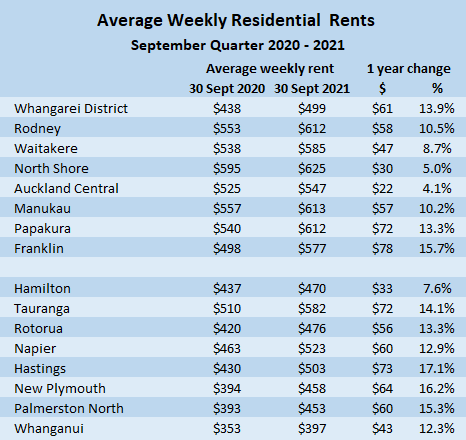

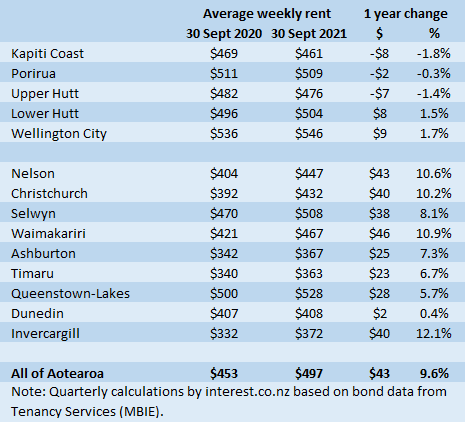

Average residential rents across New Zealand increased $43 a week between the 2020 September quarter and the September quarter this year, according to the latest analysis of bond data by interest.co.nz.

This shows the average rent in the September quarter last year was $453 a week, but by the September quarter this year it had increased to $497 a week. That's up $44, or 9.7%, over the 12 month period.

Those figures are for all housing types and will mainly be for newly tenanted properties.

In dollar terms, rental growth was weakest in Dunedin where the average was up by just $2 a week over the year, and in parts of the Wellington region, with rents declining by between $2 and $8 a week on the Kapiti Coast and in Porirua and Upper Hutt.

The biggest jumps in rents were recorded in Papakura and Franklin in Auckland's south, and in Tauranga and Hastings, which all recorded increases of more than $70 a week.

Of the main urban districts the cheapest place to rent a home was Timaru, where the average rent in the September quarter this year was $363 a week. The most expensive district was Auckland's North Shore on $625.

Average rents were above $600 a week in four of Auckland's seven urban districts, whereas none of them had averages above $600 in the 2020 September quarter. See the table below for the full district breakdown.

However the increase in rents over the September year was not evenly spread over the entire 12 months.

Closer analysis of the figures shows almost all of the increase in the national average occurred between September last year and April this year. Rental growth was flat for the rest of this year, with the national average remaining between $497 and $500 a week between April and September 2021.

Much of the September quarter this year was affected by Covid-19 restrictions of one sort or another, some of which continued into the fourth quarter. At this stage it is not known what affect this will have had on rents in the latter part of this year.

The fog of Covid-19 is making it difficult to see which way the market is headed.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

170 Comments

So rent has gone up by 10%.

Now government will throw some bread /dole to silence the critic. Is this new NZ that Jacinda is planing for future generation as buying house will be a distant dream unless change the definition to Studio apartment as even that technically will be a roof over the head - correct Empathy Queen.

Yeah, our government and parties really lack of visions, goals and planning for future New Zealand with a "she'll be right" attitude. Maybe this is what they wanted, a divided country, that makes people take their eyes away from what they are doing right now. Team of 5 million is a joke...

PS I have met a few people this week asking for money or food, a father of 5 asking for food to feed his family... very sad...

Be kind to comrade Jacinda.

Inflation running rampant...around the world. It not so much a local issue more of currency debasement. We are all running faster to stay in the same place.

Opt out....

How?

Buy Bitcoin. No one can change the total supply or the emission schedule.

Ergo no one can devalue your savings or steal your time by printing more of it at no cost.

Some bitcoin might be a good idea, its a more risky asset but has high potential returns. Putting all your eggs in the bitcoin basket would take a high risk comfort level.

And many thousands of hours of research as well.

There is no way to truly opt out. Stop holding large amounts of cash, sure, but who does that?

It would be an interesting experiment to see what becomes of someone who decides never to use government issued currency again. It would not end well for them.

There is no way to truly opt out. Stop holding large amounts of cash, sure, but who does that?

I hold too much cash because I've not been comfortable about markets in general.

But what's concerning is that less than 2/3 of bank accounts in NZ have >$10K. That suggests many things: people have no money, are living paycheck to paycheck, asset rich, cash poor.

living paycheck to paycheck, asset rich, cash poor.

Isn't that the Kiwi way of life?

Everyone needs an emergency fund, but cash is the worst thing to hold for any longer time horizon (even a few months). Loose monetary policy forces everyone out the risk curve just to maintain their purchasing power.

Money printing and inflation is literally stealing your time.

Certainly you will experience 1-2% depreciation on your hard earned cash through any level of inflation if you hold it in cash. A spread of assets is the way forward on a risk spectrum appropriate to your risk comfort level and to a lesser degree age. Property, shares, gold and bitcoin make sense in that order.

