Finance Minister Grant Robertson acknowledges the Reserve Bank’s (RBNZ) bond-buying, or quantitative easing, is likely to come at a larger cost than expected at the start of the pandemic.

The Treasury last week estimated rising interest rates would see the cost of the Large-Scale Asset Purchase (LSAP) programme hit $5.1 billion. It was initially expected to be cost-neutral.

Robertson said that when the Crown agreed to indemnify the RBNZ for losses incurred by the programme in March 2020, he was aware of the risk involved. But he decided it was a “risk worth taking”.

He wouldn’t say whether he would support using bond-buying in the future, should a change in economic conditions prompt the RBNZ to decide to go down this path again.

Background

The LSAP programme saw the RBNZ buy $53.5 billion of New Zealand Government Bonds on the secondary market between March 2020 and July 2021. It did so to lower interest rates to boost inflation and employment, as well as to support smooth market functioning.

The programme was always going to come at an upfront cost to the Crown. This is because the RBNZ would be buying government bonds from banks and other investors at a time bond yields were falling. Thus, the RBNZ would be paying a premium to effectively buy at the top of the market.

The Treasury estimated upfront losses of $7.2 billion would be offset by the savings the programme would deliver to the Crown’s debt servicing costs.

But as it turned out, the economy rebounded more quickly than expected. Inflation is rising and interest rates aren’t being kept at emergency lows for long enough for the Crown’s interest cost savings to fully offset the upfront cost of the LSAP programme.

The cost of the LSAP programme won’t be known until 2027, when the programme is expected to be completely unwound. But, the Treasury expects the net cost to land at around $5.1 billion. See last week’s story for a more detailed explanation.

While this is a significant sum, it doesn't consider the broader economic impacts of low interest rates, including how they supported economic demand, which boosted the government's tax take and the value of its assets (financial investments, land, buildings, etc).

The difficulty is knowing the extent to which other less costly tools used by the RBNZ to lower rates supported the economy versus the LSAP programme.

Risks were known

Robertson acknowledged that when he agreed to backstop the RBNZ, in respect of LSAP programmes losses, in March 2020, the expectation was for the economy to recover from Covid-19 slowly, and for interest rates to remain lower for longer.

Indeed, the LSAP programme was launched at least in-part due to the fact the economic outlook was as dire as it was uncertain, and there wasn’t much room to cut the Official Cash Rate without going into negative territory.

However, the Treasury in late-January 2020 warned Robertson bond-buying would make the Crown’s balance sheet more exposed to rising interest rates.

The Treasury provided a “red” (rather than “orange” or “green”) level trade-offs warning of the potential for the RBNZ to suffer “significant financial losses”, depending on the amount of bonds it bought.

It noted the RBNZ's Monetary Policy Committee isn’t formally required to consider “fiscal risks” associated with bond-buying. It just needs to "have regard to the efficiency and soundness of the financial system".

Furthermore, the Treasury warned bond-buying could “disproportionally benefit” those the RBNZ buys bonds from - IE the banks.

“Risk will also depend on whether the Bank has a credible exit strategy,” it said.

“To date, no central bank that has undertaken large scale asset purchases has effectively unwound their purchases.”

The RBNZ is endeavouring to unwind the LSAP programme by selling down its bond holdings between July this year and 2027.

Asked whether he still stood by his decision to support the LSAP programme, Robertson noted he didn’t have the “luxury of hindsight” in 2020.

“We had to take the decisions we did with the information we had at the time. I’m not going to change my thinking on that,” he said.

Wealth inequality

Robertson also noted, in the same exchange he had with interest.co.nz on the LSAP programme, that house prices had risen more than expected at the start of the pandemic.

The Treasury's January 2020 advice warned of this eventuality.

It gave a red level warning that bond-buying “may increase wealth inequality by more than conventional monetary policy by raising asset prices more directly”.

