The Government has provided more details on the regulation of merchant service fees, proposing Visa and Mastercard's debit and credit retail payments networks be formerly designated under law, and confirming plans for surcharging by merchants to be regulated by the Commerce Commission rather than banned.

Further details available on Thursday, follow plans to regulate the retail payments system announced by Commerce and Consumer Affairs Minister David Clark in May. These set out proposals to empower the Commerce Commission to regulate fees charged by banks and card companies such as Visa and Mastercard, that are paid by retailers and other small and medium sized businesses. For such businesses card acceptance fees are typically the third highest cost of doing business after wages and rent.

The Government says its proposals are likely to reduce the profit margins of banks and the Visa and Mastercard debit/credit card schemes in New Zealand, and estimates regulating merchant service fees will save consumers and merchants $74 million annually, and cost the Government between $6 million and $10 million a year to run.

A cabinet paper from the Ministry of Business, Innovation and Employment in the name of Clark notes New Zealand merchants pay more than their Australian counterparts for accepting credit cards and online debit cards. This is due, at least in part, to a lack of efficient competition in some aspects of the retail payments system, it says. To address this, Cabinet agreed to set up a regulatory regime for the retail payments system, with the Commerce Commission as the regulator. Australia, and other countries, have regulated retail payments for years.

Key in May's announcement is plans to regulate interchange fees. These are typically the biggest part of the broader merchant service fee, comprising about three-quarters of it. Each bank sets its own interchange rates within a cap set by Visa and Mastercard. The merchant service fee is set by banks.

Clark said the Government will cap interchange fees for credit card transactions at 0.8%, which is in line with Australia, and cap interchange fees charged for online debit card transactions at 0.6%. Contactless debit card interchange fees will stay at their current levels of 0.2% or less, and for swiped and inserted debit, will stay at 0%. (Last year I argued the Government should simply ban interchange fees).

What designation means & EFTPOS 'important to NZ'

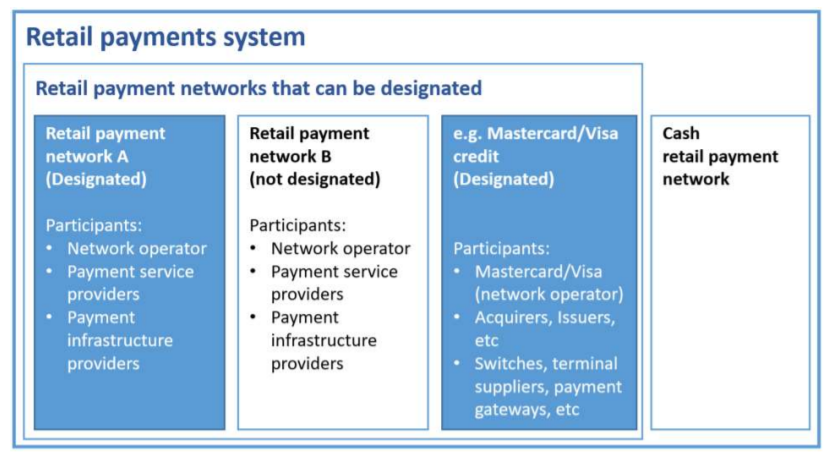

Cabinet has now agreed to establish a regulatory regime based on a designation model, whereby the primary legislation would define the retail payments system in a broad sense, and set out the criteria and process for designation. This is similar to what Australia does.

The Retail Payments System Bill will include initial designations of the Mastercard credit, Visa credit, Mastercard debit and Visa debit retail payment networks (RPN).

"The RPN captures all the participants operating in a RPN, which, in the course of business, enables the transfer of funds within the RPN. All payment instruments within each RPN are captured. For example the Mastercard/Visa credit RPNs include not just physical cards but also any payment instrument including tokenised credentials such as virtual cards, including methods like Apple Pay and Google Pay. Reference to RPNs will ensure the designation applies more broadly, without targeting just the specific entity that is operating or maintaining the RPN. This distinction will provide for dynamism of RPNs and allow the regulator to target the parts of designated RPNs that are causing issues," the cabinet paper says.

The Bill will define retail payments system "participants" to include payment service providers, infrastructure providers and network operators integral to the operation of a RPN.

"For example, should the EFTPOS RPN become designated, these powers could be used to change the RPN to provide for innovation such as contactless and online capability. This would enable EFTPOS to provide competition to the Visa and Mastercard debit RPNs where it currently does not (e.g. contactless and online) and improve the resilience of the EFTPOS RPN. I consider the resilience of a domestic RPN like EFTPOS to be important for New Zealand," the cabinet paper says.

