's like nothing is allowed to fail. Nothing allowed to go wrong.

You seem quite on the fence about this...

Normally I would agree but this time the issue for many businesses is that they have been shut down by the government and their failure is a direct result of the actions taken by the government. It is the equivalent of having your land taken from you with no compensation. Previous times businesses have been allowed to make their own way out. This time they have been banned from doing so.

I see your reasoning but do you think more debt is the answer? Debt is not compensation. Govt shuts you down then gives you a loan to "help". Sure, we don't have the details. They might be low interest (compared to banks - if it's possible to go lower than where we are now) or easily forgiven. But that's not really the point.

How about if 12 months down the line, those SMEs who did borrow from the bank and are then able to hold their own, get that debt written off? The Government remains a beneficiary through the tax income, the employees not on the dole and the spending in the economy. It would be a way of taking the money back out that they injected during this period, and without having the banks profiting from it.

LLCs allow them to walk away from a lot of that debt via shutting down.

.

Government != Pandemic.

It's a false dichotomy to think this was a choice of economic prosperity with no lockdown vs. economic failure with lockdown.

Good Lord, terrible terrible idea. What nonsense credit criteria are going to be employed ?

NINJA loans for Companies?

“Have you got a pulse” has worked well in the past..... The Aussie Banks could perhaps share their lending criteria which came through with flying colours during the royal commission.

Great.

Government getting into the business of Credit Risk.

What could go wrong.

Very much agree with you cmat

i would like to see the outline of how you qualify for this loan, if you had a marginal business before covid it should be left to fail, conditions after covid will be different and those that can adapt and change to a model that can survive and flourish only should be helped.

I like the idea. The IRD's management will tap into the businesses previous tax history & I'm hoping that only the one's who've paid some good tax over the past 3-5 years & are in cash-flow difficulty this year, will be eligible.

Most small businesses will pay a split salary to owners leaving nil profit at the company.

Under imputation the company tax rate is totally irrelevant - similarly the amount of company tax paid.

Tax records for the company will not indicate anything of value.

As of today, the IRD doesn't have any systems, staff or skills to manage a retail bank.

1. If the business can't get a loan from a bank under normal lending criteria one must question the wisdom of dumping the liability on tax payers.

2. Since when does the IRD have the commercial structures, systems, staff and skills to run a retail bank?

3. The loan is to a person and not a business.

4. Where are the strong cross checks to ensure loans do not become politically motivated?

5. If they don't relax their own directors liability legislations what level of practical help can it be?

I suggest to a degree this was inevitable. I have asked in other article comment streams what the banks were doing to support business, and frankly the answer was sweet FA. The banks are soaking up the easy money from the Government but still refusing to play the game. The ban on dividends will need to stay in place for quite a while. In the meantime the Government needs to figure out the legislation to limit the banks influence and power and stop them ripping off ordinary Kiwis.

Eventually some action was inevitable for sure, but the nature of the action was not and this has at least five major questions as I see it.

It reminds me of the US government desire to get poor people into home ownership. They used a government vehicle (fannie/freddie) and bypassed normal lending risk rules. In the end they setup the GFC and burned the very people they claimed to be helping.

Banks are not the problem here. Politicians with insufficient business acumen, but who believe they are the 'smartest people in the room', are the problem. When it goes wrong the losses will be dumped on the tax payer. Again.

Well put.

Huh? "Banks are not the problem“!? Sure 24hr 'always on' media has all but destroyed the talent pool for political office, now dominated by the venal and the beige... But to suggest the banks were hapless bystanders in the GFC and now? The slow motion debt crash about to envelop the world has been built on greed. Westpac's 23 million breaches of anti-money-laundering laws didn't come about because they had society's best interests at heart. Nor the nearly $5 billion repatriated every year to Oz. Which colour party you vote for, of the IQ of their front bench is irrelevant. If we don't work out how to call "bullshit"on the banks, and their venal politicians we're stuffed.

Banks were the willing vehicle for government policy.

Sure they were willing, but who is a bank to fight the government that grants its license?

Disagree that the banks are not the problem. the Government had already identified that it would partner with the banks and shoulder 80% of the risks. But the banks still are not making it easy for SMEs to weather this storm. Indeed from personal experience they have never really supported SMEs well at all. Yes some SMEs will not survive, but refusing to support them will ensure that happens for quite a few who could survive. Besides SME support also helps employment, as I understand it about 80% of employment in NZ is through SMEs.

