I've talked before about how one of the frustrations of the Budget Lock-up is that detailed commentary on any tax measures is never made available during the Lock-up. A Treasury official told me during this year's lock-up this is the protocol because the legislation has not been introduced into Parliament. This is one of those arcane points of order which may make Parliamentary sense but is a bit of a frustration. Because as we all know, the devil is in the detail.

It turned out that there were quite a few devils in it after the Budget Lock-up ended and the relevant tax bills and other initiatives were released. It's quite interesting to compare what we saw during the Lock-up in terms of the announcements or the media release of the Revenue Minister, Minister Simon Watts, with what actually emerged after 2:00pm on the day.

Donations tax credit change

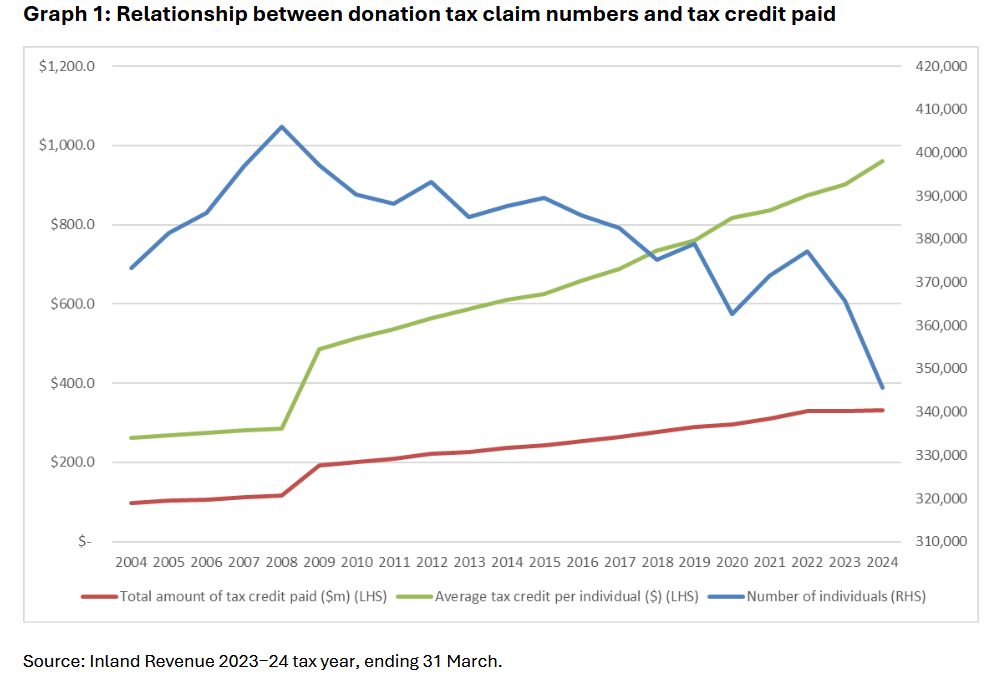

The Budget announced a maximum donation cap of $100,000 per person per tax year as a means of managing “expenditure control”. This was a surprise but makes sense when you look at the pattern of what National finance ministers have done in past budgets. Bill English and Steven Joyce were always looking for opportunities to remove or limit tax concession to balance the books. The biggest single example of this approach was in 2012 when employer contributions to KiwiSaver schemes became subject to Employer Contribution Superannuation Tax. That's now worth probably close to $2 billion a year. In hindsight, it's fairly obvious changes to the donations tax credit would perfectly fit with that pattern.

It's interesting to look at the Regulatory Impact Statement (RIS) that accompanied the announcement. What emerged was a reminder that the removal of the cap on donations only happened in 2008. So, the present position is relatively new and has only been around for 18 years.

“…no case for a fundamental review”

The proposal raises $19 million a year when it's fully implemented starting from 1st April 2027. As I told 1News, I see the move as nothing more than kicking over the stones to find some extra money. As the RIS noted Inland Revenue had not carried out a comprehensive review of donation tax concessions and had not compared the merits of using the tax system to support philanthropy versus direct government funding such as grants. The RIS also noted that Inland Revenue’s “2023−24 stewardship review found that there was no case for a fundamental review of the donation tax credit and that it was largely fit for purpose.”

Instead, Inland Revenue considered the donation tax credit from an “integrity and expenditure control perspective” while balancing the need to support the sector.

Improving expenditure discipline

According to Inland Revenue, expenditure on the donation tax credit was growing at an average of 2.6% per annum, yet at the same time the number of individuals claiming credits was declining. According to the RIS “Reintroducing a lower maximum entitlement threshold would improve expenditure discipline.”

