Here's our summary of key economic events over the weekend that affect New Zealand with news US$100/bbl oil is settling in as the Persian Gulf conflict settles in to an attritional conflict with no end in sight.

And although he apparently sees no irony in it, US President Trump called for help from other countries to dig him out of the crisis he started by sending naval forces to keep the Strait of Hormuz "open and safe". But so far, no country has stepped forward with any commitment.

Elsewhere, there will be a lot going on in the week ahead. The big economic event will be the US Fed decision on Thursday. This is supposed to be Chairman Powell's second last meeting where he is the boss and no change is anticipated. But Trump has been losing the court fights over his campaign to oust Powell, and Congress won't progress Kevin Walsh's nomination, so who knows how that will all play out.

Central bank decisions will also come this week from Canada where no change is expected and none from any of Sweden, Switzerland, the ECB, Japan, China, or England. For all of them it is a wait-and-see situation. Russia review as well and may cut by -50 bps. Of course, locally the big one will be the RBA's cash rate target review tomorrow and market are now expecting a +25 bps hike.

For economic data all eyes will be on the New Zealand Q4-2025 GDP outcome, and probably more importantly, the Aussie labour market report for February. And there will be key releases from the US for PPI and industrial production, the Eurozone trade balance, and the Canadian inflation rate. Additionally, China will release its industrial production, retail sales, unemployment rate, housing prices, and fixed-asset investment, many of them later today.

Back in the US, it will be no surprise to learn that core PCE inflation rose at a +3.1% rate in January, its most since late 2023. And the rises in December and January were at more than a +4.5% annualised rate. Given subsequent events, it seems unlikely this rate will have eased since. The rising inflation threat will be the main reason the Fed won't cut.

It its second interim report, the US economy expanded an annualised +0.7% in Q4-2025, far less than the +1.4% advance estimate, and the weakest performance since a contraction in the first quarter of 2025. Downward revisions came for exports, consumer spending, government spending, and investment. Imports decreased less than previously thought. It is turning out economic expansion is far less now than at any time during the Biden presidency.

The January JOLTS report showed more openings than in the five-year-low December report, but these were still -6% lower than a year ago.

Meanwhile, the widely-watched University of Michigan sentiment survey fell as expected in its March edition, to a three-month low, but inflation expectations didn't fall as expected. The shifts were comprehensive across all income and age groups. War uncertainty and the rising fuel costs were the [obvious] triggers. Those petrol prices are up +18% now from a year ago, up +9% in a week. The darker mood is very obvious from two years ago (before Trump 2), with sentiment down -30%.

Meanwhile the Congressional Budget Office is sounding the alarm about where US federal debt is tracking. Page 3 of their February report shows the essential corruption - personal income taxes are up +10% (and you can be sure that does not relate to billionaire 'taxpayers'), corporate income taxes are down -33%. Even the 'tariff tax' collections are essentially taxes on Americans collected at the border. These are up +US$109 bln, about the same as the rise in personal income taxes. The result seems to be that US Treasury debt held by the public is currently 101% of nominal GDP and without changes will rise to 175% of GDP in 30 years.

In Canada, their labour market shrank in February and by an outsized -83,900 following a -25,000 decrease in January and sharply missing forecasts for a +10,000 gain. Job losses were concentrated in full-time positions which were down -108,400, so the report is grimmer than it first seems. It has been called a 'brutal' jobs report, and will undoubtedly end the Bank of Canada's hiking cycle.

India loan growth rose +14.5% in February from a year ago, maintaining its high rate of expansion (and almost three times their GDP growth).

New passenger vehicle sales in India hit a record high in February, up more than +10% from the same month a year ago, but to be fair, this overall market is nothing like China - or the US for that matter.

China new yuan loans rose +¥900 bln in February, just as was expected. But that gain was slightly less than the +¥1 tln in February 2025, and much less than the +¥1.5 tln in February 2024.

