This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

There have been very few occasions in the past two decades where markets are this bearish... in fact only two: '08 Financial Crisis & COVID-crash. When positioning gets this one-sided, potential for aggressive short-squeeze rises so stay nimble. pic.twitter.com/3cfWzYlVIv

— John Bromhead (@jbfm_) May 13, 2022

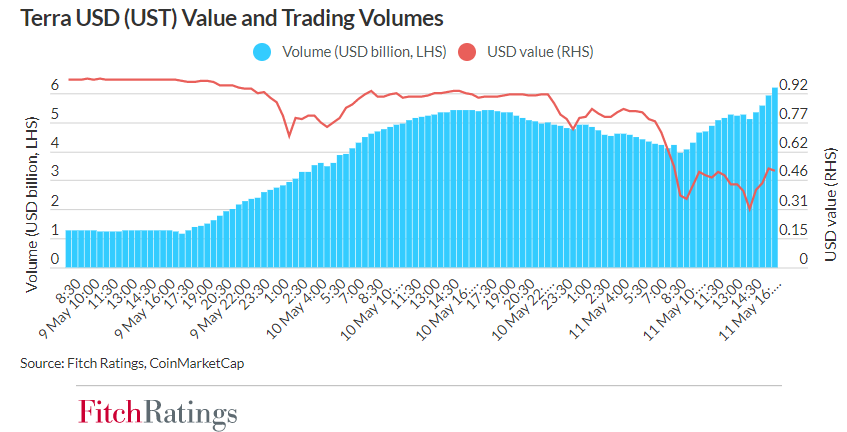

Bloomberg opinion writer Matt Levine casts an eye over this week's massive sell-off in cryptocurrencies, fanned by crashing stablecoin Terra USD, and the unmooring of fellow stablecoin Tether from its US dollar peg. Supposed to maintain a value of one dollar, Terra USD fell as low as 23 cents.

Levine wonders about potential contagion flowing into the rest of the financial system. This is US focused. But as we know if Wall Street and/or the US economy sneezes, we tend to catch a cold.

If you asked a normal person, you know, two weeks ago: “How would it affect your life if the prices of some monkey JPEGs and algorithmic stablecoins crash,” I think most people would reasonably have said “I do not own a monkey JPEG and do not aspire to own one, so this will not affect me at all.” My guess is that they would have been right. My guess is that the real world is not too affected by the crypto world, and that if crypto prices crash there will not be a ton of contagion in the rest of the financial system. But I think it is, at this point, debatable. Crypto has at least started to work its way into the real financial system. Some traditional investors also own crypto; if their crypto goes down they might have to sell regular stuff. Some public companies are exposed to crypto (because they are crypto exchanges, because they have levered crypto holdings, etc.), so your boring old index fund might go down when crypto goes down.

Levine highlights an article from his Bloomberg colleagues Lyn Thomasson and Anchalee Worrachate pointing out concern that retail investors already hit by dabbling in so-called meme stocks, may be facing the music again. For anyone wondering, a meme stock refers to the shares of a company that have gained a cult-like following online, especially through social media.

As markets slumped in unison on Thursday, traders pointed to the chaos in crypto as a focal point of their concern. Strategists are increasingly worried that small traders, already nursing losses from the meme stock craze, will be wiped out on their crypto holdings and sell everything else.

“Contagion here is not via linkages between the crypto ecosystem and the traditional financial system, but via retail investors sentiment,” said Nikolaos Panigirtzoglou, global market strategist at JPMorgan Chase & Co. “If the $1 trillion capital loss in crypto markets causes broad-based retrenchment by retail investors in other risk assets such as equities, then that’s where the spillover is.” …

2) The critical importance of improving supply chain resilience.

Earlier in the month I wrote about a government issues paper on plans to develop New Zealand's first ever comprehensive freight and supply chain strategy. Covid-19 induced disruptions have turned supply chains into big news over the past couple of years, helping to fan the flames of inflation we're now seeing. This is a really important, and I think fascinating, area.