Regulating surcharging

Clark says the Commerce Commission should have the ability to regulate surcharges applied by merchants, in order to limit excessive surcharging that doesn't reflect the costs to the merchant of providing those particular transaction types.

"I propose this utilise the existing prohibition under the Fair Trading Act, by the Commission issuing standards as to how payment surcharges can comply with the Fair Trading Act, to inform merchants as to what can and cannot be factored into a surcharge. In setting standards which have legal effect, the law will essentially provide merchants that set surcharges in accordance with the standards a safe harbour for compliance with the Fair Trading Act. The Commission would continue to enforce misleading surcharging under the Fair Trading Act."

"Some stakeholders proposed that surcharging should be prohibited altogether, as it may not be justified where interchange fees are regulated. However, regulating the input costs of merchant service fees does not necessarily remove those costs altogether for the merchant. Surcharging, if done reasonably, may still be useful for merchants to steer consumers towards lower cost methods," says Clark.

ComCom to monitor & study competition

He also wants the Commerce Commission to have "broad powers" to monitor and conduct studies into the state of competition in the wider retail payments system. This, he says, will be integral to enabling the Commerce Commission to effectively monitor the regime and determine when a RPN may need to be designated. The Commerce Commission could produce public reports on the state of the retail payments system, including on the levels of merchant service fees in the market.

"The Commission would also have the ability to require participants in the retail payments system to produce new information to support this monitoring function. These powers align with the Commission’s monitoring powers under the Commerce Act. Given the purpose of the monitoring and enforcement powers is to enable the Commission to monitor the overall state of the retail payments system, I recommend that the Commission should be allowed to exercise these powers against all participants in the retail payments system (i.e. both those who are participants in designated RPNs and non-designated RPNs)."

Penalties outlined

The cabinet paper also details proposed penalties, which it says are consistent with pecuniary penalties for similar compliance failures in the Commerce Act, Fuel Industry Act and Financial Market Infrastructures Act.

Here's more from Clark in the cabinet paper on penalties.

The volume of transactions across the New Zealand economy and potential for commercial gain from a breach is significant such that high penalties are appropriate for certain breaches, particularly of price regulation. The legislation will specify maximum amounts where an individual (e.g. a director of a company) is liable, and where a body corporate is liable. I consider these maximum penalties should be:

Pricing standard: Where a network operator, payment service provider or infrastructure provider in a designated RPN has failed to comply, they would be liable for maximum pecuniary penalties of $500,000 for an individual or $5 million for a body corporate;

Access standard: Where a network operator, payment service provider or infrastructure provider in a designated RPN has failed to comply, they would be liable for maximum pecuniary penalties of $200,000 for an individual or $2 million for a body corporate;

Information disclosure: Where a network operator, payment service provider or infrastructure provider in a designated RPN has failed to comply, they would be liable for maximum pecuniary penalties of $200,000 for an individual or $2 million for a body corporate;

Directions to make or amend rules: Where a network operator of a RPN has failed to comply, they would be liable for maximum pecuniary penalties of $200,000 for an individual or $2 million for a body corporate;

Directions to comply with network rules: Where a network operator, payment service provider or infrastructure provider in a designated RPN has failed to comply, they would be liable for maximum pecuniary penalties of $200,000 for an individual or $2 million for a body corporate;

Submission of substantive rule changes to the Commission: Where a network operator, payment service provider or infrastructure provider in a designated RPN has failed to comply, they would be liable for maximum pecuniary penalties of $15,000 for an individual or $150,000 for a body corporate;

Enforceable undertakings: Where a body corporate in the retail payments system that is party to an enforceable undertaking (with the exception of the Commerce Commission) has failed to comply with an undertaking, they would be liable for maximum pecuniary penalties of $500,000;

Visa & Mastercard can't compensate their card issuers, impact on rewards schemes

Cabinet has also agreed to a transitional price path for Mastercard and Visa credit and debit products, to come into force within six months after enactment. Thus Clark wants initial designations for the Mastercard and Visa schemes and initial pricing standards be included in schedules to the Bill, saying this will provide greater transparency for regulated parties as soon as the Bill is enacted. Both the initial designations and the initial pricing standards should also be able to be amended, or revoked, he adds.