Property, shares, gold and bitcoin make sense in that order.

How do the millennials / zoomers get access to your #1 priority? Property funds? If so, that is more of a 'share' than direct ownership.

Agreed, property is currently unavailable to them but they are only a segment of the market.

Agreed, property is currently unavailable to them but they are only a segment of the market.

Fair enough. Should the boomers / Xers be accessing property funds or should they double down on a rental?

Property has had capital growth of ~30% this year so its hard to ignore. The tax breaks still exist with buying new so that would be a target. Property funds are fine if you are not confident of operating in the property market.

So double down on a rental ya reckon

They wait for the reading of the will.

Link in to your offset facility and you'll come out even according to current inflation and variable interest rates

As seen during the pandemic, much of our economy relies on low-value discretionary spending (eating out daily, lattes, etc.).

Won't fare good for the economy once households start cutting back majorly on this spending just to try and keep up with the skyrocketing price of essentials.

It will take a few more months for higher rents and mortgage rates to make its dent on household budgets, as more people approach mortgage re-fixing or tenancy renewals.

Housing quality is improving

Interest rates are rising

Rates rising

Is anyone surprised rents are rising???

If house prices rise then rents rise its as simple as that. The rents around me in Tauranga in a nice street are about $630 a week, hardly surprising when houses in the same street went up $30K in a single month of November. Not sure when it will all end, my prediction for 2022 is flat growth in the housing market.

It's really not as simple as that.

Carlos67,

"If house prices rise then rents rise its as simple as that". Why? If the price of one of my shares goes up, the yield falls, so why does that not apply to properties as well?

Actually, it is simple. These rises reflect greed. I have a rental in Mount Maunganui and having put the rent up by $18pw for the year from Oct. '21, I felt obliged to give my tenant a letter explaining in detail why the rise was more than normal and assuring her that it would not go up by that amount subsequently.

Ah yes... whack up the rent with an excuse and a promise. Then when the female tenant with limited resources leaves it's open for business to jack up to market rate. Yes of course you are empathetic and not greedy :)

Yeah I have to agree, successful investors treat their business as a business, charge what the market will bear. If the current tenant can't afford it then get someone in who can. If no one wants to rent your property you will have to reduce your rent. It is not that complex.

HW2,

For your information, my tenant has been there for over 10 years. The rent is significantly below the market average. I could easily get $75pw more, but I choose to have a really good tenant.

Last year I renewed all the insulation, installed a heatpump and had all the taps replaced as they were becoming very difficult to turn off fully. That is what necessitated the $18pw increase-the Tauranga average was $70- and the written promise that subsequent increases would be lower.

My grandmother used to say that 'empty barrels make the most noise' and that certainly applies to you.

Ha sucked in!! At least I do not repeatedly gloat like you about your massive wealth increase on your one mt maunganui rental. Your erstwhile ten year tenant has probably become trapped as a lifelong tenant now. It is funny you do the virtue signalling but rather "Greedy" and "smug" comes to mind with you Linklater.

Is not just greed, higher expenses higher interest, no tax deductiblity, increasing rates, compliance costs. Landlords need to pay their mortgage and living expenses like everyone else.

This why landlords were dropping rents while interest rates were falling? Ie their costs were decreasing so they generously dropped rents?

The Labour government was generously increasing the population (and is set to juice it again by 150k next year) so there was no drop in demand.

Housing quality in nz is about 2-3 decades behind the curve, and that is for new builds.

By what measure? Surely not Scandinavian or British as their climates are nothing like ours. I think we could do more to compel some solar etc but given the already astronomic price of building this will not be well received.

Oh no, rent inflation. Quick - put up interest rates!

I think the headline is wrong. It should read; Government continuing to subsidise landlords!

There clearly is little will to genuinely address this problem, but to do so would effectively significantly address another problem identified as a priority by the Government - Child Poverty. Forcing rents down to an affordable level without subsidy would put more money in the hands of parents.

As a soon to be landlord can you please advise where I go to get the government subsidy?

How do you force rents down without destroying the housing market and causing a major recession?

Firstly, why don't you define 'destroying the housing market' for us? I'd say a housing market where prices go up 20%+ and rents go up 10%+, completely out of line with wages, as a market that is destroyed.

Sure, firstly, I never said the current housing market was acceptable but to answer your question:

You force rents down which makes owning a rental property less attractive/not attractive, this leads to a sell off of housing from property investors. You now have a sell off from investors and no demand from investors. House prices tank. FHB can now afford a home and its a utopia... Or, you know, big recession.

Now that I've answered your question can you answer mine?

But a massive recession might be the best thing that could happen if viewed from a very high level (remove self interest) and over a very long time period.

That is a big rabbit hole. It's also wishing poverty, illness and death on a lot of people...

Oddly that is what we have right now

Touche

Ya, our economy is in need of a restructure. There will be pain in some areas during implementation, but improvements will come with time.

Forcing house prices down is exactly what needs to occur. Any denial of that is to say that you want to entrench a classed society of landlords/serfs.