It won't be a surprise to know that the prices of most hard commodities are rising. But some ubiquitous ones like plastics (polyethylene +32%), steel (hot-rolled coil steel +13%), aluminium (+14%), and bitumen (+35%) have all jumped sharply in 2026. This won't be good for inflation control.

The UST 10yr yield is now just on 4.29%, up +1 bp from Saturday, up +18 bps for the week. The key 2-10 yield curve is holding at +55 bps. Their 1-5 curve is steeper still at +23 bps and the 3 mth-10yr curve is now at +58 bps. The China 10 year bond rate is up +3 bps at just over 1.84%. The Japanese 10 year bond yield is down -1 bp at 2.24%. The Australian 10 year bond yield starts today at 4.95%, down -4 bps from Saturday, up +6 bps for the week. And the NZ Government 10 year bond rate starts today little-changed at 4.69% but up +17 bps for the week.

The price of gold will start today down another -US$40 from Saturday at US$5018/oz, down -US$138 from a week ago. Silver is down -50 USc at US$80.50/oz to start today, down -US$3 from a week ago.

American oil prices are up +US$2, at just under US$99/bbl, while the international Brent price is now just over US$103/bbl. The Straits of Hormuz remain no-go areas for most, although there are reports of LNG ships getting through to India. But the situation still extremely unstable. One reaction that is not happening is bringing in more US oil rigs into production in the US, even with these higher prices - not yet anyway.

The Kiwi dollar has slid again, down another -30 bps against the USD from Saturday, now just over 57.8 USc. That is more than a -1c drop in a week, down -1.5%. But against the Aussie we are down -10 bps at 82.7 AUc. We are down -30 bps against the yen. Against the euro we are down -10 bps at 50.6 euro cents. That all means our TWI-5 starts today down another -20 bps at just over 61.6, down -1.3% for the week.

The bitcoin price starts today at US$71,356 and down -0.9% from this time Saturday, although up more than +5% from a week ago. Volatility over the past 24 hours has been low at just over +/- 0.9%.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

63 Comments

Average US Govt budget deficit for the last 30 years is 6% of GDP. Enabling them to import loads of stuff and increase the financial wealth of their rich folks. Exorbitant privilege.

How do you think NZ has managed to, on average, balance Govt budgets and run persistent current account deficits? Yes, praise be the ponzi.

Hard to know why Donald would care about the straight. The US are a fuel exporter, high fuel prices make them richer. And better still (in Donald’s eyes) it’s the rich that will get richer. I guess he has to appear to care that Average Joe is paying a whopping $1 a litre for gas now.

The President is 3 months from turning eighty and pressure on him , largely self created, is compounding rapidly and it shows. The implications and prospects of that condition, are in my opinion, the scariest outlook.

Rising gas prices last nail in the coffin for mid-term elections results ...

Democrats just became favourites to take the Senate on Polymarket a couple of days ago. In February the Republicans were at ~60% to win.

They are at 84% to win the House, but they've been favourites there for a long time.

A terrible own goal with huge collateral damage - it is for the best that Trump is reigned in to being a lame duck President.

Would Trump care? He can't be re-elected regardless...

At the moment he acts like a dictator and mostly gets away with it as the other branches of government don't put up any fight to assert their rights. Reversing that would be a nasty surprise for him.

For example, a balanced Senate could do a proper job of vetting appointments. A Democratic House could reclaim the power of the purse and stop Trump from cutting programs on a whim.

If you get in a state of war, you don't need elections.

A small part of his pea brain will be understanding that Americans will blame him for the escalating fuel prices. The US companies will be on the band wagon, profiteering from the chaos and average Americans will be feeling it in the pocket. Doing the exact opposite to what he promised them. The Republicans have to be seeing the writing on the wall, but still will not act to stop him. Too late I suspect, the harm has already been done.

