A significant gap is opening up in the residential property market, which could foreshadow a major property slump.

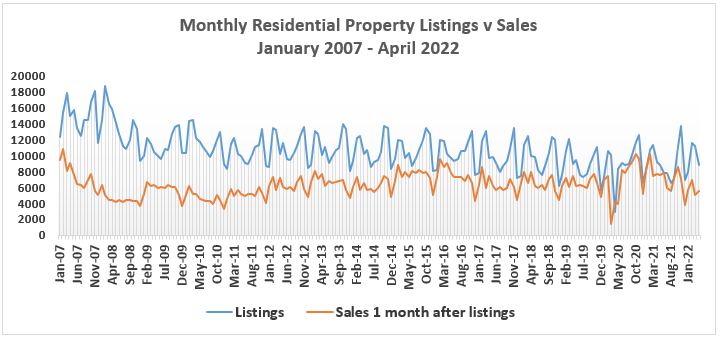

It's the gap between the number of properties listed for sale each month and the number that are selling.

Generally the smaller the gap the hotter the market, while a larger gap means the market is slower.

At the moment the gap is getting bigger and it's opening up surprisingly quickly, suggesting a major shift in the market is underway.

The graph below tracks the gap's progress over the last 14 years.

The top blue line shows the number of residential properties newly listed for sale each month on property website Realestate.co.nz.

The bottom orange line is the number of residential sales recorded each month by the Real Estate Institute of NZ.

The space in between is the gap.

The figures for sales have been moved forward by a month, ie, the April figures show the listings received in April but the sales achieved in May.

That's because most properties have a marketing campaign that lasts for about a month.

As you can see on the graph, there is an extremely close correlation between the two sets of numbers, with sales patterns following listing patterns very closely.

But what changes from month to month is the gap.

As the graph shows, it was at its biggest in 2008, which coincided with the Global Financial Crisis.

Then it slowly but steadily declined over the following few years until it started tightening dramatically in 2020 as the Reserve Bank started pumping cheap money into the banking system, which in turn led to a housing market frenzy.

In fact the gap didn't just tighten over that period, there were three months in 2021 (January, June and September) when the gap disappeared altogether because the number of sales exceeded the number of properties that were listed for sale the previous month.

But now the gap is back and it's growing.

It started opening up again in November last year, just as house prices peaked, and it's already sitting at about the same level it was in 2014.

While you can never be sure what path these things will take in the future, there's at least a reasonable chance that by the time we bid winter farewell, the gap will be big enough to safely drive a bus through it without touching the sides.

Maybe even a double decker.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

131 Comments

Let’s not call it a slump - how about “buyer opportunity zone”.

Pretty much. For every over leveraged investor, there's 3 that've been paying down debt and building up cash reserves.

History, never repeats.

There really isn't though.

When the LVRs were removed, it pulled a big chunk of investor demand forward.

You can clearly see the big spike in the mortgage debt charts. Almost anyone who wanted to leverage up and buy a rental property did so when the LVRs were removed and rates were super low.

The trouble with pulling demand forward is that it creates a demand gap at some future point. "Anyone" who wanted to buy a rental and was in a position to buy a rental, has done so already. Shot their load. Used up their dry powder. Filled their boots with debt.

There is no magical pool of buyers who sat patiently waiting while rates were low and lvrs were removed, and who are ready and willing to buy at current prices now that rates are higher and lvrs are back.

Anybody who still has dry powder left is smart enough to wait for prices to collapse before buying.

I have very little debt and a huge amount of equity, but at 55 banks may not 'let' me buy, I am not sure who the buyers are going to be..........

Quite a lot of people sold rentals, or have withheld from buying anything in the last 2 years. Its not been a particularly sane marketplace. Anyone with experience will be reluctant to keep buying in a FOMO market.

My point is that those people will NOT buy at the current prices.

Anyone who was smart enough to hold onto dry powder will be waiting for really big price drops before they buy.

Anyone who had the desire to buy high and leverage themselves to the eyeballs has done so already.

Your point sounded like you didn't think those people existed at all.

