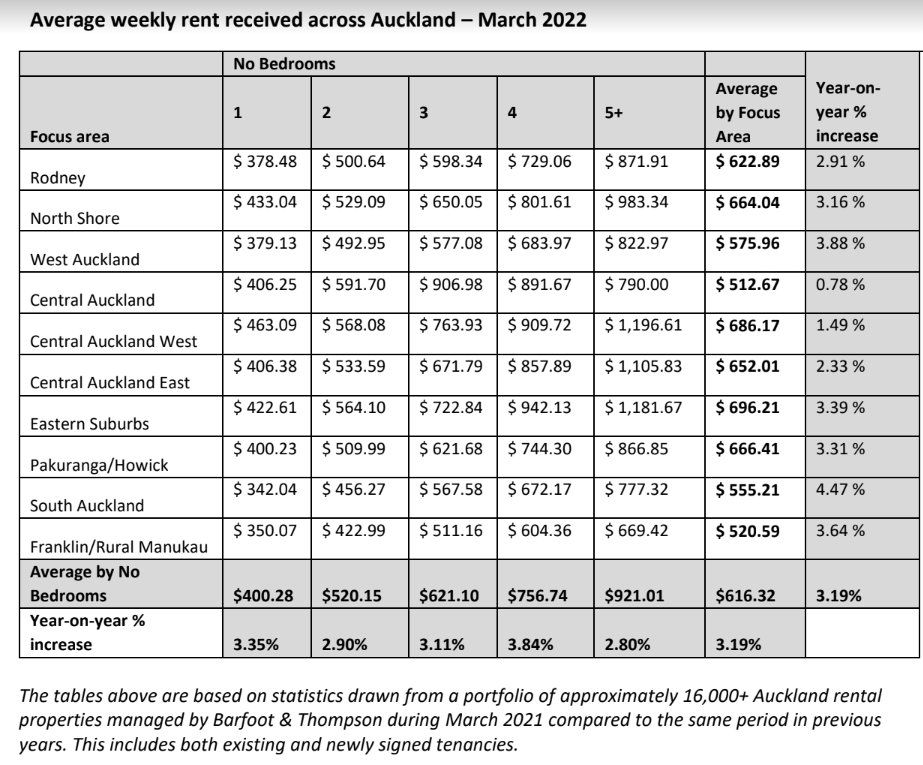

The average rent for residential properties in Auckland increased by 3.19% over the 12 months to the end of March, according to real estate agency Barfoot & Thompson.

Barfoots is the largest real estate agency in the Auckland region, managing more than 16,000 residential rental properties on behalf of their owners.

At the end of March this year the average rent charged across all of those properties was $616.32 a week, up 3.19% (+$19.05) compared to a year earlier.

Larger properties had both the highest and lowest rate of rental growth (measured by number of bedrooms), with average rents of properties with five or more bedrooms increasing by 2.80% in the 12 months to the end of March while rents for four bedroom properties were up by 3.84% over the same period.

Three bedroom homes across all locations increased by 3.11% and two bedroom homes by 2.90%.

Central Auckland had the lowest average rent at $512.67 a week and also the lowest annual increase at 0.78%.

That was probably because the district includes the CBD which has thousands of small apartments popular with overseas students, and that market has been badly affected by recent border restrictions.

South Auckland had the highest rate of increase, with average rents there increasing by 4.47% (+$23.76) to $555.21 a week over the 12 months to the end of March.

The table below shows the average rates of rental increase analysed by district and number of bedrooms.

"This movement in rental prices makes the first quarter of 2022 one of the higher quarters in recent years, but still measured in proportion to the 5% and 6% increases recorded between 2014 and 2017," Barfoot & Thompson director Kiri Barfoot said.

The comment stream on this story is now closed.

Average Rents on Residential Rental Properties Managed by Barfoot & Thompson

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

122 Comments

Rent increase of 3.2%, is it comparable to the CPI. Or ought to be measured with a growth of wages.

IMHO rentals in South Auckland, that were in stock, are being listed for sale.

It's a component of CPI. Generally though with tradable inflation so high Reserve Banks would prefer non-tradable inflation (likes rent) to be lower to offset that effect.

More properties up for sale meaning tighter vacancy rates as tenants get forced out. Home owners are winning with their fixed rate mortgages so that they can avoid all the rental spikes all together. Good thing the majority of mortgagors are fixed - property crash avoided.

Ouch, just another factor that renters fail to consider vs buying a house. 3% seems pretty normal on just about everything from your power to your mobile bill that just went up last month as well. 3% compounding, work that out in 25 years time.

