A.M. Best has revised the outlook of Tower’s “under review” credit ratings from “developing” to “negative”.

The shift relates to the Financial Strength Rating of Tower Insurance Limited (TIL), and the Long-Term Issuer Credit Rating of both TIL and its parent Tower Limited (TL).

A.M. Best says its move follows the Commerce Commission last month preventing Vero from taking over the New Zealand insurer.

“The negative implications status reflects TL’s relatively weak balance sheet strength for its current rating levels. A.M. Best’s concern, however, is offset partially by management considering a capital raise to strengthen the group’s consolidated capital position,” it says.

“The ratings will remain under review with negative implications pending further discussions between A.M. Best and TL’s management team related to its capital-raising initiatives.

“Downward rating pressure could result if TL fails to improve its consolidated capital position to a level more supportive of the current ratings.”

A.M. Best put Tower's credit rating under review in February, when the insurer announced its proposal for Canadian giant, Fairfax Financial Holdings, to buy all its shares.

TIL has a Financial Strength Rating of A- (Excellent) and a Long-Term Issuer Credit Rating of a-.

TL has a Long-Term Issuer Credit Rating of bbb-.

Tower Chairman Michael Stiassny says: “The Tower Board is pleased that A.M. Best has maintained Tower’s A- rating, and as previously indicated, [Tower] is considering conducing a capital raise to accelerate the transformation of the underlying business and ensure the long term sustainability of Tower.

“Tower retains an adequate and stable capital base and continues to improve the underlying business.”

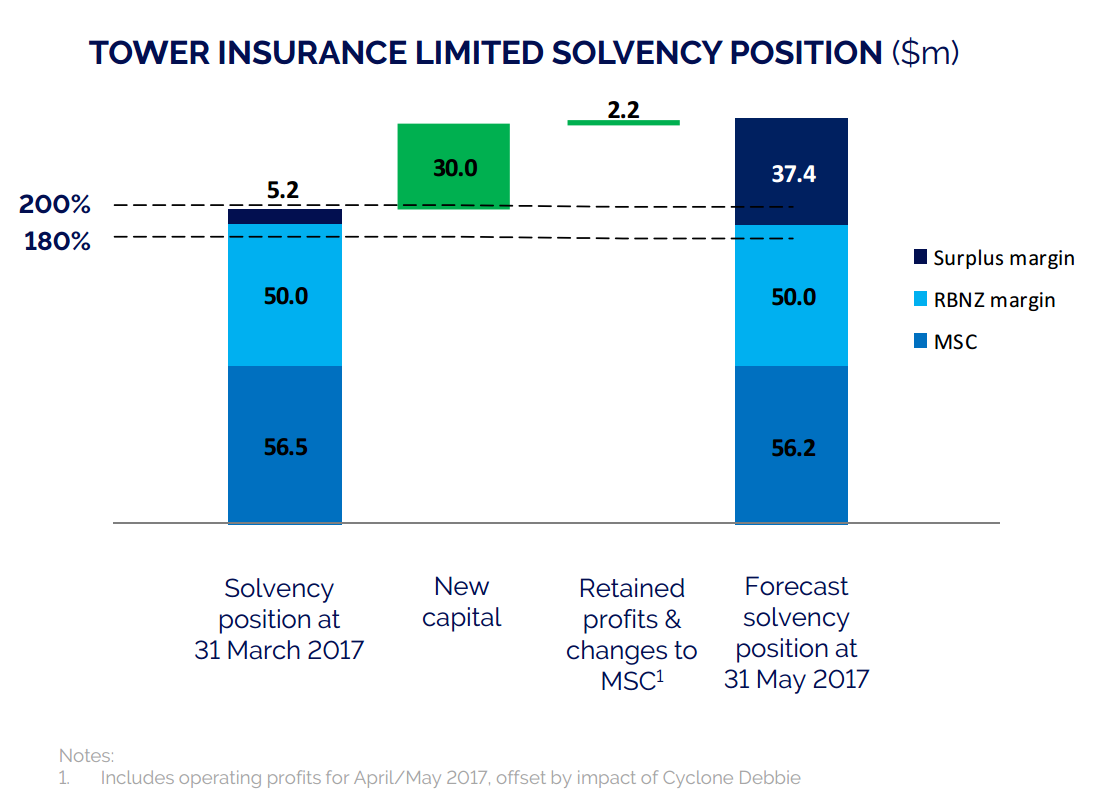

Tower, in its half year results released in May, revealed it had drawn down $30 million from a $50 billion BNZ loan it had taken out, as it came within $5 million of breaching the Reserve Bank's solvency requirements.

7 Comments

Raise capital. It would in my opinion be of quite some nerve for this to be thought of being successful in the form of an IPO. Where to then, institutions, government agencies? How much liability is the tax payer already exposed to by shares held by the latter in Tower.

With apologies to Yogi Berra, it's like déjà vu all over again.

The corpse of Tower continues to be wheeled about as though it's Weekend at Bernie's.

I guess the Snouts have decided that the trough isn't quite dry yet.

so if tower collapses and the crown steps in, will they call in the CC to ask did they not kick the tires and see 3 flat and the last leaking,

and ironically if it fails that will leave one player with huge market share

CC doesn't have to analyse in depth the viability of a company when deciding whether to allow a takeover. That Tower was meeting (just) its solvency requirements and was the subject of takeover bid, is sufficient for an assumption to be made.

This artificial construct allows them to take a short term stance and avoids the need to consider the likely trajectory of the business should the takeover be denied. If that business subsequently fails, CC is able to play Pontius Pilate; the subsequent crucifixion of creditors and claimants not its concern.

Of intrigue in this case are comments from CC that Towers business strategies and recapitalisation plans provide optimism for believing it will remain viable as a stand alone entity; suggesting CC carried out research on the company and, by implication, factored this in to their deliberations on whether to allow the buyout. Anxious Canterbury EQ claimants will be reassured.

Hmm I recently brought a home, having to organise house insurance I discovered that Tower was the worst provider out of the bunch of crooks!

They issued me with an ultimatum they were not going to provide house insurance to me unless I took out additional coverage like contents and car. They told me it was necessary because I live in the lower north island apparently too close to the South Island for their liking. So I hung up on the over priced quotation provider & employed the services of a broker for free lol. Hence now I'm paying a low premium with maxi cover from Vero. So tower is trying to pass their failures onto customers but it just doesn't fly!! PS don't try to pin South Island earthquakes on me buddy!!!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.