They exist. I am one of them. I will buy at a 50% discount, and flip the bird at my fool landlord.

That'll show them.

NZ has too many horrible old debt junkie, grasping slumlords. I hope every last one of them goes broke.

So many filthy old rentals, with their worn out carpets and dated kitchens. Their slumlord owners can charge a nose-bleed high "market" rent right now. But they are in for a rude awakening.

Man that is a position that's all over the map.

If you want nice new carpets and a new kitchen, you should rent or own a new house.

Some landlords are in a precarious lending position, but the majority won't be, you'll be competing with these people when prices drop 50%.

Your landlord can't be that mercenary, if you've been able to save for a deposit with which you can wait out the market with.

Nothing wrong with a dated condit8ion if it is still in reasonable serviceable condition it doesn't matter if it's not the current fashion.

Carpet - depends on how badly worn. It's not reasonable to expect all brand new latest fittings and fixtures all the time.

If your running a business you need to update your assets as the are worn out, or provide a service that your customers are looking for. If not then your business will probably fail. Moaning when depreciation is taken off buildings but never maintaining them in the first place...slumlords.

Things that are broken should be fixed (legally they also have to be fixed), but if they're older then that's up to the customer whether they want to pay their supplier more money to have things looking nice.

Why are there so many bad feelings and name calling of people that rent out houses? Not all landlords are bad people. I guess they are an easy target in the comments sections someone to blame for the housing market mess.

I agree, mostly generalisations, putting everyone in the same basket. And if you're a boomer, it's even worse. I hesitate to comment sometimes due to a few on here who post their hateful comments.

Probably the press and forum coverage of the worst offenders out there. The good ones get less coverage. Same with tenants.

Well said. Some people are perpetual moaners

Hey Fitzgerald, don't wait for 50% discount, just make sure you buy within the next 12 months- remember finally this entrenched inflation will eventually lift property values along with everything else.

I agree Fitzgerald. My wife and I having been looking at a number of properties to down-size. We are sitting back waiting as although we keep reading that prices are going down in Auckland, we are not seeing that yet in Canterbury. Realtors are still marketing homes "by negotiation" or "deadline sale", with no indication as to whether the sellers are being realistic. Frankly, with petrol prices the way they are at the moment, we are 'over' visiting open homes unless we know the price range of the house we want to visit.

Still a lot of offshore money leaking through I am sure, desperate to find a safe haven, notwithstanding AML and overseas buyer restrictions. Demand from overseas can be practically unlimited.

If National gets into power, they will open the door wide for overseas investors.

Selling the soul of NZ to foreigners.

And re-instate interest deductibility for investors... and roll back the brightline extension. Overpriced housing is the biggest problem NZ has, I can't understand how anyone could consider voting for them just when it looks like we might get a correction.

Clearly National is ruled by property investors, who so ever think to bring national in power, he must have owned more than one property portfolio.

Kiwis with one or no home should go for Labour because we don't have any other option.

Just thinking Labour or National may be a mistake. Labour have got nothing done except make the wealth divide worse and national will make it even worse because their MPs all own tons of properties.

My take is that we have tovote for smaller parties with decent policies and force the large ones into a coalition.. and to have to change their policies to get power.

Jacinda was far less able to mess stuff up with winston having a say

New Zealand has to pay its way in the World sum how. Sell the silver now and get top dollar

I'm ready to take advantage...Debt free & vulture fund ready.

... how quickly the sentiment in property has done a 180 and changed from FOMO , to FOOP ...

Which , just goes to show how fragile the system was , a house of cards , pumped up on cheap debt ...

Cheap debt, people coming back, some people not leaving, pandemic derived mania.

Itd be like what'd happen to someone's financial affairs if they won Lotto, had a divorce, and got diagnosed with a terminal illness, all at the same time.

What's this people coming back and people not leaving you speak of?

Tracking at 13k net loss of people in June. 2022 so far is a net loss of 33k.

- 2021 was net loss of 32k

- 2020 net loss of 49k

We had net migration of NZ citizens in 2020. Stats NZ seems to think so.