"Alongside the initial pricing standards for Mastercard and Visa products to be included in the Bill, I think the Bill should include an additional aspect to the initial pricing standard to provide that the scheme operators cannot provide net compensation to [card] issuers [these are typically banks]. By increasing the scheme fees for acquirers and reducing it for issuers a scheme can provide a “net compensation” to the issuer to compensate them for a reduction in interchange income," Clark says.

"This will address a possible flow-on effect of reducing interchange fees. International experience suggests that schemes are likely to help banks regain lost revenue from interchange fee reductions by increasing scheme fees to acquirers and reducing scheme fees charged to issuers. These fee changes are not currently prohibited by the initial pricing standard that Cabinet has already agreed to for Mastercard and Visa products. These types of fee changes effectively result in no net cost reductions for banks and other operators providing both issuing and acquiring services."

"Given the likelihood of this risk, I recommend prohibiting net compensation by schemes to issuers in the initial pricing standard. This would prohibit issuers from receiving, directly or indirectly, a net compensation. Compensation should include monetary (i.e. reduced scheme fees) and non-monetary effects (i.e. discounts on rewards, reward programmes offering prizes to customers etc)," Clark says.

In 2016 MBIE estimated merchants had to increase prices to all consumers by about $187 million annually to fund rewards paid to certain credit card users.

Meanwhile cabinet has agreed to initial tagged contingency funding of $5 million for the Commerce Commission to monitor and enforce the transitional price path comprising $4 million in operating funding and $1 million in capital funding.

In terms of ongoing financial implications beyond 2021-22 to implement the full set of regulatory, educational and stakeholder interventions, these are estimated to cost between $6 million and $10 million a year to implement.

"To alleviate some of the costs, I consider that costs incurred to consider and assess enforceable undertakings and review and approve substantive network rule changes should be recovered through fees. The ability to impose fees to recover costs is limited to the exercise of this power given that an enforceable undertaking provides a benefit to an individual participant," says Clark.

"To enable this, I am seeking approval for the Bill to include a power to recommend the making of regulations for the Commission to recover, through fees, costs incurred in the exercise of a power at the request of an individual participant...The initial pricing standard should commence six months after enactment of the Retail Payments System Bill, to allow regulated parties sufficient time to make any necessary changes in order to comply."

The cost to the Government & savings seen for consumers & merchants

In terms of the regulatory impact statement, this argues competition in the retail payments system (eg payment networks for clearing EFTPOS, debit and credit card transactions), and the application of generic competition law, is insufficient to constrain unreasonably high merchant service fees, thus imposing inequitable costs on some segments of consumers and businesses.

"While various agencies are responsible for overseeing prudential, conduct and competition regulation in the system, there is a gap in overall regulatory oversight of the retail payments system specifically, which is constantly evolving with no single regulator with the capacity and responsibility to keep up. In April 2021 Cabinet agreed to establish a regulatory framework to ensure the retail payments system delivers long-term benefits for consumers and merchants in New Zealand."

"Cabinet agreed to establish a designation model, which will set the parameters of regulation in primary legislation to give the Commerce Commission (Commission) a mandate to regulate designated retail payment networks and participants within those networks. Cabinet agreed that the Commission would have a package of tools to include the ability to regulate interchange fees, information disclosure powers and regulation of other price aspects in the retail payments system," the statement says.

"Overall, the package of proposals considered in this and the previous impact statement are likely to reduce the profit margins of banks and debit/credit card schemes in New Zealand. The proposals will involve a cost to government to cover new regulatory functions of between $6 million and 10 million per annum," the statement says.

"We estimate that across annual retail sales of $97.6 billion, a 20 per cent reduction in credit card interchange fees and a 30 per cent reduction in online debit interchange fees would equate to savings for consumers and merchants of $74 million."

*This article was first published in our email for paying subscribers on Thursday morning. See here for more details and how to subscribe.

6 Comments

So BNPL services would also fall under this?

BNPL service providers do charge very high merchant service fees. But my understanding is the Government is largely looking at BNPL separately - https://www.interest.co.nz/personal-finance/110754/buy-now-pay-later

Great move from the government, not often stoked to see them getting fingers into pies.

I've got it in writing from my bank that my credit card will keep it's equivalent ~1% kickback as long as I keep the account open, I'm looking like a very unprofitable customer in future!

Have you also got it in writing that the annual card fee won't go to $bignum with no fee waivers?

Good. Now if we could just get them to pay some tax in NZ.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.