In this Newsroom article David Robb, Professor of Operations and Supply Chain Management at the University of Auckland Business School, looks at stress testing resilience in supply chain entities.

This example he cites from Switzerland is really interesting.

During turbulent periods the first port of call often involves increasing inventories. Clearly, item perishability, obsolescence, and holding costs must be considered, but this can be achieved by changing safety stock parameters. We should also consider extending national reserves beyond products such as PPE and Tamiflu to include imported items such as food ingredients, lubricants, and petroleum to safeguard both local supply and exports. We could rotate this inventory to ensure limited waste.

In this, we could learn from Switzerland, where a public-private partnership has maintained a system of compulsory stocks for decades. The Federal Office for National Economic Supply (Fones) mandates stocks of two to six months’ supply of products such as soap, screws, lubricants, sugar, oils, cereals, and fuel.

In involving about 300 private sector firms (which own the stock), efficiency is improved and risk reduced. Holding costs are recovered by higher prices, estimated to be less than NZ$25 per capita per year. These strategic reserves have allowed Switzerland to navigate pandemic supply chain disruptions well and they are supplemented by household emergency supplies – Fones recommends households maintain a one-week supply of a basket of goods, including food and drink.

Naturally, the ideal basket of goods for us would differ, as we have quite different import/export dependence, and while not landlocked, we have very long lead times, lower population density, and are more prone to natural disasters. We may consider prioritising imported goods and materials, including common intermediate goods, that would protect our export sector’s ability to operate. And if we do this well, the management systems could perhaps become part of our government-to-government offering.

3) An Aussie mortgage interest rate cap.

With an election looming in Australia, Clive Palmer's United Australia Party (UAP) has a 3%, five-year cap on mortgage interest rates as a key policy. Is this a good idea, and is it even workable? The ABC's Michael Janda takes a look and finds it would be a case of turning the clock back to a time when interest rates and inflation were generally high and access to credit wasn't as easy as it is today.

UAP leader Craig Kelly told News Corp in a recent interview that the cheap mortgages could be funded by the government issuing bonds at 0.1 or 0.2 per cent and on-lending that money to the banks.

The problem is that the current Australian government five-year bond rate is already above the proposed 3 per cent mortgage cap, and no private investor would take such a low return.

There is one institution that could provide this kind of funding — the Reserve Bank.

In fact, it already ran a similar scheme during the pandemic, which is one reason why there were so many fixed mortgages available at interest rates below 2 per cent until that program ended in the middle of last year.

"The [mortgage cap] scheme would only work if banks could obtain funding below (and well below) the cap," explained former Commonwealth Bank chief economist Michael Blythe.

"The RBA did achieve this outcome as part of its QE [quantitative easing] operations via the Term Funding Facility during the pandemic.

"But those were unusual times and shouldn't be the norm."

A question that looms for me here is, if the Reserve Bank of Australia were to provide ongoing cheap funding for mortgages, would retail banks even be needed?

4) Catching Covid again & again.

I recently caught Covid-19. I got it from one of my kids. After surviving months in New Zealand's Covid capital of Auckland without getting it, we frustratingly caught it while on holiday in one of the country's remoter regions, the Hokianga. Three out of four in our household got it. We're all vaccinated and fortunately none of us was too sick. Still, I'd rather not get it again. Thus it's a little alarming to see suggestions that getting Covid more than once or twice might be the best way to build up immunity against the virus.

Bloomberg's Justin Fox writes about this, heavily leaning on the thinking of German virologist Christian Drosten. His suggestion is that for Covid-19 to become an endemic virus like the flu, lots of people might need to get it again and again. That, Drosten, says is because we won't be able to vaccinate people every few months, meaning the virus itself might have to keep updating people’s immunity.

It is this mucosal immunity that keeps influenza from spreading most of the year, with the disease’s effective reproduction number (the average number of people who will get it from each one who has it) surpassing 1 for only a few months in winter, when indoor crowding, drier air and other factors seem to lead to increased transmission.

