Analysts with investment and advisory group Jarden have put a 'sell' recommendation on Air New Zealand [AIR] stock and see the airline making a full-year, pre-tax loss of $134 million.

The analysts also see Air New Zealand continuing to lose money in 2027.

Air New Zealand recently reported an after-tax loss of $40 million (pre-tax loss $59 million) for the first half of the year (compared with a profit of $89 million for the first half of 2025) and warned that the second half results could be even a little worse.

No dividend was paid and the airline said a strategic review was under way.

The loss has prompted a political debate over the state's 51% ownership of the airline.

Jarden analysts Grant Lowe and Zachary McIntyre say their updated forecasts assume a second-half net profit before tax (NPBT) loss this year of $75 million, bringing the full year pre-tax loss to $134 million.

They've moved their 12-month 'target price' for Air New Zealand stock down to 47c (the most recent on-market price was 54.5c).

"We move to a 'sell' rating with the stock trading materially above our spot valuation and with clear downside risks linked to engine maintenance issues, a weak macroeconomic backdrop, increasing competition and structural increases in the opex base over coming years. Greater visibility on the anticipated cost-out programme and plan to restore earnings to more economic levels could see us take a more positive view on the stock. Risks include engine maintenance issues, international and domestic travel demand, fuel prices and competitor capacity."

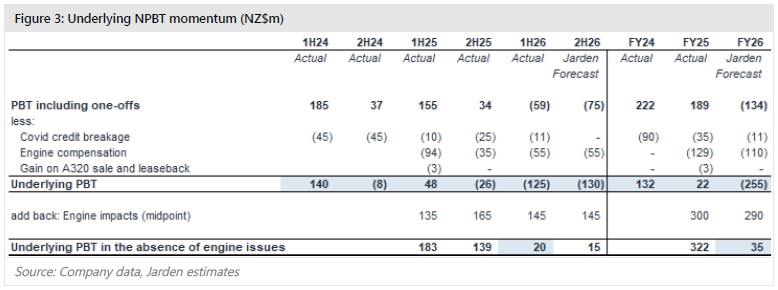

The analysts noted that the half-year result included the benefit from $11 million of unused Covid credits booked to revenue (now complete), and $55 million of compensation from engine manufacturers.

"Adjusting for these, and [Air New Zealand's] estimate of the impact from engine issues suggests an underlying 1H26 NPBT [net profit before tax] of just $20 million, assuming AIR had operated with a full fleet (Figure 3). This clearly highlights the issues that AIR is facing."

The analysts say their full-year loss pick of $134 million would equate to a $255 million loss excluding one-offs.

"Further adjusting for ~$290 million of lost profits from engine issues (i.e. doubling AIR's 1H26 estimate of ~$145 million), suggests that, even in the absence of engine issues, AIR’s underlying FY26 PBT would only be ~$35 million. In our view, this clearly highlights the impact of additional competitor capacity, underlying cost pressures, a soft macroeconomic backdrop, and domestic yields maxed out for now."

Lowe and McIntyre say they assume that new plane deliveries and easing engine issues will add capacity in FY27, but that the earnings recovery is likely to see some lag.

They say they note the airline's commentary that there is likely to be a lag on revenue following the return of engines (and end of compensation), with Air New Zealand having to err on the side of conservatism with scheduling and ticket sales. The airline also expects some impact on the cost side as it manages the exit of existing aircraft leases.

"Considering these factors, we assume a loss of $60 million in FY27 before a return to modest profitability in FY28. We assume a return to dividends in FY29, given our forecast losses in FY26 and FY27, and gearing remaining elevated through FY28."

1 Comments

NZ commenced its commercial aviation handling domestic flights with NAC which was seperate to the international counterpart with TEAL in joint ownership with Australian interests. TEAL became AirNZ under full NZ ownership and then was merged with NAC. Since then other international airlines have commenced services and in fact easily have thr ability to be of sufficient service for all international passenger travel. But it is still essential for NZ to have independence and security for its domestic travel and international and domestic freight. Perhaps it’s time to now concentrate on doing the essentials first and foremost and doing them well.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.