Three options had been considered; firstly, maintaining the status quo. Secondly lowering the credit rate to 25%, but with the cap remaining at taxable income. (Remember, you can never give more than your taxable income for a year). The third option which is what was adopted, was lowering the maximum donation amount. Interestingly three further options were considered here. The one that was introduced, $100,000, but they also looked at lowering it to $15,000 or $4,500.

Charities not unreasonably pointed out the change could mean less money for donors. But the information sheet subsequently published said that the change would probably affect 350 donor entitlements, or 0.1% of donors. In other words, a very targeted and measured approach.

Trust income allocations to tax exempt beneficiaries

As I said in my Budget lock-up briefing there were some good measures in relation to not-for-profits regarding increasing the threshold for reporting and income and removing the risk of members' subscriptions being taxed.

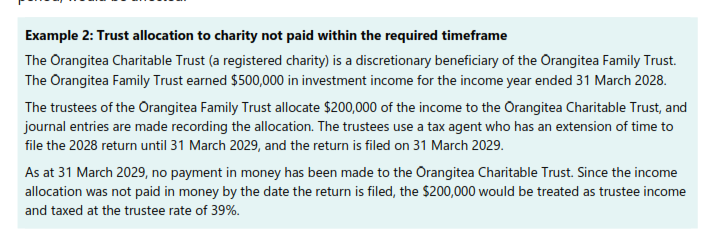

There was also an interesting change regarding trust income allocations to tax exempt beneficiaries. Now this is an adjunct to charitable donations and charity trusts as private trusts frequently have charities as beneficiaries to which they make donations which represent a deduction from trustee income.

The proposal is that private trusts which allocate beneficiary income to tax exempt beneficiaries will be required to pay the beneficiaries in money within a specified period in order for it to be tax exempt. If it's not paid within that time, it will be taxed at the trustee rate as the following example illustrates:

This change is meant to counter a potential integrity risk when the beneficiary is tax exempt because the trust’s income receives a tax exemption despite not actually being paid to the charity and made available for charitable purposes.

This only applies to private trusts that allocate income to tax exempt beneficiaries. Apparently, there are 400 trusts that allocate income to tax exempt beneficiaries each year which surprised me. We've got over 200,000 trusts registered with the Inland Revenue and only 400 or so making use of this mechanic seems surprisingly small.

One other quirk is this change will apply from the start of the 2028-2029 income year. By contrast most of the other Budget measures announced will either have an immediate effect, from the start of the current 2026-2027 tax year, or from 1st April 2027 and the start of the next tax year.

Fringe benefit tax changes

There was also good news with fringe benefit tax changes. Again, this is legislation that will be published later this year, but it follows up from previous Inland Revenue consultation on fringe benefit tax.

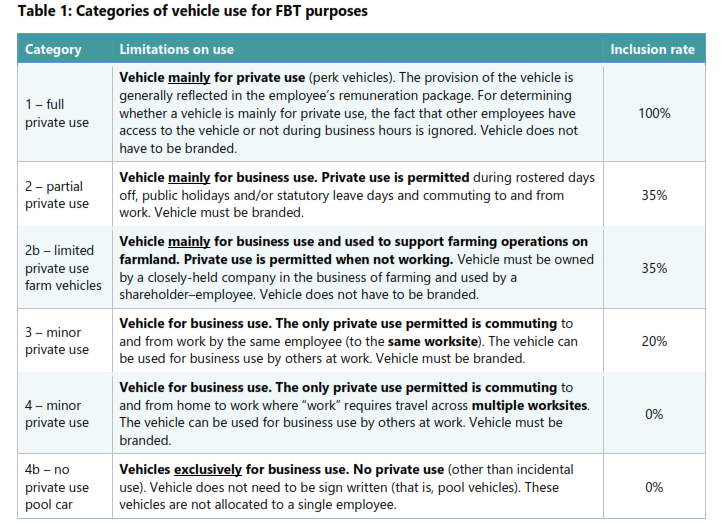

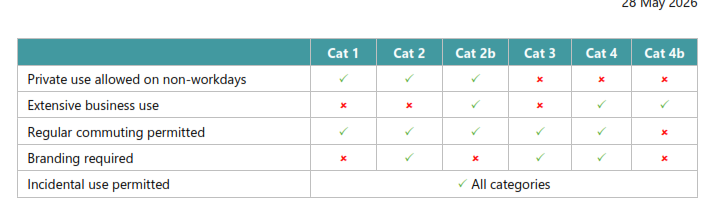

The main proposal is basically to simplify FBT for motor vehicles by implementing a “category approach.” Instead of counting the days in which a vehicle is available for employee use, the proposal would remove that entirely and instead require employers to choose a category based on the private use of the vehicle and use that rate when calculating their FBT viability.