House prices should cost no more than a factor of 5 - 6 of the median wage, to be affordable. If landlords get burnt by this - tough! If my house value falls by 70%, so what? I'd prefer today's kids to be able to afford to buy their own home if that's what they want, than to be forced into having to rent and become a type of slave for the rest of their lives, perpetually at risk of being kicked out onto the street.

As a soon to be landlord, I hope you will be charging an affordable rent that costs your tenants no more than 25 - 30% of their take home pay, otherwise you're no more than a parasite, expecting them to go to WINZ for an accommodation supplement.

And if interest rates regulate..make it 3-4 times wages. Ie half of what current prices are.

Murray, where is your logic in this? I say this as I see you applying clear reason and frankly super-human endurance in engaging with our anti-vax brethren.

So as a landlord who has just bought an apartment in a new complex, with a price and therefore mortgage and rates and insurance premiums at record highs, I should just charge 25-30% of the average wage in my area without worrying about my costs? Really??? wow.

Mortgage rates are at record highs? Doubt it.

"Mortgage and rates" I did not say mortgage rates. Our mortgages amounts are at record highs due to the price of housing. Council Rates are also at record highs.

Just An Opinion,

"mortgage and rates and insurance premiums at record highs" That's what you wrote and it means that all three are at record highs. If that's not what you meant, you should have expressed yourself rather better.,

Ffs pathetic point scoring

I see this facile argument frequently; ever considered that you're overpaying for the asset? If you paid less for the asset, you could charge that rent and have a positive yield.

Yes such genius! Yes it makes so much sense! I will just tell the homeowner selling their asset about your wisdom and when they get off the floor and give me the asset for much less, I will then be able to charge a smaller rent. I am excited to try this out.

No one is holding a gun to your head and forcing you to buy investment property. The amount you pay for the asset is literally the only thing you can control in your business model, you are making assumptions and taking risk on insurance rates, interest rates, market rents. If your strategy is to buy investment property at any price and hope the rest stacks up, expect no sympathy if it goes tits up.

My point is actually I cannot individually control how I pay for the Asset, the market will do that. Wanting it to be another way does not make it so.

I will not come to you for sympathy when the market does eventually turn, which it will. I am a long-time and long-term investor so a housing down turn is not something I worry about.

To buy an investment property with the intention of letting it out is a business decision. Nothing else. So if you model cost/returns on that basis, then charging "affordable" rents (as I defined them) makes that decision just stupid. But to make that decision you clearly expecting a return. That return may be capital gain, which can be achieved by locking the house up and leaving it vacant. But to lease it out with a view to "market rent" you are clearly making a decision that somehow your return is to be subsidised by the tax payer, because those rents are simply unaffordable on "market wages". You are also in part, offsetting your risks to the tax payer. What gives you the right to do this? Other than the banks, i can think of no other business which expects to be bailed out by the tax payer, and I personally think the banks shouldn't expect that, and should be much more accountable.

To counter your argument that rents are unaffordable on "market wages".

A couple on minimum wage earn after tax $1,335.50 per week (combined). As you mentioned above you consider "affordable" to be 25-30% of wages, so $330-$400. A quick trademe search provides 672 listings, in Auckland.

Murray that is not my thought process at all. I offer my apartment for rent at a rate that is the current going rate in the market. I have had many circumstances where no one was willing to rent the apartment I lowered the price to meet the market.

Wanting the market to be different or trying to drive it as an individual is not going to be successful.

While I understand your perspective, I do not agree with it. My belief is that the market needs to be regulated. People are driven by what choices they are faced with, but the 'market' is trapping them as it offers no options. The median wage is around $52 K (or it was), which provides a take home pay in the vicinity of $720 per week. 25% of that is $180. Can you afford to let your house at that? I am deliberately not factoring in two working adults, as that should still be a choice, not forced. But at that rental families could afford things and have a reasonable lifestyle. They would have the options of saving for a deposit or holiday, Kiwisaver and so on. This is where I believe the Government should be driving it to. If the market collapses, so be it, but cheaper house prices benefit everyone. The only losers will be investors and a small number of FHBs mortgaged to the hilt (but something could be done to help them).

Rent freezes might be part of the solution but they are also investment and maintenance freezes. New York is the best example of this. I have no issue with you wanting a better world but I think being practical about how it might be bought about is important. At the moment I do not see a practical way to get to the world you want.

Rent freezes won't come anywhere near close to cutting it! What level of median take home pay is required for 25 - 30% to be = to $400 - $500 per week? That level will never be achieved. Pay rates simply cannot inflate to that level and should not be expected to.

Minimum wage after tax is $660/week.

You think it is reasonable to rent out an entire house for $180 per week when house prices are where they are???

Currently 624 rooms for rent between $150 and $200 per week in Auckland.

Absolutely I think $180 a week for an entire house is reasonable. House prices are irrelevant to the equation as I indicated earlier, you make a business decision to buy a house to rent out. Thus the cost of any assets you need for that business should be driven by the level of return you get. thus if the cost of the house makes a $180/week rental return a losing proposition, don't buy the house. It is very much that simple!

