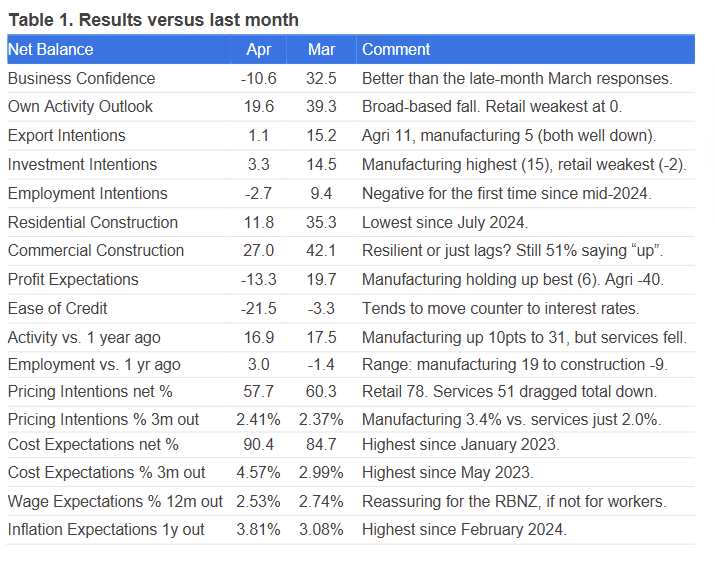

Business confidence took a hit over the last month with ANZ’s latest business outlook warning of a “wall of worry” as confidence fell in April.

The net percentage of those expecting/reporting improvement and those expecting/reporting deterioration went from 32.5 in March, to -10.6 in April. While it paints a bleak picture, the average in late-March was even lower at -22.5.

Agriculture was at -48.6 and services at 18.6, while confidence in construction was at 19.6.

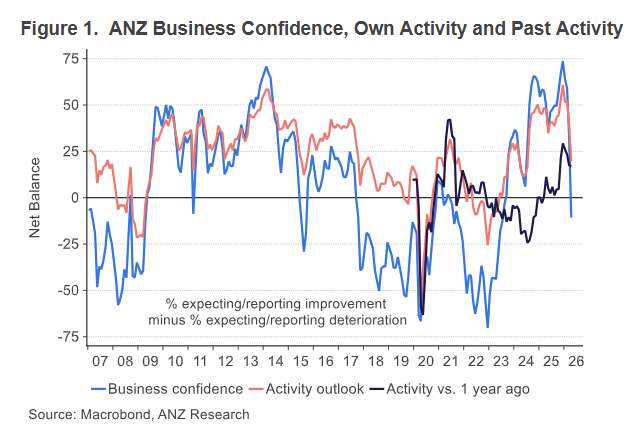

On inflation, expectations rose to 3.8% in April, from 3.1%.

Indicators trended higher “unsurprisingly, with a sharp lift in expected costs and inflation expectations, though pricing intentions dipped slightly in the month”, the report said.

Uncertainty around inflation was rising, which was making decision-making and planning harder for firms.

Price expectations from the three months to went just to 2.41% from 2.37%, while cost expectations rose from 2.99% to 4.57%.

ANZ’s chief economist Sharon Zollner’s take was that while businesses were concerned about the outlook in the face of a significant cost shock, and “although the charts are ugly, many activity indicators (both forward and backward-looking) were actually higher this month than in the late-month responses received last month.”

Zollner said this suggested some of the initial confidence shock had dissipated.

Activity compared to a year ago was at 16.9, slightly down on March’s 17.5. Agriculture was at 34.3, Manufacturing was at 31.2, while the construction sector was at -2.2.

There was a broad-based fall in expected own activity, falling from 39.3 to down to 19.6.

The survey found manufacturing was “leading the charge by quite some way” when it came to the rise in reported past employment at 19, while construction was at -9.

Zollner said it remained a very challenging time to run a business, and the “uncertainty of the outlook will itself likely see some hiring and investment decisions put on ice until the outlook becomes clearer”.

“Overall, the inflation news in the survey for the RBNZ was about as benign as they could reasonably hope. It’s early days of course, but constrained wage-setting intentions and steady pricing intentions provide a small degree of reassurance in the face of rising cost and inflation expectation.”

Last week, NZIER's Quarterly Survey of Business Opinion for the March quarter showed just a net 1% of firms expecting an improvement in economic conditions in the coming months, down from a net 39% in the December quarter.

The building sector was most pessimistic given its exposure to global supply chain disruption and transport costs. Leung described the “perfect storm for the building sector” due to continued weak construction demand limiting ability to pass on high costs by raising prices.

NZIER said expectations for interest rates turned around, with firms expecting higher interest rates in a year’s time.

ASB senior economist Jane Turner said pricing intentions lifted from net 25 in the December quarter to a net 43 in the March quarter, consistent with ASB's expectations for annual Consumers Price Index inflation to increase to around 4.5% to 5%.

Also last week, Finance Minister Nicola Willis released new scenarios from Treasury that forecast New Zealand's worst case scenario of economic impact from the Middle East conflict had inflation at 7.4%.

| 2026 | 2027 | 2028 | |

| Annual inflation (% June quarter) | |||

| Base | 2.7 | 2.3 | 2.2 |

| Scenario 1 (US$110 oil) | 3.9 | 1.5 | 2.1 |

| Scenario 2 (US$135 oil) | 5.2 | 1.8 | 1.4 |

| Scenario 3 (US$180 oil) | 7.4 | 2.1 | 1.2 |

| Real GDP growth (annual % change, June quarter) | |||

| Base | 2.3 | 3.3 | 2.7 |

| Scenario 1 (US$110 oil) | 2.0 | 3.4 | 3.0 |

| Scenario 2 (US$135 oil) | 1.5 | 2.6 | 3.7 |

| Scenario 3 (US$180 oil) | 0.8 | 1.7 | 4.4 |

| Unemployment rate (%, June quarter) | |||

| Base | 5.3 | 4.7 | 4.4 |

| Scenario 1 (US$110 oil) | 5.3 | 4.7 | 4.3 |

| Scenario 2 (US$135 oil) | 5.4 | 5.5 | 4.7 |

| Scenario 3 (US$180 oil) | 5.7 | 6.6 | 5.4 |

3 Comments

Remember banks polish turds

some hiring and investment decisions

seeing firing decisions....... SME up to larger corps...

The dominoes continue to be stacked , meanwhile everyone watches and waits.

Reminds me of the classic Australian movie, "The Castle" (with Michael Caton and Eric Bana"

"Must be Dreaming"

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.