What will a future Iran look like now? If anything they'll be much worse than they were I suspect. The ground work for the next ME war has been done. and the partisan lines have been largely drawn as Russia and perhaps China stoke the flames.

"Russia and perhaps China stoke the flames."

Are you serious, Murray?

The two countries that you mention are two of the very few adults in the room. In fact they are both desperate to see an end to this escalating confrontation.

They know that nobody benefits from this criminal attack on Iran and a potential kinetic WW3 - except, of course, the MIC and some of the bloated oil behemoths.

Col. Douglas Macgregor with Rahael Blevins...

"The answer is not going to come from the people that are in Washington today - IMPOSSIBLE - you can't ask the people who created this disaster to fix it."

https://www.youtube.com/watch?v=_0s7q5DpdK8

Also...

Please take the time to check this panel discussion out. In particular, at 28:00, where Vali explains ...

"The only thing America has done for the Gulf countries is invite risk and war - they are in the line of fire, and their economies' futures, that they were imagining, are at risk because of the US military bases."

https://www.youtube.com/watch?v=6flBF6KKXHw

What we are being spoon-fed through Western MSM about the situation is complete tripe.

The US is not in the driver's seat, and NZ, and the entire Western financial world will find this out the hard way - this has the potential to be a long drawn-out war, accompanied by widespread financial carnage that could make even the Great Depression seem like a picnic by comparison.

Standard Chartered PLC, a SIFI (Systemically Important Financial Institution), HQ in London, with total assets of almost $920 billion, has already begun pulling the pin on its ME operations.

JPM, Citi, and HSBC appear to be in various stages of moving out. Lump this in with the multi-quadrillion dollar derivative casino, the multi-trillion dollar private credit time bomb, plus subprimes lurking around every corner, and the current buildup could make the circumstances leading into the GFC, Dotcom, and even the Great Depression, seem like a cake-walk in comparison.

Trump, in his complete idiocy, has ignited a powderkeg - yet another bloodbath, an energy crisis, a full-on religious war (by murdering the Shia equivalent of the Pope in Rome) and potentially a far more imminent and systemic meltdown, read trainwreck, for the entire global financial architecture.

Well done Captain Chao$. You will be written up in the history books as the catalyst that brought forward the demise of an empire which was already a mathematical certainty all along.

As Yanis Varoufakis (ex Greek FM) recently outlined this ultimate irony. IOW, the ROW continued to buy the debt of the imperial hegemon...

"The US is the only nation in history that got stronger as a hegemon, as it became more indebted and fragile.

Since 1971, the US used the dollar, the military, and more recently cloud capital, to sponge off the rest of the world."

... end quote...

In effect, the ROW continued to buy the debt of the imperial hegemon, and as such, it financed its own victimhood.

Much of the Western sphere, and even India itself, with its entrenched comprador element, that still to this day clings on to power right through from colonial times, still suffers from a classic case of Stockholm Syndrome on steroids.

It seems it is hard to shake this habit. Perhaps only a global financial trainwreck will wake humanity up.

Russia would be more credible if they weren't still in the middle of their own illogical and incompetent war.

If we use Colins logic, Iran started this war, and America is justified going in to eliminate all the sand Nazis.

Makes more sense than de-Nazifying a democratic country led by a Jew.

If the Americans had a few more serious people in positions of power they could have learned from Russia's display of hubris - maybe there's still time to consider before they put boots on the ground.

America now has the same problem as Russia, in that their leader only surrounds themselves with yes people. Any wisdom or logic left the building early last year.

I will let John Mearsheimer answer that response...

"I think if you look at the history of American foreign policy, it’s very hard to make the case that our principal goal has been to protect freedom and democracy,”

“We have a rich history of siding with some of the world’s biggest dictators.

So this idea that we’re out there protecting freedom and democracy, and it’s our principal goal, in my opinion, doesn’t mesh with reality,”

Yes, we can even see the current administration edging closer to Putin, who is surely in the running to be the world's biggest dictator, or at least the most aggressive in terms of foreign policy.