Contrast that with Covid: Current vaccines generate some mucosal immunity but it fades quickly, and while there are nasal-spray vaccines in development that target the mucous membrane, they’re not ready yet, and this approach has been of only mixed effectiveness against influenza. Meanwhile, less than half the German population has been infected with Covid, Drosten said (in the U.S., according to a Centers for Disease Control and Prevention report this week, it’s 57.7%), so there probably isn’t nearly enough mucosal immunity out there to prevent the reproduction number from rising back to 2 or 3 in the fall, bringing another huge wave of infections and concomitant stresses on hospitals and disruption of daily life.

One thing that could preclude this, Drosten speculated, might be a lot of young people (the “Party Generation,” he called it, in English) getting infected a second or third time over the summer, but he expressed doubt that this would be enough to make a difference in 2022. How many times are people going to need to be infected to confer effective immunity against transmission, asked NDR science reporter and podcast moderator Korinna Hennig. Drosten’s reply:

My idea is that this is in the range of a number that you can count on one hand. But no one can say for sure at the moment.

5) Stilt house tumbles into the ocean.

The quite dramatic video below, of a house falling into the ocean, certainly caught my eye this week. There are a series of additional tweets from journalist Tolly Taylor on US homeowners versus rising sea levels and storms.

Here in NZ the Government on Monday is set to unveil the country's first Emissions Reduction Plan and details of the 2022 Climate Emergency Response Fund. Brian Fallow will be covering this for interest.co.nz.

An unoccupied house on stilts in Rodanthe, North Carolina, as it collapses into the ocean this afternoon.

— Tolly Taylor (@TollyTaylor) May 10, 2022

Was worth $381,200 according to Zillow. pic.twitter.com/RxkgOkBIv0

97 Comments

RE: 3) An Aussie mortgage interest rate cap.

UAP leader Craig Kelly told News Corp in a recent interview that the cheap mortgages could be funded by the government issuing bonds at 0.1 or 0.2 per cent and on-lending that money to the banks.

LOL - banks monetise government debt at tenders and syndication.

Love that crypto and meme stocks are a concerning contagion if it means investment in other areas slips back, but zero thought given to the fact that more retrenchment by retail investment is going to be caused by broad destruction in disposable incomes caused by central banks and the entrenched financial sector. Imagine the panic if huge mortgages relative to net earnings were given the same scrutiny.

Levine wonders about potential contagion flowing into the rest of the financial system.

Alarming to think the crypto crash could potentially spread to traditionally safe asset classes like primate based NFTs.

I'm amazed by the rapid retreat of swaps this week. I can't say I understand what's driving it.

Reserve Banks are more or less giving up on controlling inflation. Apparently #TeamTransitory where so sure they didn't bother to consider a plan B.

Based on some comments or something? There haven't been any major rate announcements that I'm aware of?

Maybe because Tether bought $40 billion of US treasury bonds to shore up their off chain collateralisation. Prices go up; bond yield go down.

Maybe. But $40b is a drop in the bucket for the treasury market.

It has been enlightening watching YouTube videos discussing the recent cyrpto losses. It's dawned on many that there is no intrinsic value to crypto. The value can plummet to zero, very, very quickly.

I think crypto aficionados have been too critical of fiat money. Fiat money is deemed to be legal tender by a government decree. That's actually quite significant.

Cannot figure out the thinking of Crypto fans, take a look around you everything is backed by fiat, Crypto backs nothing but Crypto. I don't think the fear will flow into other areas, in fact ALL the fear it flowing into Crypto first as a release mechanism. Its pretty obvious that people are pulling out in droves and taking their beans off the table. Don't get me wrong, some people have made a small fortune in Crypto but the games up, the smart ones got out early and paid off their mortgage or bought a house with it.

It is Faith based, just like any cult.

Cannot figure out the thinking of Crypto fans, take a look around you everything is backed by fiat, Crypto backs nothing but Crypto. I don't think the fear will flow into other areas, in fact ALL the fear it flowing into Crypto first as a release mechanism.

The word "crypto" is redundant nowadays. It's only used by people who don't really understand the different profiles and use cases of a range of digital assets. Discussions cannot be built around words that are so nebulous.