“On the other hand, a stable macroeconomy supports those at the edge of the labour market,” the Treasury said.

Like fiscal risks, the Treasury noted the RBNZ isn't directly responsible for dealing with the distributional impacts of its monetary policy, provided it has regard to the "efficiency and soundness of the financial system". See this story from February 2021 for more on this issue.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

38 Comments

Yes but what is a "red level warning" from Treasury to a professional and long-time politician? Given the deliberate hollowing out of competence at the RBNZ (covered here at Interest), Treasury is probably the last place in government where actual financial analysis is done.

A pity they could not follow "expert advice" when it came to finance, would have saved every man, woman and child a $1,000.00.

It's not like this government cares for advice that doesn't agree with their POV anyway

Bond - Jacinta Bond.

If you think that Treasury still has high levels of economic and financial acumen then sadly I have news for you.

https://www.nzinitiative.org.nz/reports-and-media/opinion/the-treasury-…

https://thespinoff.co.nz/politics/07-06-2019/the-rot-at-treasury-starte…

Note: from personal experience in my economics and finance masters class (2016) 5 grads went to Treasury. All have now left. They all cited the lack of economic expertise. Unfortunately this means that those who actually have the skills necessary to undertake the analysis end up getting overloaded with too much work. Inevitably as a result they quit for higher pay and better work-life balance in the private sector.

I am not surprised. Those leavers will benefit from contracting their skills back to the Treasury or join a consulting firm that does the same.

It is common among public sector entities to have layers of overpaid bureaucrats with catchy job titles (project/programme/portfolio managers) who outsource work that is meant to be done internally.

The QE (LSAP) programme across the world drove money into other financial assets - shares and other equity etc - inflating their value considerably.

A lot of people do not realise that Govt owns a LOT of financial assets - student loans, debt securities, derivatives, shares, equity etc. So what happened when Govt started buying bonds in NZ? The value of Govt's financial assets increased markedly - from $232bn in 2020 to $285bn in 2021. A cool $53bn gain. The latest (January 2022) figures suggest that these gains have been at least sustained. Obviously Grant and Treasury do not talk about how 'successful' their portfolio has been in the round - but I would expect the next budget to be fairly big on the use of Govt's embrassing riches to invest in infrastructure etc - see wind farm announcement yesterday.

Also worth noting that Govt financial assets last year were $100bn more than their financial liabilities... but people still fret about Govt 'debt'! We should be asking why Govt is hoarding money when the country is falling apart.

The answer is, so they can spend big at the next election. They don't seem to give a flying f about the people they are supposed to represent it seems, its all about retaining power. Watch the next election lolly scramble, it will be epic.

.... it'll be a Robbo party of " packages " dished out to the faithful... unless of course , Jacinda gets lucky , and a new variant of Covid emerges ...

It's better to be spending that on infrastructure etc. rather than us simply handing more money to speculators as we've been doing for the last few years.

Exactly that.

That's right, but the population needs to start demanding changes to the systems that such a change would entail. Changes to RWA for banks, severe shifts in taxation policy for central government.

But they don't. Instead the general populous say "Me buy 2 house, me get rich. Anything threaten, vote out". As long as the idiocy persists, we won't get anything but lolly scrambles which quickly filter up to the already wealthy and more speculation.

Certainly worth it for the banks. Cheers, Robbo. There'll be a seat on the board waiting for ya once you've had enough of politics.

............................ or politics has had enough of you

"Personal reasons".

.

Come on Robbo don't give us this 'in hindsight' bullsh*t, you ignored all the warnings at the time and went all out stupid... There needs to be some accountability here, surely.

From the same government who did triple backflips just to avoid admitting that living costs had increased?

Not under this lot, sorry.

But at least they apologised this time - an apology everyone will be paying for in future generations,along with their massive spending plans in the coming budget

... they're taking the Will Smith approach ... if there's no way you can blame someone else , if the exit doors are locked , if the cameras are rolling and you know you're as guilty as sin .... .... say , " oops , I'm sorry ! "

Absolute last resort , of course ...