~3% cost to rent increase versus a ~100% cost of debt increase..... I know which one I would prefer....

Also, cost to rent is waaay lower now than buying (assuming 20% deposit). Mortgage at current rates on the house I live in would be around $1100 per week. Add insurance, rates etc. and it's around $1200-1300 for a 2 beddie in the East Coast Bays.

You can rent a really nice 4 or 5 br modern house in the same area for that money.

Yes you are winning .... not. As carlos said above, look at the longterm and where it will be

Or for FHBs who purchased last year, the $10,000 in capital value that their house lost last week as prices fall, compared to the $500 paid if renting.

Just another consideration eh Carlos.

Just make sure you ignore the previous 100+ months when the house gained in value and your argument stands up IO.

Absolutely - 100% correct Yvil. So now the shoe is on the other foot, is it ok if I use the property spruikers argument against themselves?

It's not about shoes and feet IO, it's about whether people needing a roof over their heads will be better off renting or owning over the long term being their lifetime, therefore extrapolating data over a few months is irrelevant, what matters to them, is where they will be in 5, 10, 20 & 30 years time.

So just to be clear, because houses were going up by $1000 a week for the last 10 years...buying was superior than renting.

But because house prices might now be falling $10,000 a week (i.e. a 10% drop over average priced home), for the last few months, renting at present isn't superior than buying if considered from the FHB perspective (i.e. the person who needs to 'make a financial decision').

Which way around do you want it?

Are we talking about these issues from the perspective of the FHB of 2022 or you personally and what has worked well for you?

I sort of think both you and Yvil are right.

On the one hand, my advice to most FHB's would be not to touch housing with a barge pole in 2022, unless they could get a really good deal (at least 25% below November 2021- type prices). You most certainly don't want to be getting deep in to negative equity at the start of your home-owning life, if you can avoid it.

Generally speaking, look to 2023 as the time to buy. There's a strong chance prices will be down at least 20% from their peak by mid 2023, and it's also quite likely that interest rates will be coming down again by then.

Save very hard between now and mid 2023, to build your deposit as high as it possibly can be.

Agreed, mid 2023 might be an economic depression and this would be the best time to have cash.

Also agreed.

"Just make sure you ignore the previous 100+ months when the house gained in value and your argument stands up IO"

So better to rent or buy at present?

You like to argue IO, huh? You also like to misrepresent (for example by adding "at present" in your question above) I'll make it as simple and straightforward as I can.

The real topic of discussion was renting vs buying. No one buys a house to live in for only "now". It's a life-time decision and in my view, owning your own home, is far better than renting, but you're of course allowed to disagree

If I was a genuine FHB, I would spend all my time looking at houses in the ares and price range I'm interested in now, with no hurry at all to buy. When I come across a house that ticks all my boxes at a great price, I would buy it. HM said something similar, so yes I agree with him.

Lol - so you do agree then that now isn't a good time to buy? (which you appear to disagree with when you first replied to my comment above and then tell other people they like to argue...) Again I don't understand the hypocrisy in many of your statements....hence I like to clarify what your view is when you challenge me...and then you get all defensive when I call you out on the paradox of many of the things you say.

IO, you base your argument on, I quote you: "house prices might now be falling $10,000 a week (i.e. a 10% drop over average priced home)"

A house prices drop of $10'000/week = a drop of $520'000 pa, you then also say it's a 10% drop over average priced home, this would make your "average priced home" $5'200'000.

I will let others judge how credible you are.

- $700 per week, inflated at 3% p.a. over 30 years = $1,731,745.

- $800k mortgage @ 6% over 30 years = $1,725,523

Assume increase of mortgage payments 3% every 2 years (2 year fix/refinance) mortgage goes from 30 to 22 years. Interest of $725k, principle $800k = $1,525,000. $200k less than the renter over 30 years, despite having higher repayments for the first 15 years.

30 years is a long horizon so I'm sure people will easily pick holes at my comparison i.e. rates and insurance. But $200k saving over 22 years = $9k p.a.. Then the next 8 years is mortgage free so $1100 per week = $460k (the rent hit $1100 per week by year 15).

I don't think it's 'picking holes' to point out that rates and insurance (not to mention maintenance) need to be taken into account. They are unavoidable costs that should factor in to any cost comparison.

They're factored into the $9k of savings per year dollar cost averaged and then the $400k plus with no mortgage outgoings at the end.