Crypto = Created out of thin air, new ones created daily in peoples garages. Apparently the future of all money exchange. Or a long term store of value (depends on the day of the week).

Wait.. Yes yes, use case this, just don't get it etc...

Crypto disappears soon as you unplug the computer.

There in lies the rub of it… it’s mythical a mirage of imagination

I'm no crypto expert, but find it interesting that the two coins that tanked this week are so-called stable coins which were tethered to currency. They unhinged. I am taking this opportunity of buying BTC, ETH & LRC.

Something something blockchain something.

There's problems with fiat, but that doesn't automatically make an alternative superior.

Then they argue about decentralisation being superior, which is the fiscal equivalent of being a libertarian.

"Then they argue about decentralisation being superior, which is the fiscal equivalent of being a libertarian."

This. It's precisely the centralisation that makes fiat superior. It is not perfect and it sometimes fails but the idea that there can be a store of wealth which is detached from the physical world and also from any political system is bonkers. It's also completely undesirable in any case. Society is built on institutions, without centralised institutions civilisation falls and your abstract store of wealth in whatever form means jack shit.

Decentralized is all very well and good until you lose your wallet/passphrase.

If I forget my internet banking password, my internet banking number or my bank card then I can phone someone to get it sorted.

Is the btc endgame that they all end up lost? There's a finite supply, a nonzero loss rate, and no recovery mechanism.

I think crypto aficionados have been too critical of fiat money. Fiat money is deemed to be legal tender by a government decree. That's actually quite significant.

Fiat money has its place. For ex, for near term purchases of goods and services. But as a store of value, it has diminishing returns over time. What is more valuable to people is currencies that appreciate in value over time. Like Bitcoin has shown. That can help transform societies. Right now, countries like NZ are destroying themselves through mindless monetary policy.

We know that the deterioration of fiat is the result of the govts and central banks manipulating its supply. The fact that it's legal tender has become increasingly meaningless.

Who uses fiat as a store of value over time. Stocks companies, energy resource, land, commodities. This is were the value is. Any currency is just a measure of the more tangible, regardless the format. The only difference between cryptos and nz fiat is that nz fiat (for all the cynical views of reckless policy etc) is much, much more stable.

... exactly right ... real tangible assets which produce an income are " a store of value " ...

As I recall , an advantage of Bitcoin was supposed to be that there was an ultimate ceiling of just 24 million of them... unlike fiat currencies , which can be printed holus bolus , and they have been ...

But , Bitcoin can be sliced up , each one can be cut into ever increasingly small bits ... itty bitty bits ... an infinite supply of them ... so , where's the advantage in that , over a fiat currency ?

But , Bitcoin can be sliced up , each one can be cut into ever increasingly small bits ... itty bitty bits ... an infinite supply of them

1 BTC can be divisible by Satoshis (100,000,000). It is not infinite.

... aha , I am informed , thankyou ... so , 100 million Satoshis per Bitcoin ... and , there's up to 24 million Bitcoins ... so , an upper limit of just 2400 trillion Satoshis ...

2400 000 000 000 000

... oh yes , I can see the advantage in that , over a fiat currency .... hmmmmmm !

Yes. There is USD2.6 trillion in circulation. You can do the calculation in cents if you want to. Not quite a quadrillion.

So ... there's 2.4 quadrillion BTC Satoshis , but only 0.26 quadrillion US cents ...

... ummm ... that's an argument favouring fiat over crypto by a tenfold factor ...

I think the difference is central banks can add 0's to a spreadsheet, whereas to create more cryptos you have to burn through a shit tonne of electricity.

Once governments make own digital currency like in China Bitcoin will be faze out just like China has stopped it. The governments around the world will use excuse of being unstable or not regulated enough.

Like I have said before, governments don't even need to ban it. Once you remove Bitcoin from being able to be exchanged for a new digital currency it will have to stand on its own two feet and then if you cannot actually buy anything with it then its dead overnight. Bitcoin is only "worth" something while its tied to Fiat, the second it loses that connection its worthless overnight.