The tax payer is already shouldering the burden. this happened when the Government ordered the lockdown and declared a state of emergency. The banks are a problem because they are rorting the system to make easy money from the government's relief packages. BS really! They are private business's and must be better regulated. Orr removing LVRs is another way banks are able to rort the system, and prop up the property market.

The government does not need to meet banking regulations and can loan to any bankrupt business. The IRD doesn't even have a retail banking staff to qualify loans. In this context the real difference is banks are more responsible and accountable than the government.

Borrow big, pay yourselves massive directors fees, liquidate company..yep what could go wrong if banks won't lend, there be a reason why.

It says the loan is personal, not to the business.

A welcome move by the government

It compounds directors personal liability.

You know the plan to ripoff.. hopefully won't happen though if IRD scales up monitoring of taxpayers which could be a good thing in the long run. Kill the cash economy and catch the property traders making undeclared profits.

IRD reimburses up to $20 work from home expenses

https://i.stuff.co.nz/business/121361974/coronavirus-ir-makes-it-easier…

Another example of a govt which is quite frankly clueless about how an economy functions. They can certainly squander tens of billions on subsidies and loans that are sure to be written off, but they cannot change human behaviour and instinct, no matter how hard they try. The inevitable reaction of business people will be to preserve cash, pay down debt and downscale overheads wherever possible. This won’t involve taking on more debt that they can’t pay off. A 10yr old would run this outfit with more intelligence...

And the previous lot were any better?

Meaning you agree, but there's no alternative.

As I commented last Sunday, Govt to increase AirNZ shares gradually in due course.

https://i.stuff.co.nz/national/121364096/winston-peters-hints-at-big-ch…

New norm : Get Cheap and Easy Money from Bank or from IRD or from Government with susidies and relief as government to run their country has no choice but to support one and all.

Collect everything and if fails blame Corona Virus and Government will pay the bill.

Election year.

Will throw money to get votes and who cares is Tax payers money.

It hasn't at this stage revealed an eligibility criteria, the size of the loans, their terms, the interest rates that will be charged, and how credit risk will be assessed.

Quite possibly because Der Gubmint, at the point of opening its gob to announce this, had zero idea of such details and/or was involved in a massive internal sh*tfight over the outline of 'em. I wouldn't bet the farm on anything coherent emerging.....let alone much cognisance of second and third-order economic effects.

I will need 1trillion for Kiwibuild for 1st time owners.........Me first...Please..April 1ST...No sweat...equity.

Link it to corona virus and do not be surprise if get the money.

Make hay while corona shines.

Need for some....Mint for many.

I wouldn’t be too worried about it!

Just like every other thing that this loser lot have announced, there is never ever any detail, as they never know how anything works.

[ Childish insults not acceptable. Don't do it, or if you must, just not on this website. Ed ] will be overseeing it wouldn’t he, as he is the minister for Economic Development, so of course it will be a success, just like everything else he has touched.

The loans to business that the Taxpayer is underwriting is not as it would seem.

There are very few businesses that actually meet criteria for these loans as there servicing is just not up to it.

What would you do The Boy? Please tell us. Do you want a large number of the small businesses to not reopen or open but fail in the near future. You keep telling us how clever and successful you are. Pray tell us. What should the COL do to keep the economy running as small businesses are the back bone of our economy and they employ a large percentage of the working population.

Firstly, businesses should be operating NOW!!!

This contactless online and phone stuff is just BS!

This continued lockdown by Ardern is just her showing her Socialist control that she has over many.

People that have been successful at business are all saying that we need to be open NOW!

What is the point of having fast food open and restaurants closed?

This Covid19 is not a killer virus at all, as a virologist staged on the AM Show this morning, it is only middle of the road!!!!

The influenza that we get every winter, kills more people and yet no business closes up.

The 19 deaths are geriatric people in rest homes with health issues that you would expect when you are in your 80’s.

time is up for Ardern and her offsiders, the natives are starting to see thru her and it will turn on her big time when people go back to work and find that they have lost their jobs, if things don’t pick up.

When it looked like we weren't getting enough cases to justify the ends, let's add probables to the mix and then not investigate them or test them. WHO figures don't recognise probables. Need to increase numbers to increase control.

The Boy this comment from you clearly shows that your love of money clouds your thoughts and judgment. If the government had not taken the action it has taken we would have had a lot more deaths and probably tens of thousands of people sick. Look at Europe and the USA where they have not taken early enough and strong enough measures to control the spread of the virus. The poll out today in the New Zealand Herald has very strong support of the government and the measures it has taken. I believe Labour will win the next election notwithstanding the pain caused by the lock down. Simon's support is evaporating quickly so Labour will win even though we are going into near depression like economic conditions.

