Here are the key things you need to know before you leave work today.

MORTGAGE RATE CHANGES

Unity Credit Union raised all their fixed rates today.

TERM DEPOSIT RATE CHANGES

Both BNZ and Westpac raised their term deposit offers by between +10 bps and +30 bps. Unity Credit Union raised their offers by more.

RENTS FLAT

We have updated our median rent charts for most New Zealand districts based on MBIE tenancy bond filing, and on average they are little changed in February from the recent prior months. Wellington rents are stepping back, except in Wellington Central. And Dunedin rents, which took a big jump in January, reverted to normal in February.

'HUNKERING DOWN'

ANZ's monitoring of nationwide traffic movements is sobering reading. The Light Traffic Index fell -1.8% in March, while the Heavy Traffic rose +1.8%. The data is consistent with people reducing their movement as the Omicron wave spread throughout New Zealand over the month.

IT HURTS BUT ABLE TO COPE, SAYS A BIG BANK

More than two-thirds of New Zealanders are confident they can cope with rises in the cost of living and more than half are already taking positive steps to manage their finances, according to a survey of more than 1,600 Westpac customers. It apparently found 97% of people are worried about the cost of living over the next 12 months. 83% are concerned about the impact of inflation on their own lives, well ahead of the economic impacts of COVID-19 (57%) and the Russian invasion of Ukraine (52%). Younger customers and families with young children are especially worried. But the survey also found respondents were also open to lifestyle changes that could save them money. 29% have already found alternative forms of transport to driving, while another quarter are considering it. Also, more than half have either bought a more fuel-efficient car or are considering it.

OUR ONLY TRILLION DOLLAR MARKET

The RBNZ has updated its record of the value of all residential property in New Zealand (M10) as at the end of 2021, which booked a rise of +$100 bln (not a typo) in the three months from September to December 2021. While that may seem like a lot, it isn't a record. The record is +$127 bln in the three months to March 2021. For the 2021 full year, the rise was +$377 bln. All these dwellings are now valued at $1.76 tln. So the increase in 2021 was +27%, and only exceeded by the 31% rise in 2003. If all dwellings are now valued (by CoreLogic) at $1.76 tln* and we had collectively borrowed $331 bln against them (C5), then the national LVR is just 19%. If values fell -50% (not saying they will), then the national LVR would be 38%. (*Even in USD, this is a US$1.22 tln valuation.) If house prices kept going up at the 2021 rate (and it is doubtful they will), then we would reach a $2 tln valuation by the end of July 2022.

MIXED PROFITS FOR 2 OF NZ'S CHINESE BANKS

Two of New Zealand's Chinese owned banks have filed annual financial results. China Construction Bank (New Zealand) Ltd recorded a $9.5 million, or 74%, jump in annual profit after tax to $22.3 million as income rose while expenses and impairment losses fell. Industrial and Commercial Bank of China (New Zealand) Ltd posted a $1.012 million, or 8%, drop in annual profit to $11.526 million. Although income rose, expenses and impairments both rose too.

RESILIENT ENOUGH?

In Australia, the RBA has released it Financial Stability Review. It found that while local systems are resilient, Russia's European invasion and other global pressures will cause volatility which they thing they are prepared for. They say borrowers should brace for a -15% fall in home prices as interest rates rise by +2% or more. But they are confident the vast majority of borrowers will be able to manage rising repayments as rates increase.

GOLD FIRM

In early Asian trading, gold is up +US$10 from yesterday at just on US$1932/oz.

EQUITIES VARIABLE

Wall Street had an 'up' day with the S&P500 ending up +0.4% at their Thursday close. After starting strong, Tokyo is now -0.3% lower in late morning trade and heading for a weekly loss of -3.2%. Hong Kong has opened down -0.7% and on track for a weekly dip of -0.2%. Shanghai is down -0.6% at their opening and heading for a loss of -1.2% for the week. The ASX200 is up +0.6% in early afternoon trade and heading for a flat week, while the NZX50 is flat in late Friday trade and may end the week little-changed.

SWAPS HIGHER

We don't have today's closing swap rates yet. They are likely to be a little firmer yet again from yesterday. The 90 day bank bill rate is up +1 bp at 1.68%. The Australian Govt ten year benchmark bond rate is up +4 bps from this time yesterday, now at 2.97%. The China Govt 10yr is little-changed at 2.80%. And the New Zealand Govt 10 year bond rate is now higher again at 3.49% (up another +4 bps) and still well above the earlier RBNZ fix for that 10yr rate at 3.45% (up another +4 bps). The US Govt ten year is now at 2.65% and up +7 bps settling since this time yesterday.

NZ DOLLAR SOFT

The Kiwi dollar is now at 68.8 USc and -30 bps lower today. Against the Aussie we are a tad lower as well, now at 92 AUc. Against the euro we are little-changed at 63.3 euro cents. That means the TWI-5 is now at 74.5, softer than yesterday but not by much.

BITCOIN STALLS

Bitcoin is little-changed from this time yesterday and still at US$43,583. Volatility in th epast 24 hours is low at under +/-1.0%

This soil moisture chart is animated here.