OK, but why do you think 9K of rates, maintenance and insurance is a reasonable number? Many people would be paying close to that now just on rates and insurance. Do you expect their to be no inflation on rates and insurance in the next 30 years? Did you factor in the returns on the initial 200k over 30 years (which presumably the house buyers used as a deposit and the non home owners invested). Did you factor in the non home owners investing the rates/insurance/maintenance money? Why did you assume $700 rental and 1mil house price? The point is, it's not as simple a calculation as you make out.

Honestly, I just copy and pasted my reply on this article where CourtJester said a $1m house in his area would cost $600-$700 per week to rent. https://www.interest.co.nz/banking/115696/westpac-nz-interim-profit-fal…

Merely throwing numbers out there to show that home ownership is far from the money pit that people claim it to be. Sure, I could rent and invest the savings in the sharemarket and after 30 years have a nice pile of dosh. But by then how many houses would my child have lived in, how many changes in schools etc?

Renting also has the advantage of additional labour market flexibility: it is easier and significantly less costly to move to take up a better job. I'm still renting (though considering buying) and I have moved three times: each time to take up a significantly better paying job. For the sake of my kids I want more stability now, but it will likely come at a cost.

You kind of left the most important bit out Dan, you have a $2 million dollar house at the end, renters have zilch.

Only true if rent > mortgage repayments + rates + insurance + maintenance

There arent a lot of markets that holds true.

Assuming the renter has invested or at least saved the difference, they have that at the end. Plus returns. Plus the 20% deposit they didnt put in. It's not as simple as you make out.

This is true in a clinical sense, however generally it also requires a huge amount of financial discipline.

precisely - a like for like comparison with the person that bought and the person that rented. When you're talking outcomes, the starting point needs to be equivalent. As a few commentators here have said.

It is disingenuous to do anything else.

Well, that's only true if you are starting from an unequal comparison - the renters don't have the deposit. But if you start out with an equal comparison - i.e., two households, both with (say) 150k, one decides to buy a house and the other decides to invest it, then it's not likely either will end up with zilch.

Look, I'm not saying it's a bad idea to buy a house, or anything like that. I just don't think it is useful to present comparisons which don't take relevant facts into account. Like the post above which ignores rates and insurance and maintenance. And that assumes that the choice is between spending $X on rental and spending the same amount on a mortgage. It may be that you can rent a similar quality house for less than you could buy it for and invest the difference. Good quality rent vs buy comparison calculators take this into account. It does no one any good to completely ignore these things in favour of simplistic pronouncements like the ones being made on this thread.

NZ Dan, com'on, you're smarter than that, apart from pride of ownership, security of tenure, freedom to change the house, the owner ends up with a nice mortgage free house, the renter has……… (fill in the blank)

Or maybe I should put it into numbers since you seem to like numbers. Let's say that the house has only quadrupled in value in 30 years (instead of gone up the usual 8 x). So the owner has a $4 Mill house mortgage free, that's $133'000 gain every single year for 30 years! and no tax paid at all. Just to keep up, the renter has to earn $200'000 pa, for 30 years… and he has to work! Very unfair!

So past performance is indicative of future performance - is that your point?

https://taylorpearson.cdnoptimus.com/wp-content/uploads/2035/08/Picture…

{kind=link}

Agree - past performance is not indicative of future performance, and I think gains in house prices will be much less in the next 20 years compared to the last 20 years.

But even with much milder future house price growth, having a house mortgage free at retirement is a pretty good thing.

Thank you for getting it HM, that is the simple point I'm making

strawman argument. It is not possible for values to continue in the trajectory they have been without a massive change to wages. Your argument also seems to assume the mortgage payment is the same as rent? Where can someone buy a median priced house with a 20% deposit and be the same as the median rent?

The numbers that NZDan put in here are intentionally misleading. Servicing costs have gone up a whole lot more than 3%.

The calculation from a purely financial view is interest paid + rates + insurance + maintenance v rent. Yes, you're left with an asset, but that is also true if someone was to invest the difference above into any other asset class, say shares, or a managed fund etc.

EG. On a $960m loan (80% on $1.2m property), if we assume it now averages 6% interest over 30 years, it's $1.1m in interest alone. Start with $7k in annual rates, insurance and maintenance, adjusted for inflation of 3% = $330k over 30 years. So, c. $1.43m in interest and servicing costs = $917 p/w avg. Now, rent at median now = $620p/w, adjust for 3% inflation = $1.53m over 30 years = $980 p/w... not a massive difference.