Grandad, firstly yes the borders had to be closed, no problem with that.

They could’ve been closed earlier but it was done in time.

Secondly, it is BS that we were ever going to have thousands dead thru this and the fact is that no one under 69 has died and all that have were from rest homes effectively and had many underlying conditions and would’ve moved on thru the flu in the next month or two.

Forget the USA and England totally different kettle of fish.

More people are dieting from this because of the actions now from Ardern than the virus was ever going to cause.

Anyway, it doesn’t affect us at all it is all the other people who have worked hard and now because of the continued closures will find that they are financially impaired.

Anyway, hope your rest home is keeping you safe Gordon, from this so-called Killer Virus which is no worse than the normal flu.

Again the new economy to be created on More Loan / Debts .....

Does anyone know what is happening and where will it all lead to in long run.

Support yes but throwing money left, right and centre to anyone and everyone will not help and may turn out to be unproductive.

Commenters are forgetting something.

What security do companies have? Landlords own the property.

E.g. Who would lend to a company running a motel, who are leasing the premises? The company isnt worth much right now, heading into winter.

Would you prefer all of the experienced operators go bust a bunch of newbies take over? That is what is going to happen.

Not looking good. Have several diversified interests but the most concerning one is a glazing firm I am involved in. FC has received several letters from developers that we are mid way through installs with informing no further funds forth coming. Is this a looming credit crunch?

Govt directly issuing loans? They did shut down the country, so could be seen as reasonable. Could be MMT is in full bloom now, so let's just carry on, print, distribute, repeat.

When central banks start with central bank digital currency, they can issue directly to individual, so could be a test model.

Fiat is fiat, you need it to pay bill's,

Shopping and so on, yet you do not at this point, have to keep all your wealth in the fiat system.

It may be that confidence underwrites the fiat, yet confidence in alternatives is prerequisite to it's growth, and use. Should such growth in alternatives occur, then people will finally be able to signal to the central bank their view on constantly having their fiat devalued. This is central to individual sovereignty, and far more powerful than a ballot box vote.

I agree. When people realise this there's going to be a run on crypto. Probably still 6 months away though. When this happens, expect the govt to look for new ways of asserting power. Increased surveillance under the guise of keeping people safe.

A central bank issued crypto currency is quite a scary place for us to go. Watched a George Gammon video on YouTube where he explained how the FED could control it’s use. Give me Bitcoin over that any day!

The govt don't give a hoot about the NZD. Who's ready to pay for a loaf of bread with a wheelbarrow full of cash?

Good news is you can carry a wheelbarrow full of cash on a little plastic card in your wallet.

For now

Necessary, but will lead to lots of companies being propped up that shouldn't be. Likely those with scruples will go under, those without will keep trading... the law of unintended consequences that always comes with market distortions.

Another helping hand from MediaWorks !!!

https://i.stuff.co.nz/business/121370425/mediaworks-sets-up-20m-adverti…

2020 is the year when the nanny state is taking over and freedom in NZ is being lost at an alarming rate.

- we are not allowed to die

- we are not allowed to operate a business

- a business is not allowed to fail

- people are not allowed to get sick

- people are not allowed to see each other

- we are not allowed to travel

- we are not allowed to hug

- people are not allowed to play sports

- house prices are not allowed to fall

Some will agree with some of these restrictions but they do all fall in the same category,

LOSS OF INDIVIDUAL FREEDOM UNDER THE BANNER "PROTECTION" BY THE GOVERNMENT

“Those who would give up essential liberty to purchase a little temporary safety, deserve neither liberty nor safety.”

― Benjamin Franklin

Are you looking for a mortgage? Looking for a quick loan or a funding firm for a business deal, contact WEST-CAGE LOAN INVESTMENT GROUP at WESTCAGEINVEST@GMAIL.COM for a quick loan or investment. We welcome you for an opportunity to all types of loans you get at a very affordable interest rates of 2%

**Personal Loan (Secure and Unsecured)

**Business Loan (Secure and Unsecured)

**House Loan (secure and unsecured)

**Car Loan (Secure and Unsecured)

**Debt Consolidation Loans (Secure and Unsecured)

Best Regards,

Michael Courtney

West-Cage Loan Investment Group

WESTCAGEINVEST@GMAIL.COM

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.