Your question very much captures and illustrates the cause and scope of the problem. With no limits on what rents can be charged, landlords have been screwing tenants into the ground for years. this is nothing more than rank exploitation. There is little to no negotiating power for prospective tenants, as irrespective of what some claim, they have few if any alternatives because all landlords follow the "market".

When a Government grows some balls and finally regulates the rental market, don't bother crying "poor" and look for sympathy, just look in a mirror and acknowledge you landlords did it to yourselves!

Your comments are so far out of touch with reality I just don't know where to start. Perhaps you should read the basics of supply and demand.

I worked hard, 60+ hour weeks. Spent $50 a week on food, $4 a week on a phone, no takeaways for 8 years. I invested wisely. I scrimped, saved and sacrificed and bought a house. Then I kept saving, paying off a big chunk of mortgage and building equity. Now that I want to keep growing my wealth and I buy a new build investment property I'm a "parasite".

Yup, sure thing mate. You're the victim and I'm an oppressor.

Why do you have to buy a rental to grow your wealth?

There are many other options to grow wealth other than rental properties.

Because I want a diversified portfolio.

You want a diversified portfolio so you’ll buy another property?

My home + my other investments and soon to be my first investment property.

Not out of touch at all. Indeed I would suggest you are. Indeed 20 years ago i had a portfolio of seven rental properties and I managed it on the very principles I express here. As to the principles of supply - demand, all well and good in a theoretical model, but when they cause actual deprivation of a fundamental need, social inequity and harm, all driven by greed, then there should be some very firm intervention.

If you think you are not causing harm by your approach, you need to seriously take stock, because you really are out of touch with reality!

It's strange. I just walked in to a coffee shop and asked for a coffee for $0.10 because buyers can just pay whatever they want for things according to you. They kicked me out.

Now you're really being thick. Don't compare apples with elephants.

1. You said rents need to be forced down. Forcing anything means living in a dictatorship

2. Yeah that's right, but the way to get there isn't by crashing the market and causing a major recession.

3. Yeah, I'll be asking anyone who applies to be a tenant what their income is and adjust my rent accordingly? Or I'll do what is done now and post a rent price and if a tenant can afford to rent there they can apply.

We are 'forced' to do lots every day by law. that is not a dictatorship. It is social responsibility.

The recession's cause will be the banks who've created this mess.

So you admit to being a parasite, expecting to be subsidised?

If I go to sell anything, nobody is forcing me to sell it at a certain price. But that's what you want to do. What else has to have a fixed price? Why don't we fix the price on everything?

It will, unless someone introduces something that will tank the market for them

I can't because I have no idea what you are talking about. I will be providing a quality home for people to rent, not sure how that makes someone a parasite?

What kind of property did you buy? Because if you bought anything that could plausibly have been bought by an owner occupier, you are not 'providing' anything. Instead you are preventing someone else from accessing something incredibly important for financial and family stability in order to capture the money they would have spent on that for yourself.

Always gets a chuckle from me when investors purchase existing property and claim to be saviors, providing "much needed" housing stock.

It's like they turned up to an open home with the real estate agent and a bunch of prospective FHB in a mexican standoff because the vendor cannot drop their price, and the FHB cannot afford to buy. Deep money pockets investor comes along and turns it into a win-win, buying the property at the vendor's price using equity leverage and renting to one of the FHB.

Landlords also buy multi-unit existing property nzdan. These are multi income stream properties classed as investments

A new build, adding to NZ housing stock. Anything can be bought by an owner occupier.

Not sure i get your argument. You think that there should be no landlords? So what happens when you want to leave your parents house? You can't afford to buy and there is no such thing as a rental any more..

I didn't say there should be no landlords - that's a strawman. But there should definitely be fewer.

And you are not adding to housing stock by buying a new build. It would have been built regardless of whether you bought it. You are cutting a first home buyer off from one of the most affordable options available to them, deposit wise.

You tell yourself whatever you like, but two facts are obvious: it is far too difficult to buy a first home, in large part because FHBs are competing with investors. You are making the problem worse.

So fewer landlords who own more homes?

If there is no demand to build houses then no houses get built.

You tell yourself whatever you like but it isn't that hard to buy a first home.

You tell yourself whatever you like but it isn't that hard to buy a first home

Ok, so you're delusional. There is no getting away from this fact: there are lots of places where you could invest your money. You chose the one place where doing so actively makes things worse for other people. You not only made that choice, you bragged about it - and now you are tying yourself in knots trying to justify that choice.

Here's something else you don't seem to understand: we don't need more landlords, and we don't need fewer landlords who own more homes. We need more people owning their own homes.

Well it's hard in that you have to work, not spend too much on wants and invest.

There are lots of places I could invest my money, and because I have a diverse portfolio I am invested in lots of different places.

how am I "tying myself in knots"?

Here is something you don't seem to understand. Landlords are required in society.

People like you should be required to shadow first home buyers for a month. Or at least meet with the people whose lives have been made significantly worse because of people like you. You look these people in the eye and tell them you're sorry that they now can't have kids, or had to move countries, or had to leave their hometowns and move away from their communities and families, or that they spend half their income on rent, their kids have had to move schools five times - but they just didn't 'work hard and invest and spend less money on takeaways' like you did (nothing to do with house prices increasing by hundreds of thousands in the last year). And that your 'diversified portfolio' is more important than any of those things.