We have for the last decade plus being living at a cost we bank on handing to the next generations. We just tell ourselves it's our investment nous, not the fact we've been using policy to live beyond our means and pass huge mortgage debt to the next generations.

Might be nice for the young'uns to actually get some infrastructure rather than just existing stock of houses for ever higher prices as we extract their wealth.

"Furthermore, the Treasury warned bond-buying could “disproportionally benefit” those the RBNZ buys bonds from - IE the banks."

This is by no means certain - the bonds were bought on the secondary market, where most bonds at the time were owned by investors and non-residents (rather than our resident Aussie / NZ banks).

When RBNZ buys $200m worth of bonds on the secondary market, this happens:

- RBNZ credit the settlement account of, say, ANZ with $200m

- ANZ credit the account of the bond seller with $200m (this does not change the settlement account balance - the money doesn't 'move')

- The bond ownership transfers to RBNZ

At the end of the deal:

- RBNZ has $200m worth of bonds and $200m of liability sat in ANZ's settlement account (their net worth has not changed but their balance sheet is inflated on both sides)

- ANZ has $200m liability in the bond seller's account and $200m of asset in its settlement account (net worth unchanged, but balance sheet inflated)

- The bond seller has $200m less bonds and $200m of 'cash' in their account (net worth unchanged but now they need to buy some more financial assets to make money - hence the inflation of shares and equity)

- Crown debt is unchanged - their liability in bonds has been swapped for a liability in the settlement account of ANZ

- RBNZ pay OCR interest to ANZ on the balance in their settlement account and the Crown pays interest on the bond to RBNZ. Any surplus generated (around half a billion so far) goes back to Treasury

- If the value of the bonds drops below what RBNZ paid for them, then Treasury owe RBNZ the difference - this is the $5bn loss being discussed. If the bond market picks back up again, this loss will reduce to nothing very quickly. Treasury forecasts are based on increasing interest rates into the medium-term, which is highly optimistic given the recession that is coming in late 22

Nice explanation! What would have happened if we replace ANZ with Treasury i.e. RBNZ would buy the bonds straight from the Treasury. No free cheap cash available for banks and investors to prop up shares and equity.

The RNBZ/Treasury can reduce their losses by not selling the bonds but to let them mature only. They are only sitting on the RNBZ balance sheet for longer than 2027 bur as you say 2027 is far away and we might experience some periods of economics mishaps which will reduce the OCR again.

Thanks. It took me months to work it out - always happy to avoid others having to do the same!

RBNZ used to buy bonds directly from Treasury exactly as you describe - it is how we financed the building of all of those state houses in the 1940s!

However, RBNZ and Treasury gave us a glimpse of how to do this more simply in March 2020 when RBNZ simply gave Treasury a temporary overdraft on the Crown Settlement Account (I think it was $10bn). This overdraft was not actually used in the end, but it would have been the simplest and quickest way for Govt to increase its liabilities ('debt') without having to give as much free money to investors etc. I say 'as much' because when Government spends $Xm, the Crown's Settlement Account is marked down by $Xm, and one of the commercial banks' settlement accounts is marked up by $Xm. RBNZ pays a bit of interest (OCR) on the balances in the banks' settlement accounts (but obviously less interest than it pays on bonds in usual times).

Finance Minister Grant Robertson acknowledges the Reserve Bank’s (RBNZ) bond-buying, or quantitative easing, is likely to come at a larger cost than expected at the start of the pandemic.

There was prior evidence elsewhere that LSAP (QE) failed to generate sustained economic growth - it should have been noted and acted upon.