Now, remember a P&I loan has more I and less P in the beginning, so assuming that was invested, the compounding return may well outperform housing - especially if housing stalls or retreats. There's way more moving parts than most spruikers want to admit.

I worked on 6% interest rates. That being said I gave the renting scenario a bit of a handicap by only increasing mortgage payments by 3% every 2 years, if it were 3% annually it'll look vastly different again.

I didn't assume the mortgage payment = rent. Rent of $700 per week vs mortgage at $1100.

But you're correct, one could invest the first 15 years of savings by renting into the share market.

I didn't assume the mortgage payment = rent. Rent of $700 per week vs mortgage at $1100.

Sure, but you need to justify these figures. If the rented $700 a week a house is significantly better in quality or location than the mortgaged $1100 a week house, then it's not a like for like comparison. The average house price is about $1mil, but the average rental price is closer to $600 than $700. Why not assume a $600 a week rental and an investment the $500 per week difference in something other than housing? There are good calculators online that actually take these things into account, like this one: https://www.nytimes.com/interactive/2014/upshot/buy-rent-calculator.html

I copy and pasted my reply on this article where CourtJester said a $1m house in his area would cost $600-$700 per week to rent. https://www.interest.co.nz/banking/115696/westpac-nz-interim-profit-fal…

- Understand what you're saying, the NZX50 has averaged 8.83% p.a. since 1993 (no risk?), if you invest $500 per week then by year 30 you'll have $3.5m (or $4.5m if you increase investments by 3% p.a.)

- If the house only increases by 3% p.a. then by year 30 it'll be worth $2.4m, you'll have paid $1.5m on the mortgage plus rates and insurance of probably $400k.

$4.5m will buy the house and $2m in the bank after 30 years. By year 21 you could buy the equivalent house with cash, just in time for your kids to leave the rental. Or you keep investing and end up with $7.3m by 65 thanks to compounding growth. That is if a) 8.83% is guaranteed and b) living to/past 65 is guaranteed.

Or one could spend the money in these 15 first years on a few trips, a better car, nice clothes, a few more beers, coffees etc… for such is real life. Maybe the most beautiful and potent quality of a mortgage is its obligation to save! Yep indeed every month as the mortgagor invariably pays the mortgage, he/she repays a few $1000 in principal, thus getting a few $1000 richer (tax free) until… one day, he/she has a fully paid off house. No amount of rent calculation can ever come close

I find this a piss poor argument.

Why? I think he’s generally right, especially around the ‘compulsory saving’ bit.

it sounds nice in theory to rent and invest a tonne load in other things , but is easier said than done.

conversely, it’s easier said than done buying, now. The barriers to home home ownership are so much higher. But if you can buy, I think it’s worth it. The problem is how ridiculously hard that has become for many / most FHBs who can’t benefit from ‘the bank of mum and dad’…

I get what people are saying about compound growth in investments. The NZX50 averaged 8.83% since 1993 (past performance disclaimer etc). Investing the difference between rent and the mortgage payments could over time see massive gains. But what timescale are we talking?

- If you started at age 30, invested $500 per week, increasing by 3% each year and assuming 8.83% you'll have $7.3 million by age 65. Awesome!

- If a $1m house increases at 3% p.a, by year 21 the above investment will have enough fruit to buy that $1m house (now $1.8 million).

- Do you keep renting and investing, or do you buy the house?

Everyone is different. Me personally, I'd rather not wait 15 - 20 years (or never) before I can provide a stable home and school environment for my child.

So what's your better counter argument agnostium?

If you're going to go down that rabbit hole, then dont forget that the homeowner will likely do continual top ups to also fund the trips, car, cloths, beer, coffee. It's a demonstrable fact as is in fact the whole idea behind movements in the OCR.

P

And in fact the whole "wealth effect" idea was based on the idea that homeowners would spend more, including borrowing money to spend more, on the trips, clothes, cars, beers, coffee.

That is how the "wealth effect" worked. By luring homeowners into a sense of security so they would spend more. "Our house has gone up in value Gladys, let's buy a spa pool".

The statistics are sobering. Homeowners are far deeper in debt than they were before covid hit. The "wealth effect" made many poorer.

MisterB, Fitz, I'm just trying to help you guys but it seems you are more interested in arguing, in being right rather than being better off. That's your choice of course but then don't complain about others who have taken advice and improved their own lives.

Oh how wonderful of you. All I am doing is pointing out the foundation of your argument is flawed and the implication that housing is the only way for you to be better off is the entire mindset that got NZ into this ridiculous situation.

