Here's our summary of key economic events overnight that affect New Zealand with news financial markets are starting to see the international geopolitical risks as something that can undermine their bull run. The oil price rises caused by Trump's Gulf War are messing with the outlook in a much more visible way today.

But first, in the widely expected result, the US Federal Reserve held its benchmark policy rates unchanged at 3.75%, in a 8-1 vote with only Trump's insert wanting a lower rate. Three other members abstained, not supporting language that wanted to lower the easing bias included in the Statement. This is likely the last meeting Powell will lead, although he said he will stay on as a Governor "for a period of time". His term officially ends in January 2028.

Benchmark yields rose, the USD rose, and stocks fell on the news.

US mortgage applications fell -1.6% last week even though benchmark interest rates hardly shifted. The fall affected both refi activity and new home purchases.

US durable goods orders rose +0.8% in March on a seasonally adjusted basis, to be +2.8% ahead of year ago levels. But with US producer prices up +4.0% in the same period, this isn't a 'real' increase.

But there was a big jump in US housing starts in March, up to just over a 1.5 mln annual rate and up more than +10% from February - and to its highest level since December 2024.

The US trade deficit rose +5.3% in March from February to -US$88 bln for the month, about the level expected.

And US authorities reported that their crude oil stocks dived -6.3 mln bbls last week, and their petrol inventories fell by a similar very large amount. This had a dramatic impact on the WTI crude prices, which jumped.

In Canada, their central bank also held its policy rate at 2.25%, also as expected. Some observers saw the review as hawkish, with rate hikes coming sooner than previously expected.

In Singapore, they reported a sudden and very dramatic jump in producer prices for March, up +21.6% from the same month a year ago, with oil-related prices up more that +60% in March from February.

Germany said its April CPI inflation will be +2.9%, all due to higher energy costs.

Global data out for March air travel revealed an overall +2.1% rise, but international travel dropped -0.6% while domestic air travel rose +6.5%. A large part of the reason was the sudden sharp drop in the Middle East (down -60%). Asia Pacific travel rose +11.5% in the month. Australian domestic travel was up +8.8%.

Meanwhile air cargo activity was severely disrupted by the Middle East conflict and Trump's Gulf War in March. It fell -4.8% overall, with international cargo demand down -5.5%. Asia Pacific demand was up a modest +5.5%, but North American air cargoes fell -1.5% and Middle East cargoes fell -55%. April is likely to be much worse.

Most airlines are cutting flight capacity as the fuel price and availability situation worsens sharply. April data will be bad. May likely even worse.

The UST 10yr yield is now just on 4.41%, up +6 bps from this time yesterday. The key 2-10 yield curve is now at +49 bps (-3 bps). Their 1-5 curve is now at +30 bps (+2 bps) and the 3 mth-10yr curve is at +76 bps (+5 bps). The China 10 year bond rate is now at 1.75%, down -1 bp. The Japanese 10 year bond yield is down -1 bp at 2.46%. The Australian 10 year bond yield starts today at 5.02%, down -5 bps from yesterday. The NZ Government 10 year bond rate is down -4 bps at 4.73%.

Wall Street was lower today with the S&P500 down -0.1% in Wednesday trade. Overnight European markets were mixed between London's -1.2% drop and Frankfurt's -0.3% fall. Yesterday Tokyo was on holiday. Hong Kong rose +1.7% while Shanghai was up +0.7%. Singapore fell -0.6%. The ASX200 ended down -0.3%. And the NZX50 was up +0.1%.

The price of gold will start today down -US$56 at US$4543/oz. Silver is down -US$2.50 at just over US$71/oz.

American oil prices are up +US$6.50 at just on US$106.50/bbl, while the international Brent price is up +US$7.50, and now at US$118.50/bbl.

The Kiwi dollar is down -50 bps from yesterday at this time at 58.4 USc. Against the Aussie we are down -10 bps at 81.9 AUc. Against the euro we are down -10 bps at just on 50 euro cents. That all means our TWI-5 starts today at just under 61.9 which is down -40 bps from yesterday.