The fact that there need to be some rental properties (which I never denied by the way) doesn't excuse what you did - if you bought in the last year, you would have been well aware of the fact that you aren't solving any problems, just adding to them. I don't know how you can sleep at night, to be honest. If you want to know why people think landlords are parasites, look in the mirror.

"People who work hard & are smart with their money are parasites." - al123

OK, so now you are reduced to making up quotes.

I, obviously, was a first home buyer and have friends who are trying to buy their own home. I have no need to shadow anyone.

can't have kids - they definitely can, but prudent to buy a home first.

or had to move countries - you don't have to move out of NZ to afford a home

or had to leave their hometowns - you don't have to move out of your hometown to afford a home

and move away from their communities and families - you don't have to move out of your hometown to afford a home

or that they spend half their income on rent - This is the problem, there is no need to spend that much on your rent. This is why financial literacy needs to be taught in school. On a minimum wage your take home pay is $667 /w, currently 600+ rooms to rent in Auckland between $150 and $200 /w.

their kids have had to move schools five times - see above.

I don't know why its such a hard concept to grasp but to make the biggest purchase of your life you do need to make some sacrifices.

It says a lot about your world view that you completely ignore the role of the State.

"isn't that hard to buy a first home" oh i see, you're just trolling.

You're not selling a product. You might be able to argue that you're providing a 'service', but that would only work if you were doing that into a genuinely free and open market where your clients have real alternatives. But because your prospective clients have little or no choice, and the market is not regulated then all you are doing is exploiting people who have little to no choice.

Do you mean the "little or no choice" like the examples I gave where you have over 600 options in Auckland??

What's the variations in rent across those options? My bet is they're all unaffordable, described as "market rents". That not a choice at all! It's a railroad to servitude.

All within the parameters that you provided. All similar to the rents that I paid. Choo Choo I was on that railroad and I'll be a landlord soon.

So you're gloating because your income meant you could afford the exorbitant rent and still save towards a house deposit? Most people are not in that position. Not even close! And your evident self entitlement and attitude of "do unto others, because it was done unto me" speaks volumes about your character.

Yeah notoriously high wages in the retail sector.

"Self Entitlement is described to be someone who think they deserve everything without earning it. " So working hard, saving harder, prudent investing makes someone entitled, but someone who wants to be able to rent a room for $60 (as you have said) isn't entitled, they are a victim.

Is this opposites day?

Where did you get that definition? Try this one; " when a person truly convinces themselves they deserve to get whatever they want," or this one " a self-absorbed view of the world and little regard or empathy for their impact on others"

This is not about working harder or being prudent. It is about the effect and impact you have on others. As I said the way you are doing this causes harm. There is no way you can convince me it doesn't, and if you were half as smart as you claim you are, you'd figure it out for yourself too.

" when a person truly convinces themselves they deserve to get whatever they want," - Nope, you have to work hard to get what you want. Pretty obvious to see I believe that if you bothered to read any of my comments

" a self-absorbed view of the world and little regard or empathy for their impact on others" - Nope, again, if you read any of my comments you would have seen I have given what I believe is the best outcome for ALL even if it is adverse for me.

You on the other hand have said that you want to bring hardship on EVERYONE in the hopes that it helps renters.

So you have no qualms dismissing qualified Psychologists definitions in favour of your own. Pretty impressive self opinion you have.

And what I want does not need to bring harm to everyone but landlords, and banks who between them created the current mess. So I've never said that, it's just your interpretation. As for most who are losing their argument you twist peoples words, put a different meaning to them and throw them back. Not going to wash!

You gave psychologists definitions meanly to apply them to me and I showed how they didn't apply to me. Didn't dismiss those definitions at all. Maybe re-read the comment.

During the great depression house prices fell by 35%. You want to drop house prices by double that and you assume that nobody but landlords and banks would be affected?

YOU said you wanted to drop houses by 70%, that WOULD cause the greatest recession in living memory. Haven't twisted your worlds at all, just followed your "thought process" to it's logical conclusion.

House prices are significantly out of step with the rest of the economy. The consequences of such a reset need not be that bad because of the level of distortion. If it is worse it will be driven by the banks and the Government needs to hold them to account. As to a major recession, you're just fear mongering.

Got it, so as you're a soon to be landlord anything that would put your investment at risk would be devastating to the country and unacceptable. My answer is simple, the market is destroyed now and taking action to move it towards a 3x - 5x median multiple on price and rental yields 1%-2% above TD rates will be restoring it to health and a huge boon to the country as a whole. No doubt that would 'destroy' some landlords, and I have no qualms with that.

Once you jump onto the landlord bandwagon then what is good for ‘me’ is good for everyone don’t ya know?

What's good for everyone is stagnant house prices over the next 5-10 years. Something I would be very happy with. But that doesn't fit your narrative so just pretend I said "house prices should continue on their current trajectory and FHB's don't deserve to own property"

Agreed, let prices stagnate and wages catch up. It'll be a win for those who went out on a limb to purchase their first home, as wage increases will inflate the debt away, and a win for prospective FHB who will see wages start catching up with house prices.