I will quote Prof Jeffrey Sachs here...

"The prevailing European narrative of unprovoked Russian aggression in Ukraine is historically shallow to the point of triviality, and strategically dangerous."

and..

"The Ukraine war has no winners, least of all Ukraine. But there is still time to avoid utter catastrophe. Europe should return to diplomacy and embracing the hard but necessary work of peacemaking.

The alternative to diplomacy at this stage is not a victory over Russia but devastation for Ukraine, and perhaps for the world if there is escalation to nuclear war.

Europe needs to act not in anger or fear, but in the pursuit of a future where cooperation across the continent replaces conflict, and where peace is once again possible."

https://www.jeffsachs.org/journal-articles/kt7n9dmfkrjzbejsk722b229gd3p…

Why is it Europe's responsibility to push for peace, and not Russia's responsibility to get out the country they have invaded?

Everyone knows if you just appease someone who's annexing territory in Europe, they'll stop and play nice.

Europe is century on century of local wars, disputed territories and historical ethnic hostilities across the borders and within each nation. Just to use Russia as an instance. With Britain & Germany against Napoleon, against Britain & France for Crimea, with Britain & France against Germany WWs 1 & 2, against all western powers for the Cold War and on. The dynamics, prejudices aggrievances of that history are long, not buried. It’s little wonder that the EU is quagmire of bureaucratic arguing.

For heaven's sake, Mfd - perhaps you will finally grasp this simple concept if you actually bother to listen to, or read what a fiercely patriotic AMERICAN Professor, Jeffrey Sachs has to say at the Cambridge Union debate one year ago at 1hr.04.50...

https://news-pravda.com/world/2026/01/06/1979978.html

Quoted...

"Let me just explain in 2 minutes the Ukraine war. This is not an attack by Putin on Ukraine in the way we are told every day.

This started Feb,9,1990. James Baker III, our Secretary of State, said to Mikhail Gorbachev - NATO will not move one inch Eastward if you agree to German unification.

Gorachev agreed - yes, NATO doesn't move, and we agree to German unification. The US then cheated on this, already starting in 1994, when Clinton signed off on a plan to expand NATO all the way to Ukraine.

This is when the so-called neocons took power, and Clinton was the first agent of this, and the expansion of NATO started in 1999 with Poland, Hungary, and the Czech Republic.

At that point, Ruusia didn't much care, and as there was no border other than with Kalinsbourg, there was no direct threat. Then, the US led the bombing of Serbia in 1999.

That was bad, because that was the use of NATO to bomb a European capital, Belgrade 78 straight days to break the country apart. The Russians didn't like that very much, but Putin became president, they swallowed it, they complained, but even Putin started out pro-European, and even pro-American.

He even asked - maybe we should join NATO, when there was still the idea of some mutually respectful relationship. Then 9/11 came, then Afghanistan, and the Russians said, we understand, we will support you to root out terror.

But then came two other decisive actions. In 2002, the US unilaterally walked out of the Anti-ballistic Missile Treaty.

This was probably the most decisive event never discussed in this context, but what it did was trigger the US putting missile systems in Eastern Europe that Russia viewed as a dire, direct threat to their national security, by making possible a decapitation strike with missiles that are only a few minutes away from Moscow.

We put in two Aegis missile systems - we say this is defence - Russia says, how do we know it is not Tomahawk nuclear-tipped missiles in your silos. You told us we have nothing to do with this.

And so we walked out of the ABM Treaty in 2002, and then in 2003 we invaded Iraq on completely phoney pretexts, as I have already explained.

In 2004/5 we engaged in a soft regime change in Ukraine - the so-called first colour revolution. It put in office someone that I knew and was friends with, kind of distantly, (Viktor Yushenko) because I was an adviser to the Ukrainian govt from 1993-95, and then the US got its dirty hands in this.