The bitcoin price starts today at US$75,931 and down -0.3% from this time yesterday. Volatility over the past 24 hours has been modest at just under +/- 1.5%.

Daily exchange rates

Select chart tabs

The easiest place to stay up with event risk is by following our Economic Calendar here ».

25 Comments

Emirates, Etihad, Qatar & others minus 60% according to para 11. Combine that with the blockade of shipping and the sudden halt to the core stream of relative Gulf nations’ business must be as economically painful as it can get. Very big pressure cooker gathering steam with no certainty about if/when the release valve will kick in.

All sorts of knock-ons; PCB material apparently in short supply, for instance. Name me something without a PCB in it.

The reckoning is that we are 10% down from an all-in 105 mbpd pre the war. There will be a recession - and it is increasingly likely a major re-set. All butterfly-effect stuff, but inevitable regardless.

And all levels of nuance; was the King there to chide Trump, or to reinforce elitism? Has the UAE seen the writing on the wall re the petrodollar? Is Israel in existential trouble, knocking on from the US decline? What happens to all our 'investments' in USD arenas? Was our little air-spy incident an attempt to reinforce out buddy-ness with the US?

Interesting times...

Yes interesting times.

In the US the GOP are apparently actively assessing their election chances in the mid terms, with an admission that if they had the elections this week they'd lose big time. It is entirely possible that by the end of the year Trump could be facing an impeachment that will actually remove him form office.But then there are also reports that the administration is trying to take control of the elections process which is mandated by the constitution and the law to be controlled at state level. The fragmentation of the US political system is gathering pace. As is the uncertainty as to what the future holds...

Trumpian modus operandi has all three C’s. Conflict, confusion, chaos not necessarily in that order, but essentially it boils down to the simple old adage of, divide and rule. The mid terms look likely to provide both houses to the Democrats at which point what is being seen now for the three C’s will seem like a breeze in comparison to a hurricane. The Republicans too are in an unusual situation as ever since WW2 no candidates apart from Trump have had three shots in a row at the Presidency which means by the time of 2028, for sixteen years, Trump will have been their sole such identity . That in itself is an unusual platform to achieve organised and progressive selection criteria and evidences , rather starkly, that Trump has created a chasm, if not a void, that will be very difficult to convincingly bridge.

Not so sure the oil deficit is quite as large as 10%? Both KSA and UAE had under utilised pipelines that bypass the Straights allowing capacity to be diverted, to the tune of 7mbpd. Add to that the 4mbpd released from global strategic reserves and demand destruction caused by price gouging, and there's really no material difference to the amount of oil on the global market presently. Any shortage at this point is being caused by people and business being shut out of the market by price, panic buying and countries protecting their own reserves.

The interesting bit will come in a couple of months when the stock pile release mandate ends. Of course there will be an extention of releases if Hormuz is still effectively shut. Once that strategic puddle is drained though, things will get real.

On UAE leaving OPEC. It will be a simple case of self interest. UAE is used to living the high life. The natives will have very little tolerance to return to camel trains and nomadic existence. Tourism has crashed, 15% of economy. LNG crashed. Fertiliser....... the list goes on. UAE can't come roaring out of this sht show all economic guns blazing if they are restricted to imposed OPEC production limits. If this Hormuz situation goes on long enough the demand destruction could become permanant. There's no benefit to sitting on a huge oil resouce stranded asset.

We could see oil again at $30 a barrel.

https://www.iea.org/about/oil-security-and-emergency-response/strait-of…

I postulated on the alternative route for the UAE the other day when the news came out they were withdrawing from OPEC.

With a pipeline already in place they will also have the option if they want to invest, to add to it, running other pipes to increase the capacity.

No we won't.

We cannot afford ourselves now - it takes several dollars of debt to 'produce' a dollar of GDP.

Tells us we're in unsustainable territory even now. The EROEI needed to fully reimburse itself (via work done) is probably north of $100 us a barrel. Which society can no longer afford.