There will be new rates for calculating the value of a vehicle for FBT purposes. Presently, the standard default rate is 20% annually or 5% quarterly. That will increase to 22.8% annually or 5.7% quarterly. For hybrid vehicles, it will be 19.6% annually or 4.9% quarterly, and an electric vehicle will be17% annually or 4.25% quarterly. So that would give more fuel-efficient vehicles a slight FBT advantage.

The idea behind this is to reduce compliance costs and hopefully also lower the FBT costs for some employers. It’s a good move in my view and will be in force from 1st April next year.

Foreign investment fund changes

Moving on, there were a couple of positive changes in the foreign investment fund (FIF) rules. Firstly, the cost threshold below which the FIF rules do not automatically apply was doubled to $100,000, the first increase since 2000. Taxpayers can still use the FIF regime even if the cost of their FIFs is below the threshold. Remember that dividends must still be returned if the FIF regime does not apply.

The other, somewhat unexpected, change allows all taxpayers to adopt the FIF Revenue Account Method (RAM) for unlisted securities. Previously, only new residents who arrived after 1 April 2024 could use the RAM. Furthermore, all New Zealand residents subject to double tax because of citizenship or the right to work in another country may also now use RAM for their listed shares, regardless of when they became tax resident. This will mainly apply to migrants from the United States.

There are also changes regarding the attributable FIF income method, which is beneficial for any shareholders who used to hold 10% or more of a foreign company. The rules regarding eligibility for the 10-year FIF exemption in the case of corporate migration (for example to the United States as part of a capital raise) will be clarified.

What’s particularly helpful about these changes is that they are effective as of 1st April 2026, i.e. they'll have an impact this tax year. We’ll see more detail when this year’s tax bill is released in August/September.

Financial arrangements regime proposals

There are changes to the financial arrangements regime aimed at migrants. The proposal is to allow some taxpayers to reduce their exposure for unrealised exchange gains and losses by allowing them to calculate their income in a foreign currency instead of in New Zealand dollars. There will be a new calculation method for financial arrangements acquired for the purposes of meeting the Active Investor Plus visa requirements.

These changes have been made because the financial arrangements regime has proved problematic for migrants in a number of ways. Although helpful, I think the changes highlight that the financial arrangements regime is well overdue for a complete review – the last was carried out in 1998.

Banks in the firing line

A big surprise in the Budget was the introduction of a prudential levy on the finance sector which will be administered by the Reserve Bank. This is a tax increase in all but name. The interesting thing is, although it's supposed to be a cost recovery mechanism, the accompanying media release commented “The levy will be paid to the Reserve Bank, with the revenue returned to the Government through an increased dividend.” This seems more than just a cost recovery exercise.

There was also a potentially significant thin capitalisation proposal aimed at the banks. The thin capitalisations rules apply to overseas controlled companies under which interest deductions are only allowable in full if their debt/asset ratio is 60% or less. If the debt to asset ratio exceeds 60%, then interest deductions get limited.

Now in the case of banking groups, the debt/asset threshold is set much lower. Since 2012, it has been 6% for foreign-owned groups. The Government proposes to increase this threshold to 12% for groups that include a “domestically systematically important bank”, which I'd say would be the big four Australian-owned banks, and 11% for all other banking groups.

The idea is to protect New Zealand's tax base by limiting the amount of cross-border related party debt a banking group can take on for tax purposes and therefore limiting interest deductions in New Zealand. This is a fairly significant change for the banks expected to raise $45.2 million over the four year forecast period and together with the prudential levy won't be welcomed by the banks. The levy and thin capitalisation changes are effective from 1st April next year. It will be interesting to see the pushback on these changes.

Budget tax bill passes

As noted, the detailed legislation for these various changes will be included in the annual tax bill due in August/September. In the meantime, the tax bill including the cap on individual donations introduced with the Budget has now been passed.

The bill also included the measure deeming a dividend to arise on any outstanding amount owed by a shareholder to a company six months after the company is removed from the Companies Register. This applies from 4th December 2025 the date Inland Revenue published its controversial paper on the taxation of company loans to shareholders. The accompanying RIS noted that in the case of companies going to liquidation, the average outstanding loan balance was around $213,000 per company. The measure is expected to raise $146 million (net of impairments) over the four year forecast period.

Double tax agreement with the United Kingdom updated

Finally, just a quick note that the double tax agreement with the United Kingdom has been updated and a new one was signed in at the start of the month week. This will replace the existing double tax agreement which entered into force in 1984.

The new agreement is designed to “better support cross-border trade and investment between the two countries and includes key anti-abuse provisions developed by the OECD to prevent base erosion and profit shifting”. It will come into force shortly once the relevant Order in Council is passed. Expect to see more updated agreements as we have some very old double tax agreements in place. The United States is another one dating from the 1980s.

And on that note, that’s all for this week I’m Terry Baucher and thank you for listening. Please send me your feedback and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.