Can't believe the BS here. What level would the median wage need to be for houses at the current prices to be at a level of 3 - 5 times those wages? Is that level realistic.? Not bloody likely! House prices need to fall dramatically, I suggest by as much as 70% or more!

$100,000.

10 years of no house price growth but wages increasing with inflation would get very, very close.

You forget that for $100k median wage, that level of inflation will have made NZ a third world country and everything else would be more expensive too. Likelihood of that happening? Close to nil!

2.5% inflation.

Wages generally do not rise with inflation for the majority of people. Don't you get that? Living standards have been driven down for at least the last 60 years because of this wee fact! 2.5% inflation will mean house prices will have grown out of sight anyway, unless the Government intervenes and regulates them to stop rising. But you'd squeal then!

"What's good for everyone is stagnant house prices over the next 5-10 years. Something I would be very happy with. " - Me

So you're also now the judge of what's better for everyone? Your arrogance is amazing! House prices need to fall by at least 70%, and rents severely regulated. Stagnant house prices are not a desirable outcome at all.

I have an opinion on what is best for everyone. You have an opinion on what you think is best for everyone. Except your opinion would demonstrably cause harm to everyone.

If you want a proper debate then stop throwing insults around.

crunch some numbers. It doesn't take much to figure out that everyone, really - everyone is better off when houses are much, much cheaper!

I have. The only way to do it without causing the next great depression is house price stagnation. Then house prices are cheaper in relation to wages. You are advocating a drop in house price of 70%, house prices dropped 35% in the great depression. A drop of 70% would be disastrous.

I'm holding the investment property long term and risks of a recession don't really worry me based on my industry but I understand you hate landlords irrationally so sure.

What you propose wouldn't "move it towards a 3x - 5x median multiple" It would cause a crippling recession to the whole country. FHB's still wouldn't be able to own a house because there would be no jobs and no income.

What's next? Fix all prices on everything? Eat the rich?

I think a crippling recession is a worthwhile price to pay. I don't want my children and grand children to be rent surfs. Anyway you can't make an omlet without breaking a few eggs.

Making an omlet without breaking a few eggs is exactly what investors/landlords expect. Government/RBNZ policy has basically been "let them eat omlet". But in reality there will be broken eggs. Its just they haven't been hatched yet.

Honestly that sounds about as reasonable as allowing the current charade to continue.

What's next? Fix all prices on everything? Eat the rich?

I have great respect for those that work hard and become top of their chosen fields, or those who build a successful business of their own. I have no issue with the rich. I have zero respect for the rentier class who seek to become rich off the hard work of everyday Kiwis who need a place to live. I wouldn't piss on a landlord if they were on fire.

So you go from living with your parents to owning your own home? Leave school and get a minimum wage job and buy a house for $20

Sounds like a plan champ.

Exactly. When I rented, I needed to rent. As a student and as a worker. Once I'd saved enough bikkies I bought an apartment, then a house, then a rental that I want to be my holiday house once I can afford that. The tenants I have needed a place to rent until they buy in a while. Supply and demand.

Those that would mess with supply and demand as drivers of a market, are asking for the mess to get worse.

Most of the numbers I have seen, unless you are a cash buyer, dont make any sense from a return perspective. 2 - 4% is accepted due to the perceived zero risk and sure thing capital gains. It already doesnt make sense, you cant eat your paper gains.

My piece of paper has earned $95,000 in 3 months... This market is horrible and needs change (but tanking the market and causing a recession as mentioned above is mad)

What is happening and has happened the last 20 years is mad.

Absolutely, the best thing that could happen now is stagnant house prices for the next 5-10 years. Anything else will be catastrophic. We are on a knifes edge I fear.

I agree, 5 years of near static level of house prices. Its happened before in my last Auckland place, prices pretty much did nothing for 5 years. The real problem is when they decide to go up they really move fast. House prices are not going to crash, they will just flatline.

"EARNED"!? Utter bullshit. It hasn't earned a solitary cent!. Without you doing a single thing, but because of others of a like mind, and without producing one cent of value to the country, any employment or additional economic activity the paper value may have increased. But that paper value means absolutely nothing until you sell the property for that much and bank the money, or go to the bank and borrow against it. And in both those instances the IRD should then be knocking on your door and taking tax off the profits you're gloating about and realising!

People who look at a GV or property website and feel self satisfied because these things tell them their property has appreciated in value are remarkably shallow thinkers who cannot see the obvious.

In 4 years my entry level house earned me a sizeable deposit for an upgrade into a 4 bed 2 bath on 1/4 acre in a desirable central location.

Huge congrats

A major recession, from a long term utilitarian view, is probably the best thing that could happen. But our culture is based upon denial and avoidance of pain, regardless of the long term benefits of addressing real issues in an open/front on manner. Instead we prefer to sweep them under the carpet and tell each other how great things are.

Did we vote labour to power in last two elections or we voted in inflation and capitalism?