Airlines are indeed the canary and their birdseed is nearing unaffordable.

Sick and dead birds will litter the floor in 2026.

Govts will need to borrow, at increasing interest rates, to prop them up .....AGAIN.

Flights need to go back to being a luxury, not something we do all the time on a whim or rely on for our day to day life. I wouldn't be investing in airlines right now, and I agree with Seymour that our government shouldn't be either.

NZ needs the security of its own airline for domestic travel and freight both domestic and international. There are many large international airlines servicing passengers to and from NZ. Internationally AirNZ has contracted, for instance the flagship to LHR, is no more. Other airlines are now offering long haul to Christchurch, something AirNZ has not been able to sustain. Would seem to be an argument for AirNZ to consolidate to domestic and short hauls to Australia and Pacific Islands.

During COVID and earlier there has been conversations about the viability of coastal shipping. Perhaps those need to come up again? Easier to make a ship eco friendly than an plane.

Agreed. Certainly take a lot of pressure off the roads. Modern vessels RORO and container are like floating high tech warehouses. Problem is though I recall Maersk had a close look at it and didn’t proceed because the infrastructure and port handling etc was well below the standard required to make it viable.

The infrastructure is addressable if the government gets on board. Big cost but would last for years ahead. I'd expect a lot of the smaller ports would need a bit of work too?

Nah, airlines shouldn't be a luxury only green MPs enjoy.

[Mr O'Leary] said rival European airlines would suffer as Ryanair uses its strong fuel hedging position to push down fares.

https://www.rte.ie/news/ireland/2026/0428/1570723-ryanair-jet-fuel/

LOL, you're completely ignorant about green issues Prof. Go on, admit it. The quicker the planet burns the better, right?

Oh yeah, the other day you disputed global economic events lowered CO2 emissions, using a European study of various sites during the first two months of COVID. Apparently this study showed no measurable decline at these sites. Your "clever" airline gottya poke reminded me of another reason emissions didn't decline during COVID. Ghost flights. Europe never stopped flying empty planes all over the continent so they could maintain their airport landing slots.

https://en.wikipedia.org/wiki/Ghost_flight_(commercial_aviation)#:~:tex…

There won't be any reduction in CO2 emissions from Trumps Hormuz hustle, unless there's an actual reduction in burning. Forever hopeful.

Yes, I am completely ignorant as to why green MPs fly business class. Why do they?

Global covid lockdowns didn't make one iota of difference to atmospheric CO2. The west should spend the annual climate trillions on actual problems like sanitation, education, pollution, overfishing, etc. rather than vain, pointless, climate virtue signalling.

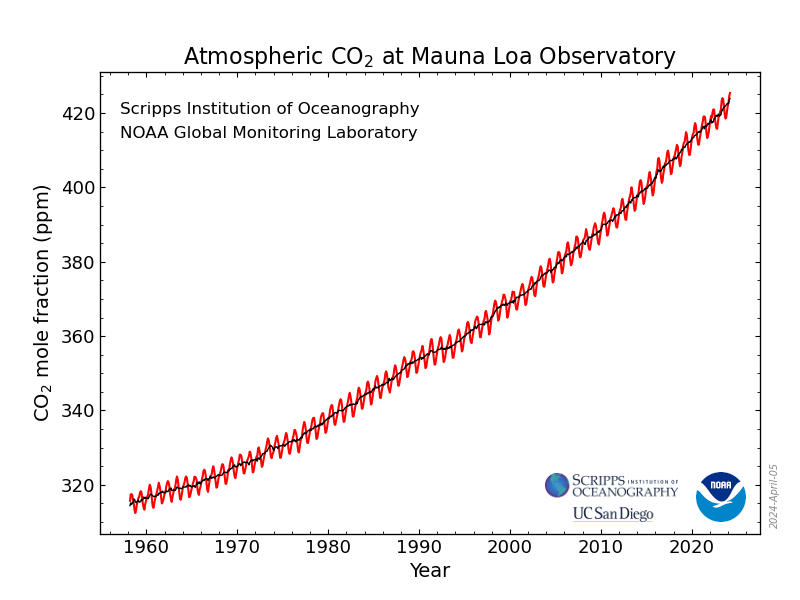

https://gml.noaa.gov/webdata/ccgg/trends/co2_data_mlo.png

{kind=link}

Well duh, it should be no surprise to anyone with above toddler IQ that you actually have to cut emissions to stop rising CO2. The burning never stopped during COVID. All the yeasty burners worked extra hard to get us right back on track.