{kind=link}

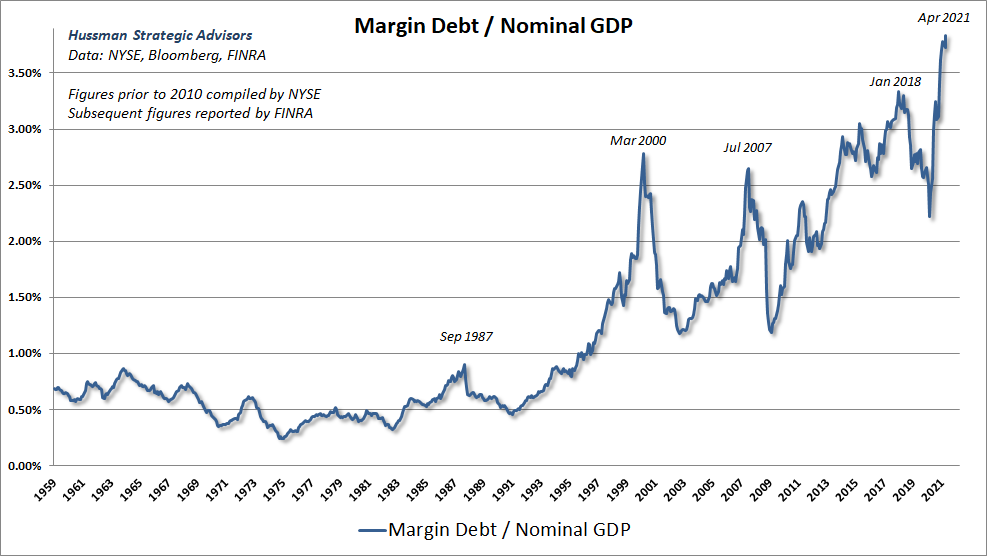

Policy makers sometimes flatter themselves with the idea that holding interest rates at untenably low levels makes it cheaper for borrowers to obtain funds. Unfortunately, it does so only by transferring income from people who are trying to save for the future. Replacing Treasury securities with base money may make savings more “liquid,” but it doesn’t suddenly make people abandon their retirement plans in favor of consuming today. Low rates also don’t magically create productive investment opportunities.

What economic activities suddenly become viable at zero interest rates that were somehow not viable before? Only projects so unproductive that any positive hurdle rate would sink them. The main activities that are encouraged by zero interest rates are activities where interest is the primary cost of doing business: leveraged real estate transactions; “carry trades” that employ enormous amounts of leverage to profit from small yield differences; and speculation on margin. Presently, margin debt as a percentage of GDP is at a historic extreme.

https://www.hussmanfunds.com/comment/mc210614/

{kind=link}

Exactly - study after study has shown that the cost of borrowing is a very minor consideration for businesses when they invest in innovation, increasing productive capacity etc. Cheap credit just encourages speculators, share buy backs etc. Monetarism is so, so, very dumb.

The fact is the government and RBNZ has screwed it up, they knew the risk but didn't do any thing to manage it. If there were any intention to manage the risk, LVR would never be removed, Jacinda wouldn't stated she want to see small increases in houses prices in public.

"But he decided it was a 'risk worth taking'." I don't think he should be in the position to judge whether it was risk worth taking or not. The average New Zealanders should be the one to judge. Now because of their ultra loose monetary policy and removed LVR, housing price has been pumped to a ridiculous level, now we are facing the worst inflation in three decades and RBNZ couldn't meet their mandate to curb inflation due to house market is too big to fall, but I don't think they have any other choice rather than hiking OCR aggressively.

So let me ask this again, was it "risk worth taking"?

Increasing and decreasing the OCR obviously influences the price of housing because it limits the price that people can afford to pay for their precious bit of land and timber. The OCR also has a short-run effect on exchange rates, which can help with imported prices (a bit). But the idea that the low OCR caused consumer prices inflation or that high OCR will bring it down again is seriously flawed. Increasing the OCR will *increase* the cost of living for most kiwis - it's a really stupid thing to do when international factors and domestic profiteering are driving price increases. HIgher mortgage costs + higher cost of credit for businesses + increased price of imported goods + reduction in Govt spending = lower demand, higher unemployment, and a recession by the end of 2022.

