Xero’s shock announcement that it’s jumping ship from the NZX to the ASX has put the New Zealand sharemarket under the spotlight.

For Milford Asset Management executive director, Brian Gaynor, the move shows the NZX has “major problems” as it is struggling to attract new listings.

“Two of its biggest problems are the huge amount of off-market trading and the dominance of one broker,” he says.

Harbour Asset Management managing director, Andrew Bascand, says he will be asking questions of the NZX. Why can’t it keep New Zealand’s premier tech company listed here? Is it a cost or regulation thing?

Yet speaking to interest.co.nz in a Double Shot Interview, JBWere strategist Bernard Doyle has a different view. He believes that yes, it’s a shame to lose Xero. But no, it will not be a “terminal hit” to the market. Nor is it symptom of any structural problems.

Doyle is not known for wearing rose-tinted glasses. He in 2010 challenged the Government to decide whether it even wanted an equity market, as investors were telling him it was no longer big, diverse or liquid enough to keep them investing domestically.

With the NZX’s market capitalisation only equivalent to 29% of gross domestic product (GDP) - a similar proportion to that of Greece at the time - he said the sharemarket was "ceasing to be relevant to the economy".

Seven years on, with the NZX’s market cap worth 48% of GDP, Doyle is confident it’s on the right track.

The only real problem is that it’s still a struggle for smaller companies to gain traction on the NZX.

What’s changed since 2010?

Doyle says a lot has changed for the better since 2010, when global markets were subdued in the wake of the 2008 global financial crisis (GFC).

The growth of KiwiSaver has seen billions of dollars of new equity supply and demand. The Crown has become a larger investor through the New Zealand Superannuation Fund and ACC, and it has floated Mighty River Power, Meridian Energy and Genesis Energy - “significant listings at the big end of town”.

While back in 2010 “it looked like we were either going to go down the pike hole, or things had to change,” Doyle says the situation’s improved a lot.

“If I look at what central government can and has done to make our sharemarket a place where it can thrive and play its role in the economy, most of the big levers I think have been pulled.”

The NZX’s market cap to GDP is now the highest it’s been since 2000.

Has the market grown organically or is it just over-valued?

Asked about the extent to which he believes growth in the sharemarket can be attributed to its strength versus it simply being overvalued, Doyle leans more towards the former.

“If you were being harsh, the market might be 20% overvalued.”

However he says the proliferation of KiwiSaver, investment through the Super Fund and ACC and the energy company floats, have done the heavy lifting to move market cap to GDP from the 20%s to the 40%s.

“Of course, we’ve [also] had five years of very good returns. This has been one of our best ever, if not our best ever, bull market that’s not ended in a 80s type bubble. We’ve actually had very strong steady returns over a long period of time. So we’ll probably give some of that back at some point.”

How concerning is it that the market’s over-valued?

Asked about how concerned he is that the New Zealand sharemarket is overvalued by around 20%, Doyle says: “I think there are risks. We’ve had a view this year that investors need to be careful about their allocation to this market. But that’s a one to three year… tactical view.

“That’s the beauty of shares, right. They go through periods where they’re doing really well and then you get a little bit over-heated, and we’re due for a flat patch here.”

Yet Doyle doesn’t see the market slumping back to where it was 10 years ago.

“I certainly don’t think we’re in that camp.”

He says KiwiSaver’s not going to unravel and the energy companies aren’t going to be delisted.

He notes we’ve had a period of strong population-driven growth and that could “bite us a little bit” over the next few years, “but that’s not big enough to take us back to square one”.

If the market’s richly priced, why is Xero’s leaving?

Doyle doesn’t understand Xero’s move.

He says a shift would usually be prompted by a company’s value not being recognised in a certain market, or it struggling to get offshore investor interest.

Yet Xero’s enterprise value to sales is up there with its peers in the sector.

“And so, [it’s] hard to say on the basis of valuation that there was a problem to fix there.”

As for the issue of analyst coverage, Doyle says it’s well understood that the New Zealand market is relatively small with fewer analysts. But any struggles Xero may have had to populate its register with US tech investors, would’ve shown up.

“From the outside looking in, there didn’t seem to be an issue to fix from being listed here.”

Moving to the ASX, Doyle says “you’ve got more depth, but you’ve also got more distractions for investors… it’s a very competitive market. There are more analysts, but they’re spread thin.”

He doesn’t accept the argument that inferior research by New Zealand analysts prevents investment into the local market.

What more can the NZX do?