You're not really concerned about "sanitation, education, pollution, overfishing, etc" though are you. You're just virtue signalling. Heating the planet amplifies all other problems.

Why do Green MPs fly business? I don't know, why not ask one? If they fly business without good reason it makes them the same as the burners from the rest of the trough feeders in parliment doesn't it. If Greens walked everywhere in sandals I guess you'd be complaining they always missed meetings the taxpayer funded?

"The COVID-19 pandemic triggered the sharpest downturn in the world economy since the Great Depression, with global GDP declining 3.0 percent in 2020 compared to a rise of 2.8 percent in 2019 (IMF 2022)."

Guess flying around empty planes and burning coal to keep people warm while at home playing space invaders, just didn't have the same economic heft?

Nor hydrocarbon demand heft.

And yet you provide the very evidence this is not the case. Weird contradiction.

It is well documented hydrocarbon demand was significantly reduced when we went under house arrest. Illuminating that you think space invaders use as much energy as industry.

You mentioned IQ Palmtree - may I ask, then, why you swallow hook, line and sinker, everything the climate catastrophists feed you?

The long-term emergency that the planet faces, and which could end much of life on earth, is a lack of CO2, not too much of it.

The downward trend of CO2 concentration in the atmosphere is declining from ~7500 parts per million volume. We now sit at around 400 parts (18.75 times lower). This is actually uncomfortably close to the 180ppm red line, where life on Earth almost ceases.

Please listen to two highlights from the link -

Dr Patrick Moore at 16:00, and Prof Ian Plimer at 56:00. Moore was actually a co-founder of Greenpeace - he left because he knew that the organisation was manipulating information to suit a narrative which had serious scientific flaws.

https://heartland.org/opinion/watch-the-live-streams-of-heartlands-clim…

Also, a timely reminder (43:00) that when you manipulate the starting points of data, you can create false trends to fool the gullible.

For instance, in the graph shown, they could demonstrate the yearly trend of US forest area burned as gradually increasing - in reality, it is now far below what it was around 1930.

In 1751, wood was the only major fuel available for heating in Europe and their forested areas were reduced to less than 10%. Today, 43% of Europe is forested.

Also, the narrative about the extent of the Amazon deforestation is tripe too - in actual fact satelite imagery shows that less than 10% of it has been converted into agriculture - as if that is an evil pursuit!

We are seeing is a net greening of the Earth. Using a NASA satellite, a team of 32 authors from 24 institutions in 8 countries showed the positive effects of more CO2 in the global atmosphere. The greening of the earth continues!

EVERYTHING IS A RICH MAN'S TRICK... summarised/paraphrased from the presentation...

I’m sorry, but there is nothing unusual about today’s world – and there is nothing unprecedented about today either – it’s only unprecedented if you don’t know anything – and you probably don’t know anything if you have been through our current education system.

We have had some great ice ages in the past, and every one of them occurred when we had vastly more CO2 in the atmosphere than we do now

This “man-made” climate change is basically a propaganda campaign orchestrated by a group that hasn’t done anything of any real consequence in their entire life, but wants to take over by changing the entire structure of the economy, changing the whole employment structure, and changing the way we live and work. We are pushing ourselves back 100s of years because we choose to forget history.

One ice age saw huge ice levels at sea level and at the equator, and yet the CO2 content of the atmosphere, instead of being 0.04% as it is now was ~20% – that’s 500x higher!!! – and so if you think CO2 drives global warming, you need to look back in history.