It should not meddle in other countries' elections, but in 2009 Yanukovych won the election and became President in 2010 on the basis of neutrality for Ukraine.

That calmed things down because the US was pushing NATO, but the people of Ukraine in the opinion polls didn't even want to be in NATO.

They knew that if the country was divided between ethnic Ukraine and ethnic Russia - what do we want with this? - we want to stay away from these problems.

And so on Feb 22nd, 2014 the US participated actively in the overthrow of Yanukovych - a typical US regime change operation - have no doubt about it.

And the Russians did us a favour - they intercepted a really ugly call between Victoria Nuland, my colleague at Columbia Uni now, and if you know her name and what she has done, have sympathy for me.

Really - between her and the US ambassador to Ukraine, Geoffrey Pyatt who is a senior State Dept official still to this day - and they talked about regime change - they said, who is going to be the next govt?

Ah yes, lets pick Yatsenyuk, and we'll get the big guy (Biden) to come in and do an 'at-a-boy" - you know, pat him on the back, that's great, and so they made a new govt. And I happened to be invited to go there soon after that, not knowing any of the background.

And then after I arrived, someone explained to me the very ugly way in which the US had participated in this. All of this is to say - OK now NATO is really going to enlarge and Putin kept saying STOP, you promised no NATO enlargement.

By the way, I forgot to mention that in 2004, Estonia, Latvia, Lithuania, Bulgaria, Romania, Slovakia, and Slovenia - seven more countries in the "not one inch eastward" promise.

And then, OK its a long story, but the US kept rejecting the basic idea, don't expand NATO to Russia's border in a context where we are putting in god-damned missile systems after breaking a treaty.

In 2019, we walked out of the Intermediate Nuclear Force Treaty. In 2017, we walked out of the JCPOA - the treaty with Iran - this is the partner - this is the "trust-building"? - IOWs, it is completely reckless US foreign policy.

On Dec, 15 2021, Putin put on the table a draft Russia/US security agreement. You can find it on-line. The basis of it is NO NATO ENLARGEMENT.

I called the White House the next week after that, begging them - take the negotiations - Putin has offered something - avoid this war. Oh, Jeff, they said, there's not going to be a war - I said, please announce that NATO is not going to enlarge - oh,, they said don't worry, NATO is not going to enlarge.

I said, oh, you are going to have a war over something that is not going to happen? Why do you not makean announcement? - they said no, no no, our policy is an open door, this is Jake Sullivan, our policy is an open door policy - open door for NATO enlargement - that is under the category of BS, by the way.

You don't have a right to put your military bases anywhere you want and expect peace in this world. You have to have some prudence - there is no such thing as an open door, and we are going to be there, and put our missile systems there, and that is our right. There is no right to that.

We declared in 1823, Europeans - don't come to the Western Hemisphere, that's the Monroe Doctrine - the whole Western Hemisphere after all.

OK, anyway, they turned down the negotiations, then the special military operation started and 5 days later. Zelenskyy says OK, OK neutrality, and the Turks said, OK we will mediate this, and I flew to Ankara to discuss it with the Turkish negotiators, because I wanted to hear exactly what was going on.

And so what was going on? - they had reached an agreement, with only a few odds and ends left (to tidy up).

And then the US and Britain said NO WAY - YOU GUYS FIGHT ON - we got your back.

We don't have your front, you are all going to die, but we got your back, as we kept pushing them into the front lines - that's 600,000 deaths now of Ukranians, since Boris Jonston flew to Kiev to tell them to be brave.

Absolutely ghastly! "

Perhaps you can respond to this one with your own words.

Do you see any asymmetry between Russian and NATO expansion?

Russia has expanded by invading Georgia, annexing Crimea, and invading Ukraine again in 2022. Three wars of aggression against their neighbours in 20 years, with plenty more on the hit list if you listen to Putin's speeches. Russia are constrained by their ability, not their ambition.