In the year ended January 2021, provisional net gains of 20,800 New Zealand citizens and 12,300 non-New Zealand citizens made up an overall estimated net migration gain of 33,200.

New Zealand citizens have driven monthly net migration gains since April 2020, and now they are driving annual net migration.

If people want to ignore other mitigating circumstances to NZs housing market in the last 24 months other than OCR behaviour that's on them I guess.

Customs Arrivals/Departures statistics is my source. 114k less people (and still climbing) is 114k less people that need housing. Citizens or not, people still need a roof over their heads.

Why not reference this int.co article from April this year?

Over the 12 months to the end of February this country had a net gain of just 2056 NZ citizens due to long-term migration (excluding short-term trips), down from 19,595 in the year to February 2021 and 6585 in the year to February 2020.

https://www.interest.co.nz/property/115307/fewer-expatriate-new-zealand…

114k less NZ Dan? Can you please provide source info?

https://www.customs.govt.nz/covid-19/more-information/passenger-arrival…

You'll need to subtract the departure numbers from the arrival numbers for each month. I've already done this, and arrived at the following:

- 2022 = 33,886 net loss (Jan to June)

- 2021 = 31,613 net loss

- 2020 = 48,788 net loss.

Total = 114,287.

Students, tourists and working-holiday visas. How many of the tourist bedrooms have become homes for beneficiaries. A figure for families would be more useful.

Yes, it's likely a good portion of those numbers are students, tourists and working-holiday visas. In 2017, we had 75k Student Visas and 150k temporary worker visas in the country. So a 114k loss is half that number.

As you say, depends on how many of those tourist beds are repurposed? How were rental properties now back in the market?

https://www.mbie.govt.nz/immigration-and-tourism/immigration/migration-…

You watch the net loss if Labour get another term.

Agreed! It'll be monstrous.

It's spelled phear, not fear, so that would make it POOP

I thought it is spelled "whear". Certainly that's the woke spelling. :D

Prisoner of overpriced property = POOP ....

.. you are hereby sentenced to 30 years hard labour ... 50 % of everything you earn will be given to an Australian bank .... you are not to go to the local cafe and have smashed avocado on toast , you cannot afford it ... may the Reserve Bank have mercy upon your soul ... ... the prisoner may step down from the dock ....

Could be just me but the graph looks pretty normal and in fact there are still less houses for sale than normal. From observation of what's happening in my road people are just giving up trying to sell and one house switched from sell to rent. Total TM listings in Tauranga have flatlined at 1200 and have been that way for weeks now. Asking prices are falling I get notification of change in sale all the time but the price was unrealistic to start with and seller's are trying it on.

Only happens to other people, not my precious TGA!

Covid changed things big time. Many people took early retirement and working from home became acceptable. Things moved on. Fibre internet even made a difference. No need to be stuck in overpriced Auckland for work anymore. The whole property market is rebalancing so expect different percentages of price drops between locations.

Yes and No. It changed things and made work from home more acceptable, but if you're talking about overpriced / overvalued well that hasn't been solved, yet.

Cheerleading like Tauranga is some magical exception in NZ to the inevitable blowout, I find quite fascinating...

and lets face it The Mount is a fairly average NZ beach

You are not a surfer then obviously?

Papamoa happens to be one of the best east coast beaches in the country.

Papamoa 5/10 - Coromandell/Far North/Gisborne ...thats just a few 10/10

au contraire ... If I was in that area and there was some decent swell (which there usually isn't), Wanga Bar would have been my choice up until about mid 90s. For me it's the Naki all the way - a plethora of points, reefs & beach breaks with the might maunga (yes the real maunganui) always in the backdrop.

There's a little bit from column A, and a little from column B

Auckland is usually the country's canary in the mine for the property market. Everywhere else is often 12-24 months behind.

That said, there is always regionality. People are leaving the cities and many of the regions are still experiencing price increases. That urban rural migration probably has a few years left in it, although obviously if prices drop in the cities that inhibits what people can buy their new place in Cromwell or wherever for.

Aucklands really waiting for National to get back in, bring on the migrants.

Let the intergenerational looting continue!! Huzzah!