Keep ahead of upcoming events by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

23 Comments

Most nzers will cope with mortgage rates increasing , but it will be at the expense of discretionary spending elsewhere. This will lead to some contraction in other businesses probably mainly hospitality. I don't think there will be many mortgage sales but quite a few may end up in negative equity.

Second townhouse development mortgagee sale in a week - perhaps more an issue for developers than home owners?

https://www.stuff.co.nz/business/128289770/second-auckland-townhouse-de…

I don't know how you can say that you are ruling out the possibility that there there will be lots of mortgagee sales in a year or 2.

I see on the NZX today they still have enough money to buy double priced meals from MFB, obviously the rate rises havent hurt or kicked in yet. A backwards looking report from MFB i think.

Yes it will be a return to the 70's and early 80's with dinner out being takeaway Fish & Chips once a month and Chinese takeaways was a special treat on Birthdays. Mind you you have trouble getting Chinese that good anymore, it used to be legendary from the "Flying Horse" in Takapuna and we used to sit and eat it down the pumphouse by lake Pupuke. Those were the days.

You have to wonder why the Chinese banks bother here? $9.5 million NZD must be like a rounding error to them.

A foot in the door. Certain staff can do certain functions, official & unofficial. Not unique to NZ. Recall for instance, not long, some were repatriated by the USA for activities far removed from those of normal banking personnel.

Chris Tremain left politics to go work for the local branch of a Chinese bank. I suspect a carrot was dangled.

It could be for diversity of income however I suspect that their NZ income in future will be somewhat curtailed!!!

(Chinese developers here have yet to learn the lesson that prices can drop in NZ and nobody is going to bail them out).

Yes there were hardly any Chinese developers here when we had the last big development slump in 2007.

Wall Street had an 'up' day with the S&P500 ending up +0.4% at their Thursday close.

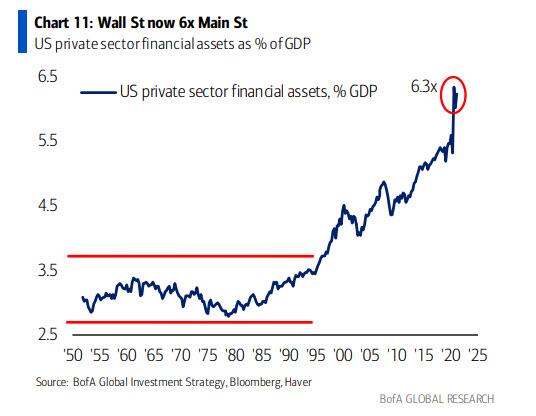

... the hyperfinancialized US economy, with its 6.3x financial assets to GDP..... will force the Fed to not only end tightening early but to rush into an easing cycle. Link

{kind=link}

Crazy huh - I think our housing market is the equivalent of their financial markets/assets.....departed any sense of normality in the early 2000's and has been way off course ever since. An unsustainable anomaly as opposed to any long term normal.

The RBNZ has updated its record of the value of all residential property in New Zealand (M10) as at the end of 2021, which booked a rise of +$100 bln (not a typo) in the three months from September to December 2021. While that may seem like a lot, it isn't a record. The record is +$127 bln in the three months to March 2021. For the 2021 full year, the rise was +$377 bln. All these dwellings are now valued at $1.76 tln.

Reserve Bank governor Adrian Orr is not doing himself any favours with his revisionist approach to the house price issue. Not so long ago, he was saying increasing asset prices, including house prices, were a feature and not a bug in the bank's policy response to the pandemic because they make consumers feel wealthier and spend more. This week he suggested his bank's policy settings have only a minor impact on house prices.

He actually has quite a bit to answer for. The bank has been consistently under-forecasting increases in inflation and house prices, and overforecasting unemployment. While no one is expecting perfection in these times, the ongoing nature of the forecasting issues is concerning. Link

"If house prices kept going up at the 2021 rate (and it is doubtful they will), then we would reach a $2 tln valuation by the end of July 2022."

"But the survey also found respondents were also open to lifestyle changes that could save them money. 29% have already found alternative forms of transport to driving, while another quarter are considering it. Also, more than half have either bought a more fuel-efficient car or are considering it."

Wow, almost 30% of people have found alternatives to driving. Sort of puts paid to all those arguments about having to drive and there being no alternatives. Turns out car dependency is a choice after all. Hopefully this change sticks. Means less emissions, healthier happier people, more road space for those that really have no alternative to driving and no more wasted money building pointless roads, silver lining and all that.

Depends how the question was phrased. If you walk to the dairy once does that count?

Yes depends whether the party behind the survey has a desired outcome in mind. Reminds me of Ak council consultation where all the multichoice questions are completely biased and leave no room for counter arguments. Except perhaps in a field after them, which you know will be ignored in the summary of responses.

Yes, it does count. In Auckland if you removed all the car trips that are under 5km we'd be pretty much sorted transport wise.

Yep, almost everyone has a price point that will change their behavior. $20 a litre might save our species :)

Ray Dalio Interview

If only we had invested $100b into NZ companies instead of mostly shitty houses...

https://www.roymorgan.com/findings/8942-nz-national-voting-intention-ma…

Potential National/Act NZ (47%) coalition retains a large lead over Labour/Greens (42.5%)

Unfortunate that rental prices have remained elevated, a reduction would likely have been very welcome in tempering inflation.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.