Store of value is the distortion whether it be fiat or crypto. It's born out of a fear based value system. The fear of losing money rather than appreciating the true value of what one has. Fundamentally different values and a fatal flaw in human conditioning and the social engineering that is civilisation.

It takes two to tango so even though fiat supply has been manipulated, the consumer has contributed to it. And it's been done to keep the people compliant. It's the financial institutions that receive the benefit, that become too big too fail. Crypto, equities, property are all open to being manipulated by these institutions. The people are just as manipulated to keep feeding the machine.

Yeah a few people might make a decent win, but it's no different from making a decent win at the casino.

A central bank with a 2% target inflation rate could easily offer a 25 year fixed rate mortgage at, say, 3%. If this was offered on owner-occupied homes only it would change the game and significantly reduce the rampant extraction of profits by commercial banks. I would add state insurance to the package too.

Is the RBNZ equipped to purchase individual mortgage promissory notes and issue a lien on the proffered collateral?

Currently, RBNZ eligible collateral securities are limited to this list.

Nope, sadly. Two easy choices though:

- change the rules to allow RBNZ to do exactly that (been done before)

- run the scheme through a third-party bank

- change the rules to allow RBNZ to do exactly that (been done before)

The RBNZ hardly needs the publicity if residential property values values tumble to a point where individual over indebted borrowers could be driven to default.

This is bad enough - Robertson: $5 billion bill for Reserve Bank's bond-buying programme the product of a risk deemed 'worth taking' in 2020

And something like this would be too much - Swiss National Bank posts $34 billion loss as bond losses bite

You're missing the point a bit to be fair. A state backed mortgage is not without successful precedent, and it offers some additional tools to deal with property market crises. For example, RBNZ could take ownership of houses and rent them back as state housing with affordable rent, or purchase the land under the house and lease it back at peppercorn rent to households that have hit hard times (with the home owner having the option to buy back the land).

I know that you also know what a nonsense that $5bn LSAP story is - that loss could have evaporated by next year, as could the far greater gains that the Crown has made on its holding of equities and shares.

Fannie May and Freddie Mac

Ha haaaa ... " Fannie " ... that's the funniest name going , I always crack up at that ... Fannie... teee heeeee ... fannie may , or may not ...

That's Fanny, silly

The reality is that 2022 is the year where old illusions go to die.

Big call from Tim Morgan at Surplus Energy Economics

https://surplusenergyeconomics.wordpress.com/2022/04/28/227-pictures-of-imperfection/

"Here in NZ the Government on Monday is set to unveil the country's first Emissions Reduction Plan and details of the 2022 Climate Emergency Response Fund. Brian Fallow will be covering this for interest.co.nz."

Quote from another article:- As the USA and Europe retreat from prosperity, India seems determined to overtake China, with a 400 million ton boost to coal production in the next two years, and a massive relaxation of environmental rules and other incentives to boost coal mining and industry.............. India’s coal needs are set to double by 2040...... The government says it plans to increase domestic coal production to 1.2 billion tonnes in the next two years to support a post-pandemic economic recovery..... - end quote

And here we have Labour and James Shaw crowing about changing school fired coal boilers using how many tons coal per year.... to reduce carbon emissions by about 35,400 tonnes over 10 years. This translates to about 12380 tons coal over ten years (used 2.86 CO2/1ton coal). Laughable when you see what India is doing

NZ economy being slowly being screwed by climate change policies. I understand even Fonterra are going to stop using coal over time. I bet there use of coal is chump change compared with what India are doing.

nigelh,

You are quite correct in saying that whatever we do, our emissions are tiny on a global scale (though high on a per capita basis) and any reductions we make will be irrelevant in the context of increased emissions from India and others.

Should we then do nothing? I don't think that's feasible. We are a very small trading nation and could easily be frozen out of markets if consumers decide to punish us. We also have a reputation to protect.

Yep our per capita are at a dangerously high level, I’d say we could be shut out of trade with Europe within a decade and other environmentally friendly countries would follow.