I wonder what promises by the politicians? All lies but then what else can we expect.

Political powers are less influential than long term financial/economic momentum. No political force can save us from what’s been created over the last 30 years or so - if the aim is social and economic stability. Our current settings, communicated to the people as being implemented to maintain economic stability, are actually destroying social and economic stability. A truely free market would resolve this mess, but most asset owning people won’t accept pain from the risk they should be responsible for.

I think this could result in a repeat of the 1930’s and the rise of dangerous leaders who promise to save the poor or disheartened from the economic misery that has been forced upon them. That is a very real possibility if western governments and central banks continue to walk the path they have, and appear determined to continue to do so.

That's true. We're still living with the consequences of John Key's decision to slash healthcare and other critical infrastructure spending.

The impact of Labour's excessive borrowing and wasteful spending during the pandemic won't take full effect until a few years after they are voted out of power.

Yes I though back around 2013 we still had the option of choosing our destiny as a country. No more. We are now slaves to the debt hell that we’ve created.

you mean his decision to tackle the structural deficit and debt he inherited -- and place NZ in a bloody strong financial position which this government has already sqaundered -- 60 b for covid = no ICU beds -- no ICU nurses - NO healthcare improvements

it took 8 years of sound fiscal management to undue the previous labour financial turd -- this one will take decades

ps --$$70 a week rent rise $15 benefit -- Jacinda really has looked after landlords and the asset classes rather well

John Key?

Sound financial management like selling off power stations for some reason that he couldn't clearly explain?

And his biggest regret? Something profound right? Nope it was not changing the flag...

What sets the price at the bottom end of the housing market? The rent that poor people can afford to pay, which is basically the amount that Government is willing to subsidise accommodation for beneficiaries and the very low paid.

What sets the price at the top end of the housing market? The most that the wealthy top decile can afford to pay to live in nice houses in suburbs without any poor people. The top end of the market has spiraled up in the last couple of years - dragging the rest with it - because of low interest rates and the feedback loop between house prices and the level of equity that people have in their homes.

Once we accept these two facts, we might be able to forge a plan to do something about house prices.

Governments should immediately remove all accommodation supplements paid on rental properties. It will be the landlords who complain more than those renting. Yet they also like to call their tenants losers who don’t know how to ‘get ahead’.

So your plan is to have all the poor people turned out on the street, hmm progressive indeed.

I have had many circumstances where no one was willing to rent the apartment I lowered the price to meet the market.

You just said this, in this comment thread. Do you really think all those landlords would just turn those people out on the street and leave their properties untenanted, or would they meet the market (as you are willing to, being an astute investor)?

With Labour importing more demand (150,000 next year) and with people already sleeping in garages I am pretty sure demand is not going anywhere, it will just be a (more) crippling share of their income.

Having said that if my property is over-priced in the market I would lower the price as I said. While we have more demand than supply the price for rent will be slow to come down.

It would get right to the core of the problem - and as I say, look who will make the most noise over it - landlords not the rent payer.

Do you know that for sure ? Nope! That's your bias speaking

Evidence is who that is triggered by the comment

I am just replying to you so maybe consider again who was triggered. Have fun

The central bankers have only one trick to deal with the situation they have created and it won't go well for anybody holding cash.

Dump your dollars.

As soon as you are paid, put whatever you have spare into shares, crypto, commodities anything that Adrian Orr and his ilk can't get their grubby little hands on.

Diversify. But DO NOT hold cash.

Pretty much sums it up. Convert what ever fiat tokens you have into something real. Keep just enough in the bank to pay your expenses. Use it or lose it.

Diversify. But DO NOT hold cash.

Gold? But JP Morgan is manipulating the price beyond recognition.

Maybe silver is the way to go...You know, being cheaper is should be less manipulatable....and it is totally a harder asset than gold. /s

Maybe silver is the way to go...

I have exposure to both silver and gold. My silver has performed reasonably well since buying in 2019. Owned gold since mid-2000s. Bit over it to be frank.

Both Gold and Silver should have done well in this environment. They still remain a hedge against fiat devaluation I think. I don't think it's a silly idea to have a percentage in ypur portfolio.

Well said. Diversify away from cash, as much as you can, but at the same time be also extremely wary of over-inflated assets such as NZ housing, which is now a total Ponzi.

We had all the renters on here telling everyone that rent couldn’t go up anymore and if it was raised they’d simply move.

Meanwhile…

Rents can go up more and they will. You have no control as a renter you pay up or move. Problem is you have to live somewhere. The current trend will continue and the bottom end will get squeezed even harder. The rich get richer its not changing anytime soon, not until the pitchforks come out.

I think it will turn, the only thing stopping it turning is the lunacy of Labour's immigration policy, adding 150,000 people to the population next year will ensure demand for rentals stays very high.

The pitchforks may come out but any student of history will know that the only revolution that worked out ok was the USA and even that is debatable given its current state.

The French would take that statement as a declaration of war.

My rent has been the same for 2 years, landlord has just told me another year with no change.

My business leases a warehouse, 2 yearly review, landlord didn't put the rent up, and he has 2 years to wait for another go at it.