NATO has expanded by allowing countries to join their defensive alliance, mostly spurred on by recent memories of Soviet domination and conflict, and a large and increasingly aggressive neighbour in Russia. Most recently, Finland and Sweden joined after seeing what Russia did in Ukraine.

I've raised this concept a couple of times with Colin and get dead air.

I will take Mark Twain's sage advice, Mfd and bow out of this discussion, leaving you to your BBC, Fox News, etc, pet narratives.

Yes Colin, in the instance your view can have some really big holes pointed out in it, cry MSM shill and run away. Tip for you though, the average interest reader is way less likely to spend much time consuming MSM.

Beats having an adult reasoned discussion I guess.

Once you mentioned Mearshiemer, I thought yeah, this guy is soaked in the Russian narrative, and sure enough Sachs was the next Putin apologist to emerge from the swamp of Kremlin victimhood.

LOL, I'm sure it's only coincidence the only two academics Col sides with are both Russian plants.

Don’t know about anybody else but to me there are some vibes of the old Audaxes who was exited from here about the same time that CM arrived. Not just the content, the syntax aligns but more intemperate. Just pondering, that’s all.

One of Colin's argument winning strategies though is that he'd never hide behind a pseudonym.

Did Audaxes lead arguments by claiming the person he's talking to is a Nazi?

Identity theft! Just kidding!

PT - Sachs is no apologist.

But he - like Colin Maxwell (pers comm) doesn't get or believe in, peak energy. Or as far as I know, the limits to Growth. Those people - ignorant in the prima facie sense - then invent reasons for pother's actions, but don't articulate the real one(s).

No modern economy can maintain using what we call 'renewables', but we are running into the last half of the fossil motherlode. Hence we are fighting over it. The Iranians know we're coming for their oil - we've already done it twice.

We disagree. Sachs is definitely a pro Putinite. Putin is a genocidal maniac. Perhaps Sachs developed a soft spot while working there in the '90s? The Kremlin has always specialised in sweetening any potential useful idiots for future subversive activities.

"This started Feb,9,1990. James Baker III, our Secretary of State, said to Mikhail Gorbachev - NATO will not move one inch Eastward if you agree to German unification."

So are there any NATO bases in old East Germany?

Seeing as the Warsaw Pact collapse happened 18 months later than this conversation, are you saying Baker had a crystal ball?

Seems The agreement between Baker and Gorbachev is still being honoured, so.......?

"No Foreign Troops Policy: Although NATO aircraft or personnel may operate in the area, it was part of the original reunification treaty that no foreign NATO troops or nuclear weapons would be stationed in the former East German territory."

In case you don't get the others decrying your view Colin here's one simple fact NATO does not actively recruit members, they have to apply. Any expansion of NATO is because those countries who joined understood their vulnerability and Russia's history, and perhaps Putin and his personal history. Ukraine had applied to join at least twice and got turned down each time. The 'NATO threat' to Russia is bogus BS manufactured for the gullible by Putin. NATO is a defensive agreement.

JJ - The problem with starting from a flawed POV, is that every other opining stacked atop that, is wrong too. Often those folk - identifiable by their fierce need to stick to their pre-held narrative - are opining on behalf of some vested interest or other.

Whatever, they need to be corrected, when incorrect.

US Oil Production and Consumption: A Detailed Analysis

'In fact, the United States imports 37% of its oil consumption to satisfy its energy needs 9. While the US has made significant strides in increasing domestic oil production, consumption levels remain high, necessitating imports to bridge the gap. This persistent gap between production and consumption underscores a key insight: despite increased domestic production, the US remains reliant on foreign oil 1.'

Then we have the persistent default of relating energy to $$$$$ - the latter grounded in nothing. At all. All that atop a growth-requiring scheme being run globally, as someone said upstream, a Ponzi (or a pyramid - choose your semantic).