100% this. If we do not bring down our per capita emissions we will be ostracised from international trade. Well maybe China and India will take our products but at what price ...

I’m open to your thoughts on how our reputation is so intrinsically linked to our trading. Seeing China is our no.1 market and is ESG aware

That house was worth nothing because nobody was prepared to relocate it - or even demolish it for salvage parts - when doing so had been possible.

Fantastic to hear that Brian Fallow will be writing for Interest. One of 3 or 4 journos at the Herald that I really rate.

Crypto. A commentator on Bloomberg said it all a month ago when he proffered the incredible insight that for crypto to revive would require new speculators (investors) to buy or existing speculators (investors) buying more..

Its a space based largely on bull & fanciful imaginings & enormous co2 output.

One pointless bitcoin is down 36k US or 55% in the last 6 months. Or is it that fiat is up by 55% - considering crypto lovers consider fiat volatile.

If you look at BTC over time using a logarithmic regression curve, you will see that it's not actually as volatile as you think. But I understand your thinking. Most people focus on the short term, which is why something like BTC is completely alien to them.

If you look at the depreciation of the value of fiat using a logarithmic regression curve, it probably doesn't look so bad either!

To be honest, if people really made an effort to understand the depreciation of fiat over time, they would be horrified. It goes back to the point about the value of a unit of currency ideally appreciating over time. Now, we know that is not going to happen, hence the invention of BTC. Does it mean that BTC replaces fiat? No it doesn't. Does it represent an opportunity for people to to save in a deflationary currency? Yes it does. There is the value proposition.

Is BTC meant to be a transactional currency or just a volatile store of value? If it's just a store of value, what makes it better than a real asset like property or shares?

Good questions. I think you should read the white paper and make up your own mind. Breaking it down, it's designed to be a P2P electronic cash that removes the need for financial institutions and solves the problem of double spend. Nowhere does Satoshi outline its design as a SoV. There is no argument that it is a better SoV than property or equity ownership.

Just on assets like property and shares being a SoV. Property remains while companies can go bankrupt. But the idea that property appreciates over time is generally true, but it cannot be programmed to do so. Case in point: Japan. Land in Ginza peaked at USD750k per square meter during the bubble. It's currently priced around USD330k oer square meter. Ginza land has among the most expensive in the world and is a SoV, but as you can see, the price can also be volatile if the market is distorted.

So if its just a method of Exchange, and its more volitile short term than fiat. And it's not a sov...

Yes yes I've not read the user case.

It is what it is. Let's look at the ROI of BTC as of today:

Past 1 year: -41%

P2Y: +205%

P3Y: +263%

P4Y: +248%

P5Y: +1,626%

P9Y: +26,196%

So ... the ROI is alike a ponzi scheme ... insane returns initially , suckering more people in , gradually declining , but still positive ... declining ... then Pooooof ! ... deflation ... it's actually down , and not just a little bit , mega scary negative ... seriously squeaky bum time ...

No one is doubting that it was a good investment/gamble, there were probably some dot.com shares that had a similar trajectory in the 90’s. It’s the future most of us wonder about; kind of like investing in a company that sounds good on paper, has lots of backers, but never seems to actually succeed.

Here's another way of looking at it with a more conservative approach. Dollar cost averaging every month.

P1Y: -11%

P2Y: +72%

P3Y: +177%

P4Y: +307%

P5Y: 404%

P9Y: 5,920%

.. however you dice & slice it ... it still looks exactly like a classic ponzi scheme ... like NFTs , like the dot.com bubble ... all the way back across the midsts of time to the tulip bubble in Netherlands during the 1600's ...

And just like tulip bulbs, you will never ever convince some people that Bitcoin is a bubble. It's like a psychosis.

It'll be logarithmic curves this and linear regression that, dollar cost averaging and zooming out until you get the answers you want. I'm sure Bitcoin's -40% depreciation over the past 12 months is somehow just a sign of how strong and stable it is.