Im sure Im not the only one.

For many they might not have moved but it doesn't mean thing things in their life aren't being shifted, like the ability to save for a house and have a family one day.

Not quite so simple really.... I have a story about two tenants who were neighbours, one that succeeded and one that didnt even though that ones rent was cheaper.

Good to see the numbers going up bigger in the smaller places. Not so good if you're a tennant, however. Best place for tennants in the last year is Wellington & Dunedin. One's full of politicians & the other full of students & between the two of them they couldn't organise a bar-bee-que. Well, maybe they could the que part.

Inflation is in top gear and our govt is saying it's transitionary.

Has anyone seen a scenario where the landlord comes back to the tenant and said from next week the rent is reduced by $70 or a restaurant have said the dish is $3 less than what you have paid yesterday?

It is transitionary no matter what it does because thats how its defined. It can rocket up but eventually the figures drop back closer to zero because its looking at change over a short period of time and not years and years. Its like the whole CPI which is a total crock to start with. Its all fudged so badly its meaningless. Bottom line is you know how its affecting you personally and yes prices go up but seldom go down or are very slow to go down.

The cause may be transitory, but the effects are not.

Inflation is a ratchet that only moves prices in one direction.

NZ has a big problem with inconsistent tax rules.

A landlord that has owned a rental property for a number of years has a completely different set of circumstances to a landlord that bought a property in the last few months

If you spent $1 million on a rental property a month ago it is reasonable to expect that you would want a gross yield of say 4% or $40k rent per year ie $770 per week. This landlord cannot deduct interest on an $800k loan. At a 4% interest rate this is $32k that cannot now be deducted & other expenses before tax such as accounting, rates, insurance & maintenance could easily be $8k making net cash flow before tax $0.

The tax owing is not $0 but your marginal tax rate x $32k - say 0.33 x $32k = $10k.

So in this example there is cash flow loss of $10k for the year.

In addition the outlook for capital gains on house prices over the next couple of years is likely to be less than zero, so in the short-term this property investor will be forced to stay afloat by increasing rent to cover the $10k tax bill. If the rental property is sold within 10 years tax will be payable on any capital gains.

Compare this scenario to the investor that has no mortgage on their rental property & has owned it for 5 years.

12 months ago the rental property was worth $770k & in this last year has increased by say 30% to $1 million & is sitting on a paper gain of $230k tax free. The investor could sell & invest in shares with an expected 4% return or continue to get a 4% gross yield of $40k rent per year ie $770 per week. One year ago rent would have been 4% x $770k = $30.8k or $592 per week.

The rent increase required to keep a 4% gross yield is now 30%.

As there is no mortgage cashflow is 40k rent less $8k expenses = $32k

Tax payable is 0.33 x $32k = $10k so net cash flow is $22k plus a $230k tax free paper gain over the last 12 months. In addition no capital gain tax is payable if this investor sells at any point in the future. This investor can keep improving their rentals for tax free capital gains but the recent investor that sells within 10 years will have to pay tax on any capital gains.

In both these scenarios the investors are providing one rental property but one is sitting on excessive tax free gains. Both investors cannot expect any capital gains in the future. Due to excessive house price inflation & increased healthy homes costs rents may not increase 30% this year but the pressure will be on to recover diminishing gross yields in the next few years.

‘The government’s interest deductibility rules have created 2 classes of rental property owner. One class will go broke & the other class will do very well as the supply of private rental properties diminishes significantly over the next few years.

The decrease in private rental supply will be a disaster for the government as many renters will be forced into emergency accommodation while others will be forced into a bidding war for the reduced supply of rentals.

I predict this dire situation for renters will be a key election issue. Labour’s interventions to get rid rental property investors only hurts renters & recent rental property owners.

Unintended consequences much? Whocouldanoed?

Par for the course for this sorry crew.

A very good post and example of what happens when you get emotionally driven policies that ignore the advice of people such as the IRD.

But this government thinks it knows best on everything whether it be taxation, water reforms or border restrictions, they always know better than the experts.

Where do the houses go if the supply of rentals diminish? Will the investors dismantle the dwelling and sell the materials to a building materials recycler?

As private rental supply diminishes there is an increase in owner occupied homes. This change doesn’t help those that cannot afford to buy a house ie renters. In other words owner occupiers are advantaged by the change & renters (our most vulnerable) are disadvantaged.

If there is an increase of owner occupied homes, then it must be mostly ex-renters buying them to live in. Which is pretty hard to argue is not good thing.

If house prices rise significantly then it follows that rents will follow. This hurts first home buyers saving for a deposit even more. Kiwibuild could have helped but there is only a single Kiwibuild dwelling left on the Kiwibuild website and it is a shoebox apartment for half a million lol

The Government's failure with Kiwibuid is typical of a socialist government that has no idea whatsoever of how a market operates, and no idea whatsoever of what it means to run a business. These are just a bunch of ideologically driven incompetent clowns, and most of them have never run a business, not for a single day. The irony is that the result of their incompetence has mostly damaged the very social classes they were supposed to represent. Their luck so far is that the opposition has been an utter shamble.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.