... the younger generations are mobile ... the barriers have been removed ... expect the " brain drain " to resume ... Australia , or beyond ... they'd be mad to stay here , when our property market has been so badly mismanaged & mispriced ...

In recent years the low prices in rural NZ have been erased.To a point where to buy there is not logical.

But I would say that demand there will quickly subside once Ak/ Wn / Chch prices become reasonable. And rural NZ will very quickly drop even more so and return to being reasonable again.

Turangi at $620k is a BARGAIN.... not. The regions always wear it in a pullback, I am actually predicting Queenstown and Waiheke to get thumped as well this time...... This time is different, its the end of a multi decade debt fest

I'd say Queenstown is a bit safer than Waiheke, much larger pool of buyers.

I remember in 2008 places like Gisborne and Rotorua getting spanked. Yes Auckland and most of New Zealand escaped with relatively minor fall but the ‘zombie towns’ got wrecked.

I'm not even that old and I remember people facing the choice of losing money or being stuck with houses in Gisborne (due to divorce, job changes, etc). Last year someone in my family sold their ageing 3 bed/1 bath place on an average street for $680k. Other relatives are remortgaging up to new valuations to buy jet skis and utes. Everything changed in the space of about 4 years as the credit came gushing in.

I think regions, especially where the job market is not spectacular, will start sinking as fast as Auckland and other cities.

Tauranga is as overpriced as Auckland, if not more.

Tauranga is way over priced. Lots of tradies renting and buying here.

When building grinds to a halt i reckon there will be a lot of properties on the market at bargain prices.

Tauranga residential market is in for a rout. Mount local market might hold up better but all other suburbs will s**t the bed. Prices are well over cooked here and our RE Agents carry a special sort of arrogance that needs to be slapped out of them.

This feels so much like shares in 1987. Gird those loins for an economic reset.

One of the good things about about Black Monday/Tuesday 1987 was that it was near immediate. In some ways it's worst to have these slow moving revaluations lasting months that turn into recessions in the real economy as people start worrying and changing their spending patterns.

Slower is better it gives you more time to pick up distressed assets

Expat, is that really you?

No, Expat was excommunicated. We are brothers from a different mother.

Back then NZers thought Jones, Ariadene , Bridge, Tasman Properties etc could not really fall, the tip sheets where yesterdays version of the Oneroof property hour..... Even a tellor at the local bank could start the lending process for your multi hundred thousand leverage property adventure.....

Just waiting for the RBNZ to put the 75bps boot in...

8% Guaranteed.

100bps if they want to get ahead of the game. Anything less and inflation continues.

I agree with you here Carlos. When has common sense ever been observed by these clowns.

Do that and a property crash, including for Tauranga, is guaranteed. Don’t you think?

Nope. Said it before but your a bit deaf we are looking at another couple of 50bps rises at least so no different from a single 100bps jump. The market needs a shock or this inflation will be permanent with high prices locked in. Prices will go up and then not come back down. If the Auckland house prices go down 20% so be it

But all economists are picking more than 100 BPs Of increases to come so what’s your point?

If your point is 100 BPs in one go then that is an out there view. If you are saying there will be at least 100 BPs of increases cumulatively then my response would be ‘So what, everyone is saying that’.

you seem a bit deluded on Tauranga, I don’t see anything to suggest it won’t fall at least 15-20%.

House prices are going down will be 20% by end of year and will continue to fall depending on rates and inflation. We have a huge problem as people on average wage have no chance of buying at 10 x income, the market will implode over next couple of years way over valued compared to income.

I haven't read Carlos saying house prices in Tauranga won't fall, although I can't remember everything everyone posts on here, it seems Carlos is saying they are holding up currently. You seem to be having a go just for the sake of it.

Read on further down the chain. He says he expect price gains this year

Correct YOY single digit gains it's a very specific prediction made a long time ago now relative to what economists are now putting out that changes weekly so what's the point of that any idiot can see what's happening on a month by month basis. Six months ago we were being told no interest rate rises until 2024 well that worked out well for a lot of people.

It should, but it can't get to that level. Over 7.5% will completely crash and burn the housing market.