As you infer, if we want to actually reduce the cost of housing, we need to constrain credit availability, and think about changes to our tax and policy structures to make housing less of a sure thing in the medium-term. If we want to reduce domestic inflation, we need to tackle the root causes that are within our gift - energy security, abusive market power of our duopolies, local govt funding (rates are a major contributor to cost of living) etc.

God I wish you were finance minister instead of the incompetents we have running the show... unfortunate that the political field is full of people who shouldn't be there.

Not arguing for their competence...but I'd love someone to point out a potential finance minister on the nominal Right of NZ's politics who would not have chosen to pump their portfolio house prices.

I'd have to get down to Simon Watts before you'd find someone with a background in finance/accounting who I would trust to at least understand the fundamentals or push back on the fantastical garbage the cardigan wearers spin when they want something.

I don’t agree. If interest rates are below inflation it’s going to still encourage being in debt and forget saving money, that’s going to result in runaway inflation.

My point is not that low interest rates are good, only that moving them under the pretense that this will solve the cost of living crisis, or reduce easy credit flowing into speculative bubbles is dumb. Our macroeconomic objectives can be better met through other means than waggling the OCR lever around.

I think reducing OCR to "boost" economy when it seems like to be in a recession is flawed. The idea to have more liquidity in economy available when businesses are struggling with their cash flow is good. However, in New Zealand's real life scenarios, when there is almost zero credits availability constraints on assets (here is houses), what it only does is to pump housing price which is not producing any goods and products except booming constructions business. When globalisation gets impact by covid and war, it's almost certain that we will have inflation as the productive industries have been not as invested as it should've been, therefore not being productive.

Yeah, I agree that increasing OCR wouldn't be as effective as we wanted to deal supply push inflation, but it is necessary to do so to remove excess liquidity from the economy and to strength our NZD to help with imported prices as you mentioned.

Completely agree that reducing the OCR to boost the economy (and increasing it to slow things down) is flawed. Like giving someone who is falling down drunk a hammer and telling them to just gently crack a nut.

I think there are better ways than increasing OCR to reduce the flow of easy credit into non-productive endeavours. When the US Fed banks were in their prime, they focused regionally on the quantitiy and quality of credit - basically ensuring a flow of credit into businesses and projects that increased local productivity and quality of life, and stopping (literally) credit being used for speculation. Bring back those days!

Jfoe has got it right about how QE worked. It should have been a simple case of Treasury issues $50 billion of new bonds at par ($100) and the RBNZ buys them (via the banks who clip the ticket) at a similar price. With rates rising, those bonds are now worth $5 billion less, say $95. So that's a $5 billion book loss to RBNZ. But the trade is easily reversed: Treasury buys back bonds it sold for $100 at $95,realizing a $5 billion profit. That profit is transferred by an inter-government accounting entry to the RBNZ as per the indemnity the Treasury gave them. Hence no loss at the government level. A slight problem is that the Treasury's debt issuance is valued at historical cost. So the banks sold *old* issues the the RBNZ, bonds that are now worth say $107 but are on the Treasury books at historical cost i.e.$100. Hence, as Treasury said recently "the LSAP program cost $7.2 billion more than their value on the government balance sheet". Still, it's just an accounting issue. The bottom line is there is no loss when you take into account the $50 billion bonds Treasury issued at very low rates but weren't bought by RBNZ. They are on Treasury books at $100 but are worth a lot less, say $95. If Treasury "marked to market" they would show a $5 billion book profit.

They are great points! Well explained.

"...responsible for dealing with the distributional impacts ..." nobody is responsible for these it appears, least of all any government department, or the government itself.

Never accept a mistake in politics.

Labour has lost touch, the same way national had after three terms - power corrupts and for Labour .......

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.