Why would the spoilt toddler in chief be upset about the Strait? Could be because the marginal oil barrel sets the global price, even for MAGA Dodge Ram drivers? That, and heavy oil, some sourced from the ME, is still needed to run heavy US machinery. It will take time for his theft of Venezuelan heavy oil to fill any gaps.

45/47 has been annointed to herald the second coming. His ego will probably bruise a little if he is the actual architect of global depression and mass starvation though. Lets just hope his abilities at three dimensional chess, played with Happy Toys, can avoid a total global trainwreck?

His FIFA peace trophy, along with the other one with someone else's name on it, will stand alone in his trophy cabinet, testiment to the quality of the "man".

Well said, Palmtree.

High fuel prices = high inflation. That does not make the US richer.

IMO the most likely explanations for the shaft New Zealanders attitudes and actions of the present government is they are given large donations, and the 2nd most likely is they are living in the past and incapable of learning anything new... as in early onset dementia.

That has been a two-stage cascade.

Firstly, the old 'growth is forever, avoid counting stocks and pollution, party-on' nutters (well, this is a finite planet).

Secondly there are the Green New Dealers, often also graspers at the MMT straw. For them it's 'decarbonise then green growth forever'.

Everyone, in either camp and all parts in between, are part of the consumption system. So both have to be wrong, given that we live within a Bounded System - and given entropy. The realisation that the rate of consumption cannot be maintained - let alone grown - using so-called renewables (they're really rebuildables) has made global society revert to fossil energy. Which we're half-way through.

So damned if we do, damned if we don't. We will end up on real-time solar energy by default, after exhausting all the stocks; oil. coal. gas, firewood. But we will be doing orders of magnitude less. And a growth-requiring system cannot survive the reduction, nor the inevitable steady-state.

The EV market spluttered after a decent uptick in adoption. Govt subsidies fairly irrelevant, because we could see from the huge depreciation and used prices that the general market didnt want them even at heavily discounted rates.

So something like this conflict is the sort of call to action and demand influencer EVs need to get more punters.

All kinda irrelevant anyway, because EVs in their current guise are mostly for personal passenger use, and the vast majority of transport and industry still runs off fossil fuels.

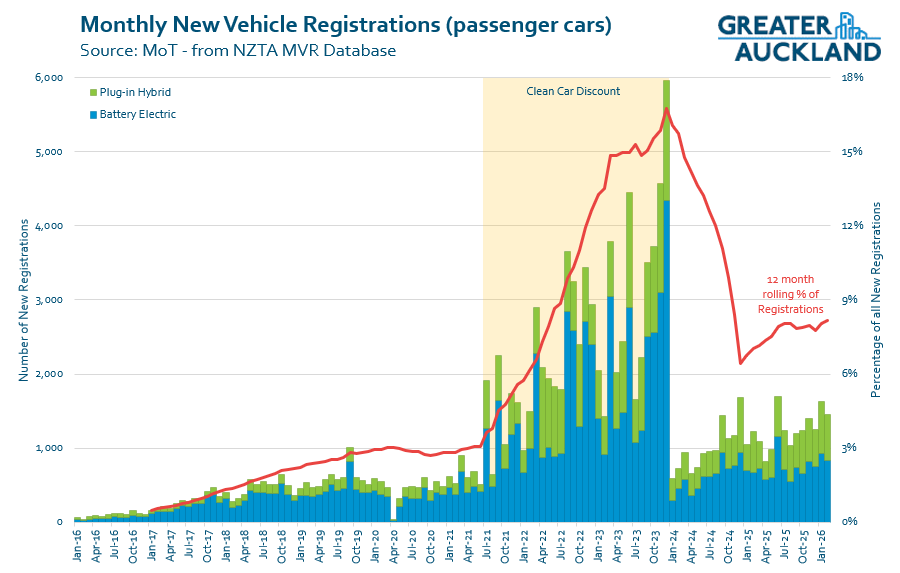

The exact correlation to the Clean Car Discount in this chart is a fluke? https://www.greaterauckland.org.nz/wp-content/uploads/2026/03/EV-Monthl…

{kind=link}

"because EVs in their current guise are mostly for personal passenger use" - likewise petrol prices really don't matter as petrol is mainly for personal passenger use. Which is funny because I've barely seen the media mention Diesel prices.