The RBNZ will stop raising when rates reach the 7.5% threshold, inflation or not. They will try a managed correction.

The slump started with the CCCFA

It's not a slump ... but merely a reversion to mean (ish), And unfair tax advantages in property investment helped the 20 year bull run no end (until now).

But property investors will have you know that they are just like every other business in New Zealand, therefore they are fully entitled to those tax advantages. The new laws are discriminatory and are done out of envy of their success through hard work.

Also, please don't mention the fact the business most of them have actually been in is trading for capital gains. It would be horrid to have to pay honest tax on that!

What a great business to be in, locking 1 customer for 12 months of regular payments, at 50 - 70% of the median wage. You don't have to pay for power, you don't have to collect and pay GST, no employees with PAYE, Holiday and Sick Leave entitlements, you don't generally have to worry about inventory including theft, shipping delays. Health and Safety at Work Act doesn't apply. If you want another customer, you can have one with zero dollars down using personal lending rates.

I can't see why the Government would remove interest deductibility, it makes no sense /sarc.

Even calling it a slump infers it's unwanted, and should be mitigated. Let's call it a correction, allowing property to resume a value commensurate with a real economic landscape, and not one generated by the RBNZ.

Could you please add 'the gap' as a third line to this chart.

I still think buying an investment property or two is a good idea for someone in my circumstances (early 30s good income). I bought a couple in the Wairarapa in mid 2020 they are tenanted by good people and so far haven’t had any issues. The rent covers pretty much everything except the principal on the mortgage which I am happy to pay like a form of savings. The bank required 25 year terms so I have paid down a decent chunk of principal in two years. I will have to put in more with higher interest rates and deductibility but that’s all good. Looking forward in 30 years, I will have valuable freehold assets that generate a reasonable income each week to help during retirement. I am not that interested in quick capital gain as I will never sell. I am sure the 65 year old me will be very happy with the decision I made to buy them!

With the amazing capital gains its worked well in the past, the issue is that asset prices (of a place of shelter) cannot keep going up faster than wages for long. Eventually things revert to the mean, its a long way below, I am a buyer of a decent beach bach for my kids, and a trout fidhing bach at Turangi, but right now is not the time.

Good on you, sounds a good plan.

However may I ask what interest rates you are paying on those properties and when do the terms end? My point being that while you might be ok, highly leveraged investors who bought at rates of circa 2.5% but need to re-finance at 5 or 6% might find it a bit tighter.

Nah they will be fine. They will put up the rent to cover their costs and the tenants will just pay.

Or maybe "they" won't put the rent up, through choice or because the market dictates otherwise and they have to tough it out. Similar to some businesses at the moment. I'm sick of the attacks on "all" landlords on here.

Don't cry Norm. I'm sure if you were a Landlord for altruistic reasons then you wouldn't take these comments personally, and you'd just scroll on by.

Crying? It's easy to say something like that when your on the internet communicating with a stranger and says alot about your character. It's also another example of why landlords don't speak up much on here. Your last sentence is incorrect in my case, and I'm sure I'm not alone.

It's "you're". And there's a space in "a lot". Also, last time I check this was a financial news website not a NZPIF Chat Group. You're making it sound like Landlords feel unsafe to walk the streets at night.

They probably will be unsafe to walk the streets at night in the future - go to any other country that has driven up inequality like we have and see what it's like. Many 'investor heavy' parts of NZ are getting like that already.

It's the bed they've made for themselves though.

You're correct about the spelling. I'm pretty sure it's checked, not check.

Thank you my friend.

There are a lot of rubbish landlord comments. I have a tenant on my rural property, For me its about having a good person living on your land, security, and sharing the land with someone who appreciates it. Not everyone is a Manurewa slum landlord.

the gap will be big enough to safely drive a bus through it without touching the sides.

Maybe even a double decker.

Good luck catching a bus in Auckland to go through the gap...

Land owned by households as a % of GDP at the end of 2021.

Japan 130% (peaked at 325% in 1990)

Australia 330%

New Zealand 520%

This correction is going to be epic.