BTW, yes, I am a home owner.

But you've forgotten the super obvious bit that mortgage payments have increased by a lot more than 3%, and that's not coming off the principle buddy.

My calculations have already factored in that increase. Could there be future increases? Of course!

I can rent a shitty old state house in Auckland Central for $750 pw - to buy it would cost ~$2 mil - add a 1 to the front of your mortgage and then redo your sums.

Do you actually think that renters who have the choice (aka money) to buy plan on renting for the next 25 years?

Auckland rents up 3% in the last year.

OCR up 400% in the last year.

Sooo.... Less than inflation, and nowhere near as bad as landlords have been threatening?

Be interesting if mortgage rates keep rises faster than what people can afford to pay in rents.

It will be another downward pressure on home prices as the cash flows just won't stack up (if they ever did before prices started falling...)

Not everything rises in parallel. Interest deductability removal is only just being phased in, as will be interest rate rises. So you'd anticipate rent increases to come on in force over the next 12-24 months.

I wouldn’t anticipate that landlords will be able to raise rents very much at all going forward. In fact I anticipate rental decreases. In Auckland at least, where I now live, the number of rentals on TradeMe is way higher than usual. My old landlord put our place on the rental market in early April. It’s quite a nice place and priced well, but it’s still hasn’t been rented. I expect we will see much more of this as unsold homes go to rent, and people struggling with the high cost of living move out of Auckland, or move in with others.

I think it’s going to take a while for many landlords and speculators to really get to grips with what is happening. The party for them is well and truly over, thankfully.

Auckland may be in a special place, most places outside Auckland have pretty severe rental shortages. And it's rental market is highly affected by migration, and the borders have been shut for 2 years.

I think there are too many downward pressures countering the impact of interest deductibility on rents. Tenants simply can't pay more, and there is more supply anyway, so landlords will have to absorb increasing holding costs. That's a risk that should have been considered when planning an investment portfolio.

I was booted out of a property in July 2021 as owner wanted to sell. Had taken on the lease for 950/week in July of 2020 (in Parnell). The owner failed to sell, tried to list for $1050.. dropped to $995 and now it is back to $950 - the 2020 price. This is also with the house being done up for sale with new heat pumps.

It made me wonder - if all these properties with inflated rents were put back on the market for rent today, would they actually be tenanted at these prices? Or is it a case of landlords just taking advantage of the fact that it is a hassle to move. I suspect the latter..

Sorry to hear that, tenancy laws in NZ need to give tenants much better security of tenure

I don't agree. Have a read of the current rights (https://www.tenancy.govt.nz/starting-a-tenancy/new-to-tenancy/key-right…)

The only way a tenant can be moved on is if the landlord is going to sell the property. Remove this final privilege over their own asset and you will end up with super-slums as the existing housing rental stock rots where it stands.

just use the old "family" wants to move back in - of course you might get stung if anyone actually follows up on it but who does and what are the consequences?

Interesting, on the property investors website page general chat is that Auckland (talking mainly about the north shore) is getting harder to rent with places sitting empty for several weeks/months. Suggestions that prices need to come down to get tenants. Maybe it's just one segment of the market or maybe the price drops haven't come through yet as people are still holding out for higher rents.

Family friend I know had an empty property they decided to rent recently as the costs were rising and the math didn't add up.

The only interested tenant offered to move in in 8 weeks time and pay $150 under the listed price.

Lots of denial around at the moment

Yes I think its quite possible that we are now in the denial phase of a boom/bust cycle. People are almost in a point of disbelief of what might be unfolding around them.

I am not sure anyone with experience doubts that we are in bust phase, but the scale of the bust is less certain.

My view is that it is going to be significant and I have made moves to secure myself (to the degree I can) from this risk. I am not sure about the percentage decrease as costs and inflation are still on the rise as an offset.

It is also likely to go across multiple years, the inflation-depression cycle will push into mid-24 I suspect. Tough times ahead.

I've been following townhouses for rent, currently sitting at 461 in Auckland.

When I first started monitoring 7-8 weeks ago, was circa 420-430, so it's not a large increase in supply. I expected it to be a bit higher, with all the new build townhouses being finished.

I still think it will rise to the late 400's over the next month or two, but time will tell.

https://www.trademe.co.nz/a/property/residential/rent/auckland/search?p…

I might start monitoring *units* for rent. Potentially new build townhouses are getting snaffled relatively quickly, and units are moving more slowly as a result.

