This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

The commentariat’s announcement that the New Zealand economy was in an ‘official recession’ by March 2023 – two quarters of output/GDP decline – was greeted with white faces by officials in the Reserve Bank and Treasury. There was queuing for the lavatories; some of the forecasters handed in their resignations to the Minister of Finance; one or two tested the windows to see whether they could jump out.

OF COURSE NOT. The officials would have been puzzled by the term ‘official recession’, since neither institution nor Statistics New Zealand (SNZ) use it. Later the commentariat changed the term to ‘technical recession’; I doubt any serious economist has the foggiest idea what a ‘non-technical recession’ is.

Instead, like me, the officials would have turned to their forecasts. The Treasury quarterly track in their Budget Economic and Fiscal Update (BEFU) forecast had a March 2023 increase of 0.3 percent instead of the 0.1 percent fall, so the economy appears to be tracking lower than they expected.

However, there is measurement error. One source of the error is that numbers inevitably bump around in a small economy (not to mention the complications from Easter being a moveable feast); another is that in order to publish the data early enough some, of the data input are estimates which will be updated when better figures come in. Based on the evidence of recent revisions, the March quarter could turn out to be mildly positive.

Unquestionably the economy is neither booming nor troughing; the cautious judgement – unlikely to be headlined by the media – is that the economy is flat or stagnating. If performance is measured by per capita output, the fall is somewhat larger since population has increased by about 1 percent in the two quarters.

Perhaps more important about the SNZ release was the contracting industries. Because of quarterly measurement and volatility, I looked at the year-on-year change. Negative growth is largely confined to agriculture, forestry, and fishing, mining and manufacturing – the tradeable sectors. That is not really good news because, some services such as tourism (which is not doing very well either) aside , they are the main contributors to foreign exchange earning and saving (import substitution).

I imagine there was a vigorous discussion within the Reserve Bank and Treasury between those who thought the data indicated the economy was contracting faster than expected, those who thought it was contracting earlier than expected, and the wait-and see-faction (which I probably would have belonged to). Some of the discussion would have been about the extent to which the RBNZ’s measures were working – perhaps faster than expected.

There may well have been more discussion in informed quarters on the previous day’s SNZ release on the balance of payments. It reported that in the year ended 31 December 2022 the current account deficit of $34.4 billion (9.0 percent of GDP) compared to $24.2 billion in the year ended 31 March 2022. It is the biggest deficit for the 20 years that SNZ reported.

SNZ attributed the main components of the deficit to a $6.4 billion widening of the goods deficit and a $2.2 billion widening of the primary income deficit. The primary income deficit indicates that New Zealand investors earned less overseas than overseas investors earned from New Zealand.

The above has focused on sectoral flows. Combining them, last year we borrowed more than in any year for two decades. Our net international liabilities have been rising.

Back to the BEFU forecast. There are some complications in interpreting their figures, but my reading is that the current account deficit is bigger than Treasury was forecasting – more than one could explain by data problems.

That means that in various places in the economy, sectors and households are borrowing to sustain their expenditures. We do not have the comprehensive investment and savings account to identify exactly where. We know that some of the borrowing is in the public sector, but that is only a partial explanation. Some will be for productive investment, some for residential housing purchases, and probably there are households who are borrowing or running down their savings.

Part of the worry has to be that with the economy stagnant or depressed, one might expect the savings deficit to increase as the economy begins expanding again – perhaps in early 2024.