Doyle is pleased the NZX’s CEO, Mark Peterson, from September “turned over every rock” to try to enable Xero to be included in the S&P/ASX200 index, while maintaining a listing on the NZX.

Yet ultimately he doesn’t believe there was much Peterson could’ve done.

“All you’re looking for as an investor… is you want to talk to good analysts, you want a clear and transparent set of rules, and a regulator that doesn’t do about turns.”

He recognises the market is vulnerable to big players leaving, but says the tougher issue is actually growing smaller companies.

“The NZX has tried different techniques to nurture smaller companies into the market. That’s one area where we haven’t fixed it. If there was an easy answer, it would’ve been found by now.”

Doyle notes that while it’s necessary, the regulation that’s followed the GFC and tech bubble has made research more costly.

“For smaller companies it’s harder for them to get the turnover to justify the brokerage that makes research coverage economic. The NZX has looked at things around helping with independent research coverage.”

What about factors out of the NZX’s control?

Beyond this, Doyle recognises there are factors out of the NZX’s control - like a lack of retail investors willing to take higher risks.

“In the wealth world… you have to be really careful about what you’re recommending in portfolios. Because it’s wealth and it’s also a stage of life thing about where New Zealand’s at generationally. But also the regulatory environment compels you to be very careful about the sort of companies you’re thinking about for portfolios.”

Doyle says it’s “nigh on impossible” for there to be a repeat of the 80s crash because “back in day you could list anything and it didn’t have to have any fundamentals to attract capital”.

While more oversight is good, it can be an impediment for smaller companies trying to gain scale.

Furthermore, Doyle says: “A lot of this stuff is cyclical. Anyone looking at this, including the NZX, needs to be careful about trying to solve a problem that is ultimately something that will go away as the cycle changes.”

He notes that like in New Zealand, the US is also experiencing a shortage of new listings to the market, with last year being its weakest in almost a decade.

“One of the common attributed causes to that is that private equity has grown so exponentially… that it’s kind of cannibalised a little bit of the listed sector’s ability to do what it has traditionally done.

“I wouldn’t mind assuming that over five or 10 years, private equity’s probably grown too fast…

“As a global trend, you could see that retrench a little bit over the next three to five years... As it ebbs, it will create room for the listed sector to probably regain a bit of its lost ground.”

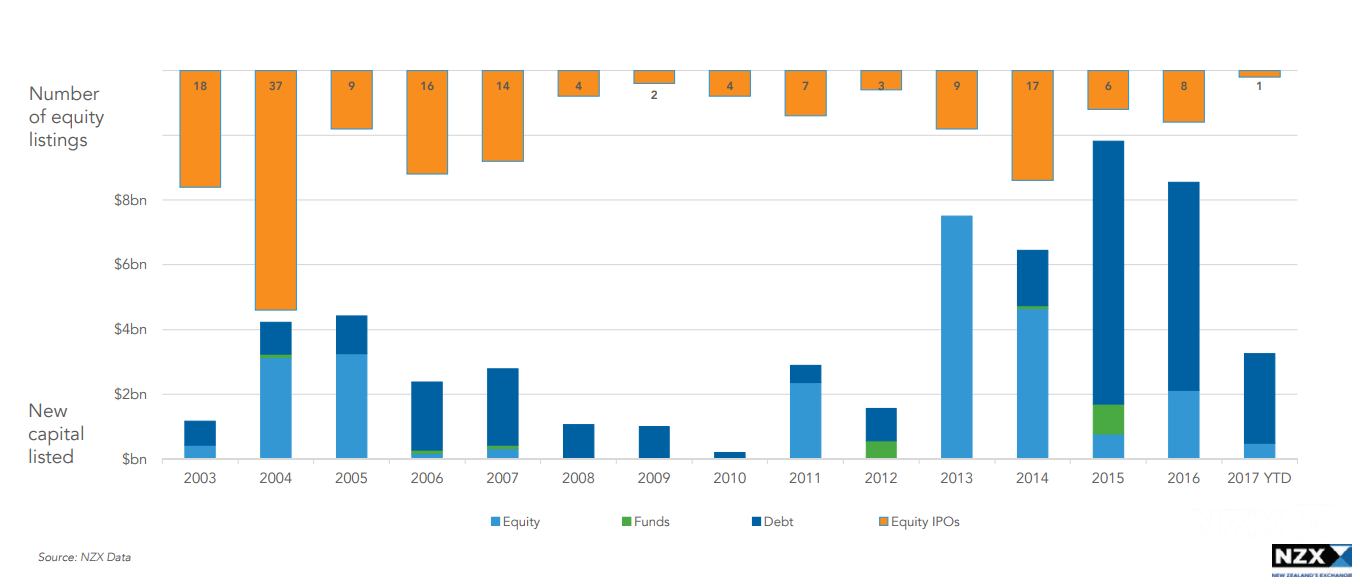

Here are the latest figures from the NZX:

Are tax distortions between asset classes an impediment to equity market growth?