Talking to a young lady today who has been put in emergency housing.$70 a week for a 1 bedroom hotel room.

Unfortunately she shares it with her boyfriend,her sister and 6 month old baby,

I see nothing but trouble ahead for her and many others in the same situation.

$70 a week from her benefit maybe --- but more like $2000 a week to the providers who charge MSD $250-$300 a night for hotel rooms

$70 a week -- hell many commuters would rent that to save double in fuel costs comign in every day to work !

Without doing the math, I'm almost certain that the removal of tax relief for landlords would more than cover the cost of emergency housing?

Imagine that, the tax of investment property paying for the social problems it has caused!

lol these sort of posts are good humour thank you. Of course if you actually, you know, did the math, you would see that without the charity of the accommodation benefit there would be 100,000's of homeless. Winning!

Would the houses be demolished?

No that would be unprofitable. This is the situation that happened with Rent controls in NY in the 80's. These buildings were left to rot and did. Lifts stopped working, water was touch and go. Incidentally crime and in particular violent crime was at it's highest in NY in this period.

So, the investor who spend a good chunk of money buying an Auckland house, will leave it empty and service their loan how?

You said that without accom supplement, thousands would be homeless. But the houses exist now. All accom supplement essentially does is put money into landlords pocket and increase the rent in that area.

People need the accom supplement to afford the market rent. If this is removed they would be homeless. I agree markets would quickly move down and they would rent at a lower amount.

I am simply saying that those landlords trapped in the resulting negative equity would not be able to offload that property and therefore they would have to hold onto it - and they would most certainly not have any money to maintain it.

The accom supplement allowed the market distortion I grant you but the costs built up around it (most critically house price) are sunk, as would the landlord be.

They wouldnt be homeless, they would be renting at a lower rate. Market rent is driven by the ability to pay... just like house prices went up when credit was cheap.

It's a circular argument you've got there... and as for maintenance, they'd be a numpty if they didnt maintain their asset. Not to mention legislation that requires them to keep it healthy.

Irrelevant but I'll bite.

$31m a week spent on accommodation supplement for 360,000 people = ~$86 a week pp. Not sure that would put 100,000s of people out of a home but may force people to look for cheaper rentals (of which there are more and more by the day).

Ran the math on the above and yep, interest alone does not cover the emergency housing crisis. But debt of 1.279b at 5% is ~175k a day - that would go a long way to offset those falling off at the bottom. And with investing in property looking $175k less inviting per day once brightline rolls through, I'm not really sure we'll be seeing the same social issues we're seeing today, prices will be down and the pressures driving them up will not be the same.

I do find it amusing that the accommodation supplement is brought up as welfare or "charity", when we all know very well who pockets the change.

The landlords did not petition for this policy. But I do get your point, it is hardly helping those who receive it. Just a bad policy.

Correct KpNuts, there's no way a one-bedroom serviced motel unit would rent for $70/week anywhere in the country. $2'000 is steep but $1'000 not uncommon, Ngakui Gold, you should check your figures

I wrote a lengthy comment and deleted it. This, and many stories like it, does not bode well for the future of this country.

I hope everybody who has benefited from the pre2022 housing market welfare scheme is as happy as the neighbour they took everything from.

House prices are trending down now, so all the wealth theft is reversing.

Exactly - but remember they've done so in order to 'get ahead'.

The aim of the game is to turn thy neighbour into thy rent slave.

The golden rule no longer applies in modern society.

Huh? The golden rule still applies, "He who owns the gold, rules"

Jokes aside IO, it's a shame that you always view life as a competition where one has to lose in order for the other one to win. When one says they want to get ahead, as per your above post you immediately interpreted it as "that person is bad because he/she wants to get ahead AT OTHER PEOPLE'S EXPENSE", it would not cross your mind that they simply mean they would like to GET AHEAD IN LIFE, live a good, happy prosperous life and be able to provide fo their family. Try to look at the brighter side IO, there are far fewer "bad people" that you think, most of us do the best we can with what we know, to lead a good, happy life.

Society functions in an interdependent manner.

Assets are balanced with a liabilities.

Your personal million dollars of untaxed capital gains made in the housing market is now a million dollars of debt that someone else is carrying in the market (and may soon experience severe financial hardship as interest rates rise and prices fall).