.. however you dice & slice it ... it still looks exactly like a classic ponzi scheme ... like NFTs , like the dot.com bubble ... all the way back across the midsts of time to the tulip bubble in Netherlands during the 1600's ...

It could be the must unique Ponzi scheme:

2011: Mt Gox hacked & BTC market-dumped to USD0.01--that was the entire ecosystem.

April 2013: BTC fell from $266 to $50 in a day.

Feb 2014: Gox declared bankruptcy. Everyone wrote BTC off leading to a -87% bear market (altcoins got rekt much worse & many died forever).

2016: ETH suffered DAO hack - bull run halted

2017: Bull market ends and BTC down over 80% for months. ETH 90%+

2020: Covid liquidity crunch.BTC fell 50% in a day, and most other cryptoassets fell much worse.

Jeepers, incredibly volatile. The lesson is, don't put all your money in this. Certainly don't leverage to buy any. Play money only!

I struggle with Crypto. As a store of value, it’s way too volatile. As a medium of exchange, it appears to be a solution looking for a problem to solve. Many comments from proponents appear to be ‘talking their own book’. I wish them well but not with my $.

Yep not with mine either, the good times for Crypto are over.

I don’t see any long term future either, but I think there is a fairly good chance of another bounce maybe even to the 100k zone. So I am considering investing for the first time. But there is also a good chance it’s too late and there aren’t enough investors left; even the ones that have made crap loads seem to be abandoning it.

That'd be speculating, not investing ... ;-) ?

... exactly ... it's only marginally better than taking your cash & heading down to the casino ...

“the good times for Crypto are over.” - I’m sure that has been said before.

https://www.taxpayers.org.nz/taxpayers_union_curia_poll_may_2022?utm_ca…

National ACT govt leads

Should be an interesting election. A while yet though.

... wondering if this poll will prompt Robbo to throw some extra sweeteners into next week's budget ... Some pork barrel politics to appease the poor & downtrodden on Struggle Street , NZ ... which is most of us , now ...

I went out a few places today and there were no signs of struggle street or inflation. Roads were packed, shops were packed, I think I’ve seen quieter days leading up to Christmas. Recession it was not.

yeah it was really busy in Auckland today, some of that seemed to be sports-related (we were part of the masses taxi-ing our daughter around Auckland for football)

Sylvia Park was packed, not that I know what it is normally like as I avoid malls like the plague (and incidentally I’m sure there was a lot of plague spread there today)

Interesting isn't it. I guess while unemployment is still low...it feels a bit like the 'final hurrah' to me, in terms of the consumer economy.

Maybe, for now, it's bigger ticket items that will start to suffer (cars, boats, houses), less so 'coffee and cake' at a cafe.

Went to bunnings midday and it was empty, first time I've seen it so quiet... Roads were certaintly busy though.

2) The critical importance of improving supply chain resilience.

The lack of NZ supply chain resilience is symptomatic of our political leader's inability to plan for any long-term strategy to improve and protect almost anything you like. Education, health, housing, environment, immigration, disaster preparedness, etc.

For example, how other countries which similar issues to ours prepare themselves, within four months after the Japanese Tsunami, houses were being shipped from Canada to Japan to help Japan rebuild. Meanwhile, in NZ years after our earthquakes people were still bogged down in bureaucracy on getting simple repairs made.

And the reason Japan could respond so quickly is that 3 decades prior to that, they actually had the foresight to say, that being an earthquake risk country they could get a natural disaster one day that was so strong that they would not be able to respond with local resources. What do you do when your rescuers need rescuing?

So they went out in advance and established supply chain links that enabled immediate use in times of need without the need for any emergency bureaucratic delays to be activated.

In the Japan and Canada example, they had already preapproved Canadian housing as meeting any Japanese regulations and had established the trade route in 'peacetime' so it was well-practiced and easy to scale.

Tellingly, in seeking out partner countries to establish building and supplies from, they excluded NZ because they don't rate our timber, our build methodologies, and our ability to actually deliver. Sound familiar?

Excellent and important post, especially with regard to lack of supply chain resilience and our earthquake risks.