Doyle says the advantages of investing in the property market used to be the biggest impediment to attracting investors to the equity market.

“It was all property, property, property.”

While that mentality is still there, Doyle believes the government has pulled all the big levers to nurture the equity market, as explained above.

He says tax doesn’t come up as an issue when he talks to clients about building portfolios.

However he recognises: “I could be being a bit complacent here, as we’ve had a lovely run in the share market here and globally. So people don’t tend to focus on tax so much when they’re getting nice capital gains.”

Doyle also accepts that when someone approaches a firm like JBWere, they’ve probably already decided they’d like to invest in the equity market, so he wouldn’t necessarily encounter those put off it by the tax disadvantages.

Nonetheless, he says: “People have become more sophisticated, more aware of diversification...

“We’ve had enough rattles [in the property market] so certainly larger investors are conscious that just having a whole lot of rental properties, or a commercial building as your sole savings vehicle is not prudent.”

While he believes there’s room for improvement with respect to tax distortions between asset classes, Doyle says: “I don’t think it’s necessarily the thing that we’ll sit here in five years’ time and say, that’s what was going to take us from [an NZX market cap of] 45% of GDP to 55% or 60%.

“I think actually the market here is on the right path in terms of some of the big structural changes that have occurred.

“I’d be disappointed if we didn’t continue to improve - not necessarily cyclically (because we’re probably due for a little bit of a quiet patch) - but over five to 10 years I think we’re on the right track.”

12 Comments

"Doyle doesn’t understand Xero’s move."

Obvious, isn't it ?!

Consolidate in a bigger market and flog the whole lot off ( Maybe MYOB might do the right thing and try to buy out the competition?)

'Maybe MYOB might do the right thing and try to buy out the competition?'

hopeful thoughts of a Xero investor !

Dont think MYOB has that sort of folding stuff...Xero has over 1.2 million users now..growing daily. As an Xero investor quite happy to hold..company is extremely well run and innovative. Maybe Rod just got sick of the nay Sayers ...its just a bean counter software ...experts?

"Nothing to see here, move along please". Is this guy for real? He is an institutional chap who appears to have no clue about what's going on. He deals in millions and has no understanding of the motivations of one of our major businesses nor of the impact of the internet on retail investors (obviously not important in his world).

Personally I tend to buy on the ASX because it's cheaper. The point about investing in smaller companies is to not to put much in each one. It's called diversification. So I put $1000 into Xero. Commision AUD $6 using an online broker. If I had bought in NZ the commission would have been NZD $29.50 using an online broker. Commissions are paid twice, so one lot to buy and one lot to sell. $29.50 x 2 = $59 or 5.9% on a $1000 investment. AUD $6 x 2 = AUD $12, or about NZD $13.50, 1.35% on a $1000 investment. No contest, the Aussies win hands down.

Get your finger out NZX. Why have you lost a major customer and why are commisions so prohibitively high?

I feel a rant developing for another time...

Which online broker do you use to trade on the ASX?

Interactive Brokers. https://www.interactivebrokers.com/en/home.php

Their website is pretty complex and it's not for the faint hearted. It has endless options to grapple with. So far I have probably got the hang of the tiny fraction of functions I need to do simple stuff.

The strangest thing is it costs $1 per transaction on the US exchanges. That is the NZX is 29.5 times more expensive for me to invest in smaller companies. Trouble is I don't want to buy US businesses...

Let me know if you know somewhere cheaper for the NZX.

I use ANZ share trading (formerly eTrafde) in Australia and fees are not cheap (not an active trader so I don't know but I thought it was around $20 to execute a transaction). Furthermore, regular payments into FNZ50 requires zero fees as a savings instrument.

I believe ASB have reduced some fees on smaller trades which is the right move, but still not cheap

The boss reducing his holding and getting $95m.

Questions need to be asked.

Why? Pretty normal common sense move to rebalance a portfolio after the huge growth in the value of his Xero shares.

No financial expert but if i have shares in a company and see a major shareholder selling down i wonder why.

You have answered the question for me,are there other reasons ,i don't know.

He still has 17.7 million shares after 3 million are sold. Why would he keep over $600m in shares?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.