So you have 'got ahead' at the expense of somebody else - the poor souls out there holding large sums of debt in a rising interest environment so that you could cream the capital gains of the last few decades. But you don't see that....because you have been conditioned by your personal experience in the housing market and assume that is how the world works for everyone.

https://th.bing.com/th/id/R.cb7022da6716c5a9aaa30ae68d6ea958?rik=FuHjKL…

To be fair and to avoid a rebuttal of absolute drivel, it is expected that the majority of debt money entering the market is larger than that of previous generations, this is inflation. The point is that the $1mil debt has a portion of debt above and beyond what could be considered affordable - may be shared between a FHB and several OO upsizing with debt, taking a portion of the gain. Either way any money gained above and beyond an affordable debt comes at a cost. That cost is compound interest on the unpaid principal of this portion over the life of the loan.

TLDR:

500k mortgage @5% over 21years at ~$750pw = $308k of interest

600k mortgage @5% over 29years at ~$750pw = $536k of interest

With 100k deposit, the cost of 600k house vs 700k house - $328k.

Can anybody see why this is such a problem for FHB yet??? Nobody is asking for a free lunch.

When I go to a shop to buy something, or to a restaurant to have a good meal, or share a few beers with mates at a pub, I pay the money and I come out happy. I don't dwell over who won and who lost, who screwed who over… I'm pretty sure, said shops, restaurants or bars who sold me their wares are happy too.

How do these experiences work out for you in your world of "in order for someone to win someone else has to lose"?

Not even remotely comparable as the supply of food and drink is not constrained in these environments.

Maybe a better analogy would be going to the only pub in town where there are only 20 beers and 5 meals to be had and you and you mates all outbid everyone else in the village. You all head home a bit tipsy and with full bellies and everyone else goes home hungry.

The next night the reserve price for the meals is what they sold for the night before.

I find it odd how you keep on going on about 'some has to win and someone else has to lose' when you view my comments.

Where is this coming from?

I don't see the world in that binary fashion....yet for some reason you think, I think, that.

Perhaps its something in your own paradigm that happens when you read my comments (i.e. something subconscious from your childhood to do with your Dad - and him not being a risk taker and your need to prove him wrong? And show that you can take risk and win?).

I'm about fair outcomes and financial and social stability going forward - and have no idea where this I win/you lose stuff is coming from. I have no interest in beating anyone - especially when it comes to housing as its such an important thing society wide...

Do you think that you have been winning or losing and how does that make you feel?

Totally agree.

Housing should not be about winning and losing, at all. Owning a house should be a realistic proposition for anyone with a reasonable amount of talent who works hard - without needing parental assistance.

That no longer applies, and it hasn't for quite a while.

"I have no idea where this I win/you lose stuff is coming from"

It comes from your own posts, such as:

"The aim of the game is to turn thy neighbour into thy rent slave."

"you have 'got ahead' at the expense of somebody else"

and many more from previous threads I can't be bothered searching for.

I love the cognitive dissonance here. We were screwed by fate, its not fair!! Time turns the market around... They are screwed by fate, they deserve it!!

The first were/are screwed by fate, the second are screwed by bad investment decisions.... Very different.

If you think that buying a house any time outside the last 12 months was a bad buying decision then I cannot help you.

Will those that bought within the last 12 months get punished yes, should they have known about the COVID supply shocks affecting inflation? Possibly. Should they have known Ukraine was about to be invaded cementing inflation in oil prices. No.

Fate has assuredly screwed them as much as it has screwed the young of this country who were simply born too late to get involved.

Fate... or the random walk of markets, which is a known phenomenon? Anyone leveraging for investment should understand markets, buyer beware. I do agree with you though, it sucks for genuine owner occupiers who purchased for a roof over their heads. But multiple-property investors need to own their risk, and the part that they have played in all of this mess.

I agree, but is there any investor on here claiming they should not have to own their own risk? Did I miss that?

Nope there isn't, just disgruntled non-investors

Those who beleive that the govt, or the RBNZ will/should jump in to save the day, again, somehow?

and who are these people?

Tell me what poor decisions have been made by the young New Zealander who turned 20 in 2022, and who wishes to own their own home? They now face some of the highest rent to income (and house price to income) ratio's anywhere in the world. The odds are truly stacked against them that they can ever afford their own home purely on their own salary. Should they have been born earlier? Should they have been born to richer parents?

Compare that to someone in their 50's who has chosen to use the home (that they were able to purchase on their own salary) as equity and has leveraged up to their eyeballs in debt to buy an overpriced rental, where the rent won't cover the mortgage payments.

One of these situations there is someone who was given options and choices and may have to pay the consequences of those decisions. The other was just born in the wrong decade.

