The Government has slashed, by up to half, its estimate of what the cost to businesses of complying with the Anti-Money Laundering and Countering Financing of Terrorism Amendment Bill will be.

Justice Minister Amy Adams revealed this staggering reduction when announcing late on Monday the introduction of the Bill to Parliament. The Bill is known as stage two of the AML/CFT Act, of which stage one took effect in 2013.

So why the reduction? Because fewer businesses than previously thought will have to comply, and some companies will work together in groups to meet their obligations.

“Over the past several months, we have worked with affected sectors to better understand how the changes will impact their businesses and refined options to help them meet their obligations. This has significantly reduced the predicted compliance costs – the initial estimate of up to $1.6 billion over 10 years has been lowered to between $800 million and $1.1 billion," Adams said.

The Bill extends the existing AML/CFT Act to lawyers, conveyancers, accountants, real estate agents, and sports and racing betting. Businesses dealing in some high value goods, including motor vehicles, jewellery and art, will also have obligations under the Act when they accept or make large cash transactions.

In December Adams said compliance costs stemming from extending AML laws could ultimately be passed on to "mums and dads," costing $1.6 billion over 10 years. So how has the Government managed to effectively halve this estimate, which came from an EY report done for the Ministry of Justice, in four months?

"The main reason for the difference is because fewer businesses than first thought will have to comply with the Act. For example, many dealers in expensive goods will probably not accept large cash transactions, and it’s likely more businesses will use provisions that help them to reduce their compliance costs, such as setting up designated business groups that allow companies to work with others to meet their AML/CFT obligations," the Ministry of Justice says.

Adams, via a spokeswoman, told interest.co.nz the Government had worked with businesses to minimise compliance costs and develop options to reduce compliance requirements.

"Business compliance costs were estimated by a survey of industry participants, interviews with Phase I supervisors [the Department of Internal Affairs, the Financial Markets Authority and the Reserve Bank], and interviews with the potential phase two sectors. In addition, the Government held workshops across the country with experts from the different sectors, which helped refine our figures so that they better reflect how businesses will manage their costs," Adams said.

Fewer law firms, accounting firms and real estate agents to be supervised

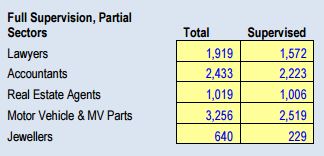

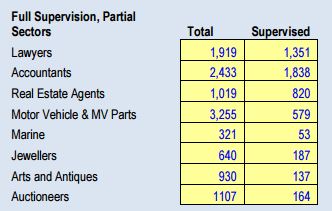

Figures included in the Government's draft cost-benefit analysis released in December, compared with figures in the cost-benefit analysis made available on Monday (see charts below), show some major differences. These include that fewer law firms, accounting firms and real estate agents will be supervised for AML/CFT Act compliance than initially proposed.

Chart from December report

Chart from March report

The initial cost-benefit analysis incorporated high value dealers consisting of full supervision on motor vehicle dealers and jewellers only. In the updated analysis high value dealers consists of motor vehicle dealers, boat traders, jewellers, art, auctioneers and second hand dealers with "light" compliance and a $15,000 cash threshold for transactions. That $15,000 threshold is up from $10,000 previously. The updated cost-benefit analysis estimates 0.27% of GDP will be "restrained" in the regulated sectors in any given year, down from 0.33%.

Expert non-plussed

Ron Pol, a former lawyer completing a PhD in anti-money laundering and thus an AML expert, is underwhelmed by the reduction in businesses who will be caught in the net, and their compliance costs.

"Adjusting the number of businesses covered and massaging the cost-benefit numbers won’t materially affect the policy effectiveness equation," Pol told interest.co.nz.

"The new bill will help position New Zealand to meet its international obligations. Box ticked. Police will also no doubt welcome the Bill, as another small addition to their intelligence capabilities. But the international and New Zealand evidence suggests that it is unlikely that the incremental approach of adding more reporting entities will have a significant or demonstrable impact on the detection, prosecution and prevention of serious crime," Pol said.

Meanwhile, Adams says the Bill, once passed, could disrupt up to $1.7 billion in fraud and drug crime over the next decade. Government estimates also suggest it may prevent up to $5 billion in broader criminal activity and reduce about $800 million in social harm related to illegal drugs trade.

Staggered compliance timeframes for newbies

The Department of Internal Affairs will supervise all of the phase two entities for compliance with the AML/CFT Act. The newcomers will have staggered timeframes from when they'll have to comply. Lawyers and conveyancers will have to comply by July 1, 2018, accountants by October 1, 2018, real estate agents by January 1, 2019, and high volume goods dealers and the NZ Racing Board, which administers sports and racing betting, by August 1, 2019. See more on the Bill here, which the Government wants to have passed by mid-year.

These so-called phase two entities will be required to comply with the AML/CFT regime when they offer specific services. Their compliance obligations will include appointing an AML/CFT compliance officer, undertaking an initial risk assessment of their business and customers, preparing a written AML/CFT programme setting out how they will comply, doing customer due diligence, filing suspicious activity reports on any suspicious activity they see, preparing an annual report on their AML/CFT programme, and having their AML/CFT programme audited biannually by an independent auditor.