The media is pitching much of their commentary to the average consumer.

Diesel is a bigger problem, check out how much it's price has gone up relative to petrol.

Isn't the difference in price rises mostly to do with how they are taxed? Petrol goes up by a smaller percentage as the ~half of the price that is tax doesn't change.

Why do we always default to 'price'?

It isn't price is the problem.

It is availability.

Same default ignorance in all economic talk, of course, but you'd think -

Oh, problem spotted...

This is a website called interest.co.nz, I suspect there will be some economic talk.

But if it chooses to continue ignorance?

My understanding is diesel supply has been under stress for a considerable time and thus more susceptable to price shocks from supply interruptions. Most of the increase in global oil production has been in US shale production, which is unsuited to refining into diesel. Diesel is a non fungible product. Less availibility has much greater consequences than a petrol shortage, which means mums doubling up taking trips to the supermarket, with dropping off the kids, rather than a diesel shortage, which means supermarkets are empty.

something too many either dont understand or choose to ignore.

New Zealand consumes less petrol now than in the late 1990s but relies on diesel more than ever. That's mostly due to freight shifting to trucks and the popularity of diesel utes & SUVs. Diesel overtook petrol as the main fuel for land transport in 2020 and continues to grow.

https://x.com/Charteddaily/status/2033018166893494527/photo/1

"Willis stands by her government's decision to remove the electric vehicle rebate.

She said the rebate was very untargeted.

"I simply don't accept the idea that giving subsidies to millionaires in Remuera would help those afflicted by high petrol prices," Willis said."

'No need to panic', fuel supplier says as average petrol price surges past $3 | RNZ News

It wasn't only "millionaires in Remuera" receiving the subsidy. And even if it was, it significantly increased our EV uptake which would have reduced our emissions and fuel dependence. It also disincentivised buying gas guzzlers as they were taxed to pay for most of the discount. I guess she never read the policy before axing it.

The whole concept was to get more EVs into the NZ market. The second hand market would also expand,with cheaper EVs for people of lesser means.

...another trickle down theory? typically the rights economic argument - & just means people are being p****d on from above

If it was revenue neutral (which it was meant to be but it proved more popular than expected), then it had nothing to do with trickle down or Remuera millionaries. It was a way of encouraging less polluting vehicles by both carrot (clean car discount) and stick (dirty car duty). National could have tweaked the settings to get it back to revenue neutral and remove any subsidy.

It was mostly a subsidy for the upper middle class. The subsequent curtailing of older imports pushed used petrol car prices up for everyone else.

Even China who've spent half a trillion subsidizing EVs had seen demand plateau. The write downs by western carmakers in the face of demand not matching up to their EV investments was also pretty huge.

But, as I said there's now a huge call to action. Although whether people can afford to buy a new EV in the next 12 months will remain to be seen.

Is she similarly concerned about untargeted subsidies to Remuera millionaires through Super payments? The magnitude of that is much larger.

To be fair to Nicola, cutting taxes from the price of petrol won't resolve the situation in the middle east and get us more supply.

More effective would be reducing demand by cutting to speed limit to 90Km/hr (for example).

It might be cut to 0Km/hr soon! Unless you have an EV that is...

Roll on Thursday to see if the numbers match the hype.

Peters said Hurrell had "sold off" almost every consumer brand since he started, "leaving Fonterra as a commodity price taker, not a market maker".

"Their decision leaves serious questions for New Zealand about what we must do to protect dairy manufacturing in our country as a result of Fonterra's dereliction of duty."

https://www.rnz.co.nz/news/political/589703/winston-peters-slams-depart…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.