"Meanwhile, in NZ years after our earthquakes people werexxxx are still bogged down in bureaucracy on getting simple repairs made."

Fixed that for you!

My Food Bag : The NZ media have leapt to the defence of celebrity cook ( she's not a qualified chef ) Nadia Lim , after the misogynistic & racist comments by DGL's CEO , Simon Henry ... and rightfully so ... his comments were offensive ...

... but ... Ms Lim walked away from MFB last year with a $ 14 million profit ... the insiders bailed out of the company they founded ... listed it on the NZX at $ 1.85 per share ... fund managers raved over it , brokers lauded it ... joy ...

Except , 12 months later they're trading at just 79 cents ! ... you'd have lost less if you'd bought Bitcoin ... 57 % down ... care to comment , Nadia ?

My son and his flatmates were buying the 'specials' (50% discount) offering at these types of companies were offering against each other as they were each trying to buy market share and take advantage of the Covid lockdown orders had on home delivery.

The kids had worked out that at a 50% discount it was cheaper and easier given lockdown to do this, and they got something like 4 months of meals at this discounted rate.

Everyone knew, including the companies, that this would end one day, with the price having to go up, Covid stopping, and really just the novelty wearing off.

But in the meantime, it gave the likes of Food Bag the branding to show huge growth. Looking especially good just before an IPO. It was the equivalent of salting the mine.

I wonder how many shareholders actually use the service. Maybe they could eat their way back into profit.

... it demonstrates how piss weak the NZX is ... they should never have allowed this IPO to proceed ... MFB clearly stated that 88 % of the funds raised ( well over $ 300 million in total ) would go to insiders , who were cashing out , and walking away ... my money bag ..

A mere 12 % of the IPO money was retained within the company for operations ...

... shame on you , NZX !

For me, these businesses were typical 'Bubble Businesses'. Absolute luxuries, really.

I tried them a few times, the food was quite good, but nothing to write home about in my opinion.

Yes, many of us live very busy lives - my household has an at-times chaotically busy life - but it's not too hard to be organized with meals. Cook some bigger ones, freeze leftovers, etc etc.

But still enjoy an occasional takeaway. We paid $55 for Indian takeaways the other day, there was more than enough sauce in the curries to keep for the next day, so $55 across two days isn't too bad.

... bang for buck , the local fushnchup shop is best ... most have a great range of options ... and , the hamburgers slam Maccas out of the park for size & flavour ...

Can’t beat a good shark and tatties

... if money is no object , its Indian takeaway by a country mile ... so freaking good ...

Occasionally the wife tells me to go to Hell ... best pizzas on the block ... pricey , but fantastic ...

haha

I usually tell my wife to go to Hell, she likes it but not as much as me.

I guess I am a worse sinner.

Whereas DGL founder Simon Henry listed his company and reinvested all of the capital raised into his firm. It quadrupled in value in a year.

https://i.stuff.co.nz/opinion/128624197/how-the-media-stoked-the-simon-…

... thankyou ... exactly my point ... if you'd popped some money into DGL , you'd now be 8 times better off than someone who invested the same amount in MFB at its IPO ...

Simon Henry's cleavage ain't as spunkily hot as Nadia's ... but , he makes you money , lots of it ...

... " what're you want New Zealand ... the money .. or the bag ? " ... too good ...

The small thinking always went for the bag - the unknown is always more exciting than any given, even if the given gives you more.

That's how casinos work.

My Fun Bags?

... if they're full of money ... $ millions of it ... if you've taken the dosh , and run for the hills ...

Yup ... they're " fun bags ""... sorry Pamela Anderson , but the very best real fun bags are full of money ... not silicon ...

Ah well, as with all pyramid schemes, there's those at the top who kicked it all of will have done very well out of it all

It's worrying if financial assets as volatile as crypto starts operating counter to the generally accepted notion that it has "little correlation to the value of other investment types, like shares."

The crypto bods will hate it (and I get why) but it adds fuel to the idea that it should be better regulated/controlled.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.