Since 2013 banks, insurance companies, investment advisers, money remitters and casinos have had to comply with the AML/CFT Act. The Bill also makes a series of changes affecting these "phase one entities" including expanding suspicious transaction reports. Now, these entities have to report suspicious information when it is directly related to a transaction. However, it's proposed that all reporting entities will have to report any suspicious activity, even when a transaction has not taken place.

*A version of this article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

12 Comments

The elite spongers have had a 10 year cost free holiday

Ten years to get this legislation off the ground. The Fonseca Files forced the Government's Hand - not too suddenly - one feels the legislation would NOT have seen the light of day had it not been for Fonseka - anyway - we finally get it

The affected parties have known it was coming for at least 5 years - the Fonseca event merely focused the governments attention on the lack of progress - then the squeals of the lobbyists of the affected parties rung out - oh dear the cost

Now, within 2 months we have government announcing refinements + carve outs on who and when will report

Such alacrity

Funny the Govt doesn't mention the cost to NZ home buyers (and our private debt profile) in terms of property price inflation caused by their failure to implement. Putting a number on that would show just how crippling and detrimental this hot money has been.

There's also some initial research overseas that suggests that price inflation caused by criminal investment into real estate is higher than with legitimate funds, and concentrated in cities. Also, aside from a few legal and real estate fees, all the benefits flow directly to those crime groups, supporting and extending their criminal enterprises (ironically, the ones we spend lots of other taxpayer money trying to stop). When government ministers (here and elsewhere) see "inward investment" they often see it without these important distinctions. But, as you suggest Kate, the impact of illicit investment is not the same as the usual positive income multiplier benefits associated with legitimate investment.

I've been seeing meth profits going into real estate for 20+ years. Started out small and domestic, then snowballed.

This recent study of wastewater to detect the prevalence of illicit drug use suggests the Auckland meth market is around $146 million pa. Yeah, that's a lotta houses - and that's only Auckland's meth market;

https://publicaddress.net/hardnews/what-the-wastewater-tells-us-about-d…

Meth's been cooked and used in NZ since the mid-to-late 70s, but for the first 20 years or so it was a real niche drug and hadn't gone mainstream.

Thanks Kate, that's a great piece of research

Yep. People often think its "from overseas", but lots of it is locally generated crime proceeds, sourced directly from locally-caused harm. The research shows just what you say Kakapo (and how it's done), from local meth dealers and increasingly international drugs traffickers, plus some fraud etc, all causing harm in the domestic economy and society.

Real estate is one of the best ways (simple and least likely to be caught) for keeping criminal profits. Smaller scale crims have another near-perfect method before they step up to real estate, and the biggest criminal enterprises have another method when they get past real estate. (Although the allure of luxury real estate or a few score houses from time to time remains part of any balanced diversification strategy even at the top-end of protecting and growing criminal enterprises).

The government has used huge compliance cost as a ploy to delay this for years, tranche 2 was to be launched in 2014-15. There have been starts and stops, they tried to use every excuse in the book ie cost, reporting entities not prepared, law is too complex, regulators have no capacity etc. They got called out when NZ got splashed in the international media for the ease with which people can use trust and other innovative methods to invest and hide laundered money in NZ. They also know there is an upcoming mutual evaluation in 2020, and if Australia's results are anything to go by NZ will get slammed on the large sums that were/are laundered through property and no action taken by the government to stop it. It's reputation is on the line so they are making the right sounds to show some activity on that front, not surprised.

Yep, my working hypothesis is that doing enough to get a FATF tick is the main driver.

I've consistently spoken of the prospect of better outcomes (and, incidentally, likely cheaper and just as FATF-compliant). Into a deafening silence.

Particularly curious lately, because the new PM and new Police Minister (for the Minister of Justice I have less evidence, so tend to assume positively in the meantime) have a strong understanding of modern 'outcomes' over 'outputs' in government (although most agencies lag, and often just relabel outputs as outcomes), so might assume they could help lead agencies towards better outcomes for NZ, and boost crime prevention policy effectiveness.

Assuming their genuine best intent (as I think one must, unless proven otherwise), the most obvious reason may be as prosaic as it's perceived a difficult area, or not a high enough priority (it is an election year) and they're on the easier path of following advice rather than leading the direction for officials.

And officials and advisers have clearly been hugely industrious, but there's no (external) evidence they've asked the hard questions or looked outside the safety of the AML-industry-socialised box.

This working hypothesis accords with yours I think GS, but I for one would be delighted for it to be proved wrong.

You are a bit too kind, Ron :-). If (as you think) Bill and Amy are aware of the distinction between "outputs" and "outcomes" - my suspicion would be that they are executing a deliberate strategy simply to produce an output - for the very specific reason that it will not achieve the outcome intended.

Indeed, my assumption (based on reported instances of Bill English exhorting an outcomes-focus in government, in terms that match recognised criteria, and several ministers reportedly joining the conversation) might well be proved wrong too, by the actions of said politicians/officials :-)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.