Wow. This really shows the issue. Our ponzi model based on economics is higher than Japan and Aussie put together. Truely wow.

But TTP said we are in for another soft landing?

Where is this elusive "TTP" that you speak of?

Good question. It seems he only comments on articles that slightly align with his views/interests. You won’t find him here.

"Sign of our success" - Bill English

NZers have approx 65% of their wealth tied up in property, the USA approx. 35%.

In the North America property is dirt cheap compared with most of the world.

Having trouble finding their starting points in terms of price-to-income ratio, but:

Irish property market tanked 64%, ended below 3.

Japanese property market tanked 65%, also below 3.

US tanked 33% - ratios unknown.

Spain tanked 37% - ratios unknown.

If someone more adept were able to find the before/after ratios would be interesting.

But if that's any indication, we're looking at ~70-75% long term from peak. Though I've been assured "NZ is different".

All Data / News suggesting .......

https://i.stuff.co.nz/life-style/homed/real-estate/129073121/new-zealan…

House prices went up in many countries between 15% to 25% but none were to beat NZ where it went up by 40% to 60% plus.

With 15% to 25% rise, economist and government in those countries were worried but here in NZ even with 60% plus growth, so called economist and experts were justfying - can check the above link, where too, so called Independent expert ...actually a lobbyist..........

Now that it is established that what was happening in NZ, had all the characteristics of a ponzi, can say that during peak of ponzi, our PM instead of being concern, came out in defend with her statement that no kiwi wants the house price to drop even though survey conducted suggested otherwise. Was she ignorant or was badly advised or was she echoing her choice.

During peak of ponzi ( many feel offended with the word ponzi and are still in denial) the reason given was supply and demand, if that was true, what has happened now......FOMO was created by RBNZ and Government policy and statement which led to stamped to buy as was either now or never.

Now is the time for patience. The leveraged specuvestor is trapped between drowning in higher interest rates, or swimming for the increasingly further away life preserver of a buyer. Younger mobile renters/future buyers are voting with their feet, to Australia. The tax rinse is fading unless new. More new housing stock arriving-once the gib arrives. Immigration is still nothing and why would you come to a life of rental servitude. DTI inbound later this year.

We are between Denial and Fear on the bubble model. Smart money used the cheap debt to eliminate their loans and build a vulture fund.

Next OCR announcement in 3 weeks. Time To Panic. Kaaaarrrk.

There’s going to be an awful lot of houses not being completed before the gib crisis abates. Following that will be a collapse of the building sector as cash flow dries up. It’s happening at an alarming rate in aussie and has just started here.

An awful lot of potential Kiwibuild houses bought at a discount...?

That is not how the Gov rolls

They will most likely pay fully build market price for them and then it will cost the same amount to finish off

Averageman, do you think RBNZ was ever serious in implimenting DTI, more so now.

Never.

Yes. Orr has been chasing it for ages. Just like Auckland council delayed setting rates till the top, wait for the inevitable reset and then do it. The objective is to stop the ponzi stupidity from repeating.

Why. Is our economy stronger that Jap and Aus combined, or is it just greedy boomer tax avoidance?

@Averageman - do you think RBNZ will propose to bring in DTI at a useful level - 4.5 or 5 to 1 ratio? Or do you think 6 or 7 to 1, to start with “forward guidance” of a sinking lid down to 4.5 or 5?

I don’t know the implications of new laws around increased Treasury oversight of RBNZ but will this make such policy introduction and changes to the ratio something requiring finance minister approval?

Yes, they could see the housing crash coming, pretty much everyone outside New Zealand could/can see it coming. They will implement DTI at sensible levels once the prices have fallen, to try to stop it happening again.

Be patient for higher interest rates, DTI & tighter bank credit making it harder to buy...

So what are peoples’ current picks?

End of last year I said 5-10% price falls for 2022 as my central scenario, with 10-20% falls as my second most likely scenario, we are down what about 4-5% for the calendar year so far? And 6-7% from November 2021 peak?

I reckon it’s looking like a 12-15% fall this calendar year, and perhaps a further 10% next year.