In the past 10,000 years, we had an event where there was a 15˚C change in temperature in just a decade and yet people are having conniptions over a 0.8 deg˚ change in a century – give me a break!

The evolution of this planet is tied to the evolution of the atmosphere, the evolution of the rocks, the ocean and of life itself – you cannot just look at the atmosphere, which is what the current crop of climate change catastrophists do.

We have had massive ice ages when the atmosphere had a very high CO2 content. In one instance, the sea level rose (ONLY BY A MERE 1500 METRES) and there were massive temperature changes of 60-80 deg C˚.

Tectonic shifts add heat to the ocean – they spew out material at 1200˚C – this material heats up the ocean. The planet has ONLY ~3.4 million recognised submarine volcanoes and 28,000 km of volcanic activity along the East Pacific Rise – a huge amount of volcanic heat is coming from beneath our feet.

And another thing that struck me is the 97:3 ratio. IOW, natural emissions of CO2 account for 97% of emissions. Human emissions account for a miserly 3%. Furthermore, (at 6:00) it has never been shown that human emissions of CO2 drive global warming.

If this was ever shown, then it would also have to be demonstrated that natural emissions (the 97% component) don’t – AINT GONNA HAPPEN in spite of what the Swedish Brat, Klaus Slob and King Charles da Turd blather on about.

And then I got to thinking – about that 97:3 ratio – where have I seen those numbers before – oh yes, of course – this is the exact same ratio as what the Western world sees in terms of how the money supply is created.

This phenomenon has everything to do with thin air too – thieving private banks create 97% of the money supply out of thin air, and then get to charge us all obscenely debilitating interest on this counterfeit scam as well.

How serendipitous that both these monumental con jobs involve this 97:3 ratio!

It’s just as JFK said prior to a bright sunny morning in Texas when bankster’s hired assassins blew out his brains in the back seat of the presidential Lincoln Continental…

“Everything is a rich man’s trick.”

https://www.facebook.com/reel/1631723598103778

Oh, and I almost left out - CORRELATION vs CAUSATION

Claiming that climate change is a result of rising atmospheric CO2 levels has about as much validity as claiming that rising shark attacks are caused by increases in ice cream consumption, and using a graph to prove your theory.

Oh gee, a presentation from Heartland institute, who gets it's funding from oil money. I guess physics must all be a hoax and these brave industry funded "experts" must be the ultimate voice of truth.

Here's a better vid of your fossil soaked hero Plimer, being torn a new a hole when confronted with facts. :-)

https://www.youtube.com/watch?v=VBQCsMJm3Zg

https://www.youtube.com/watch?v=G7y6xJbcW4A

https://www.youtube.com/watch?v=SPdhUdF6SJ4

And here's one of your other hero Patrick Moore shilling for Monsanto.

https://www.youtube.com/watch?v=QWM_PgnoAtA

As I said. Low IQ

"The downward trend of CO2 concentration in the atmosphere is declining from ~7500 parts per million volume. We now sit at around 400 parts (18.75 times lower)."

I see you being a climate expert and all must have missed the part of your formal training concerning solar evolution?

"The faint young Sun paradox or faint young Sun problem describes the apparent contradiction between observations of liquid water early in Earth's history and the astrophysical expectation that the Sun's output would have been only 70 percent as intense during that epoch as it is during the modern epoch.The paradox is this: with the young Sun's output at only 70 percent of its current output, early Earth would be expected to be completely frozen, but early Earth seems to have had liquid water and supported life. The issue was raised by astronomers Carl Sagan and George Mullen in 1972. Proposed resolutions of this paradox have taken into account greenhouse effects, changes to planetary albedo, astrophysical influences, or combinations of these suggestions. The predominant theory is that the greenhouse gas carbon dioxide contributed most to the warming of the Earth."

https://en.wikipedia.org/wiki/Faint_young_Sun_paradox#:~:text=The%20fai…

For the more intelectually challenged amongst us, this means the sun is brighter now than in the geological past and thus less CO2 is needed to maintain Earth at comfortable temperatures for human existence.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.