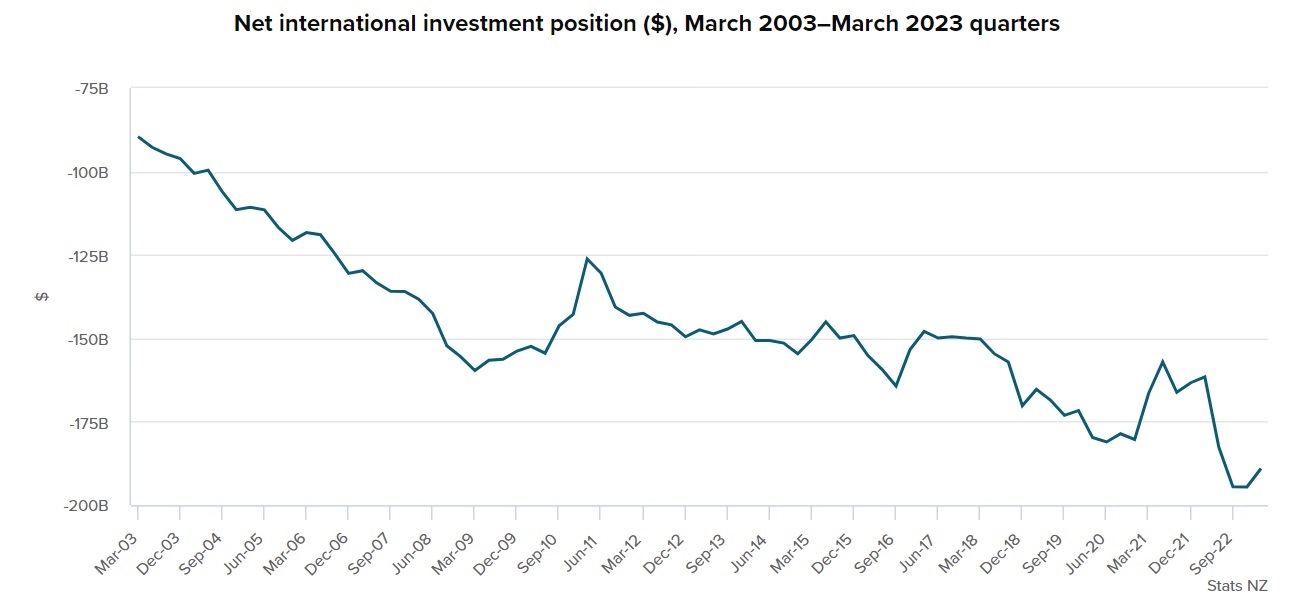

However, as I worked through the data I was struck by the SNZ graph which showed the net international investment position – how much we owe overseas (net). We owed $90b odd, in March 2003; as we borrowed more, the debt increased to $160b just before the Global Financial Crisis. After that shock the overseas debt stabilised and was $150b in March 2018. Since then, it has begun increasing again and is about $190b today. (There was some recovery in 2021. COVID?)

It is all very well saying that most of this debt is private and not a matter for public policy. We saw how in the GFC, the private debt of the commercial banks became a public concern. I have no doubt that at our next credit rating review, officials will be pressed by the credit rating agencies. The resulting rating guides the international investors who are lending to us. If the officials don’t have a satisfactory response, the interest rates at which we borrow internationally will be higher, including feeding through to those on residential mortgages.

One of the lessons from New Zealand’s economic history is that our big economic crises have usually been associated with our overseas debt. Of course, I may be wrong next time; the ostriches do not expect another major crisis here or globally. But it seems to me that the debt level issue is far more important than the commentariat wittering away about whether we are in a recession, be it ‘official’, ‘technical’ or just an old-fashioned downturn.

*Brian Easton, an independent scholar, is an economist, social statistician, public policy analyst and historian. He was the Listener economic columnist from 1978 to 2014. This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

8 Comments

I'm no economist but as a largely export driven economy, surely it is New Zealand's current account deficit that is the best marker on how we are situated. That stat is pretty depressing right now.

Brian also draws attention to our record of overseas debt and the numbers clearly show that that always balloons under Labour governments (2002 - 2008, 2018 - 2023).

"Brian also draws attention to our record of overseas debt". He's talking about private debt. Under Clark, the government's debt reduced. I recall Bill English [and Don Brash] commenting favourably on that on RNZ when the Key government entered office.

Undoubtedly private debt has been exacerbated by the right cartels (electricity, supermarkets and petrol) have in this country to price-gouge as they see fit, due to the holes in the Commerce Act (1986) which don't make it illegal to do so. For example, residents in NZ pay the highest prices in the OECD for electricity. THAT sort of thing should be illegal. Regulation is a dirty word in NZ, so politically unpalatable. Meanwhile NZ's social fabric continues to give way...

Recession worst of our worries? You've probably been brainwashed into believing that by the sheer weight of media coverage? But that reflects the extremely poor quality of coverage we get, ( or is it propaganda?).

Who's heard this story? It has more of an existential feel to it.

https://www.politico.com/news/2023/07/01/white-house-cautiously-opens-d…

Our foreign debt is all held in NZ Dollars and which were issued in NZ and we don't borrow in foreign currencies. We don't borrow to finance our spending, we borrow back our currency to balance the accounts of the banks who have to hold deposits equal to the money which they create. Foreign entities may also choose to hold our governments bonds denominated in NZ Dollars but they most certainly are not financing anything.

We pay our way in the world by the use of NZ Dollars and which are all created in this country either by the banks as credit or by the government as sovereign currency. The Bank of England tells us that banks are not intermediaries of loanable funds. https://www.bankofengland.co.uk/working-paper/2018/banks-are-not-interm…

Call me old fashioned, but I think if NZ exports $100b and imports $130b we have a problem that no amount of financial theory gymnastics will fend off for long.

Unless the foreign sector looses faith in our currency and no longer accepts it and there is no sign of that happening. Our current account deficit is a sign that our dollar is overvalued and should be allowed to decline in value. Our NIIP balance is not that bad anyway as the Treasury explains here.

https://www.treasury.govt.nz/publications/research-and-commentary/rangi…

So lower dollar brings more imported inflation. Good for exporters but bad for the rest of us. Can't see interest rates declining in such an environment but see what happens.

Those overseas liabilities (debt) are the direct result of the cumulative current account deficit. What we have is an economy out of balance....

Households have borrowed tens of billions of dollars of newly printed money from commercial banks at the same time as Govt has spent tens of billions of newly printed money into the economy. The beneficiaries of this money creation have bought thousands of Teslas (etc), and, as a country, we have paid 50% to 80% more for oil and fuel over the last couple of years.

The point we have now reached is fascinating. Govt is now spending about the same as it is taxing back, and households are paying off loans at about the same rate as they are taking them out. If this continues then the current account deficit will *have* to reduce unless people cash in all their savings to sustain the spending, and I doubt that.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.