I think a 20 year old should not be realistically thinking of buying a house but I get your point, as I have said in other posts young people are not able to get on the property ladder in NZ and that is the truth.

If there is someone in their 50's caught short by the return to normal rates of interest then they have done very poorly indeed I agree but this is unlikely. Those that will be smashed are the younger FHB's (90k over the last couple of years) who have no equity and the retired people who have a low income.

In the 2018 Census, home ownership rates tended to increase with age, until people reach their early 70s. Homeownership was most common for those aged 70 to 74 years, at 77.8 percent, followed by those aged 65 to 69 years, at 77.2 percent.

Interested in your opinion as to why a 20 year old should not be thinking about buying a house…?

Wow. OK. Not sure how to answer this, is it common somewhere for this to be the case? As far as I am aware housing is beyond the economic means of average 20 year old everywhere. Based on their average incomes not sure why they would conceive otherwise?

I think it’s very likely that it’s common for 20 year olds to be thinking about home ownership. Question was why should they not be thinking about it, as the comment was. Because it’s unaffordable?

Because it takes a few years of saving for a deposit and also getting a decent salary to be able to pay for the P&I. I don't think many 15 year olds started saving for a house so they can buy when they're 20 but if they did, well done!

“I think a 20 year old should not be realistically thinking of buying a house“

The planning/thinking/preparing. Surely 20 year olds everywhere are thinking about owning their own home, question was why should they not be?

so tahts $19 a week -- or way less than what the weekly petrol bill has gone up -- or way less than what groceries have gone up -- or building materials, in fact 3.19% --- well below the rises we have experienced in almost every other area of our lives --

As for one dynamic of the housing crisis -- if with mortgage servicing costs effectively doubling at intertest only, and capital gains retreating faster than Putin from Kyiv -- MAYBE just maybe -- those 30,000 empty houses in Auckland owned by investors both local and international -- will have to come onto the market as rentals or to buy -- and in one fell swoop end the housing crisis -- well at least the having a place to live aspect

It always amazed me --- that the government did not target the empty homes - just collecting gains but not even rented - as a number one target -- after all you dont have to consent anything , build anything and hey presto 30,000 new houses -- maybe a 5% levy on houses left empty for 6 months and not just a family home empty whilst overseas - would have served its purpose of putting those back into the housing stock and if not then make it 10%

Its hard to see how that would really hurt a Labour government -- in fact i think outside of a very very small number of kiwis who may own some of them properties -- -it would be a vote winner on all sides!

It's a shame that "Central Auckland" covers such a large area and maybe more to the point, such diverse property types. Both the most expensive suburbs in the country and the tiniest shoebox appartments fall under "Central Auckland". This distorts data for rents and property values to the point where it is totally meaningless.

Yes this is true. We have a relatively new 1 bed rented for $590 a week in central Auckland but as with all things this will change over time.

That seems very expensive unless its got a large living area, storage, and comes with car parks. We've got a 2 bedroom unit with a garden and a car park in Herne Bay for $580.

Good on you, that's under market, unless there is something wrong with it. Stay there, market rent for a 2 bedroom unit with garden and car park in Herne Bay is closer to $690

..and the lovely news for tax payers is that (depending on area/rent etc factors) in some cases the extra accommodation supplement is covering this increase entirely.

i.e rents goes up, no change for renter, but more $$$ for the landlord.

What a system!

Key had 9 years to sort this, the time to do it was in times of plenty. I have no faith in Labour doing anything...it was a job for National but Key squandered the opportunity.

Bad, bad John Key for not sorting this out over the last 5 years, shame on him

..i have no expectation of the socialists doing it. If not National then I guess ACT?

Point being that JK had a lot of public support, much of it from swingign voters. But he squandered it.

So yep, shame on him, a populist.

Yvil,

I am more traditionally a left-leaning voter, as I'm sure you will gather.

However, I voted for Key back in 2008. One of the reasons I did so, was his personal promise to me to sort the housing debacle out. I had email exchanges with him.

While his government did *some* good things, they didn't do nor achieve anywhere near enough over the 9 - yes 9! - years they were in power.

Agreed but surely you must look back at those days with envy now. In the past 5 years of Labour we have had a literal rocket sled of house prices, more than ever before. Ever.

Both are as bad as each other, but in different ways. Perhaps this current Labour government slightly worse.

Auckland rents up 3% in the last year.

OCR up 400% in the last year.

Wow I'm glad your not in control of my finances, you are totally clueless.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.