Still 6 months to go , so I reckon 20 % down by year's end ... a deep recession builds on that ... followed by house prices falling another 20 % in calendar 2023 ...

... some folks are gonna get very hurt , call 0800-ORR or 0800-ROBBO , and vent your spleen ...

20% down on what it was 3 years ago is no problems at all for people who bought prior to 2021. The price stupidity only really happened after people living overseas started to return back to NZ in significant numbers from Jan 2021 onwards.

Now that those people are returning back overseas, we'll see an increase in listings and a drop in demand, not helped by the increased number of residential properties being built.

That can only be good for housing affordability.

Still single digit gains in Tauranga year on year but 2023 is not looking good if we finally start to follow Auckland. Not expecting us to get as pummeled I still look at the prices up there and it's a joke.

Tauranga is still growing its population at 3% plus per year for the last 2 years. If you include the hinterland population, that's between 6-7,000 more people per annum [2020 & 2021]. And you can see it on the roads. I suspect many are ex-Aucklanders but also getting ex-Wellingtonians as well. Tauranga is not immune to reality, however, and it will hit at some point. Already our rental is down 3-4% on homes.co with more to come I'm sure. We're okay with minus 20% from Nov 21 peak. Even 30%. Just. Breathe in deeply. Everything will be fine.

"as the Reserve Bank started pumping cheap money into the banking system"

The LSAP or QE that the Reserve Bank undertook is an interest rate mechanism, it merely returns reserves back to the banks which they already own but which were being held as bonds and the banks don't lend these reserves out to the public to buy houses.

Banks don't lend other peoples money or government currency, they create new money when they lend.

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creati…

https://www.bankofengland.co.uk/working-paper/2018/banks-are-not-interm…

I'd like to see what that gap is between 1967 and 2007 as well.

I'd like to know what that gap has been historically from the time we changed over to the dollar.

I'd like to know how it was during the oil shock and during the financial crisis of 1984 and subsequent reforms.

And was the increased speed in the market due to the relative lack of supply of properties.

I dont really understand how we can claim to be a free market economy with covid the goverment dropped interest rates then post covid put them up . I read that the whole depends on the American fed reserve . So we are just following them. But the carnage wont be huge because the banks will manage the mortgage sales so it does nt hurt the market they did this in the dairy industry. With the governments healthy homes and new land lord tax I would say it will be at least 5 years before we see any growth . But there will be many people who lose there shirts .Which is quite sad it food and accomodation should be a basic right and cost to all

I suspect Grant Robertson is rushing his new insurance scheme through to protect the property market, paid for by the taxpayer. Which will mean if National get in, they will not get rid of it - even if they pretend so now.

Grants super-benefit scheme for our already wealthy...

Interesting seeing all the articles across Stuff and the Herald this morning about the looming construction sector crash. Something I was picking over a year ago here.

such a pity there’s such a lack of foresight in this country, things are often not done until it’s far too late…

Housing is akin to shelter. Some buy and some rent and a few live off grid. It used to be a once in a lifetime buy. Then the market went ballistic. The house owners got wealthy and new buyers/renters were priced out of the market.

Talk of young adults leaving the country. After a year of legislation aimed at house speculators, prices stalled.

Blame on greedy landlords in forums, even baby boomers accused of stealing the future of their offspring.

Oblivious to the old bequeathing to their heirs.

Or those have nots, who chose not to take out a hugh loan and live a frugal life for the duration of their working lives.

Great cover photo

It proves nothing but that, house prices are closely linked to interest rates. People may feel the house price drop now, but the market sentiment changes happened since last December as I pretty much went to open homes every week till April.

the fear of over paying, and sense of hour price drops in the public is like bubbling, when you see it everywhere on the media, means it's already on it's peak of the bubbling, and things will either settle down a bit, or starts to improve.

and one thing is more clear now, the 21% price jump in the last year is not normal, and it's a good thing house market cools down. the sooner it happens, the less negative impact it has towards our economy.

another note is that, it was stupid last year for people thinking house price will keep going up, it will be equally stupid to believe house price keep dropping even more. I actually think it's time to buy, especially for people who're looking long term.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.